DTC - Solo Brands: Stellar Growth Expected Eyeing The Consumer

2023-08-17 11:32:53 ET

Summary

- Strong US retail sales in July indicate continued consumer spending and diminishing excess savings.

- Solo Brands (DTC) is recommended for investment due to its modest valuation, strong EPS growth outlook, and favorable technical setup.

- Potential risks for Solo Brands include competition, reliance on a small range of products, and challenges with senior management tenure.

- I outline key price levels to watch as the second half unfolds.

It was a July heat wave in terms of the recent Advance Retail Sales report published by the US Census Bureau. Consumers keep on spending and excess savings continue to dwindle. With positive real wages, though, there's little cause for concern for now. Could that change once the student loan moratorium ends and if we see a tick-up in the unemployment rate? Maybe, but so far so good on the consumer front.

Strong US Retail Sales in July

EY Parthenon, Sober Look

I reiterate my buy rating on Solo Brands ( DTC ) for its modest valuation, stellar EPS growth outlook, and a favorable technical setup.

According to Bank of America Global Research, DTC is a Direct to Consumer platform that offers products through a portfolio of Leisure brands including: (1) Solo Stove (64% of 2020 Pro Forma revenue) - a provider of premium, smokeless fire pits, camp stoves, and grills, (2) Chubbies (21% of Pro Forma Revenue) - a digitally native casual & activewear brand, (3) Isle (10% of Pro Forma Revenue) - paddle board brand, & (4) Oru Kayaks (6% of Pro Forma Revenue) - origami folding kayaks that can be stored in car trunks, closets.

The Texas-based $567 million market cap Leisure Products industry company within the Consumer Discretionary sector trades at a high 23.6 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend. Following its Q2 earnings report earlier this month, DTC has a high 72% implied volatility percentage, and the stock carries a short interest of 3.9%.

Earlier this month, Solo Brands issued better-than-expected Q2 adjusted EBITDA of $25 million along with strong wholesale revenue ($31.3 million compared to an expected $21.9 million, BofA notes). Non-GAAP EPS verified at $0.22 versus the $0.21 consensus while sales fell 4% year-on-year. Its gross margin declined slightly compared to the previous year amid a shift in channel mix and fewer promos in the D-T-C channel.

Despite near-term pressure in this channel due to reduced digital advertising spending and delayed new product launches, I assert the growth trajectory appears strong. The company's long-term potential lies in its innovative products, international expansion, and growth into new categories. Helping to send the stock higher around the Q2 report was a raise of its adjusted EBITDA margin target from 16.5%-17.5% to 17%-18%.

Looking back on price action earlier this year, shares rose big following the Q4 earnings report in March but then fell back in May after the company issued an equity offering . But the stock looks cheap to me, as I will outline, and momentum has returned.

Potential risks for Solo Brands include the potential for wholesale growth to outpace direct sales, affecting gross margins more than expected. The company also faces challenges with short average senior management tenure and a heavy reliance on a small range of fire pit products for Solo Stove's revenue. Moreover, competition from established grill-makers, smaller fire pit brands, and larger activewear/outdoor companies could potentially impact the long-term prospects of Solo's brands.

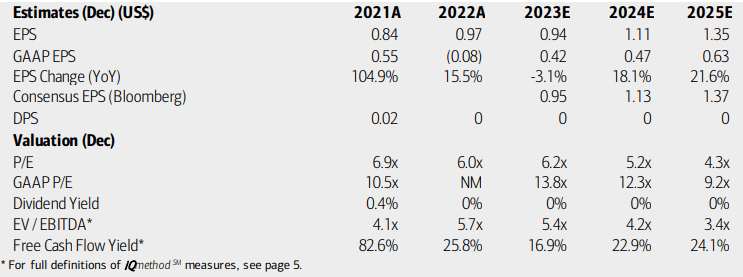

On valuation , analysts at BofA see earnings falling modestly this year before per-share profit growth accelerates in 2024 and sustains a high growth level in 2025. The Bloomberg consensus forecast is about on par with what BofA projects. Despite high free cash flow, no dividends are expected to be paid by the company. Still, both its operating and GAAP earnings multiples appear attractive while DTC's EV/EBITDA ratio is less than half that of the broader market.

Solo Brands: Earnings, Valuation, Free Cash Flow Forecasts

{kind=link}

Digging in further, there isn't much history with Solo Brands to use for a relative valuation to itself, but we can compare the stock to its sector to determine if it is a solid value. With just a 6.5 forward non-GAAP P/E, it trades at a more than 40% discount to the sector median. Moreover, shares sell at an enormous discount when eyeing the forward price-to-book ratio. Overall, given its robust growth trajectory, if we assume $1.00 of EPS over the next 12 months and apply a conservative 12 multiple, then the stock should be near $12. The low P/E is perhaps warranted given where other D-T-C peers sell for.

DTC: Compelling Valuation Metrics

Seeking Alpha

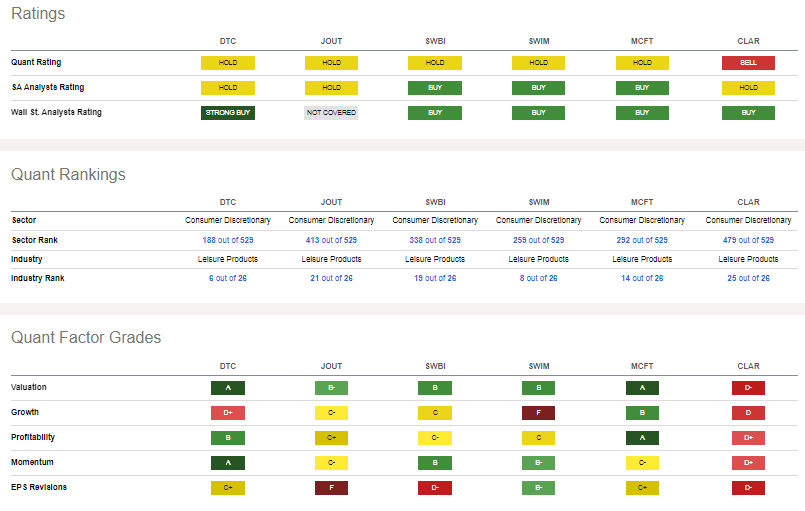

DTC has one of the best valuation ratings relative to its peers while its share price momentum is best in breed. Don't be deceived by the growth rating as this year's EPS dip should be temporary. What's more, high profitability is something not many other D-T-C Driven Lifestyle Brands / Leisure Brands & Retailers industry firms can boast.

Peer Comparison

{kind=link}

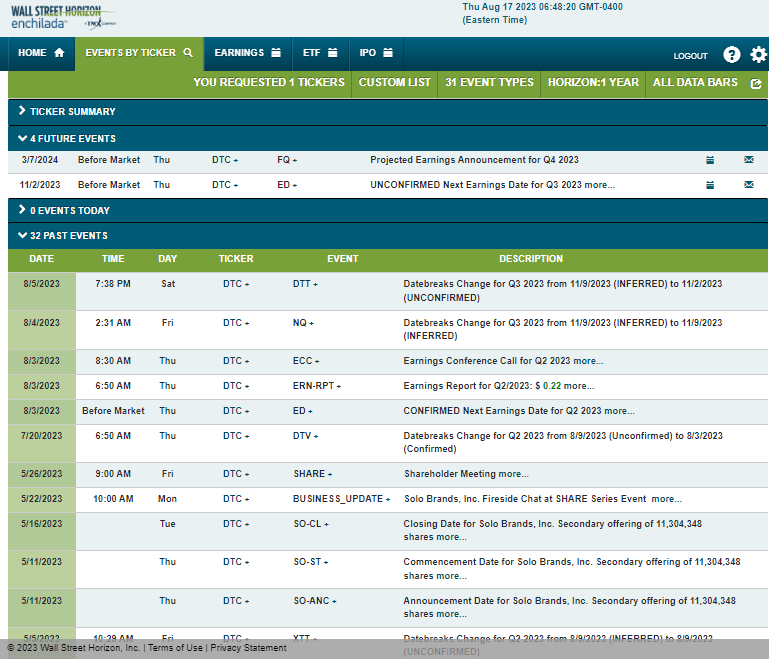

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q3 2023 earnings date of Thursday, November 2 BMO. The calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Risk Calendar

{kind=link}

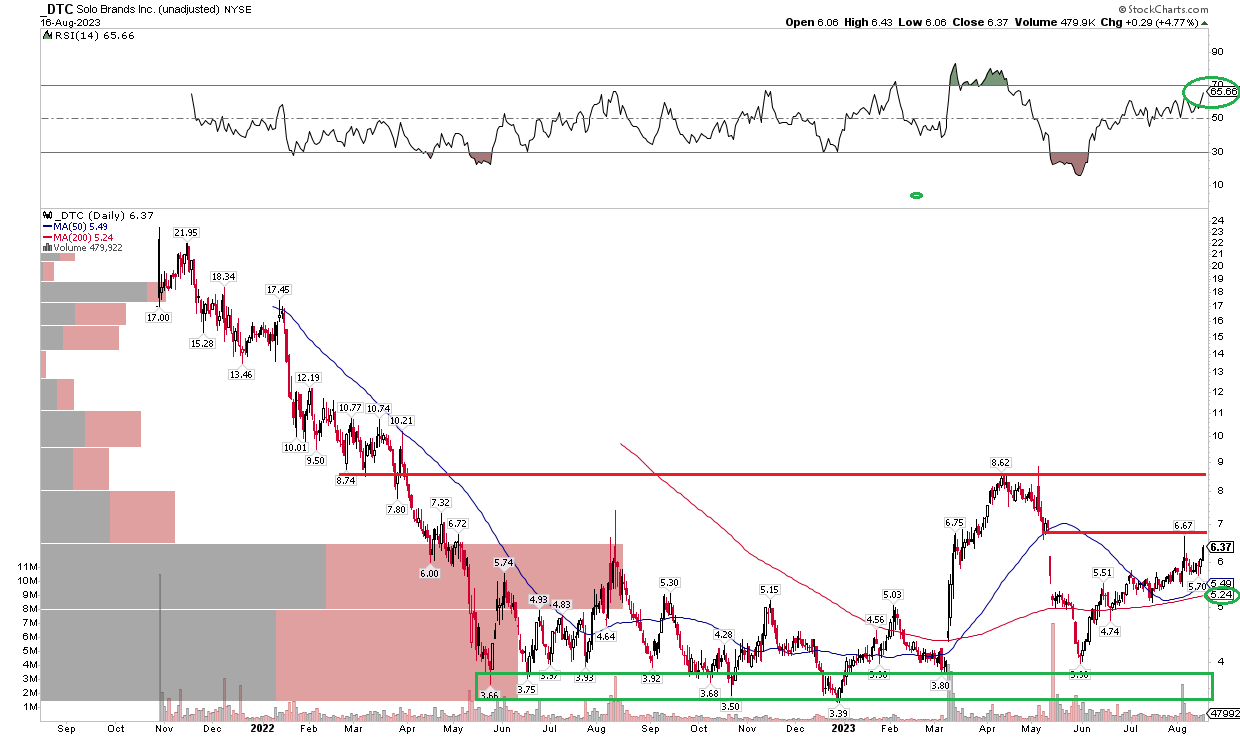

The Technical Take

After plunging following its debut in late 2021, DTC found an eventual floor in the $3s. I was bullish on the stock late last year , and that proved to be a solid call. But where do things stand today from a technical point of view? Well, notice in the chart below that the stock has been on the rise after a major gap down related to the aforementioned equity offering in May. The rally has been impressive in my opinion given that the RSI momentum indicator at the top of the chart just made a fresh rebound high and considering that the long-term 200-day moving average is now positively sloped.

But I see resistance at two notable levels. First, we have the gap-fill level just below $7 - that's precisely where selling intensified earlier this month after the post-earnings pop - it is a good reminder to pay attention to key technical spots. There's longer-term resistance, however, at the $8.62 mark - the April peak. On the downside, a stop under the 200dma and the range-highs from late 2022 through early 2023 appears prudent.

Overall, the chart is constructive given that we have generally seen higher lows off the December bottom last year.

DTC: Spotting Upside Resistance, But Momentum Remains Strong

{kind=link}

The Bottom Line

I reiterate my buy rating on DTC. Its valuation appears great given the growth outlook while the technical picture has its headwinds, but Solo Brands still looks to be in an uptrend.

For further details see:

Solo Brands: Stellar Growth Expected, Eyeing The Consumer