CA - Slate Grocery: 10% Yield With An 80% Payout Ratio What's Not To Like

2023-10-12 14:09:05 ET

Summary

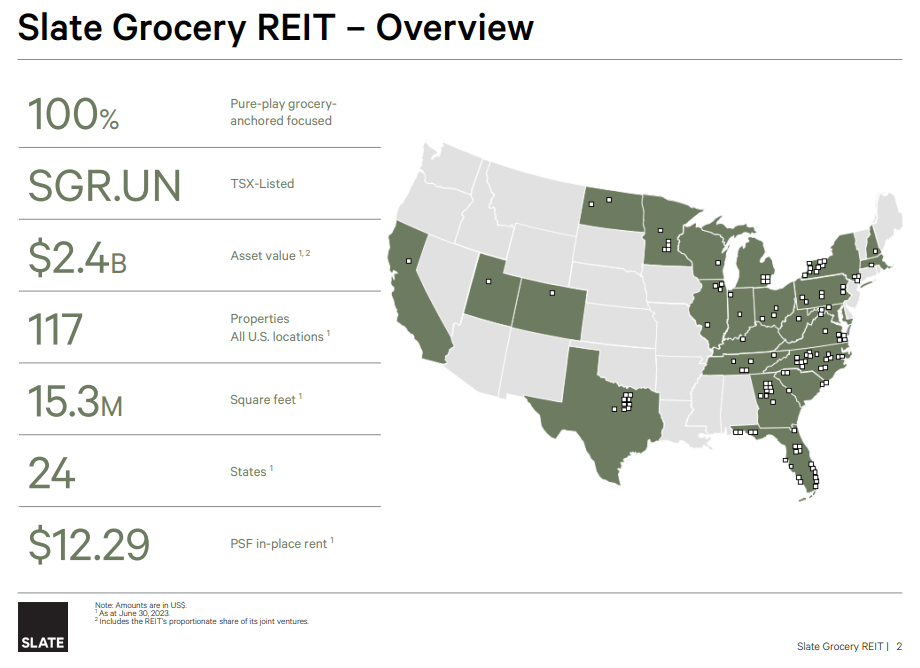

- Slate Grocery REIT, based in Canada, owns a portfolio of 117 grocery-anchored properties in 24 US states.

- The company focuses on properties that are anchored by grocery stores, which provide stability and consistent foot traffic.

- We examine this 10% yielder and give you our take.

Headquartered in Canada, Slate Grocery REIT ( SRRTF ) ( SGR.UN:CA ) ( SGR.U:CA ) owns a portfolio of 117 "grocery-anchored" properties, comprising over 1,800 leases. The properties can be found in 24 of the 50 US states, with a higher concentration in the sunbelt region.

{kind=link}

So this is a Canadian trading REIT, that has no exposure to Canadian assets.

A quick note on the different trading symbols is appropriate here as well. In Canada, Slate Grocery trades under

1) SGR.UN:CA-which is the Canadian dollar quoted symbol.

2) SGR.U:CA-which is the US Dollar quoted symbol. All discussions below refer to US dollars.

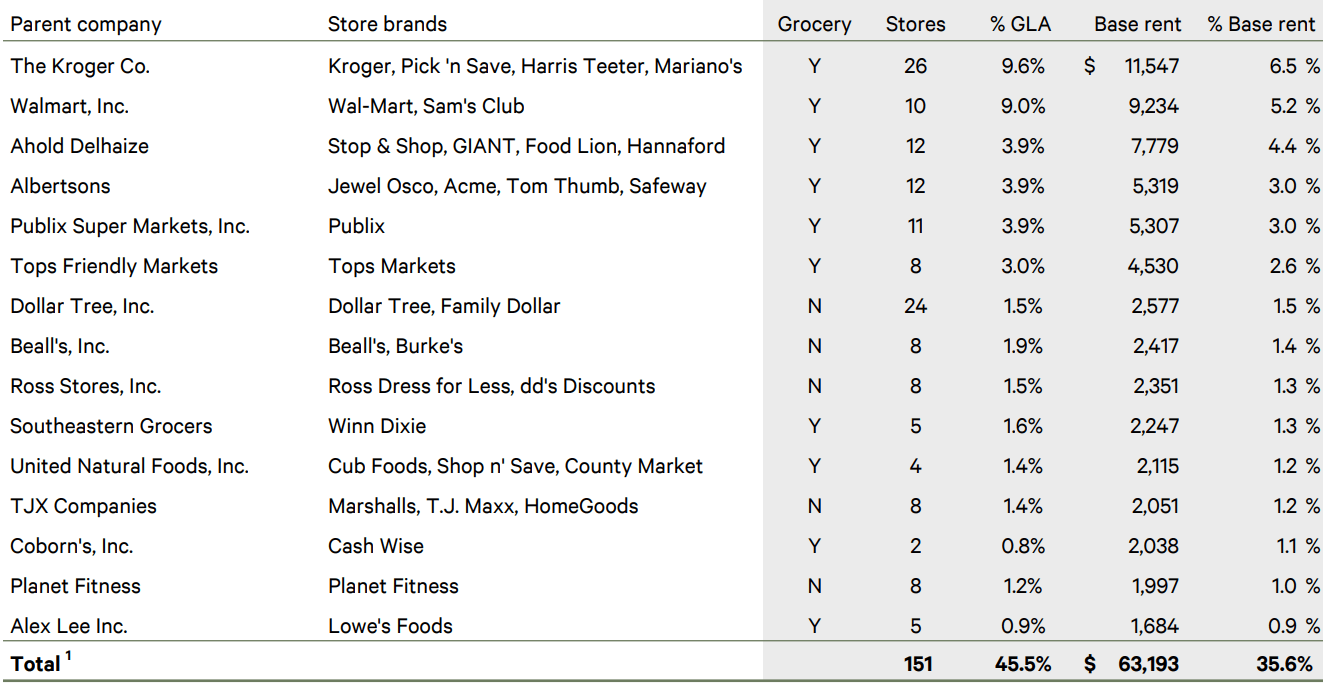

A grocery-anchored property is one where the majority of the leasable space is rented by a large grocery store, with smaller tenants littered alongside it. In Slate's case, two grocery giants, The Kroger Co. ( KR ) and Walmart Inc. ( WMT ) are the top-2 tenants, occupying close to a fifth of the gross leasable area and accounting for over 11% of the base rental revenue.

{kind=link}

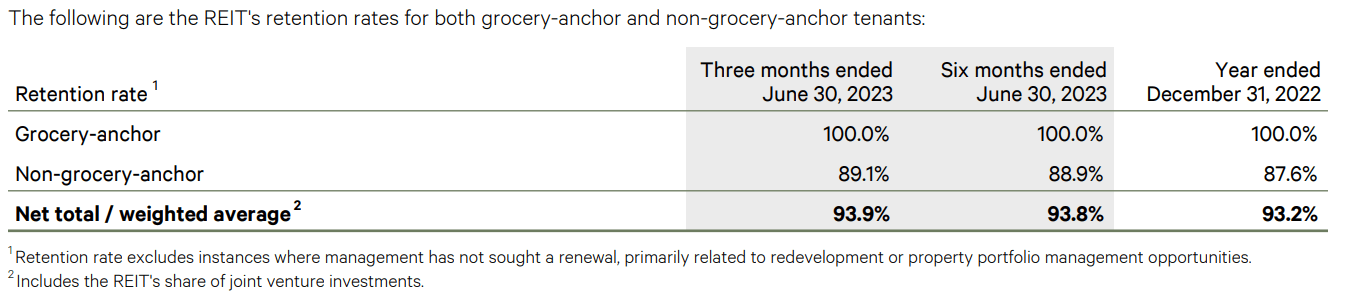

At June 30, 2023, the portfolio was valued at $2.4 billion and spanned around 15.3 million square feet, 93.9% of which was occupied. This was a slight improvement over the Q1-2023 and a 70 basis points improvement over the end of last year.

{kind=link}

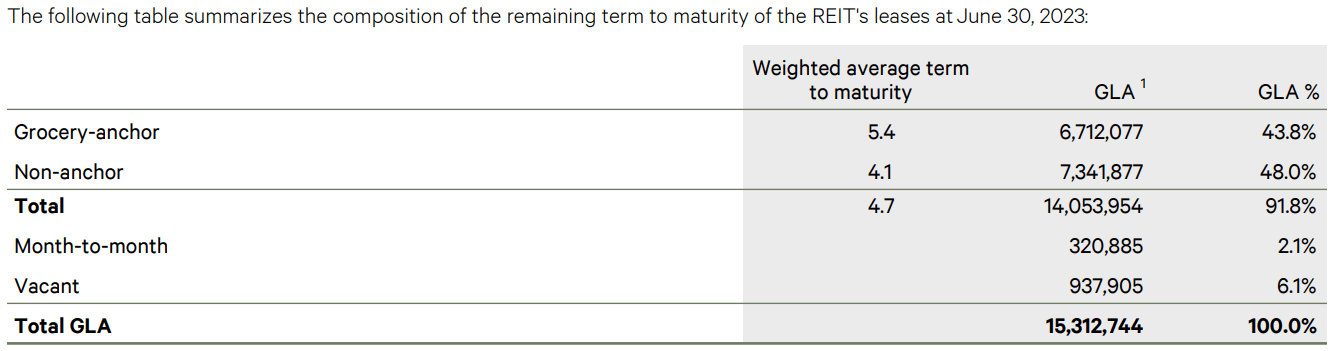

With the occupancy of the grocery-anchored tenants running at 100% like clockwork, all of the improvement has come from the non-grocery-anchor leases. The term to maturity is also higher for the grocery-anchored tenants. On the whole, the portfolio weighted average term to maturity at June 30 was 4.7 years.

{kind=link}

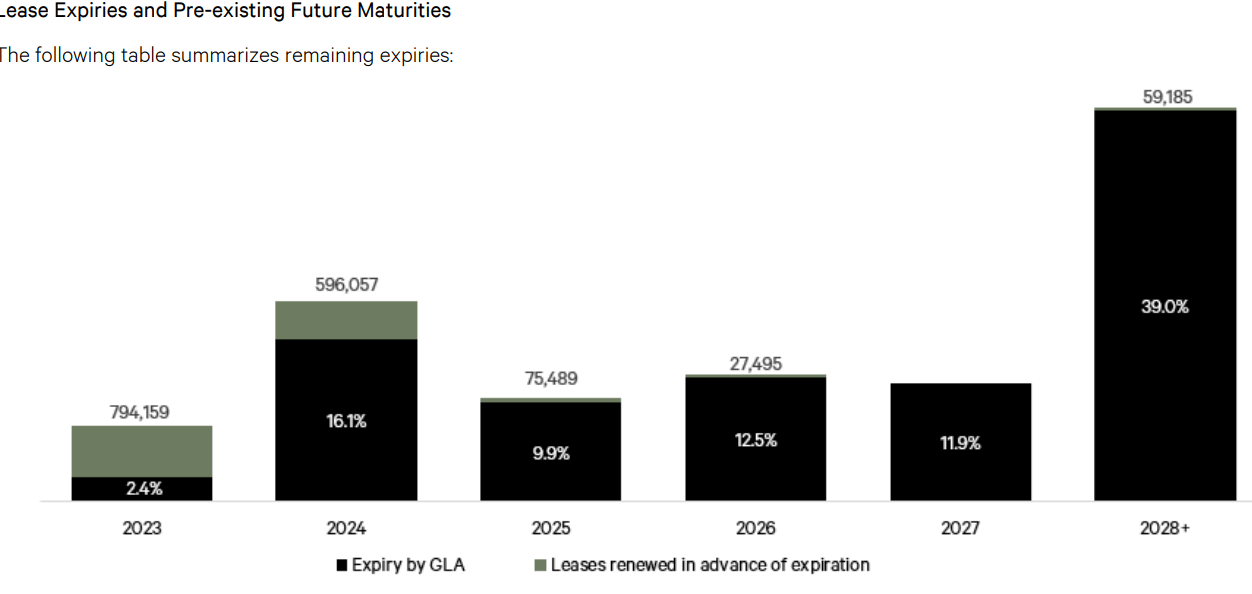

At the end of Q2, Slate had already taken care of more than half the leases that were coming up for renewal in the second half of the year. What remained to be renewed related to their non-grocery-anchored tenants and constituted around 2.4% of their portfolio.

{kind=link}

2024 has 16.1% of the REIT's portfolio coming up for renewal, a little more than half of which is for grocery-anchored tenants. If the 100% retention record continues unabated, they can concentrate on the 7.8% of the renewals relating to the non-grocery-anchored tenants. Slate's policy is to "lease to high-quality tenants in well located centers typically below the average market rent for U.S. strip centres, allowing for increased value in the portfolio through rental rate growth". We can also see this in action for the last several reporting periods, where the in-place rent has had a gradual increase.

{kind=link}

Almost all of Slate's tenants have net-lease agreements, which allows it to recover majority (if not all) of the operating expenses pertaining to the properties. This helps them have a consistent net operating income or NOI and makes them relatively less exposed to the vagaries of inflation.

{kind=link}

Our protagonist is managed by Slate Asset Management (Canada) LP, that also holds a 5.6% interest in the REIT.

Slate pays a monthly distribution of 7.2 cents, with the last increase coming in December 2019. At the current price, this grocery centered REIT yields its unitholders a cool 10.5%.

We will note here that the distribution was maintained through COVID-19.

Q2-2023 Results

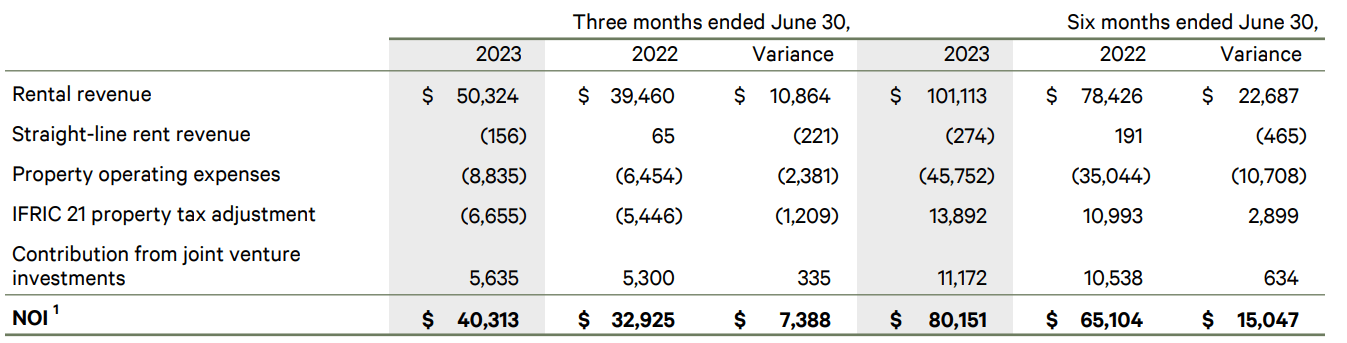

There were 14 grocery-anchored acquisitions and increases in rents on renewals and new leases, which drove Slate's revenue higher by a whopping 27% on a year-over-year basis.

{kind=link}

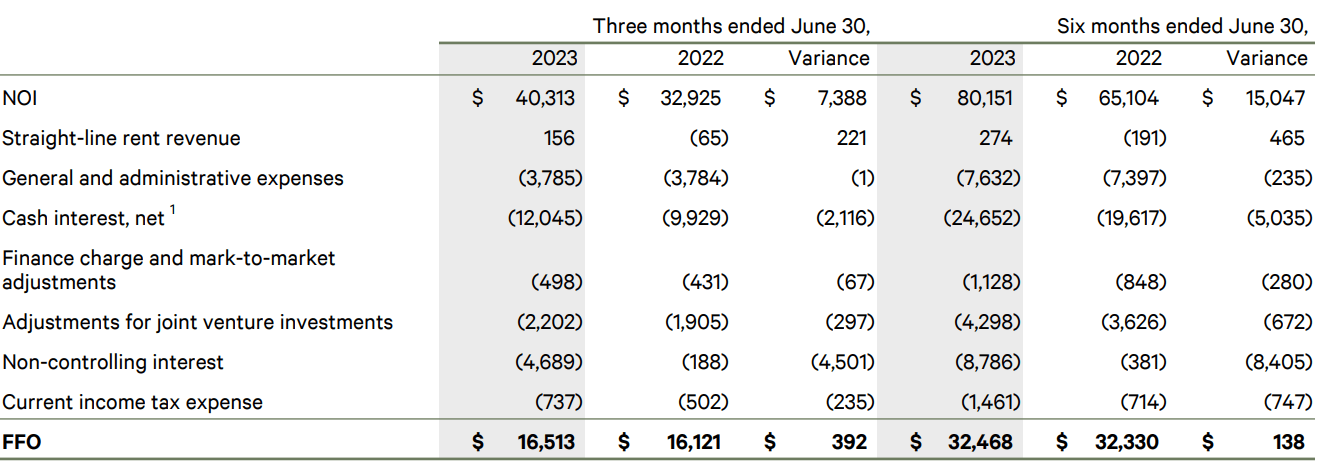

Some of this increase was absorbed by higher expenses, but most of it did trickle down to the NOI, which was higher by 22% compared to Q2-2022. Interest expense played a spoiler though, allowing the FFO to retain only a fraction of this revenue/NOI party. Nonetheless, the Q2-2023 FFO beat the comparative quarter by close to 4%.

{kind=link}

The FFO per unit also increased from 0.26 cents to 0.27 year over years, resulting in around the same increase as the total amount.

Interestingly enough, this expansion was debt fueled and funded and the last major share offering was in 2021. Slate actually bought back a small number of units in 2023 for an average price of $9.69, well under its internally calculated net asset value of $14.24.

This was reflected in the lower FFO payout ratio in Q2-2023 compared to the prior year.

{kind=link}

Debt

One of the major issues in investing in any REIT today is the fallout from higher interest rates. On the Canadian side, most REITs have been extremely blasé with their debt maturities. We saw NorthWest Healthcare REIT ( NWH.UN:CA ) go into 2023 with zero give on that front and they cut their distributions . We saw Artis REIT ( AX.UN:CA ) do the same and while they have not cut, their FFO payout ratio has basically doubled . Dream Office REIT ( D.UN:CA ) is now a few weeks away at best from chopping their distribution .

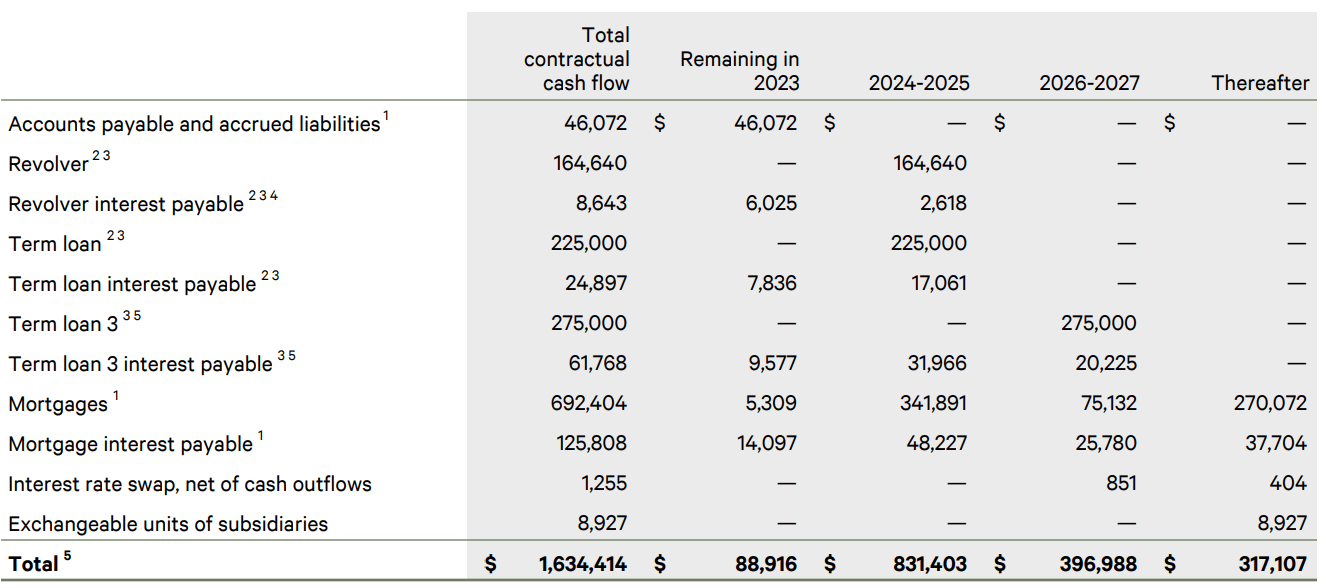

Slate Grocery is a bit better balanced here for 2023 with minimal maturities. But 2024 and 2025 have close to 50% of the debt coming due.

{kind=link}

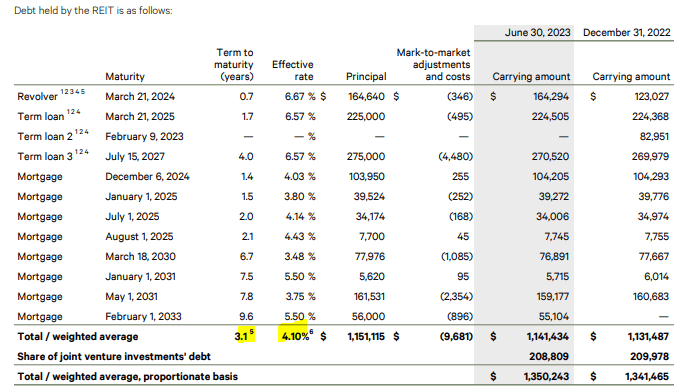

The picture above does not give the weighted average interest rate or term maturity, so we are giving you the next one for that.

{kind=link}

There are 6-month extension options all over the place and if exercised they would push the weighted maturity higher. Investors might be tempted to think that the other good aspect here is that some of the front line maturities already bear a decent interest rate, so the jump would be less. But that is not accurate as the floating rates are mitigated with interest rate swaps currently. So when that loan comes due and the swaps mature (2.4 year weighted average as of Q2-2023) there will be a big jump. As of Q2-2023, interest costs were up about 20% versus last year.

Valuation & Verdict

Grocery anchored locations are generally more resilient. We have also seen a drop off in retail supply in the US for a few years now so the current locations are doing better. The large amount of inflation we experienced has also helped with nominal revenue changes and help the landlord with rent increases. The REIT has a solid yield and it is trading at a good discount to NAV. That NAV itself is based on realistic cap rates.

{kind=link}

So there is a good deal going for the REIT.

The debt maturity profile still requires for there to be a break in the interest rate cycle for the company to do well.

{kind=link}

2.1X interest coverage is something you really don't want when you have a weighted average debt maturity on the low side. While some may brush aside these fears, do keep in mind that this is the asset management team leading Slate Office REIT ( SOT.UN:CA ) that did a dance with 12X debt to EBITDA and is headed right into the abyss. We are giving this a pass as well.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Slate Grocery: 10% Yield With An 80% Payout Ratio, What's Not To Like