NLCP - So You Want High Yield?

2023-06-24 07:00:00 ET

Summary

- A REIT that yields 10% or higher almost always means that investors perceive very low growth, or even worse, a potential dividend cut.

- I will recommend double-digit yields from time to time.

- They aren’t necessarily the safest REITs on the planet, and most have a high probability of a dividend cut.

This article was published at iREIT® on Alpha on Thursday, June 22, 2023.

Before I get started, let me conduct a survey.

What do you consider high yield?

- 5% to 7%

- 8% to 10%

- 11% to 15%

- 15% and higher

I find this to be an interesting topic these days, especially since we’re in the midst of a rising rate environment. For example, the average dividend yield of all equity real estate investment trusts, or REITs, in the iREIT® coverage spectrum is 5.1% compared with these sectors:

- iREIT® Equity: 5.1%

- MLPs: 6.4%

- BDCs: 11.0%

- Commercial mREITs: 12.0%.

As I explain in my new book, REITs For Dummies , a REIT that yields 10% or higher almost always means that investors perceive very low growth, or even worse, a potential dividend cut. That’s why most of our recommendations are in the “A” category (5% to 7%).

Many of the REITs in that bucket generate growth of around 5% per annum, which is why they have consistently generated total returns of around 10% per year (5% dividend + 5% growth).

However, as most readers know, I will also recommend double-digit yields, from time to time. They aren’t necessarily the safest REITs on the planet, and most have a high probability of a dividend cut.

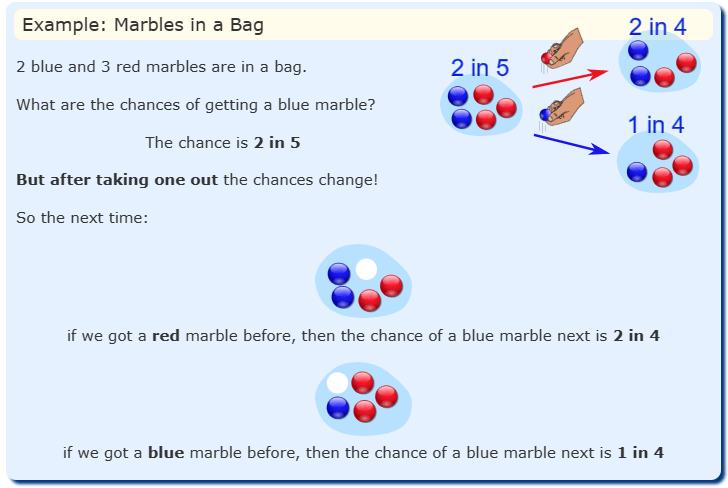

I remember when I was in college studying statistics.

I’m sure you remember the marble probability game.

{kind=link}

As you can see, when you remove marbles from the bag, the next event depends on what happened in the previous event.

Not to get into the weeds here, but high yield investing is similar to statistics. In order to play the game, you must carefully analyze each company to determine the probability that the company can sustain its dividend.

Also, everything is event driven, which is why we look closely at income statements, balance sheets, investor presentations, and of course meet with management.

It’s also worth noting that Mr. Market is also good at statistics. He provides us with a real-time opinion at least, in which he provides us with a probability score.

Sometimes he’s right…

And sometimes he’s wrong…

Sachem Capital Corp. ( SACH ) – Dividend Yield: 15.25%

SACH is a mortgage real estate investment trust (“mREIT”) that originates and services a portfolio of short term loans that have a typical duration of three years or less. Their loans are secured by first mortgage liens on commercial real estate with properties primarily located in the Southeastern and Northeastern regions of the U.S.

SACH does not lend to owner-occupants, but rather investors or developers that use the loan to develop, acquire, or improve commercial or residential properties that are held for investment or sale.

Typically, SACH targets loans with a 70% loan-to value (“LTV”) ratio but will occasionally offer loans with a higher LTV ratio depending on other factors such as additional collateral and the credit quality of the borrower.

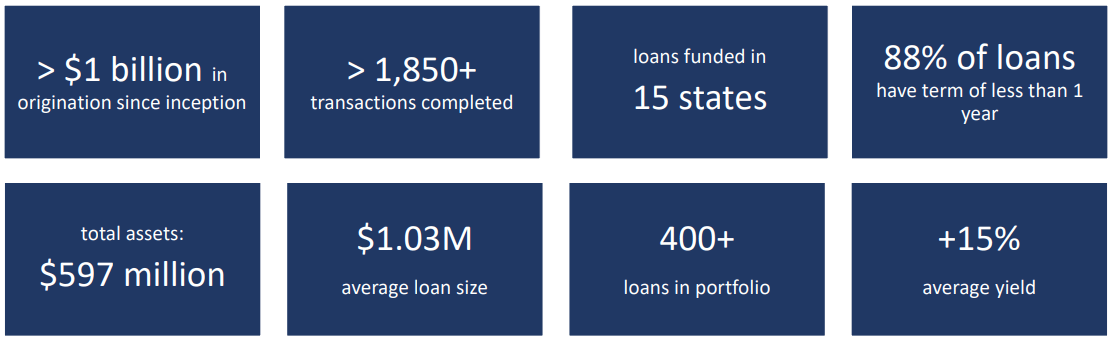

Since their inception, SACH has originated over $1.0 billion in loans and has completed over 1,850 transactions. They have over 400 loans in their portfolio with an average loan size of approximately $1.0 million and the majority of their loans have a term of under a year.

{kind=link}

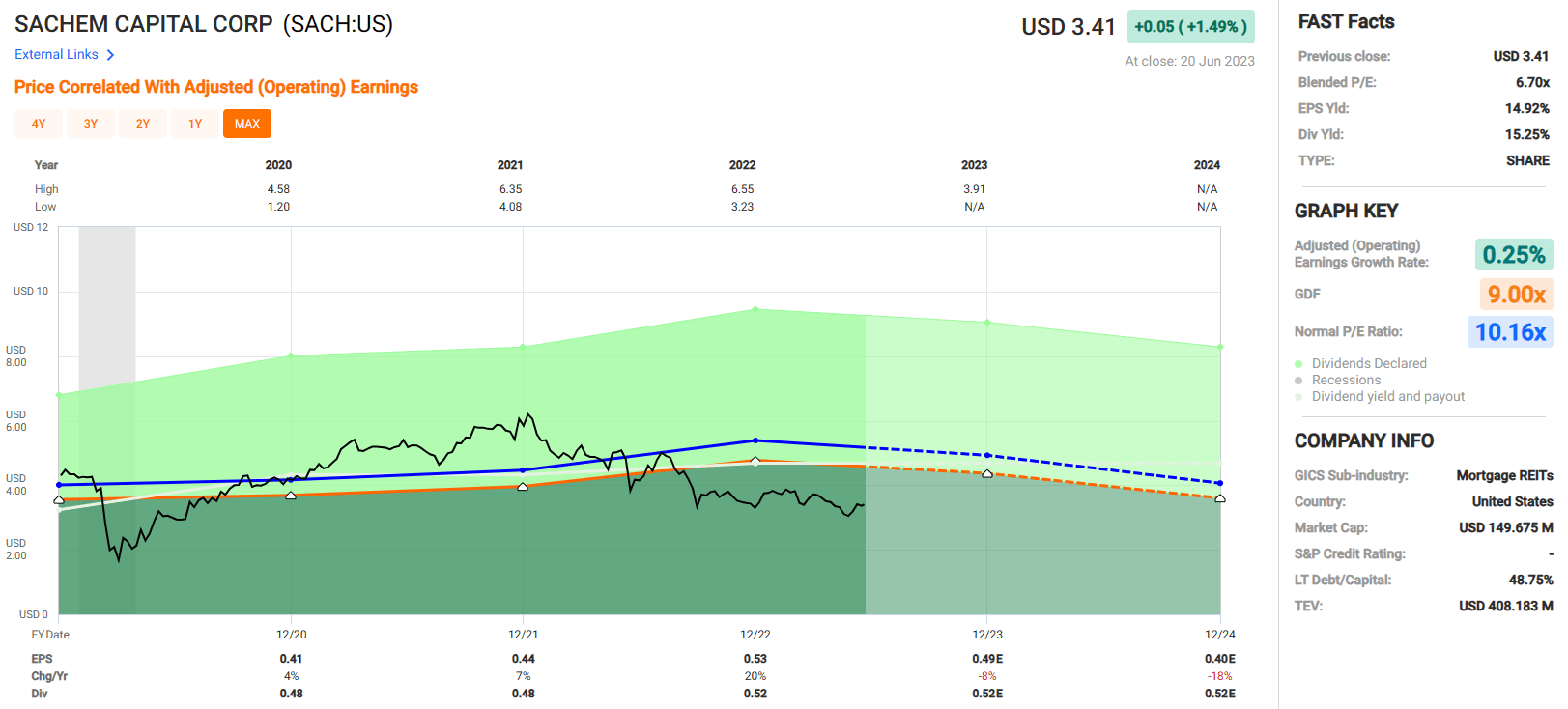

Sachem Capital pays a high dividend yield of 15.25%. They paid $0.48 per share in 2020 and 2021 and then increased it by 8.33% to $0.52 per share in 2022.

Analysts expect the dividend to remain constant at $0.52 per share in 2023 and 2024.

Based on operating earnings, SACH’s dividend payout ratio was 98.11% in 2022. In 2020 and 2021 their payout ratio was 117.07% and 109.09% respectively. The payout ratio as of the end of 2022 is the most conservative it has been over the last several years and keep in mind that most mortgage REITs have a payout ratio of around 100%.

FAST Graphs (compiled by iREIT)

SACH’s earnings increased from $0.41 per share in 2020 to $0.44 in 2021 for a 7% increase.

In 2022 earnings increased to $0.53 per share for a 20% increase.

From 2020 to 2022, SACH grew operating earnings on average by 10.29% annually.

Analysts expect earnings to fall by 8% and 18% in the years 2023 and 2024 respectively, but it appears that this has already been priced in as the stock has fallen approximately 16% over the last year.

Currently the stock is trading at a blended P/E of 6.7x, which is well below their normal P/E of 10.16x. At iREIT®, we rate SACH a Spec BUY.

{kind=link}

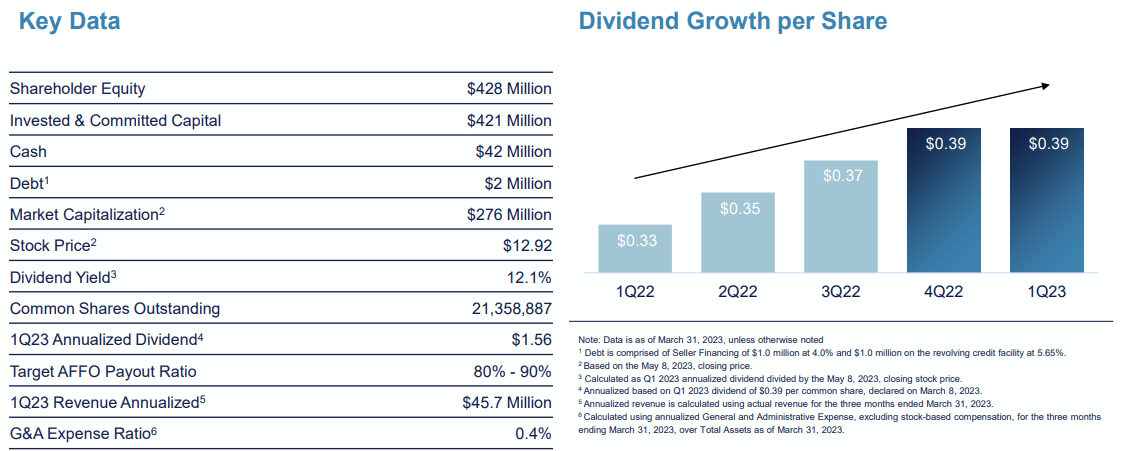

NewLake Capital Partners, Inc. ( OTCQX:NLCP ) – Dividend Yield: 12.42%

NewLake Capital is a REIT that engages in sale-leaseback transactions for properties that cultivate or dispense cannabis. Their properties are leased to state-licensed cannabis operators on a long-term, triple-net basis.

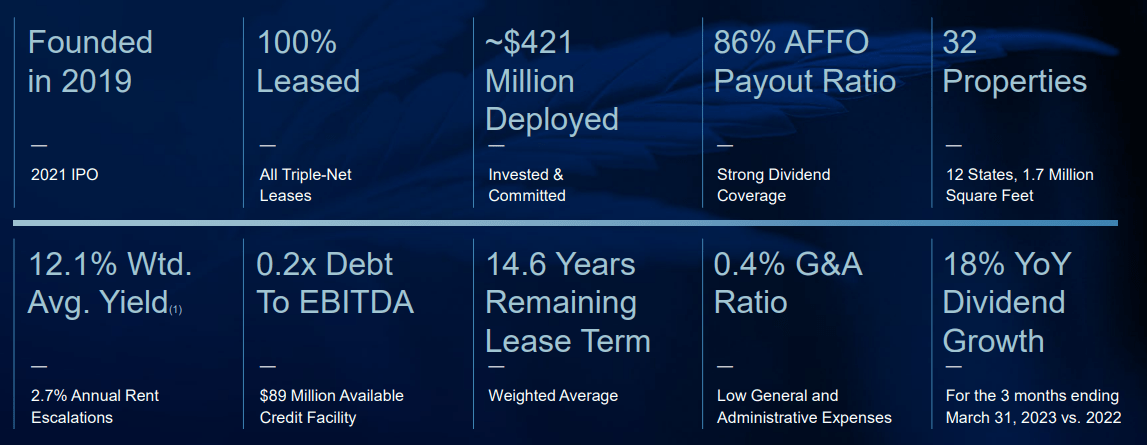

NLCP’s portfolio consists of 32 properties with 13 tenants which includes 15 cultivation centers and 17 dispensaries. In total their properties cover 1.7 million square feet, are located in 12 states, and have a weighted average remaining lease term of 14.6 years.

The company has a short history as it was founded in 2019 before going public in August of 2021.

{kind=link}

NewLake pays a 12.42% dividend yield and has delivered year-over-year dividend growth of 18% from the first quarter of 2022 to the first quarter of 2023.

In addition to the high yield and impressive growth rate, NLCP’s dividend is well covered, with an adjusted funds from operations (“AFFO”) payout ratio of 81.36% as of the end of 2022.

The dividend payout ratio is at the low end of their target range of 80% to 90%, so they should have plenty of room for future dividend increases. Additionally, analysts project AFFO to increase by 6% in 2023 and 17% in 2024 which will further provide a runway for dividend growth in the coming years.

{kind=link}

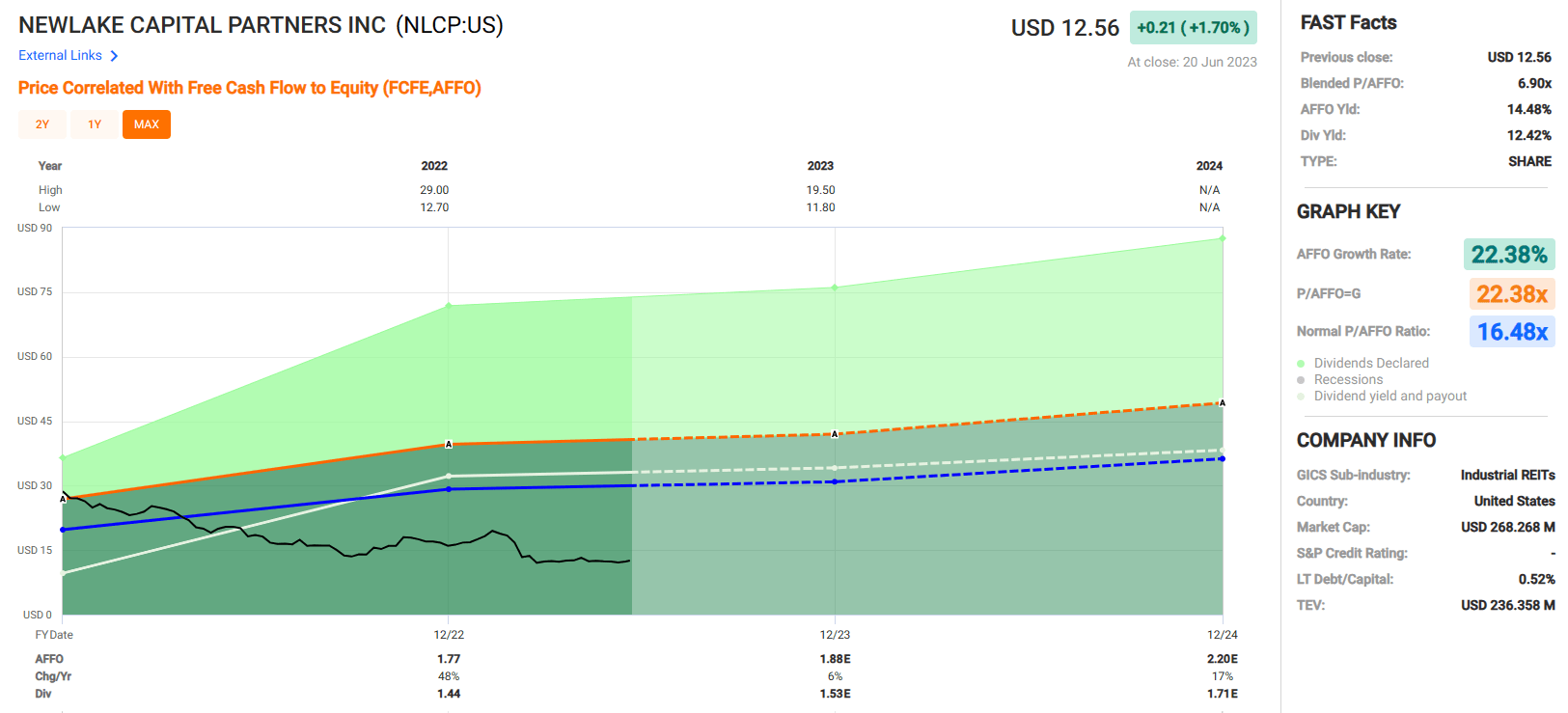

Multiple factors including the uncertainty surrounding cannabis legislation and the general economic backdrop have contributed to the -33% decline in the stock price over the last year.

The price action has pushed the AFFO yield up to 14.48% and the dividend yield up to 12.42%, all while NLCP has experience rapid AFFO growth. Currently the stock trades at a P/AFFO of 6.90x, which is a significant discount to their normal AFFO multiple of 16.48x. At iREIT®, we rate NLCP a Spec BUY.

{kind=link}

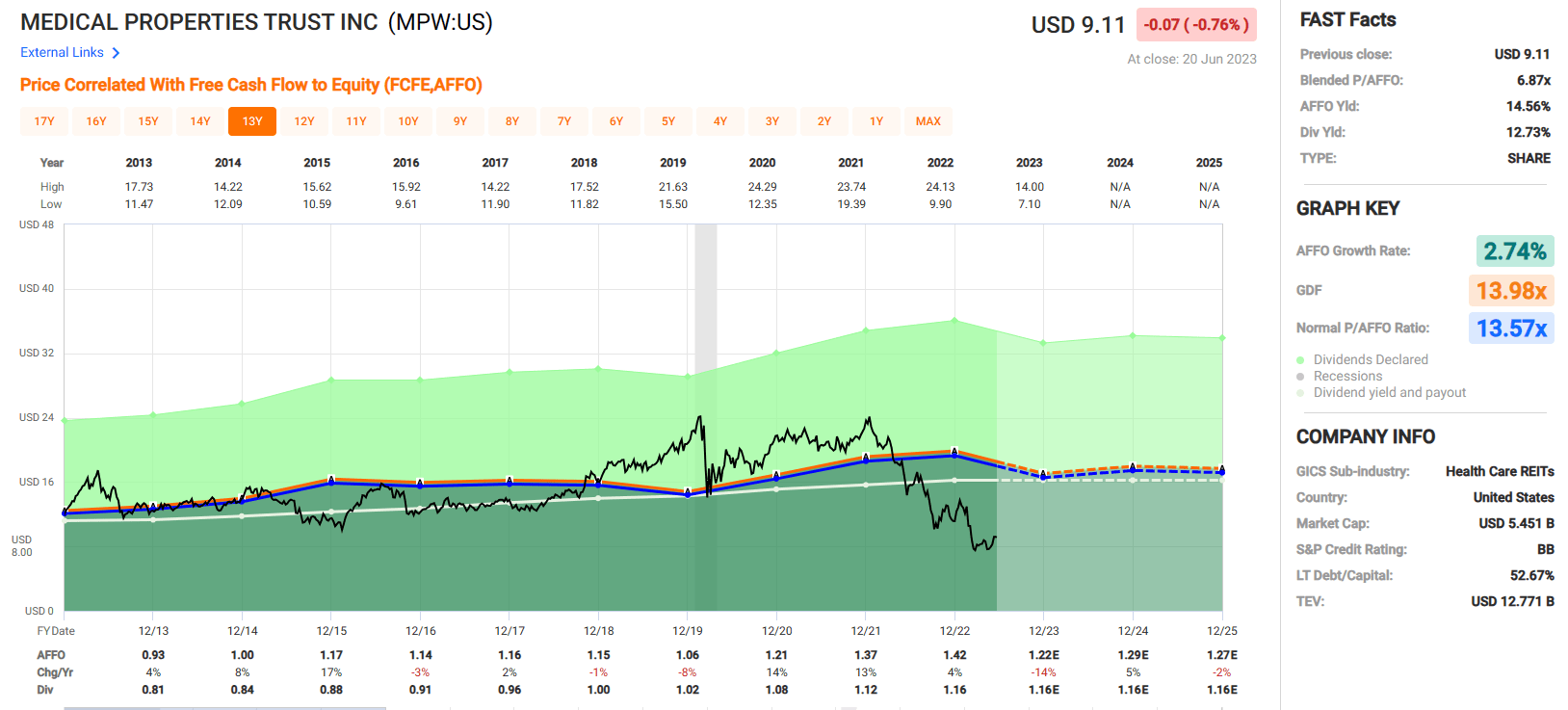

Medical Properties Trust, Inc. ( MPW ) – Dividend Yield: 12.73%

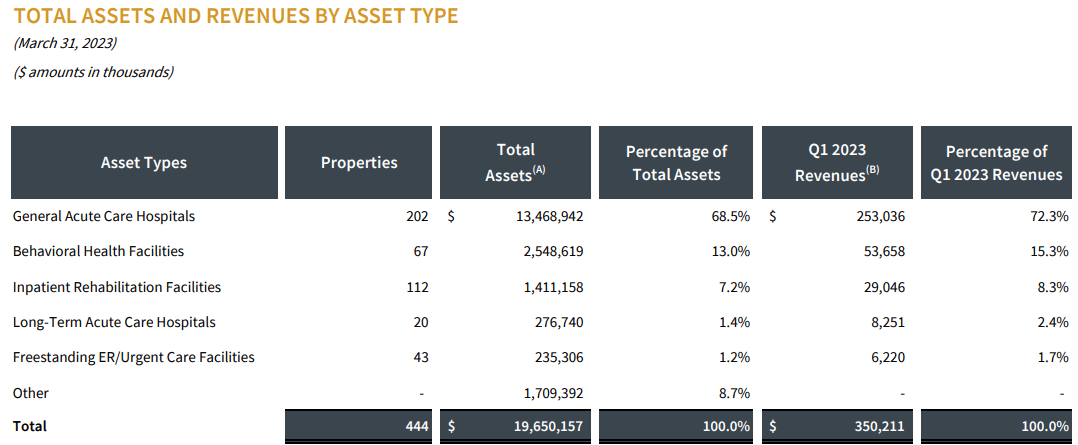

Medical Properties Trust is a REIT that specializes in healthcare facilities that are net-leased. As of the end of the first quarter, MPW had investments in 444 properties that contain approximately 45,000 licensed beds that were managed by 54 operators.

MPW has properties in 31 U.S. states as well as international properties located in seven European countries and in South America.

The majority of their investments are in general acute care hospitals, which made up 72.3% of their first quarter revenues, followed by behavioral health facilities which made up 15.3%. MPW also owns impatient rehab facilities, long-term care hospitals, and urgent care facilities.

{kind=link}

MPW pays a 12.73% dividend yield that is well covered with an AFFO payout ratio of 81.69% as of the end of 2022. Analysts expect AFFO to fall by 14% in the current year which would put the AFFO payout ratio at approximately 95% if the projections hold up.

While an AFFO payout ratio of 95% is on the high side, MPW should be able to maintain their current dividend rate, assuming there are no significant tenant issues, but dividend growth is likely to be slow or non-existent for the next several years.

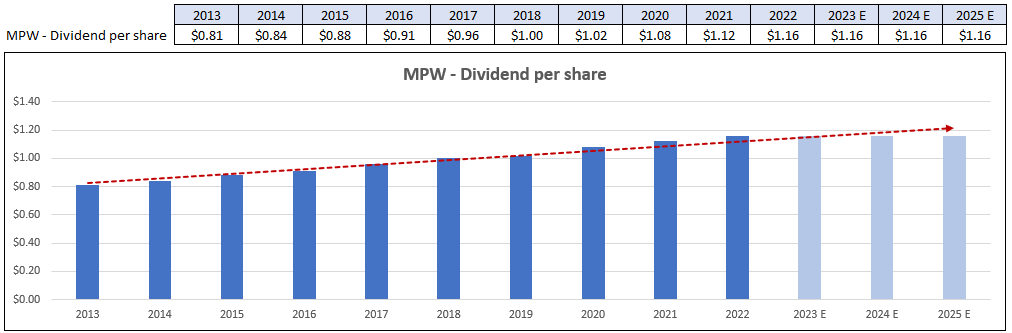

However, MPW has increased its dividend each year since 2013 and has delivered an average dividend growth rate of 3.79% over that time period. Given MPW’s dividend history, investors should expect dividend growth to resume as soon as the payout ratio gets back to a more conservative level.

FAST Graphs (compiled by iREIT)

{kind=link}

MPW has been at the center of several short campaigns recently which has contributed to the stock price’s decline of almost 40% over the past year.

Much of the short seller argument revolves around their tenant health and concentration, but as MPW has pointed out on numerous occasions, they invest in the property, not the tenant, and the critical nature of their properties should allow for another operator to step in if any of their existing tenants defaults on their lease.

Currently the stock is trading at a P/AFFO of 6.87x, compared to their normal AFFO multiple of 13.57x. Additionally, the stock is trading at a steep discount to their net asset value (“NAV”) with a P/NAV ratio of 0.66x. At iREIT®, we rate MPW a Spec BUY.

{kind=link}

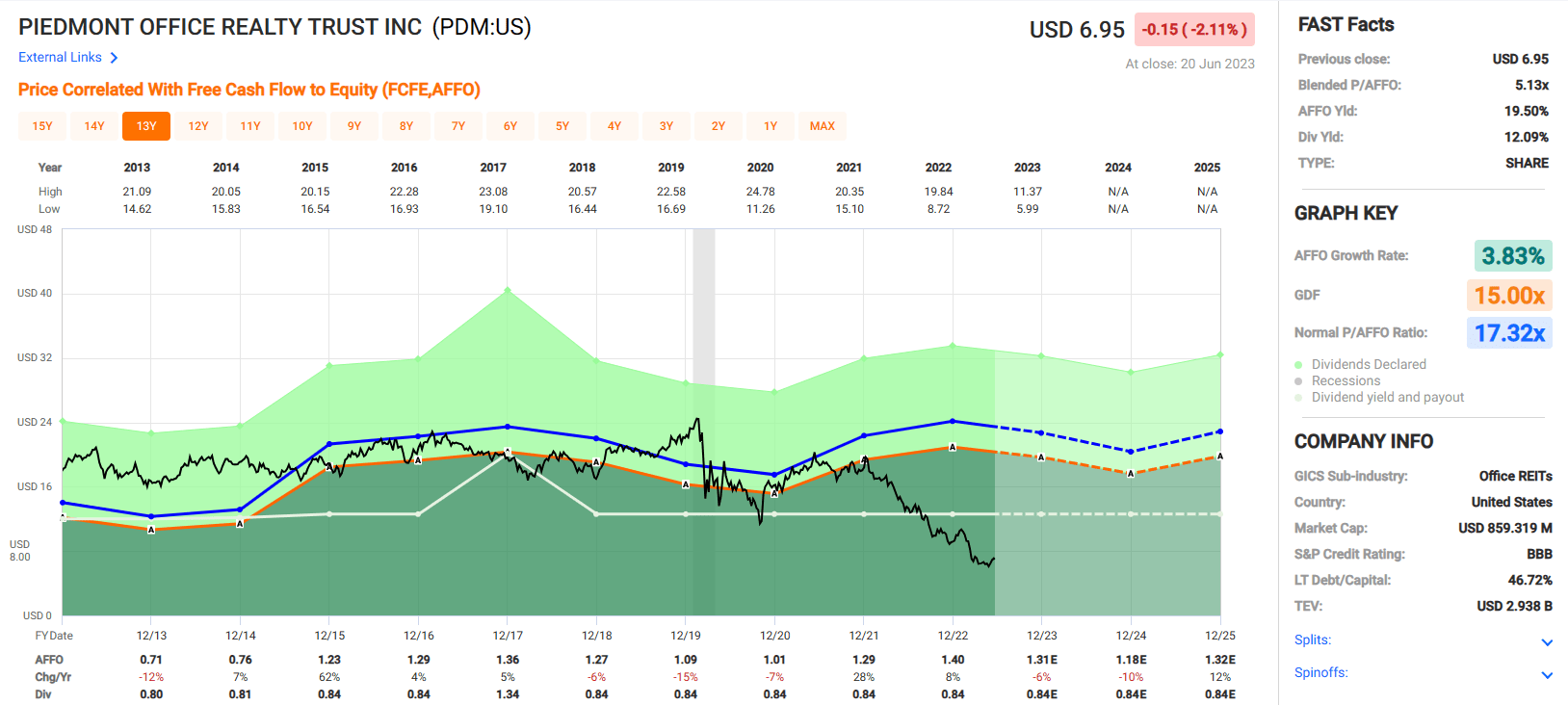

Piedmont Office Realty Trust, Inc. ( PDM ) – Dividend Yield: 12.09%

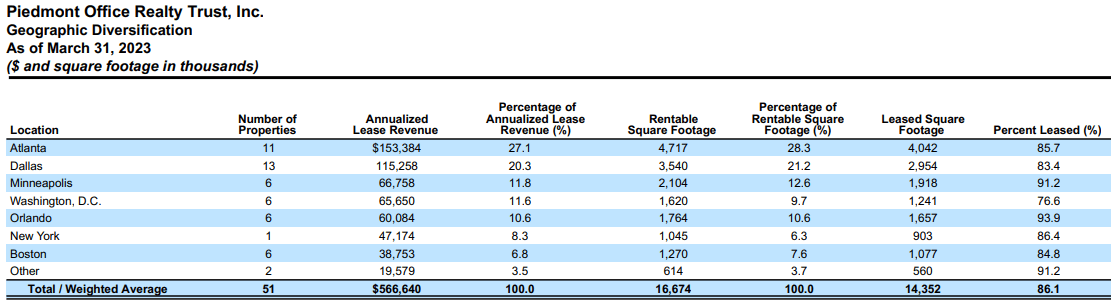

Piedmont Office is a REIT that specializes in Class A office properties that are primarily located in the Sunbelt region of the country. Their portfolio of in-service properties consists of 51 buildings that encompass approximately 16.7 million rentable square feet and are 86.1% leased.

While they have properties outside of the Sunbelt, over two-thirds of their annualized lease revenue (“ALR”) comes from their properties that are located in Sunbelt markets.

The majority of their tenant base is either investment grade, government agencies, or nationally recognized companies and no single tenant makes up more than 5% of their ALR.

Piedmont’s average lease size is around 15,000 square feet and has an average remaining lease term of approximately 6 years. PDM’s largest 2 markets are Atlanta and Dallas with 27.1% and 20.3% of their ALR coming from these markets.

{kind=link}

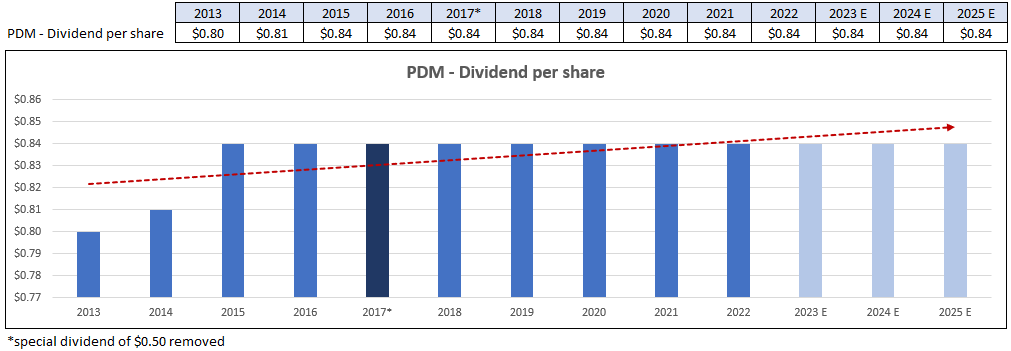

Piedmont Office pays a 12.09% dividend yield that is well covered with an AFFO payout ratio of 60.22% as of the end of 2022. They don’t have the most impressive dividend growth track record as the dividend has been maintained at $0.84 per share since 2015, but they also did not cut their dividend during the pandemic.

In 2017, PDM paid a special dividend of $0.50 along with their normal quarterly dividend of $0.84 for a total cash dividend of $1.34 that was paid to shareholders that year. In order to normalize the dividend history, I’ve removed the special dividend from the chart below.

FAST Graphs (compiled by iREIT)

{kind=link}

The office sector has struggled recently due to concerns over the work from home movement, but I believe this has already been priced in as the stock is trading at a significant discount to its normal multiple.

Currently, PDM trades for a P/AFFO of 5.13x, compared to its normal AFFO multiple of 17.32x. Additionally, its trading far below its net asset value with a P/NAV of just 0.39x. At iREIT®, we rate PDM a Spec BUY.

{kind=link}

In Closing…

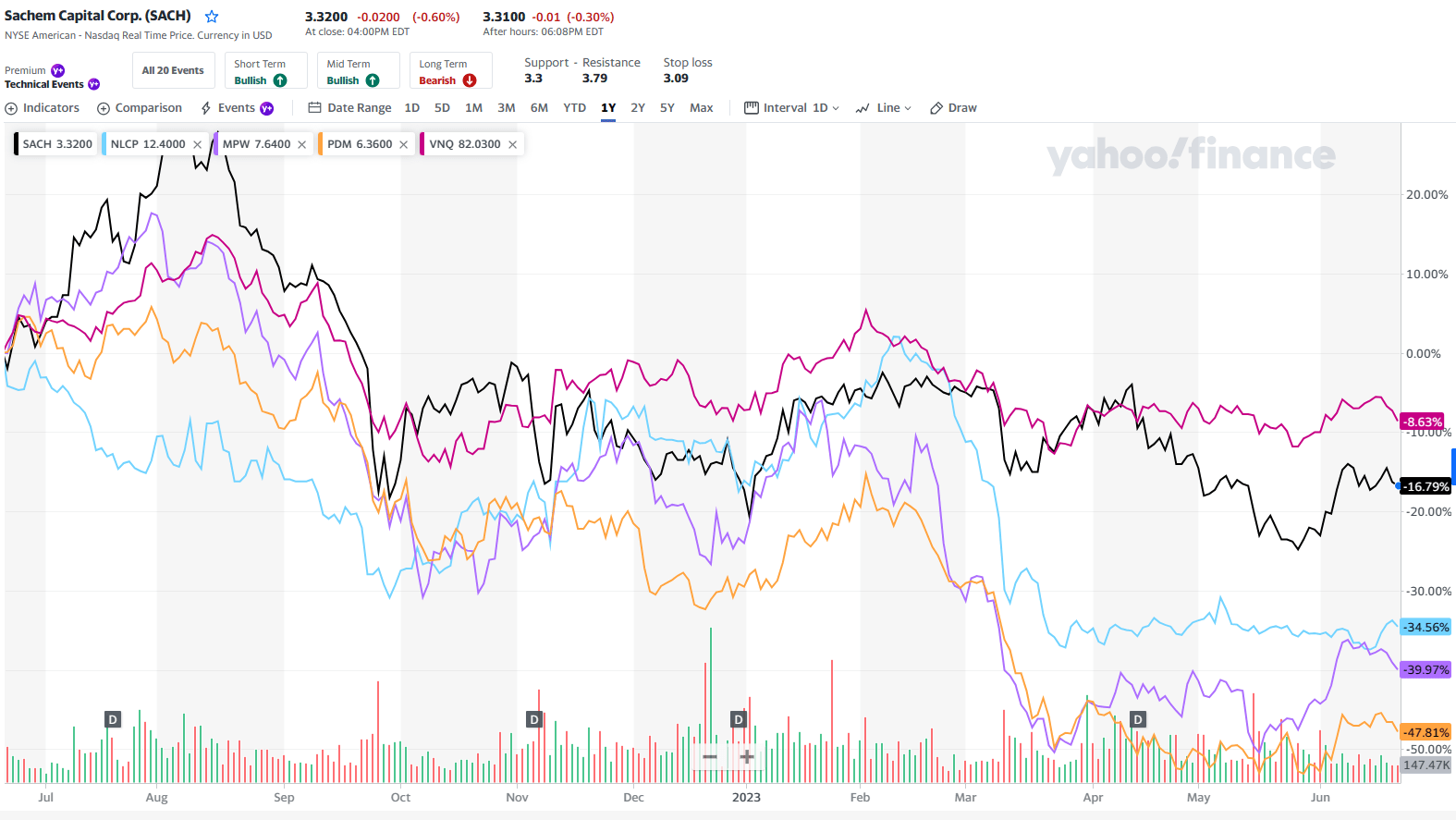

As viewed below, all four of these high-yielding REITs have underperformed the Vanguard Real Estate ETF ( VNQ ) over the last 12 months:

{kind=link}

VNQ shares fell by 8.6% compared with…

- SACH dropped 17%

- NLCP dropped by 35%

- MPW fell by 40%

- PDM fell by 48%.

This does not include the dividend, but you can see clearly that the “raised nail gets hammered.”

Is there more pain, or perhaps there’s gain ahead?

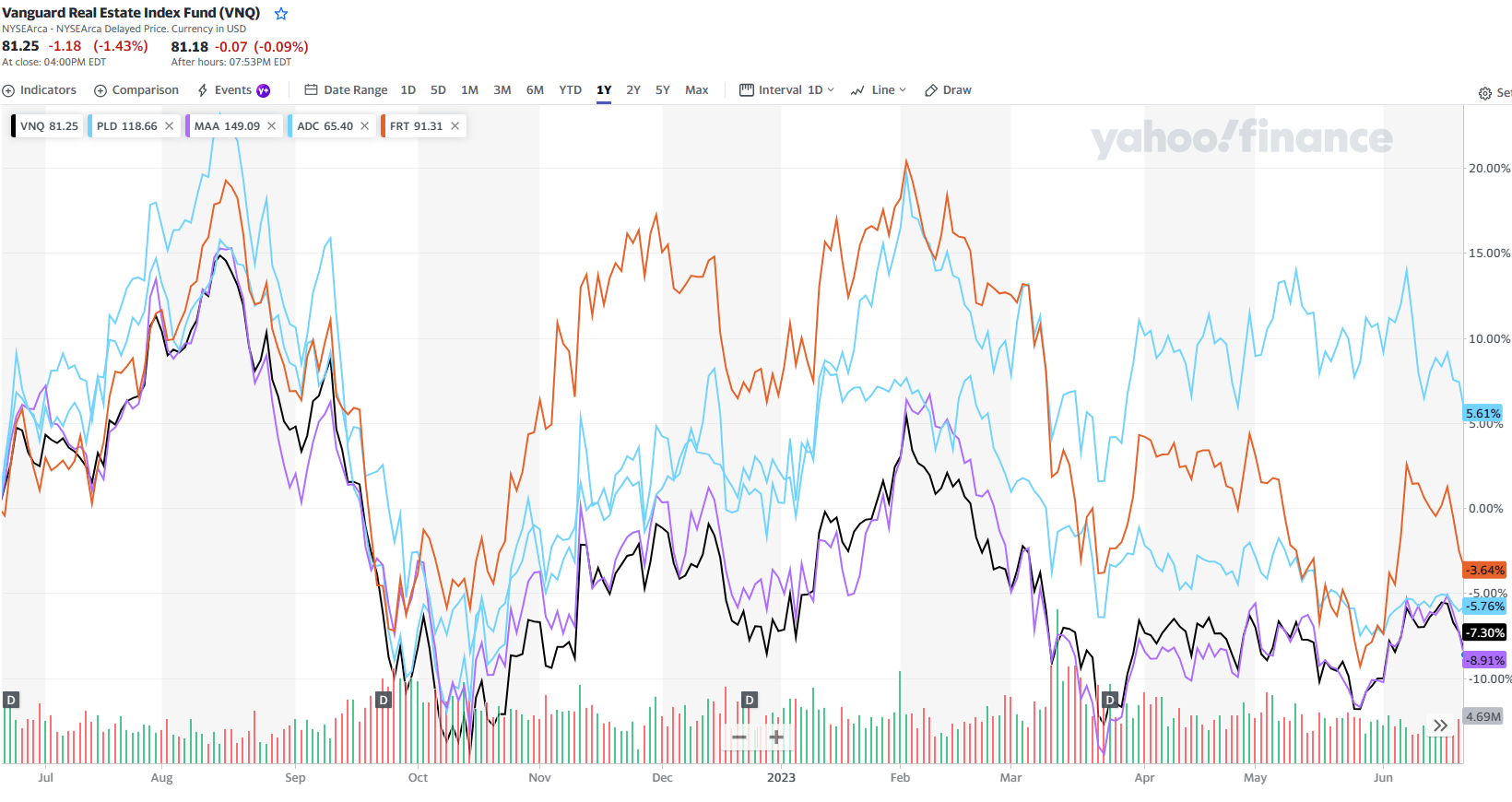

I decided to pick a random sample of SWANs using the same time frame (12 months):

{kind=link}

Prologis ( PLD ), Mid-America ( MAA ), Agree Realty ( ADC ) and Federal Realty ( FRT ) all performed in line or slightly better than VNQ.

Of course, the reason these high-yielding REITs are high yielding is because shares have declined much more .

Which leads me to my conclusion.

What’s the probability of a dividend cut?

Remember, every reader has their own risk tolerance limitations , and I cannot tell you whether to buy or not to buy. All four REITs are rated speculative which simply means that you should proceed with caution and don’t put all your eggs in one basket .

As always, thanks for reading and best of luck (you may need it).

For further details see:

So You Want High Yield?