SFTBY - SoftBank Group Is Ready To Play Offense

2023-06-23 13:50:46 ET

Summary

- SoftBank reported steady net sales of $42.79 billion and consolidated investment losses of $5.71 billion, with net asset value at $105 billion, falling back to 2016 levels.

- The company's worst-performing quarter was Q1 2022, but since then, its net income performance has shown consistent improvement.

- SoftBank's ARM business is extremely profitable and poised for growth, while CEO Masayoshi Son's passion and innovation continue to drive the company forward.

Business update

In its recent quarterly report , SoftBank Group Corp. (SFTBY) announced steady net sales at $42.79 billion. Unfortunately, its investment losses rose to $37.80 billion. The sale of $32.81 billion of Alibaba transactions, however, compensated for this considerable loss, resulting in a consolidated investment loss of only $5.71 billion. The revenue from SoftBank's own consumer business, which includes mobile services, communications, Yahoo, and PayPal financial services, has decreased from $6.06 billion to $4.28 billion given the challenges of the macro environment. On the brighter side, the worst performing quarter for SFTBY was Q1 2022 with a net income of $22.54 billion. Since then, SoftBank's net income performance has shown consistent improvement.

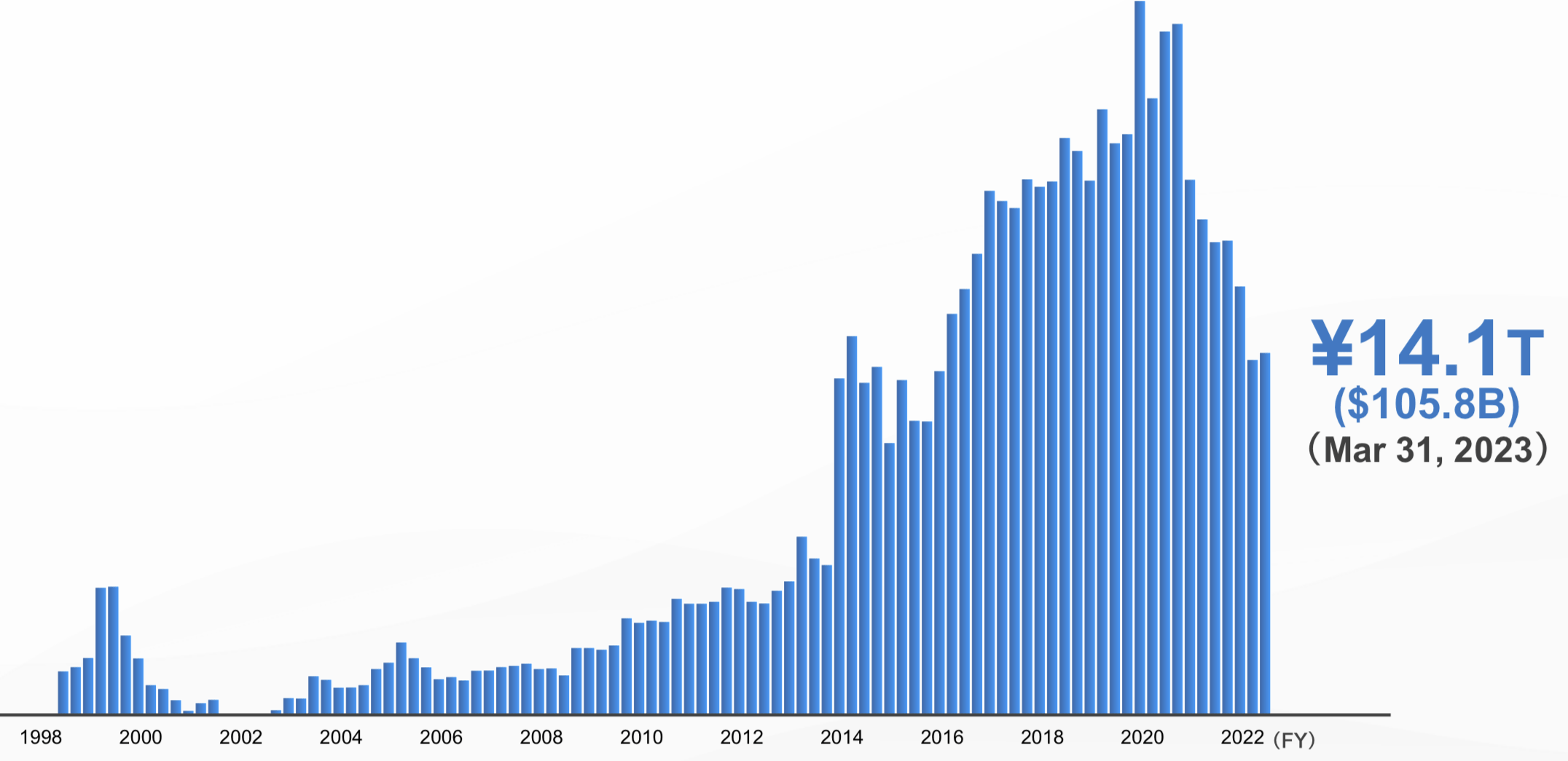

Overall, the net asset value ((NAV)) currently stands at $105 billion (chart below), which has fallen back to levels last seen in 2016, prior to the launch of the Vision Fund. In essence, SoftBank has not generated any substantial returns over the past seven years. This outcome is particularly disappointing for SoftBank, considering its role as a technology and growth investor, especially given that asset prices like the SP500 have significantly increased since 2016.

Softbank NAV trend (Softbank presentation)

{kind=link}

After the turmoil, SoftBank is in a strong position to play offense

Since 2020, SFTBY has faced numerous challenges, including the underperformance of Vision Fund companies and a failed WeWork IPO. This resulted in a massive $18 billion loss in May 2020 and layoffs for 15% of the fund's employees. Vision Fund 2 only raised half of its $108 billion target, and in 2022, the Vision Fund suffered a record $27.4 billion annual loss. High-profile departures included Marcelo Claure and Rajeev Misra, major figures within the company. To manage the loan-to-value ratio and ensure stability, management made further decisions like staff cuts and liquidating significant holdings (including Alibaba and Uber) in 2022.

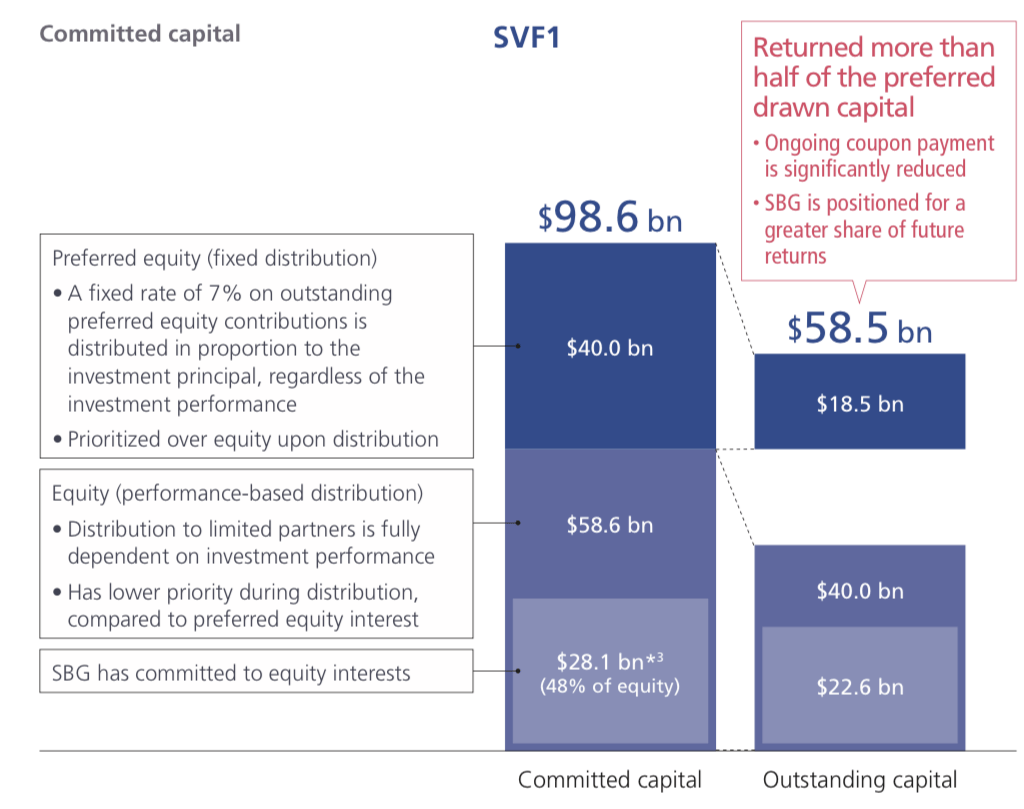

Currently , SoftBank's financial position is considerably stronger, with a loan-to-value ratio of just 11% and a robust cash position of $35.9B. The once worrisome preferred equity in Vision Fund 1 (chart below), which stood at $40 billion with a 7% fixed distribution rate regardless of fund performance, necessitating a hefty annual coupon payment of $2.8 billion, has been notably reduced. This figure has fallen significantly as the preferred equity now amounts to just $18.5 billion.

Vision Fund structure (Softbank Presentation)

{kind=link}

Finally, the proportion of Chinese stocks in SoftBank's portfolio has significantly declined, going from 51% in 2021 to a current level of 14%. SoftBank, with its Vision and Latin American funds, has transformed into a genuinely diversified global AI investor, with investments in 438 different companies. This investment strategy provides SoftBank with both resilience and a substantial scale to navigate the ongoing evolution of artificial intelligence in the coming years.

ARM is an extremely profitable business and has huge potential for growth

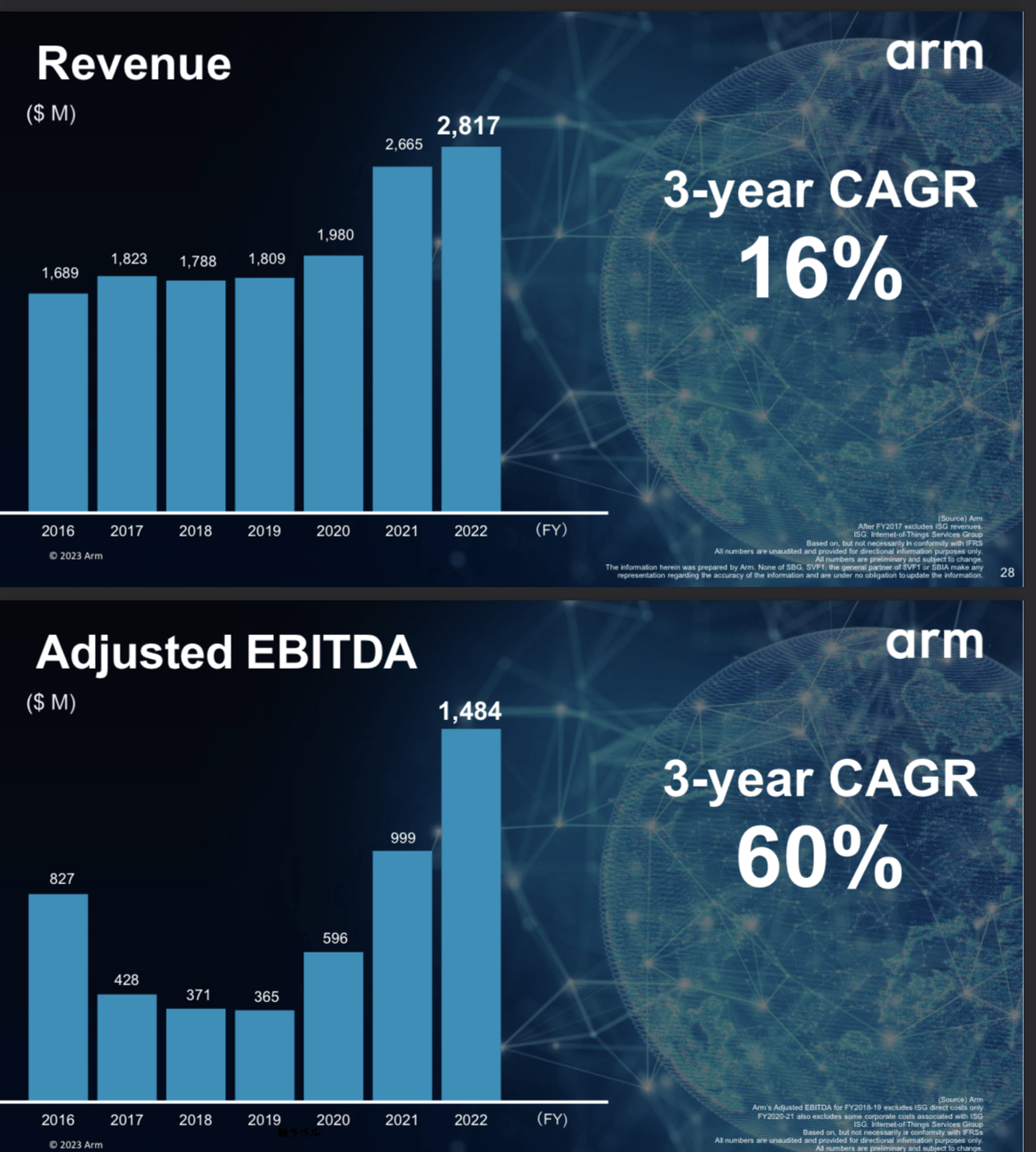

ARM (SFTBY fully acquired in 2016) can be considered a key player in the private sector when it comes to the field of AI. It is a company that has attracted the interest of major players like NVIDIA, although acquisition attempts have been stymied by regulatory bodies. ARM's chip designs, renowned for their low power consumption and high efficiency, not only dominate the mobile applications sector but also hold immense potential in the training and execution of AI models. Masayoshi Son has said that ARM has been working to build a substantial engineering team and establish robust processes in previous years. With this foundation in place, ARM is now prepared to go public and scale its operations. As the chart (below) indicates, ARM is extremely profitable with sales of $2.8 billion and an adjusted EBITDA of $1.4 billion. Even in the challenging macro environment of 2022, it has demonstrated a consistent pattern of accelerating growth.

ARM revenue and Adjusted EBITDA (Softbank presentation)

{kind=link}

Valuation is low

With an enterprise value of $177 billion (including $52 billion in cash), I find the current valuation considerably low, especially considering the $105 billion NAV is at a low point and numerous capitalization opportunities exist. If we look at the price-to-book value comparisons (below), SFTBY has been matching with Prosus NV until 2021. Now it is below 1 which is way lower than others.

The value of ARM is currently reflected in the Net Asset Value through asset-based financing, amounting to approximately $ 22B . However, ARM's recent performance, with a 3-year CAGR of 60% for Adjusted EBITDA and 16% for revenue, suggests a higher worth. The company is in discussions with major clients like Intel ( INTC ), Google ([[GOOG]], [[GOOGL]]), Apple (AAPL), though exact figures remain undisclosed. Given ARM's significant 249% increase in adjusted EBITDA, it's conceivable that its IPO value could exceed Nvidia's $40 billion offer from 2020. Even if we conservatively estimate a $40 billion valuation, SoftBank could see an immediate increase in NAVs of $18 billion. Overall, the stock is undervalued.

Bottom Line

In my view, investing in SoftBank is like backing an ETF for emerging AI companies-a sector with promising long-term prospects. However, it's important to note that SoftBank's trajectory is largely steered by Masayoshi Son, who owns nearly 30% of the company and is known for his aggressive stock buybacks. Despite the inherent risks and occasional missteps in venture investing - as seen with WeWork, View, Didi, Getaround, among others - Son's unwavering commitment, tireless work ethic, and capacity to innovate are undeniable. His Vision Fund faced a rocky start since 2017, and its future performance remains uncertain. Nevertheless, betting against Masayoshi Son may not be the wisest move.

For further details see:

SoftBank Group Is Ready To Play Offense