SPR - Spirit AeroSystems: The Bull Buy Thesis Fades

2023-08-15 09:28:02 ET

Summary

- Spirit AeroSystems Holdings, Inc. has shown disappointing results and is being kept afloat by customers like Boeing through repayable funds.

- The company's growth driver, the Boeing 737 program, has underperformed, and other programs are loss-making without prospects of cash or profit generation.

- Spirit AeroSystems has experienced increased losses and margin decline, and its targets for margins and free cash flow are in doubt.

Spirit AeroSystems Holdings, Inc. (SPR) is one of the stocks I have marked as a stronger buy compared to the OEMs in the past. While I believe Spirit AeroSystems will do better going forward, the company has shown disappointing results getting itself from one problem into another, and in the process it is being kept afloat by customers including The Boeing Company (BA) via repayable funds.

The company previously aimed to return to 16.5% margins and 7 to 8 percent free cash flow margins, but for quite some time on the back of inflation and now with a new labor contract in place, those targets are in doubt. Meanwhile, we do see continued cost growth and forward losses on some programs which leaves the Boeing 737 as the sole big commercial airplanes cash cow. In this report, I discuss the most recent quarterly results and provide a valuation for Spirit AeroSystems.

Spirit AeroSystems News: Improvement In Shipset Deliveries

{kind=link}

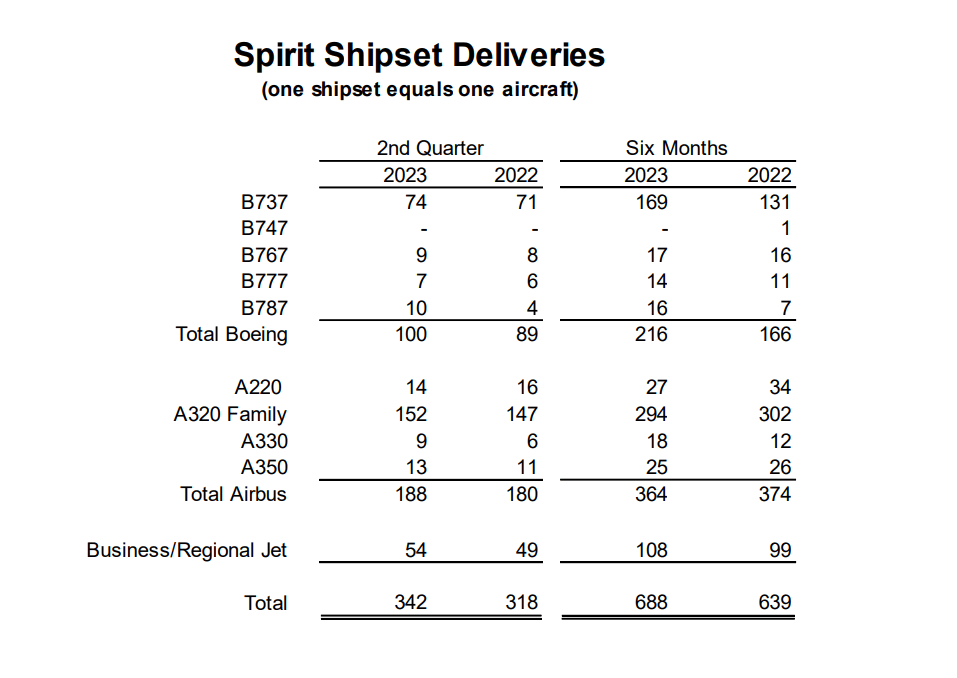

The difficult business and news flow of Spirit AeroSystems is that against every piece of good news, seemingly there are multiple negative items. The Boeing 737 program should be the growth driver for Spirit AeroSystems, and the company has started increasing the production rate to 42 shipsets per month at the start of August. However, we do see that due to a work stoppage and the vertical fin issue, year-over-year Spirit was only able to increase Boeing 737 shipsets by three units which is simply poor performance.

The company also has the Airbus A220, Airbus A320neo, Airbus A350 and Boeing 787, but these programs are loss-making programs without any tangible prospect of cash or profit generation. It barely helps generating a strong bullish thesis for Spirit AeroSystems despite its diversification in the commercial airplane industry as well as expansion in defense and aftermarket.

Spirit AeroSystems Back In The Red

{kind=link}

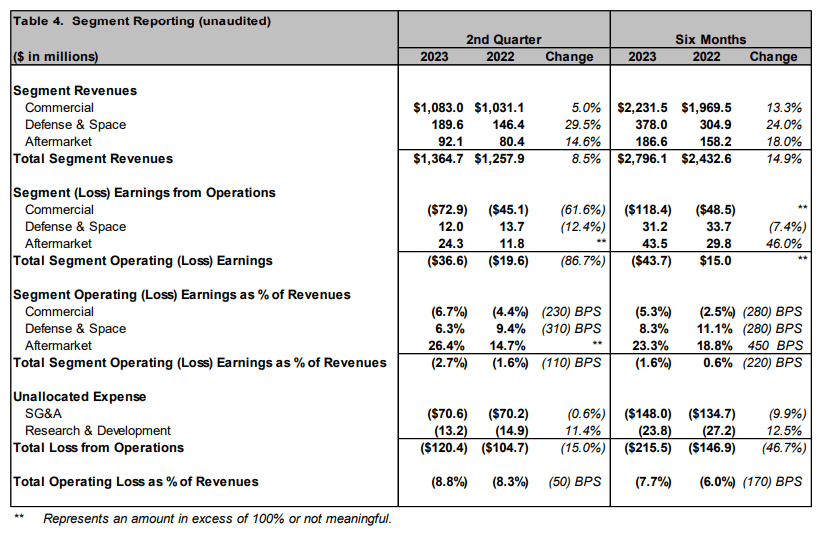

For the Commercial segment, revenues increased 5%, which was lower than the 7.5% increase in commercial shipments. During the quarter, Spirit recognized a $23 million contra-revenue charge to account for the costs associated with rectifying the vertical fin issue on the Boeing 737 fuselages that were already shipped to Boeing. Excluding this charge, the revenue growth would be more in line with the shipset growth for the second quarter. Defense & Space revenues grew almost 30% driven by P-8A Poseidon and development program volumes while after-market sales grew 15% as spare parts sales and services remained strong.

While revenues grew 8.5%, Spirit AeroSystems saw its losses increase by more than 85% on segment earnings level and 15% higher losses from operations with margins declining from negative 8.5% to negative 8.8%.

The commercial segment saw $23 million contra-revenue charges to account for repair costs to date on fuselages already delivered to Boeing. Furthermore, Spirit shared that the fuselage repairs in their own facilities were completed within the estimated $31 million meaning that another $17 million in additional costs were charged in Q2 2023. Spirit expects no substantial additional costs from rework on in-fleet airplanes, which is a positive, but the wording of its contra-revenue charge suggests there could be further costs as the repairs on the fuselages already delivered to Boeing are completed.

Furthermore, there were $7.3 million in strike related costs, $38 million in forward losses charged on the Boeing 787 program due to the new IAM union contract and increased input costs, while costs for the A350 increased by $28 million and $27 million for the A220. If we were to add back these costs to get an adjusted margin, we would see a profitable segment at a 3.7% margin and 8.4% if we were to add back the excess capacity costs that the company is currently carrying.

In the defense segment, there was a 310 basis points margin contraction driven by cost growth on the P-8, KC-46 tanker and CH-53K which brought a nearly 460 basis points margin pressure. The entire business would have been breaking even including excess capacity costs and would have a 4% margin including excess capacity costs. What this basically means is that the company is carrying significant costs as it has tooling in place to produce more than what it currently does. On the Boeing 737 program, the rate will increase to 42 this month if that has not happened already, but the company will also feather in blanks into the production system which will bring the Boeing 737 rate effectively to 35 per month.

So, the entire business will see improvements mostly into the next year but many programs are not profitable without a clear sight on when that will happen or whether that will ever happen and that leaves the Boeing 737 program as the sole cash cow for Spirit AeroSystems next to higher sales targets in defense and aftermarket. The way I view it is that the company is working on the A220, A350 and Boeing 787 without and prospects of profit in the near future.

For 2023, Spirit AeroSystems previously anticipated around 420 Boeing 737 shipset deliveries but that has now been reduced to 370 to 390 units which will significantly lower the free cash flow for the year as well as revenues. The company now expects full year free cash flow usage of $200 million to $250 million guiding basically flat on free cash flow for H2 2023.

Is Spirit AeroSystems Stock A Buy?

{kind=link}

The investment thesis for Spirit AeroSystems has been rather straightforward: As production rates would go up, the unit profits and total profits on the Boeing 737 program would go up while on other programs the unit losses would reduce as Spirit AeroSystems could amortize fixed costs over a bigger number of shipsets. The business should have been able to get back to 16.5% margins with 7 to 9 percent free cash flow margin. However, inflation and higher input costs have significantly deteriorated the picture and Spirit AeroSystems seems to be unable to negotiate a way out of OEM pressure which leaves the company a long stretch away from its targets and for the foreseeable future we don’t see major success for the company in the commercial airplane industry other than on the Boeing 737 program.

Defense and aftermarket sales should provide some tailwind as well, but there is extremely little reassurance that the continued cost growth the company already faces will not repeat. I added the expectations for Spirit AeroSystems in my model and based on those numbers and the fresh pressures faced there is no upside this year with around 20% upside into next year, which I believe warrants a rating downgrade from Buy to Hold.

Conclusion: Spirit AeroSystems For The Patient Investor

For a long time, Spirit AeroSystems stock looked like the no-brainer to capitalize on the Boeing 737 MAX production ramp up and that still remains the case but the picture is becoming significantly more clouded by continued cost growth on other programs and the seemingly weak position Spirit has in negotiations with OEMs which leads to the company absorbing losses instead of generating value on some key commercial airplane programs. That itself is not new, but the fact that the company likely will remain in an unclear and troublesome position for some years with pressure on free cash flow generation is disappointing.

As a result, I am downgrading the stock from Buy to Hold with the note that over the long term Spirit AeroSystems will likely generate value again, but at this point there is simply too much uncertainty on the timelines and financial performance.

For further details see:

Spirit AeroSystems: The Bull Buy Thesis Fades