SLCA - Smart Sand: An Underfollowed Gem

2023-06-13 15:58:04 ET

Summary

- Smart Sand, a micro-cap proppant company, reported stronger than expected 1Q23 results with a 98% increase in revenues compared to 1Q22.

- Conservative 2Q guidance stalled a rally on the strong results.

- Meanwhile, the balance sheet is strong, and the company bought back 11% of outstanding shares in the first quarter.

- Smart Sand is trading at 1.5x our conservatively modeled 2023 EBITDA estimate, much lower than peers. We expect growth in volumes, revenues, and EBITDA to eventually shrink this discount.

The Basic Story: We have written on Smart Sand ( SND ) a number of times, most recently here . In summary, they are a micro-cap (< $70 mm) proppant company with three mines (Oakdale, Utica, and Blair) shipping northern white sand, NWS, primarily into Appalachia (Marcellus and Utica) and the Williston Basin (Bakken). They acquired their third mine, Blair, in 2022, and it began shipping sand after the most recently reported quarter in May 2023 to Canada. With Blair, the company has a combined production capacity of 10 mm tons per year. Their mines have access to all four Class I railroads. They don't ship sand to the Haynesville for those concerned about reduced activity levels in that play. They do ship limited volumes to the Mid-Continent and into the Permian Basin, but for now these are not big markets. They have a modest but growing logistics service providing last mile services including sand inventory management and well site sand storage silos (SmartSystems). And they have a nascent Industrial Product Solutions sand segment. This ISP segment is small and not yet broken out in the financials. Their larger peer US Silica ( SLCA ), which we also have a position in, is seeing high demand (and rising prices) for industrial sand used for a widening variety of end purposes.

1Q23 was stronger than expected. Note that pricing and multiples in the following table provide a view of how they were as of the 1Q23 call, dated 5/9/23). Current estimates have risen and can be found in the table at the bottom of this piece.

{kind=link}

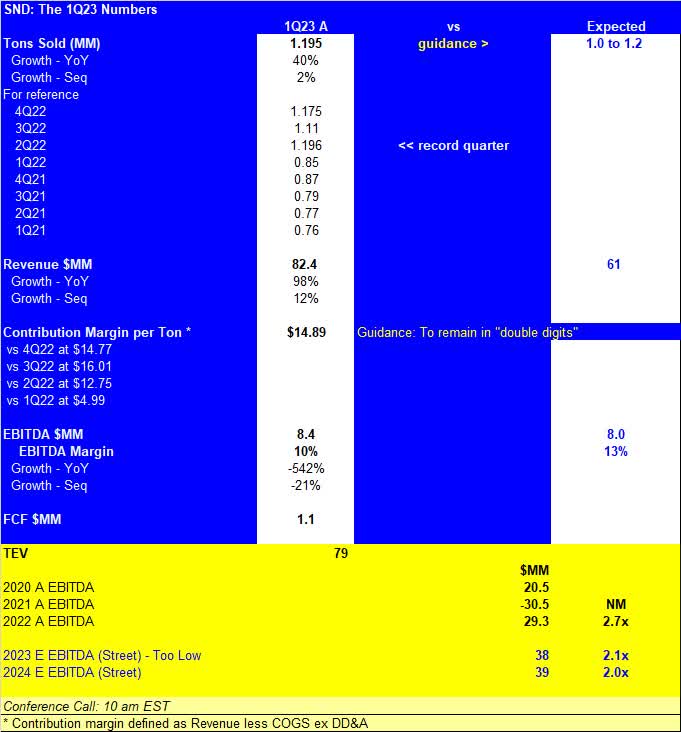

1Q23 Results Were Better Than Expected... The quarter saw them ship their second-highest volumes on record. Volumes came in at the upper end of their guidance for the quarter, at almost 1.2 mm tons, up 40% from year ago levels. This equates to 67% of operational capacity during the quarter (Blair was not yet online). The strong volumes along with higher sand pricing prompted a beat of consensus revenues by a whopping 35% driving revenues up 98% vs. 1Q22. Contribution margin (revenue less COGS net of DD&A) was a winter time healthy $14.89 per ton, which was in line vs. 4Q22 call color that CM would hold to double digits during the quarter despite seasonally higher production costs and elevated transportation costs. This compares to $4.89 per ton a year ago. Lastly, EBITDA came in at $8.4 mm for the quarter, just ahead of consensus. Note that TTM EBITDA is $39.6 mm, yielding a TEV to TTM EBITDA figure of 1.54.

... But The Short Term Outlook Was Flattish Due to Weather. Management normally does not provide guidance beyond the current quarter. On the 1Q call, they said to look for 2Q23 volumes in a range of 1.0 to 1.2 mm tons, which would be flat at best with 1Q23 volumes and was the same as 1Q23 guidance given on the previous call. Poor April weather served to blunt shipment guidance, and the market appears to lose interest during the call when they guided to this level of 2Q sales. Shipments from Blair mine began in May, and we are looking for a modest ramp this year and next, supported by their key initial customer in Canada.

Macro Recap: Marcellus sand demand continues to be solid and Smart Sand's output is underpinned by their multi-year contract with Appalachian heavy weight EQT Resources (EQT ). As of 1Q23, EQT was not looking to reduce activity stating they are " running two operating horizontal rigs and thus not contemplating reducing rig activity. But we have flexibility around our completion cadence as well as our choke management program". Data from sand tracker Spears & Associates shows US demand for NWS and in basin sand growing from 128 mm tons in 2022 to 140 mm tons this year, and it shows undersupply from in basin capacity in several key basins in the US and Canada. We have not seen a big slowdown in the most recent data for well completions, either. Anecdotal evidence from their peers, upstream names, and third-party sources all highlight robust demand and even with a modest pullback in US activity, sand remains undersupplied.

Z4 Thoughts and Estimates: After the quarter, we had a chance to catch up with management as a check on our expectations.

As with all of our chats with members of company management, we don't ask management teams to bless our numbers. And we don't focus on the next quarter. We are 2 to 3 year holders, at minimum, unless something really goes askew with a story or the macro backdrop. If a management team is willing, however, we do ask that they check our thoughts for reasonableness, and we've done that here.

Volumes. Management believes that over time, Blair can reach the same kind of utilization rates that their Oakdale and Utica mines now enjoy, somewhere in the 60% range. In an effort to be conservative, we've modeled a gradual increase in volumes for Blair and little change for Oakdale and Utica.

We would rather be low, than high, any day.

Z4 Energy Research

Pricing and Margins. 1Q23 implied revenue was near $69 per ton. For 2023 and 2024 we're modeling $62.50 which assumes some moderation occurs as the pace of rig and completion activity goes from last year's up and away to this year's dip and then, we believe, sideways action. We don't see rigs cratering, and we do think much of the price related program adjustments for 2023 have already taken place. This is a comment about average activity levels, it comes from our broad net of quarterly conference calls and post quarter calls, and doesn't apply to any one basin. For instance, rigs in the Haynesville likely have further near-term retreat than other plays. As noted above, the Haynesville is not a focus for SND. For contribution margin, we're modeling mid-teens, not much higher than current levels. This along with some modestly elevated operating cost assumptions drives EBITDA growth as noted in the cheat sheet below. This yields TEV/EBITDA multiples for both years that are well below 2x.

Given capital program guidance, we see the name reporting increasing amounts of free cash flow in 2023 and 2024. Note retirement will consume a portion of that FCF later this year, but 2024 could see a more formalized return of capital plan. Management are large shareholders. Perhaps they would like a dividend. Alternatively, and maybe a better use of capital, would be a move to take in shares prior to establishing a sustainable dividend program.

In summary, Smart Sand is a micro-cap sand name with good growth potential, but it remains relatively uncovered. The name registered strong 1Q23 results, again beating numbers, but retreated post quarter with a soft group and their flattish 2Q23 volume guidance. However, we think these points are worth highlighting:

- North American proppant demand remains resilient. We expect activity in 2H23 to flatten after seeing some retreat in 2Q23.

- Management owns 29% of the company and is conservatively plotting a profitable growth course. They've steered the company through difficult times and more prosperous ones like the one we are enjoying now. The balance sheet is in good shape and is less levered than their peers. The company bought back 11% of their shares during the first quarter, removing what had been an overhang.

- Despite the strong balance sheet, improved margins, and a rising volume outlook over the medium term, the stock currently trades at an extremely low 1.5x our 2023 EBITDA estimate. The stock remains under followed, but we understand management will be hitting the road more this year in an effort to get more eyes on the story.

- We believe we have conservatively modeled volumes and pricing and see upside for both. If Blair is able to bolster company sales as meaningfully as in the conservative take outlined above, then our view is management will, likely next year, move to return turn a portion of the resulting free cash flow back to shareholders.

- We note that larger peer US Silica ((SLCA)) trades at 3.5x Street, 2023 EBITDA. We own some of that name as well and while it's bigger and easier for larger holders to establish a position in, we also note the balance sheet is more encumbered and their growth path is likely to be slower. Simply meeting the gap in the multiples half way, at 2.5x, would put SND at $2.65 per share.

{kind=link}

For further details see:

Smart Sand: An Underfollowed Gem