DTC - Solo Brands: Assessing The Company's Worth Ahead Of Upcoming Q3 Earnings

2023-11-03 03:53:01 ET

Summary

- Solo Brands operates in the consumer discretionary sector, selling outdoor products through a direct-to-consumer platform and retail partners.

- The company's stock price has dropped significantly since its IPO, which may make it now attractive to value investors.

- Solo Brands has strong liquidity and working capital, but its long-term assets and liabilities pose risks. Growth is necessary to sustain share-price gains.

Intro

Solo Brands, Inc. (DTC) operates in the consumer discretionary sector, using a direct-to-consumer platform to get its products to market. The US-based company sells the likes of camp stoves, fire pits, paddle boards, and kayaks (under a variety of different brands) through both its digital network as well as through multiple retail partners. Since most sales continue to come through the company's direct-to-consumer digital platform, one of Solo Brands' forward-looking objectives is to significantly rachet up the number of wholesale & retail partners, especially in international markets.

This company came across a screen we ran where the objective was to find profitable companies, with low debt and low valuations to boot. Although Solo Brands' earnings are not much cheaper than what the sector is offering at present, the company's stated sales, assets, and cash flow multiples all come in significantly lower than the average as we see below.

| Multiple |

| Solo Brands - (Trailing) |

| Sector Average |

| Price To Earnings (GAAP) |

| 12.35 |

| 14.65 |

| Price To Sales |

| 0.47 |

| 0.77 |

| Price To Book |

| 0.62 |

| 1.9 |

| Price To Cash-Flow |

| 2.29 |

| 7.53 |

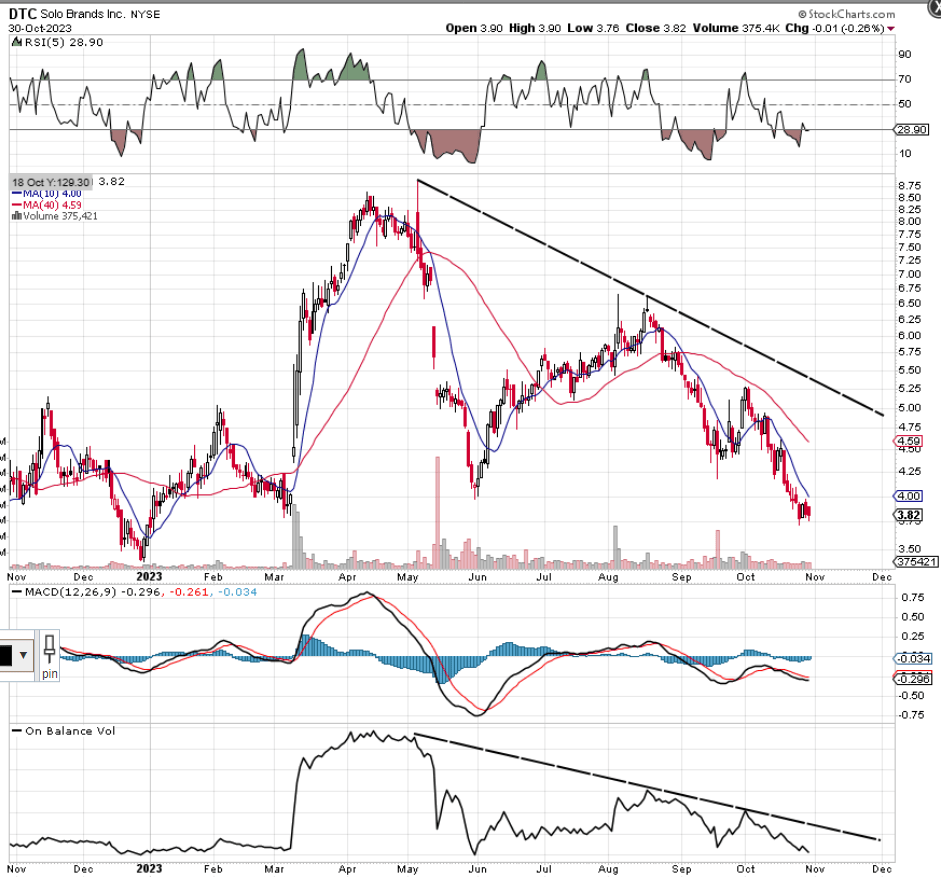

As we see from the chart below, the secondary offering which took place in early May was the catalyst that spurred the share price into making lower lows over the past six months or so. Shares fell 10%+ on the day of the announcement where shares were offered at $5.25 a share. Suffice it to say, given how the company remains light-years off its IPO price of $17 a share, value investors (considering the company remains profitable) may be enticed by Solo Brands at these bargain basement levels.

DTC Technical Chart (Stckcharts.com)

{kind=link}

Q2 Trends

Although Solo's revenues slightly missed estimates in Q2, GAAP earnings of $0.12 a share beat consensus by $0.04. Management as they put it decided to 'lean' into the momentum it was achieving in the wholesale business where the company continues to sign up new retailers and gain additional shelf space to boot. Because of the momentum garnered in 'Wholesale', management pared back its advertising spend in digital which is understandable for the following reason.

Solo Brands now sees far more potential for growth in the 'wholesale' business especially in international markets where partnerships are virtually untapped. Wholesale grew its sales by 57% in Q2 whereas direct-to-consumer fell by 14%. The line of thinking here from management's viewpoint is that growth in 'wholesale' will improve customer awareness surrounding Solo's brands over time. While this may be true, going this route presents several risks such as the following.

Firstly, since the retailer needs to get his cut, margins are invariably lower than the direct-to-consumer route. Furthermore, Solo has FAR less control in that retailers will always do what is best for them to drive their profitability. This begs the question of whether Solo would be able to compete aggressively in a down market for example. At present, Solo's net profit margin comes in at 3.37%. Although innovation regarding new products can always add value, the question is whether Solo Brands would be strong enough to compete successfully in a downturning wholesale market. Apart from lower margins, Solo's receivables for example (due to looser payment terms) could increase meaningfully on the wholesale side. These are areas that investors should research going forward.

Therefore (taking into account Solo's attractive valuation ), let's delve into the company's balance sheet to see if we can gain insights into what this company is worth in the grand scheme of things.

Current Ratio (Liquidity)

Strong liquidity in a company is crucial as it demonstrates the availability of sufficient capital which in turn would keep operations going if earnings (for whatever reason) were to come to a grinding halt. At the end of Q2 , DTC's current assets came in at $211+ million of which cash & equivalents ($60.6 million) and inventory ($113.7 million) were the biggest line items in this section. Concerning current liabilities (obligations that are due within the following 12 months), management reported a figure of $68.2 million at the end of Q2 of which accounts payable ($13.9 million) & accrued expenses ($23.7 million) were the biggest current liability line-items in this section. Therefore DTC's current ratio (current assets / current liabilities) comes in at 3.10 which demonstrates that the company has ample liquid assets to cover its near-term obligations. Furthermore, working capital at the company continues to grow, and inventory ($113.7 million at the end of Q2) levels have remained consistent in recent years whereas sales due to multiple acquisitions have continued to grow. These are encouraging trends from a working capital standpoint.

Long-Term Assets & Liabilities

When we turn to DTC's long-term assets section, we see that goodwill ($374.9 million) & intangible assets ($230 million) are the largest line items by far in the company's long-term asset section. Goodwill is the 'fat' over book value DTC has paid on previous acquisitions whilst intangibles come from the likes of brands, copyrights & trademarks which have been bought from third parties and are reported on the balance sheet at their fair market values. Net property, plant & equipment for example ($54 million) only make up 8%+ of the company's long-term assets which is a trend that must be watched for the following reasons.

If past acquisitions do not live up to their billing, goodwill over time tends to get dialed down in value due to 'expectations' for whatever reasons not being fulfilled. Furthermore, intangible assets' value can be very difficult to determine over time, and many times have a finite nature to their value. Suffice it to say, given the uncertainty that exists with the long-term value of DTC's goodwill & intangible assets, if we were to remove these line items, the company's total assets would only come in at a drastically reduced $266.3 million.

On the long-term liability side, we see that this section's largest line item (long-term debt of $136.3 million) continues to inch upward which may indicate a growth problem. Long-term liabilities come in at $229.8 million whereas DTC's total liabilities came in at $298 million at the end of the company's most recent second quarter.

Therefore, by subtracting the company's liabilities from its asset take (which we have modified), we get a negative adjusted shareholder equity number of $31.7 million. Suffice it to say, when we work off this number, both the company's book multiple and debt-to-equity ratios would be null & void. To reiterate, we removed the company's intangible assets to get DTC's equity value down to brass tacks in terms of how much equity could be realized today . Although the company's goodwill & intangible assets are worth a lot of money, investors should remember that they are very much forward-looking metrics meaning their true value (which should show up in earnings growth) still has to be proven.

Growth Expectations Need To Be Realized

As alluded to above, Solo Brands with trailing net earnings of $17.5 million, trailing sales of $518.5 million, and a current market cap of $216.28 million, currently trades with an attractive trailing GAAP earnings multiple of 12.35 & a very low trailing sales multiple of 0.42. However, given the number of intangible assets on the balance sheet as well as the company's significant debt (where the present earnings run-rate would take almost eight years to pay off the long-term debt load), growth is now a prerequisite to ensure sustained share-price gains.

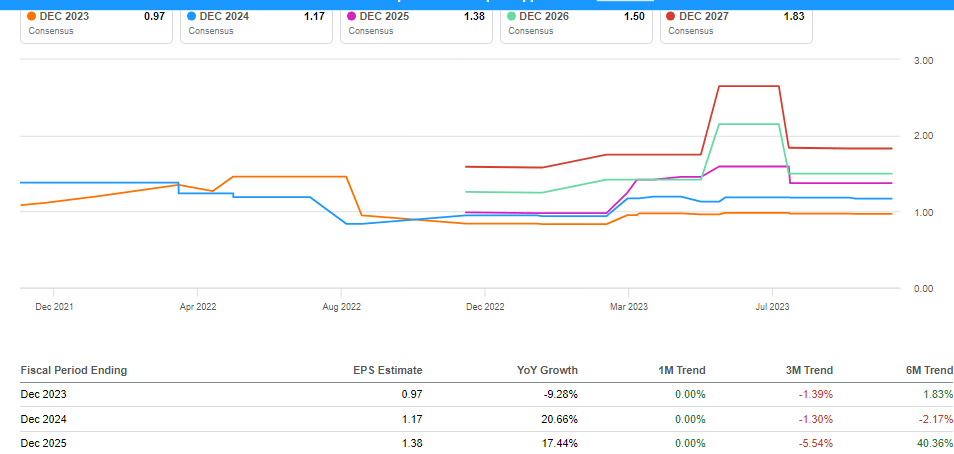

As we see below, robust bottom-line growth is certainly expected both this year and next but that $1.17 normalized EPS estimate for next year could easily be dialed down further in upcoming months. Therefore, we recommend investors watch quarterly earnings numbers (starting with Q3 numbers next week) very closely as shares of DTC will predominantly trade in alignment with its projected growth rates going forward.

Solo Brands Consensus EPS Revisions Trend (Seeking Alpha)

{kind=link}

Conclusion

To sum up, although value investors may be attracted by Solo Brands' low valuation and expected growth path, high intangible assets, and high debt mean the company has to at least meet its numbers to keep the stock elevated. Furthermore, being a micro-cap stock, failure to meet its growth projections may result in aggressive selling due to the below-average number of shares traded in this play. DTC looks close to its fair value as we head into the company's Q3 earnings numbers. We look forward to continued coverage.

For further details see:

Solo Brands: Assessing The Company's Worth Ahead Of Upcoming Q3 Earnings