TRIN - Solid 10% Yield From Blue Owl Or Sixth Street?

2023-08-03 06:15:00 ET

Summary

- This article discusses dividend coverage for two of the larger and more well-known BDCs currently yielding around 10% including supplemental dividends.

- I own both of these for the reasons discussed below including credit quality, previous dividend increases, and supplemental dividends.

- We suggest one of these companies to buy today with a list of positives and negatives that investors should consider.

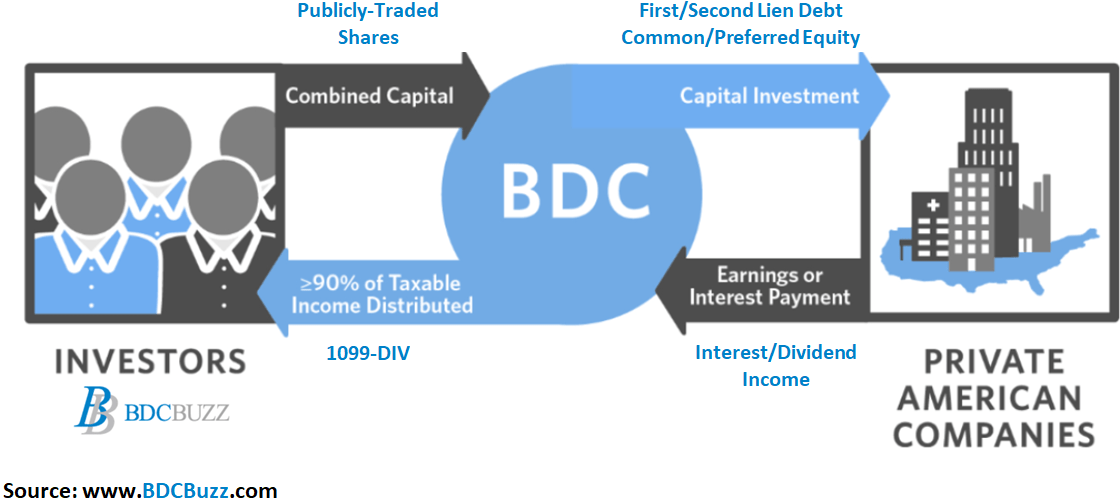

Quick Introduction To Business Development Companies

Business development companies ("BDCs") invest shareholder capital in privately-owned, small- and medium-sized U.S. companies generating income from secured loans and capital gains from equity positions, much like venture capital or private equity funds. Anyone can invest in BDCs as they're public companies traded on major stock exchanges.

{kind=link}

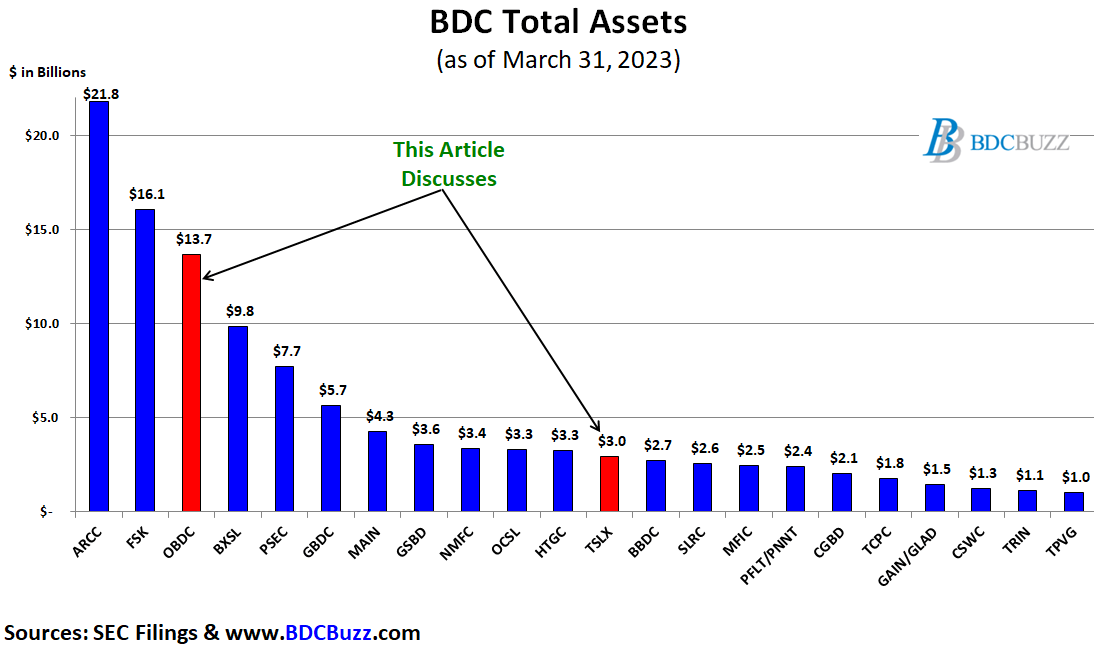

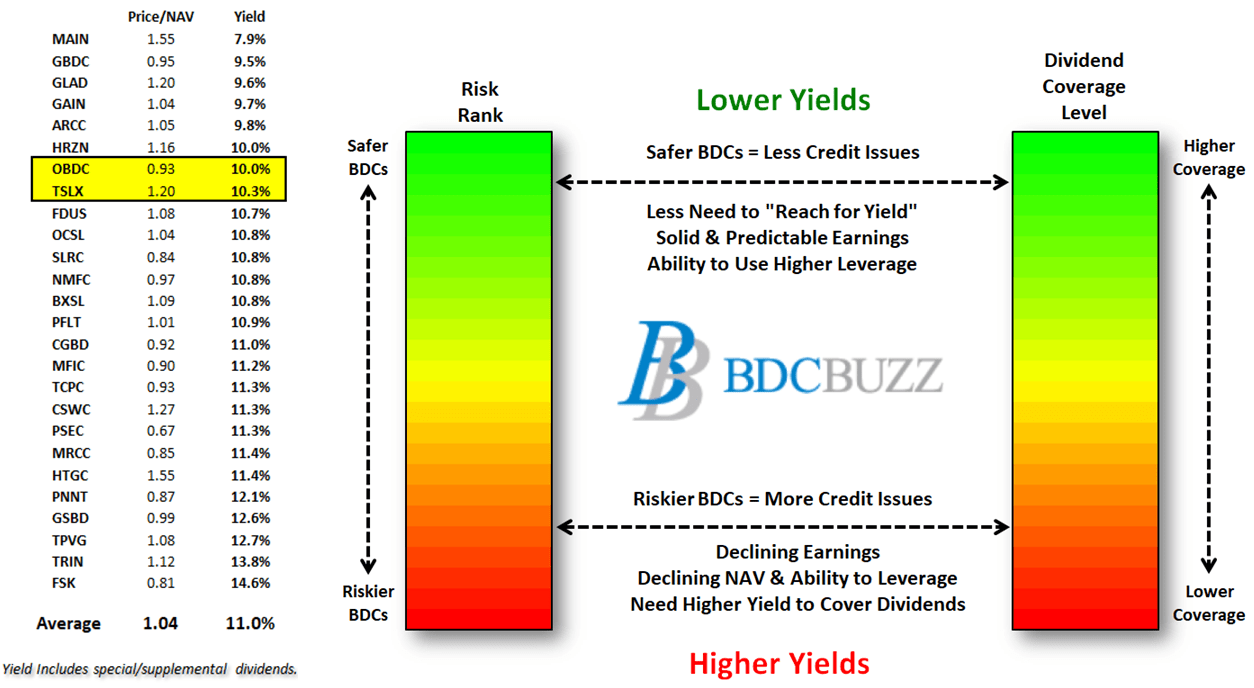

The BDCs in the chart below account for around 90% of the total assets and market capitalization for the sector. This article compares Blue Owl Capital ( OBDC ) and Sixth Street Specialty Lending ( TSLX ) which are among the larger and more well-known in the sector.

{kind=link}

Over the last six weeks, we discussed the portfolio credit quality and/or dividend coverage for many of them including Ares Capital ( ARCC ), FS KKR Capital ( FSK ), Prospect Capital ( PSEC ), Goldman Sachs BDC ( GSBD ), New Mountain Finance ( NMFC ), Oaktree Specialty Lending ( OCSL ), Hercules Capital ( HTGC ), PennantPark Floating Rate Capital ( PFLT ), PennantPark Investment ( PNNT ), BlackRock TCP Capital ( TCPC ), Gladstone Investment ( GAIN ), Gladstone Capital ( GLAD ), Monroe Capital ( MRCC ), Trinity Capital ( TRIN ), and TriplePoint Venture Growth ( TPVG ) in the following articles:

- TRIN: Initiating Coverage Of This 14% Yielding BDC

- Solid 10% Yield From GAIN & GLAD

- ARCC: Assessing Dividend Coverage For Its 10% Yield

- OCSL or NMFC For Solid 11% Yield?

- Better High-Yield Buy: FSK or PSEC?

- PNNT: Big Win From Dominion/Fox Settlement

- Venture Debt Opportunity Yielding 13% To 14%: HTGC or TPVG?

- TCPC or PFLT For Solid 12% Yield?

- Safer 12% Yield: GSBD or MRCC

As shown below, many of these BDCs are among the highest yielding. The yield for OBDC includes $0.10 per share and TSLX includes $0.20 per share of supplemental dividends (discussed below).

BDC Buzz & SEC Filings

Also, many BDCs have investment grade ("IG") bonds/notes for lower-risk investors building a balanced 60/40 portfolio (composed of 60% to 70% stocks/equities and 30% to 40% bonds or other fixed-income offerings). These notes were previously overpriced, but prices have declined and are now at attractive levels. OBDC and TSLX have multiple tradeable notes (CUSIPs: 69121KAA2, 69121KAB0, 69121KAC8, 69121KAD6, 69121KAE4, 69121KAF1, 69122JAA4, 69121KAG9, and 87265KAF9) currently yielding between 7% and 8% as mentioned last month in " Introduction To BDC Google Sheets ."

BDC prices have continued to head higher as investors are trying to front-run the upcoming Q2 2023 earnings season which will likely be strong, similar to the previous three quarters. It's important to note HTGC, BXSL, GLAD, GAIN, ARCC, CSWC, and MAIN, have recently increased their dividends, announced special/supplemental dividends, and/or reported strong results maintaining credit quality with increased NAV per share. As shown below, TSLX will be reporting after the close of the markets today followed by OBDC next week.

BDC Buzz & SEC Filings

Comparing Dividend Coverage

The three biggest mistakes that new BDC investors make are:

- Focusing on historical dividend coverage instead of projected dividend coverage which is heavily reliant on portfolio credit quality.

- Not taking the time to dig into portfolio credit quality and assess which investments could potentially have a negative impact on earnings and NAV.

- Not understanding why BDCs trade at different prices and thinking that price-to-NAV is the only measure to find a "good deal." Please see the end of this article for a quick discussion of how BDCs are valued.

Each quarter I update the financial projections for each BDC with base, best, and worst-case scenarios to test the sustainability and/or changes to the current dividends. Below I discuss many of the drivers used for projecting dividend coverage including the base, best, and worst-case projections similar to what we provided in the "ARCC: Assessing Dividend Coverage For Its 10% Yield" article linked earlier.

OBDC

Blue Owl Capital ( OBDC )

OBDC has better-than-average dividend coverage mostly related to:

- Previous increases in interest rates

- Reinvesting repayments at higher yields

- Increased dividend income from Wingspire and its OBDC Senior Loan Fund

- Prepayment fees and accelerated OID

- Maintained higher leverage

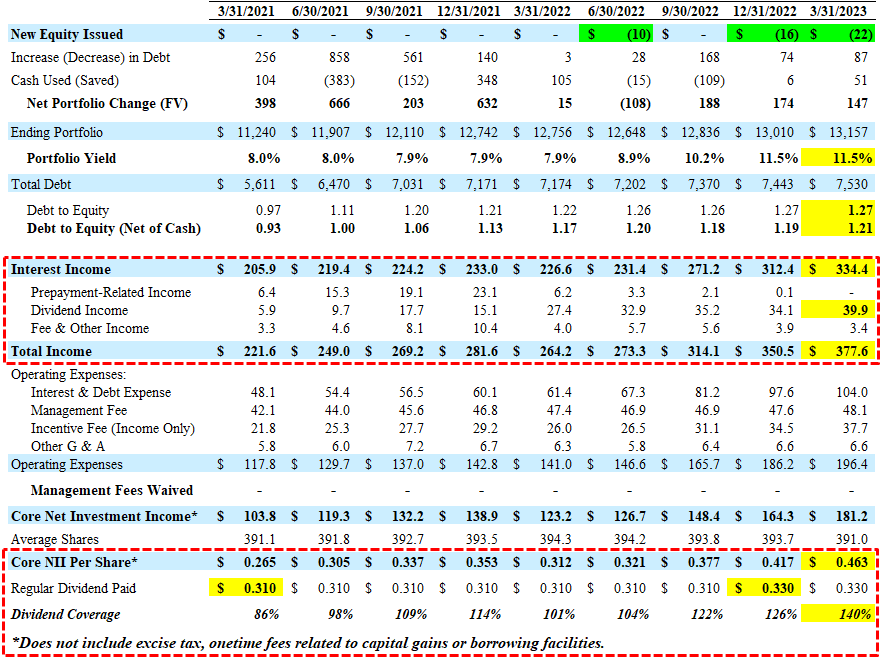

For Q1 2023, OBDC beat its best-case earnings covering its dividend by 140% mostly due to increased dividend income from its OBDC Senior Loan Fund and Wingspire and slightly higher-than-expected portfolio growth.

The current market environment remains a very attractive one for direct lending. With the public market mostly unfavorable for new issuance, we continue to see direct lenders financing nearly all of the deals that are coming to market. These opportunities are attractive because they are for high-quality borrowers with enhanced spreads, documentation and leverage levels. ORCC [OBDC] is currently benefiting from this environment, largely through amendments and other repricing events which continue to help increase the overall spread on our portfolio.”

“Recent volatility in the credit markets and general capital constraints have underscored the benefit of scale for direct lending platforms. Given the potential challenges to come over the near to medium term, we believe that the market environment over the next couple of years will favor larger platforms like ours. Size and scale are increasingly important when it comes to fundraising, deal flow and access to financing as well as hiring and retaining top talent. And we believe that the strength of our platform will be even more apparent during this time. When conditions are more challenging, people naturally gravitate to the stability and security that larger platforms provide, and we expect to be a beneficiary of this dynamic.”

{kind=link}

OBDC management mentioned the more lender-friendly environment with higher overall yields and better terms, including stronger covenants (safer investments) taken into account with the best-case projections:

Even with lower rates, we're going to have terrific earnings at ORCC because they're still much higher than they were a year ago and our spreads are elevated as well . So even in an environment, if you take the forward curve, we should have very strong earnings this year and next year. So I feel really well positioned on that. To your question, is there some -- can we grind that spread even higher? I mean look, this is something we've been really focused on. And if you've watched us quarterly, we have, for the last six quarters, really been able to grind spread higher in the portfolio as we rotated out of some lower-spread investments . It's been a very active and deliberate strategy, patient, thoughtful. So possibly, we could do a bit better. It really depends where market spreads go as the market strengthens. But I think our spread is very high already relative to the peers. But we'll have to see how that aligns with where new deals are coming at the time that's happening.”

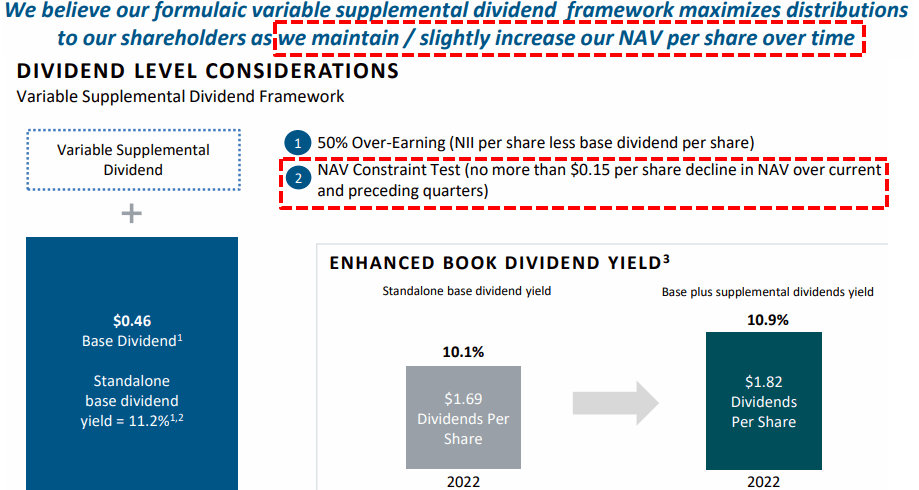

OBDC previously reaffirmed its regular quarterly dividend of $0.33 per share plus a supplemental dividend of $0.06 per share for a total of $0.39 per share for Q2 2023, which was the previous best-case projection .

Our Board approved a supplemental dividend of $0.06 per share, which is an increase of $0.02 from the prior quarter. This is in addition to our previously declared $0.33 regular dividend which results in total dividends of $0.39 for the quarter. In total, this represents an annualized dividend yield of over 12% based on the current share price, which we believe is very attractive in today's market. We also delivered an ROE of 12.1% for the quarter, and we would expect to deliver an ROE in excess of 12% over the full year based on our current outlook for rates and credit performance.”

Many BDCs have opted to take a conservative approach when setting their regular dividends (just in case rates head lower) and using supplemental/special dividends to pay out excess earnings. This means that if portfolio yields decline, we will see lower amounts of supplemental/special dividends but the regular dividends will be maintained especially "Level 1" dividend coverage BDCs. OBDC management discussed this on the recent call:

Going into the third quarter of last year, we were confident that rising rates and continued credit performance were going to drive significant improvement in earnings. As a result, we increased our regular dividend by $0.02 and added a formulaic supplemental dividend to our quarterly dividend structure. We recognized that we would significantly outperform the regular dividends in a rising rate environment and wanted to create a predictable mechanism to share that upside with shareholders. Compared to the second quarter of 2022, the average base rate in the portfolio increased roughly 300 basis points and the NII has grown by over 40%, which has driven the growth in our supplemental dividend. We instituted a supplemental dividend on the back of our continued earnings momentum to ensure that our shareholders benefit from the higher rate environment. We expect to continue to evaluate our dividend policy going forward to ensure we are striking the optimal balance of sharing upside while also protecting the stability of the dividend across all market environments .”

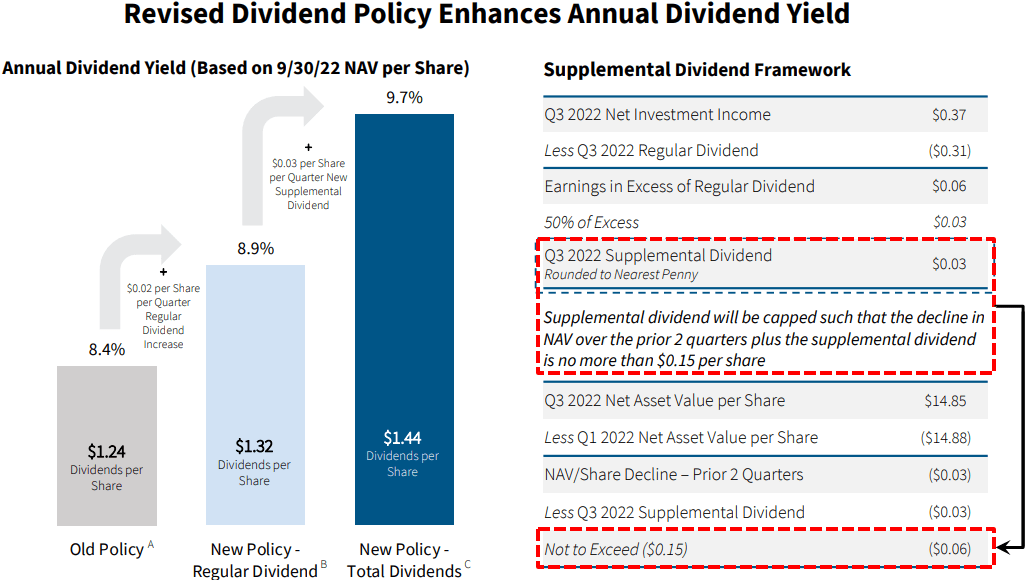

OBDC has adopted a formula-based supplemental dividend in an amount to be determined each quarter calculated at 50% of earnings in excess of the regular dividend. Also, when calculating supplemental dividends, management takes into account a “NAV constraint test” to preserve its NAV per share. Supplemental dividends will be capped such that the decline in NAV over the prior two quarters plus the supplemental dividend is no more than $0.15 per share.

The supplemental dividend will be variable each quarter, calculated at 50% of NII in excess of our regular dividend, rounded to the nearest penny and subject to certain measurement tests. It will be announced with quarterly results and paid in the following quarter. OBDC shareholders will receive a dividend 8 times a year.

{kind=link}

The company can easily support dividend increases in the base and best-case projections:

We are pleased with the continued strength of our earnings. We believe this quarter's NII represents a sustainable level in the current rate environment. We could see further upside if repayments pick up or dividend income from our strategic equity investments and the senior loan fund increase. Conversely, we could also see a decline in NII if rates drop or non-accruals increase, although we do not currently see evidence of either happening in the near term.

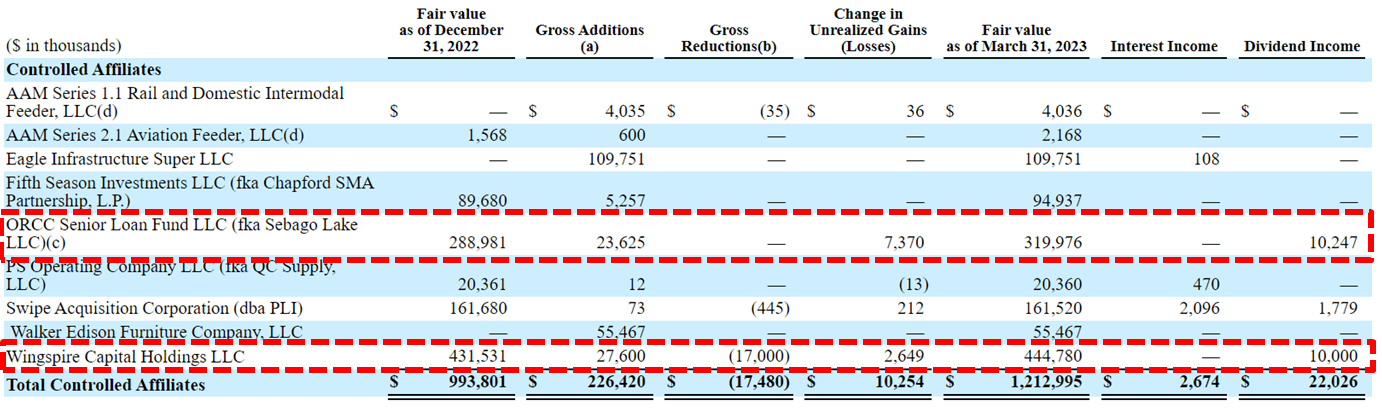

The updated projections take into account increases in dividend income from Wingspire Capital Holdings and from its OBDC Senior Loan Fund, which combined currently account for 5.8% of the total portfolio but likely higher over the coming quarters. During Q1 2023, these investments provided dividend income of over $20 million:

{kind=link}

Wingspire previously acquired an equipment leasing company (Liberty Commercial Finance) and there was an increase in the Senior Loan Fund that will likely drive additional dividend income during 2023. Also, on Aug. 2, 2022, Owl Rock announced an investment in Amergin Asset Management , a newly formed portfolio company created to invest in a leasing platform focused on railcar and aviation assets.

We've been really pleased with the performance in Wingspire. As a reminder, we built that business organically working with a very experienced management team. It took a few years for them to sort of hit the momentum that they're at now. It's performing quite well and delivering very attractive dividends and ROE for ORCC. There, we talk to them regularly. And I think they're seeing good market conditions already just given the environment. And we will -- we do expect to continue to provide additional capital to Wingspire as they find opportunities . It stands to reason that if regional banks pull back from credit support, that will provide additional opportunities for Wingspire . I don't think we've seen that effect yet. In addition, generally in a weaker economy, companies will turn to asset-based financing more frequently . So I think that I agree with the supposition of your question. There will be more opportunities for Wingspire and we can put more capital in it and earn really attractive returns .”

In November 2022, the company announced the approval of a $150 million stock repurchase program, a portion of which may be executed under Rule 10b5-1 in order to make purchases outside of the company's open-market window. Also, certain affiliates and employees of Blue Owl have indicated that they intend to participate in an investment vehicle that will be authorized to buy up to $25 million of OBDC common stock, which will be held for investment purposes. During Q1 2023, the company repurchased another 1.8 million shares for $22.1 million or around $12.27 per share (an 18% discount to the previous NAV per share). As of May 10, 2023, a total of $73.7 million of common stock was purchased at an average price of $12.22 per share.

We have also continued to work towards our previously announced repurchase target of $75 million through the combined buying power of the company's share repurchase program and the Blue Owl employee investment vehicle. As of May 10, an incremental $22 million of ORCC stock was purchased bringing total stock purchased to $74 million at an average price of $12.22, of which $49 million was repurchased by the company.”

OBDC has higher-than-average amounts of payment-in-kind (“PIK”) interest income, currently around 11.4% of total income or 12.9% of interest income, which includes its non-accrual investment in Walker Edison Furniture , as mentioned later. Also, OB Hospitalist and Tall Tree Foods were partially/fully converted to PIK during Q1 2023. However, management discussed this on the previous call and mentioned that most of the PIK is not related to restructured investments and/or credit issues. My opinion is that OBDC has an excellent history of credit quality and continues to invest in larger companies that would likely outperform, so a higher amount of PIK is acceptable, but I will continue to watch over the coming quarters.

With the vast majority of our PIK income is not from credit problems , it's from specific deals where we were asked to structure our investment with either a portion or all PIK at the get-go, and we thought it was reasonable to do so for credit specific reasons. It's like 85%, 90% of our PIK income. We have very little PIK income from credit problems. So, it's just not an indicator of stress in the portfolio. If you're asking me, I think about where we are low double digits, it's about the right level of PIK. So I don't think we expect to take that number higher. As I mentioned before, we're not seeing request for PIK from troubled credit situations, but we are in a very comfortable place there and there is nothing – there is no so you should not look at as a cause of concern of the portfolio because that's not what it's an indicator of.”

{kind=link}

TSLX

Sixth Street Specialty Lending ( TSLX )

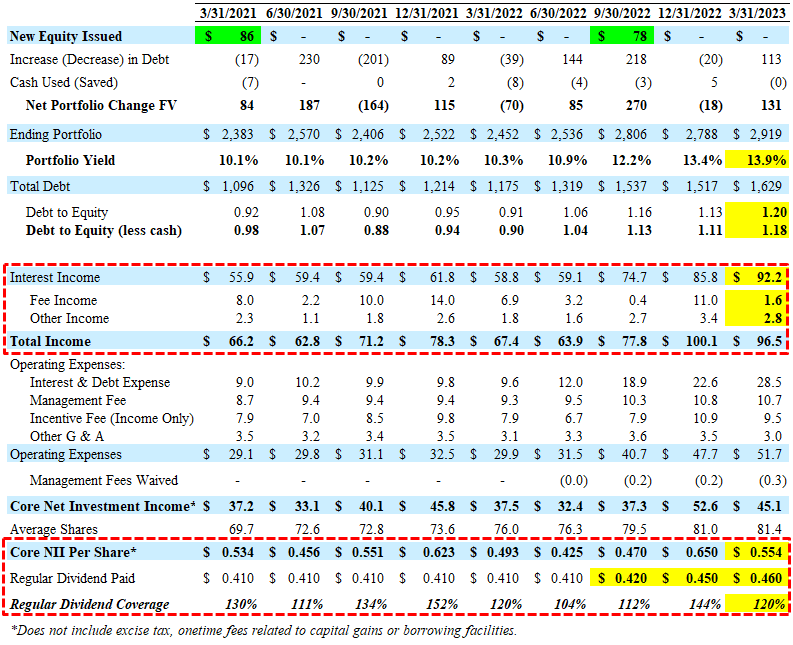

For Q1 2023, TSLX reported between its base and best case projections covering its regular dividend by 120% with much lower-than-expected fee and prepayment-related income, including accelerated original issue discount (“OID”) accretion of only $0.5 million (compared to over $8 million the previous quarter). Also, there was another increase in the overall portfolio yield from 13.4% to 13.9%. Leverage increased slightly and remains near the midpoint of its targeted debt-to-equity ratio between 0.90 and 1.25.

On the repayment side, higher interest rates and the lack of more traditional capital market financing alternatives have led to a slowdown in refinancing activity, resulting in less portfolio turnover over the last couple of quarters. Activity-based fees represented only 3.6% of total investment income for the quarter. Year-over-year, total investment income has increased 43%, largely driven by asset sensitivity from higher interest rates in our floating rate investments. We expect that the interest rate environment will continue to support core earnings without the impact of any activity related income based on our base dividend level.”

{kind=link}

BDCs should continue to benefit from tightened lending policies and potentially increased banking regulations, which will likely include stronger capital and liquidity standards for certain banks. BDCs have a distinct advantage over banks in that they have “permanent equity capital” and are not subject to “runs on the bank,” which could lead to the forced liquidation of undervalued assets.

Let’s start with the pullback for banks. I think that’s most definitely happening. I think there has been a realization that banks had not completely understood their business model. And their business model is lending long and borrowing short through deposits . And those deposits, they have been able to hold at very low cost. And I think everybody is kind of woken up because of the kind of the big systemic issues of bank failures and started moving – the deposit beta is much higher than they thought, they have started moving the consumers and businesses start moving things to money market funds and treasuries and moving things out of deposits. So, I think banks are going to pull back on lending until they understand what their capacity of lending is given the balance sheet on the right-hand side of both varying probably unstable to them. And that will cause banks get close out their options. And I think people are starting to talk about a credit crunch, which I think is good for private lenders . And then on the ABL side, most definitely, I would expect capacity to be cut in that space as well. And so I think that will most definitely create opportunity for kind of generally our specialty lending verticals.”

The recent instability in the banking sector is likely to have a considerable effect on BDCs, resulting in continued improvement in yields on new investments and a wider range of investment opportunities. As a result, BDCs can continue to be very selective in their new investment choices. Earlier this month, TSLX management mentioned the more lender-friendly environment with better terms, including stronger covenants (safer investments) and higher overall yields taken into account with the best-case projections:

I’d like to start by sharing some observations on the broader market backdrop, in particular, the secular shift towards private credit that has been a persistent theme over the last few quarters. We believe the opportunity set for our business is the greatest we have seen in recent history and at least since the global financial crisis. The development in the financial sector has further increased market share for direct lenders as banks are tightening credit and public markets remain unreliable in light of heightened economic uncertainty. As a result, nearly every financing opportunity is coming to the private credit market due to the flexibility and execution and certainty that direct lenders with capital are able to provide. This shift has been a positive for our business as we continue to build a robust pipeline while remaining selective. Broadly speaking, M&A and LBL activity have meaningfully slowed, but the scale and quality of companies refinancing has generally improved given the shift towards private credit.”

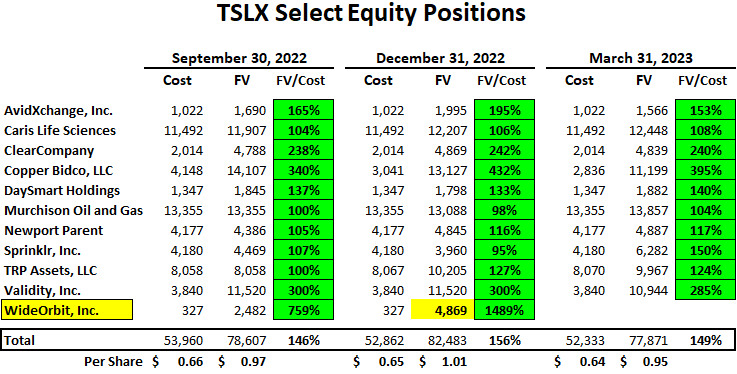

Most dividend coverage measures for BDCs use net investment income (“NII”) which is a measure of earnings. However, some BDCs achieve incremental returns with equity investments that are sold for realized gains often used to pay supplemental/special dividends. During Q1 2023, TSLX realized another $5 million or $0.06 per share of net realized gains mostly related to the full exit of WideOrbit .

Our full payoff during this quarter was our investment in WideOrbit, which is a provider of TV and radio traffic management software. As a reminder, we made our initial investment in July of 2020 in the COVID-driven market dislocation. Our ability to play offense during this time, not only benefited the company in this need for refinancing, but also allowed us to structure the transaction with favorable terms for shareholders, including potential upside through ownership of warrants. In February, the company was acquired by the Lumin Group, which included a repayment of the outstanding balance on its credit facility and proceeds to outstanding warrant holders. TSLX received $5.2 million in proceeds from the sale of our warrants, resulting in a r ealized gain of $4.8 million or $0.06 per share and generated a blended IRR and MOM on our total investment of approximately 17% and 1.4x respectively.”

As shown below, many of its equity positions are still marked above cost which could result in an additional $0.31 per share of realized gains if sold/exited at March 31, 2023, fair values.

{kind=link}

TSLX has increased its regular quarterly base dividend from $0.38 to $0.46 per share over the last nine years. In May 2023, the company announced another supplemental dividend of $0.04 for a total of $0.50 per share paid in Q2 2023, which was slightly above the previous base case projections of $0.49 per share.

It's important to point out that the base dividend of $0.46 per share is easily covered, especially given that the company has earned an average of $0.54 per share over the last three years. As mentioned in the weekly BDC sector updates, I'm expecting fewer (and smaller) increases in the regular dividends but larger supplemental dividends over the coming quarters, as BDCs prepare for potentially lower rates in 2024. TSLX management discussed this on a previous call and has set the dividend at a level that is based on the "forward interest rate curve through 2025, which is subject to changes in the market." This is another example of higher-quality management.

In the near term, we expect that net investment income will exceed our newly established base level due to our increased earnings power. However, we determined $0.46 per share to be an appropriate level based on looking at the forward interest rate curve through 2025, which is subject to changes in the market. We don't want to put ourselves in a position where we would have to cut the dividend. And so we set dividend where we see a significant cushion in the next couple of years. We were just looking at the curve.

During 2022, there were lower amounts of supplemental/specials paid partially due to increasing its regular dividend plus its NAV constraint test. However, there is a good chance that the company will pay higher amounts in 2023 related to increased fee and prepayment-related income, higher portfolio yield, the reversal of previous unrealized losses, and undistributed taxable income (“UTI”) which recently increased from $0.77 to $0.87 per share and continues to build. There will likely be another " special" dividend announced in 2023, in addition to supplemental dividends paid over the coming quarters, as management typically avoids having excessive amounts of excise tax by “cleaning out” the spillover as it “creates a drag on earnings” and “burning our returns with the excess friction costs incurred through excise tax”:

We estimate that our spillover income per share at quarter end is approximately $0.87. As part of our focus on capital efficiency, in conjunction with our board, we will review the level of undistributed income as the year progresses to ensure we minimize potential return on equity drag resulting in excise tax . At some level, this will likely require the payment of additional distributions to our shareholders similar to how we address this in 2020 and 2021.”

When calculating supplemental dividends, management takes into account a “NAV constraint test” to preserve its NAV per share:

{kind=link}

BDC Valuations

There are very specific reasons for the prices that BDCs trade driving higher and lower dividend yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage). BDCs with higher-quality credit platforms and management typically have higher-quality portfolios and investors pay higher prices. This drives higher multiples to NAV and lower yields.

{kind=link}

As a part of assessing BDCs, it's important to take into account expense ratios. BDCs with lower operating expenses can pay higher amounts to shareholders without investing in riskier assets.

“Operating Cost as a Percentage of Available Income” is one of the many measures that I use which takes into account operating, management, and incentive fees compared to available income. “Available Income” is total income less interest expense from borrowings and is the amount of income that is available to pay operating expenses and shareholder distributions .

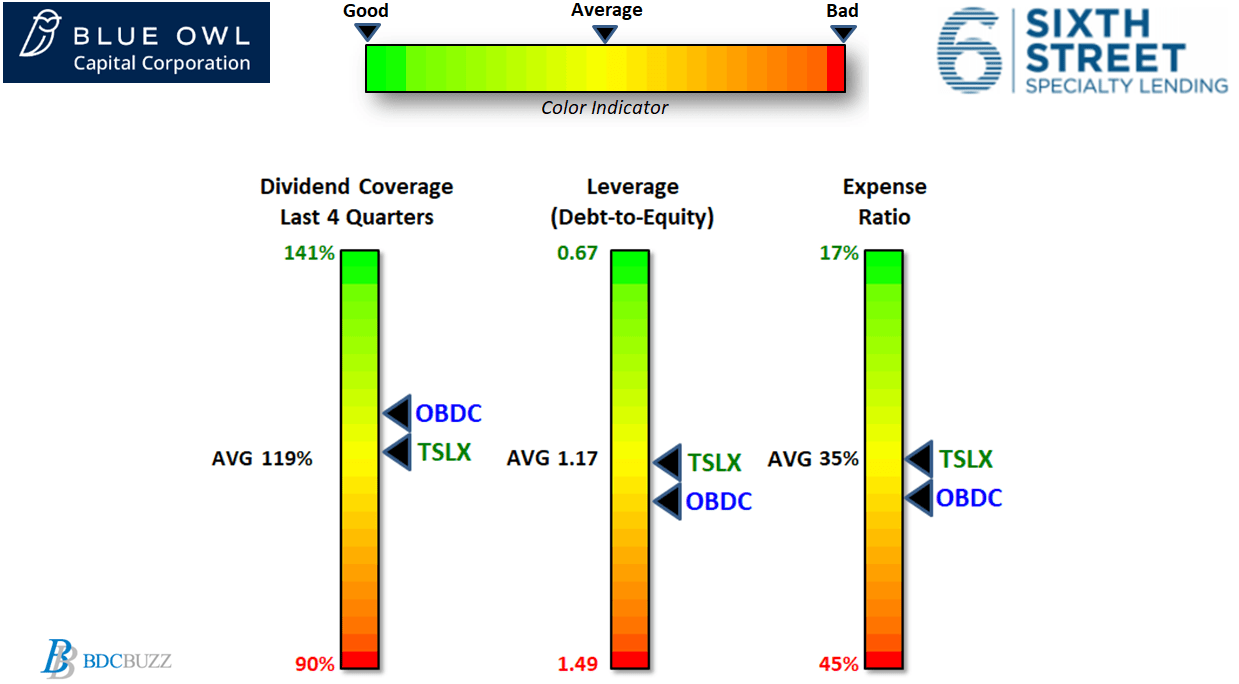

The charts below compare a few metrics for OBDC and TSLX compared to the average BDC including dividend coverage over the last four quarters, leverage or debt-to-equity, and expense ratios. As mentioned earlier, please do not focus only on historical dividend coverage especially compared to projected coverage.

{kind=link}

OBDC has slightly higher historical dividend coverage partially due to having slightly higher amounts of leverage (debt-to-equity) but also a higher expense ratio. It's interesting to note that these BDCs have similar fee agreements including a base management fee of 1.50%, incentive fees of 17.5%, and a hurdle rate of 6%, as shown below.

BDC Buzz & SEC Filings

As mentioned earlier, TSLX has increased its regular quarterly base dividend from $0.38 to $0.46 per share over the last nine years and has already paid $0.13 per share of supplemental dividends in 2023. I'm expecting another $0.11 per share of supplemental dividends over the next two quarters for total dividends of $2.08 per share in 2023 which is around 12.5% of its NAV per share ($2.08/$16.59).

OBDC is currently paying a regular quarterly base dividend of $0.33 per share plus $0.10 per share of supplemental dividends so far in 2023 and likely another $0.10 per share for a total of $1.52 which is around 10.0% of its NAV per share ($1.52/$15.15).

The average BDC was previously paying around 9% of NAV in annual dividends (also mentioned earlier) which has increased to almost 11% mostly due to the positive impacts from higher interest rates as BDC assets are primarily at floating rates. Investors pay higher prices for BDCs that pay higher dividends as a percentage of NAV per share which is why TSLX trades at a much higher multiple . Please keep in mind that BDCs that trade above NAV have the ability to issue shares at a premium which is accretive to NAV and provides capital to invest in this favorable environment.

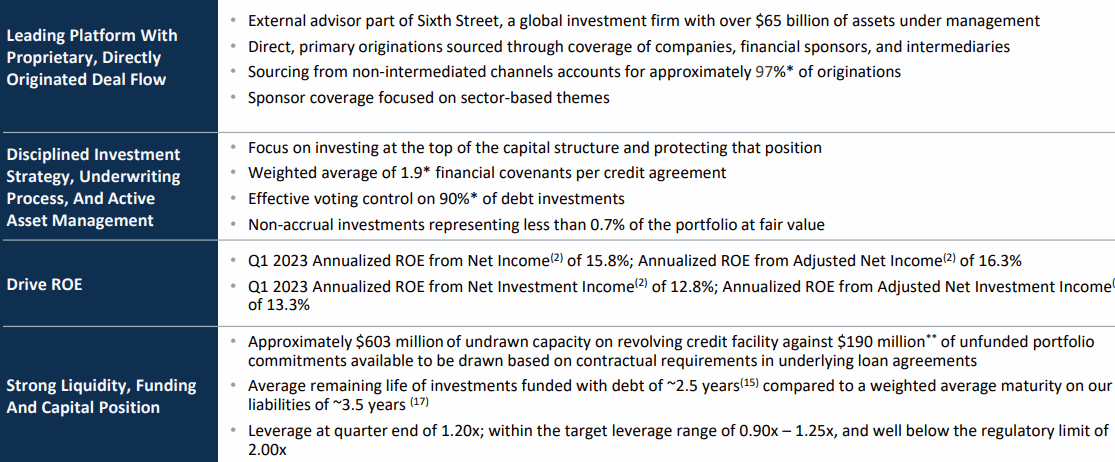

If I had to pick one of these BDCs to buy today it would be TSLX for a few reasons including being one of the highest-quality BDCs that perform well during distressed environments with management that's very skilled at finding value in the worst-case scenarios, including distressed retail and energy investments. TSLX often lends to companies with an exit strategy of being paid back even through bankruptcy/restructuring and is proficient at stress testing every investment with proper coverage and covenants. Management has prepared for the worst as a general philosophy and historically used it to make superior returns (as shown earlier). TSLX’s portfolio is 91% first-lien with an average of 1.9 financial covenants for each debt position, 82% with call protection, and 90% effective voting control.

In a following article, we will discuss TSLX's portfolio credit quality including its watch list investments.

{kind=link}

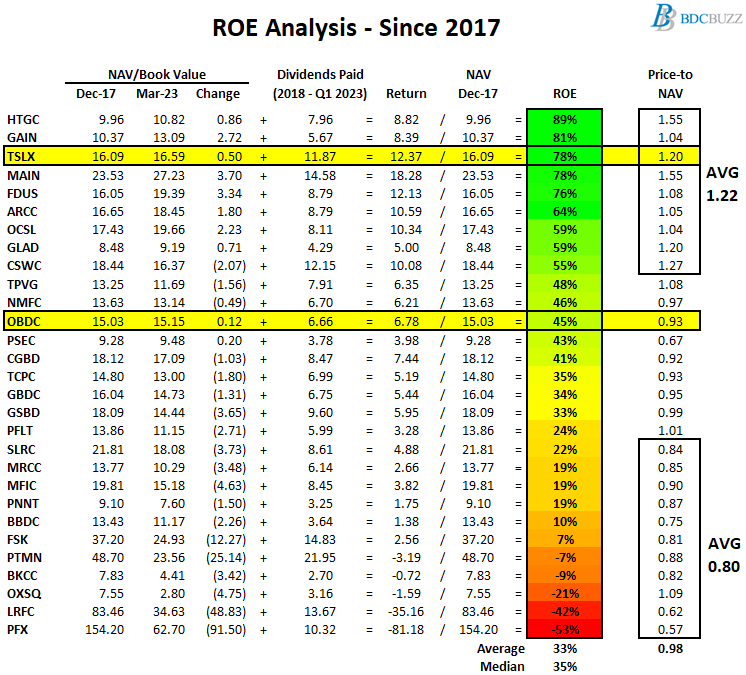

Another reason that I prefer TSLX is the following table shows the changes in NAV per share and dividends paid between Dec. 31, 2017, and March 31, 2023 , as a simple proxy for return on equity (“ROE”) to shareholders. It's important to note that many BDCs prefer not to pay special or supplemental dividends unless absolutely necessary because they directly reduce NAV per share. Also, some BDCs purposely pay lower dividends relative to their earnings, which contribute to higher NAV per share. However, this table takes these into account along with the current price-to-NAV ratios, showing that investors pay higher multiples for BDCs that deliver higher returns to shareholders .

Most of the BDCs with higher ROEs have historically held higher amounts of equity investments. However, TSLX has relatively lower amount amounts of equity positions and a much higher first-lien currently around 91% but has still delivered higher returns to investors as shown below.

{kind=link}

TSLX Important Considerations

The following are many of the positive considerations for TSLX, some of which are discussed in this article:

- Increased its regular quarterly base dividend from $0.38 to $0.46 per share (last nine years)

- Base dividend of $0.46 per share is easily covered, especially given that the company has earned an average of $0.54 per share over the last three years

- Paying supplemental and special dividends each year (since 2017)

- Bed Bath & Beyond continues to be marked up, reflecting a quicker resolution and upside earnings potential due to the “capitalized make-whole amounts, which could positively impact earnings in the range of 0 to $0.105 per share”

- Undistributed taxable income (“UTI”) increased from $0.77 to $0.87 per share

- Management has set the dividend at a level that is based on the “forward interest rate curve through 2025, which is subject to changes in the market”

- Management avoids excessive amounts of excise tax by “cleaning out” the spillover/UTI

- Upcoming supplemental dividends due to overearning the dividend

- Reduced leverage due to recent equity offering and repayment of Bed Bath and Beyond

- Investment grade ratings by S&P (BBB-), Moody’s (Baa3), Fitch (BBB), Kroll (BBB+)

- No near term maturities of borrowings with the earliest occurring November 2024

- Relatively lower amounts of non-cash/PIK income

- Portfolio is 91% first-lien, with an average of 1.9 financial covenants for each debt position, 82% with call protection, and 90% effective voting control

- NAV per share has increased by 6.6% over the last 3 years (better than most)

- Net realized gains of over $50 million or around $0.61 per share over the last four years

- Only 0.7% of portfolio investments at fair value on non-accruals status

- Very low amount of "watch list" investments that remain under 5% of the portfolio

- Around 99% of the portfolio debt investments at variable rates

- Diversified portfolio with the top 10 investments accounting for 25% of the portfolio

- Conservatively marked portfolio (higher quality reported NAV)

- Management focused on ROE with the ability to earn higher returns through investing in distressed retail ABL and energy investments

The following are many of the negative considerations for TSLX, some of which are discussed in this article:

- Added another first-lien loan with American Achievement to non-accrual status (along with its other positions that were previously on non-accrual)

- 100% of borrowings are at variable rates (this is a positive if rates head lower) due to swaps on its lower cost fixed rate debt (from matching assets and liabilities)

- Higher cost of borrowings (for the reasons discussed above)

- Recent decline in stock price partially due to the recent equity offering

- Only 6.0% hurdle rate before paying incentive fees, partially responsible for its average expense ratios

- Lack of "total return" hurdle or "look back" provision when calculating income incentive fees to protect shareholders from capital losses

For further details see:

Solid 10% Yield From Blue Owl Or Sixth Street?