SPSC - SPS Commerce: High Quality Company Set For Explosive Growth But The Stock Is Just Too Expensive

2023-07-26 03:48:13 ET

Summary

- SPS Commerce in the past 5 years saw sales rise by a CAGR of 15%, EBIT by 45%, and the forecast calls for more double-digit growth.

- Despite impressive growth, SPSC stock looks overvalued, trading at 100x earnings, 13x sales, and its EV/EBIT ratio of 87 is about 350% higher than the sector median.

- The cloud-based EDI provider is well-positioned for long-term growth, however, with a network of 115,000 customers and strategic footholds in retail giants like Walmart, Costco, Amazon, & Kroger.

SPS Commerce, Inc. ( SPSC ) has seen revenue grow by a CAGR of 15% over the past five years, with operating income growing at a 45% clip, and the forecast calls for even more double-digit growth. The stock has great momentum as well, but may be running too hot, as it is now trading at over 100x earnings and 13x sales. Moreover, its EBIT ratio is more than 360% above the sector median and 30% over the stock's 5-year average. That said, although now is not the right to buy, the stock is worth holding onto given the debt-free company's growth path on all levels. Through its retail cloud services and supply chain data integration products, the company has strategic footholds in companies like Walmart and is well positioned for long-term growth. It also has an impressive earnings record, beating EPS and revenue targets every year since it went public in 2010.

Company & Market

SPS Commerce, headquartered in Minneapolis with about $500 million in annual sales and over 2,200 employees, is a full-service provider of cloud-based electronic data interchange ((EDI)) solutions that primarily connect retailers, grocers, distributors, and logistics firms. It was originally incorporated as St. Paul Software, Inc. in 1987 before becoming SPS Commerce in 2001. 80% of its employees are based in the United States, with the remainder located in Australia, Canada, New Zealand, the Philippines, and Ukraine, while about 80% of sales is derived from U.S.-based customers, although the company is looking to expand globally.

The company provides EDI technology and integration services that help customers automate and streamline order fulfillment and other business processes across the entire supply chain. The primary service offering, called SPS Commerce Fulfillment, drove about 86% of company sales in Q123 . The remainder derived from analytics and product data management solutions.

In addition to implementing the EDI product itself, which includes integration with trading partners, the company dedicates staffing resources to customize and operate the technology on behalf of customers. The company has pre-built EDI integration solutions compatible with ERP, order management and e-commerce systems from dozens of software and 3PL providers including Oracle, SAP, Microsoft, and Shopify.

{kind=link}

SPS operates within a highly fragmented, rapidly changing market. It goes head-to-head with major traditional "on-premise" software firms, such as IBM Sterling and OpenText, who provide EDI integration services but offer managed solutions as opposed to full-time services. SPS has sized its total addressable market at $5 billion.

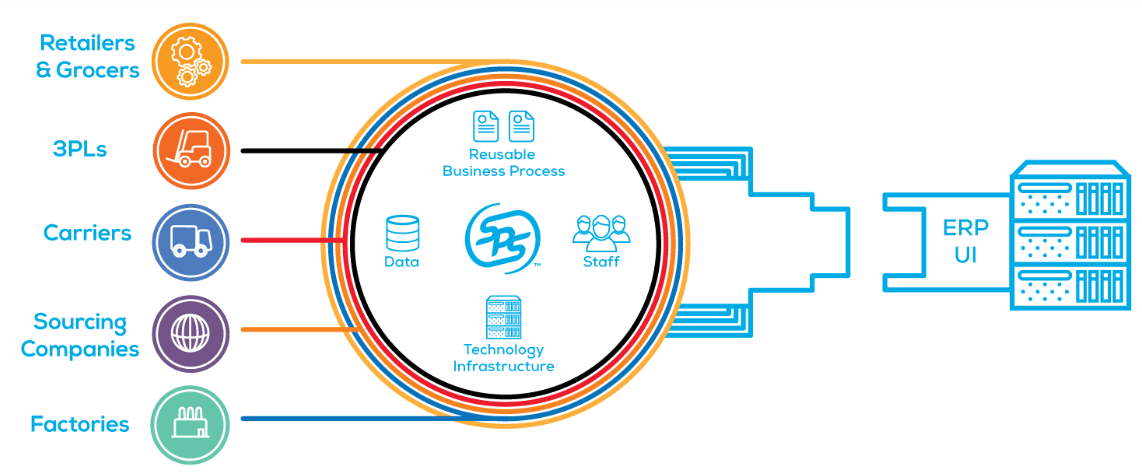

SPS says it has the world's largest cloud retail network, consisting of more than 115,000 customers , including industry giants like Walmart, Costco, and Walgreens. The growth model is impressive - once it gets a foothold in a certain company, it can penetrate, market and sell its products and services up and down the entire retail supply chain.

SPS Customer Network (SPS Q123 Investor Presentation)

{kind=link}

Performance

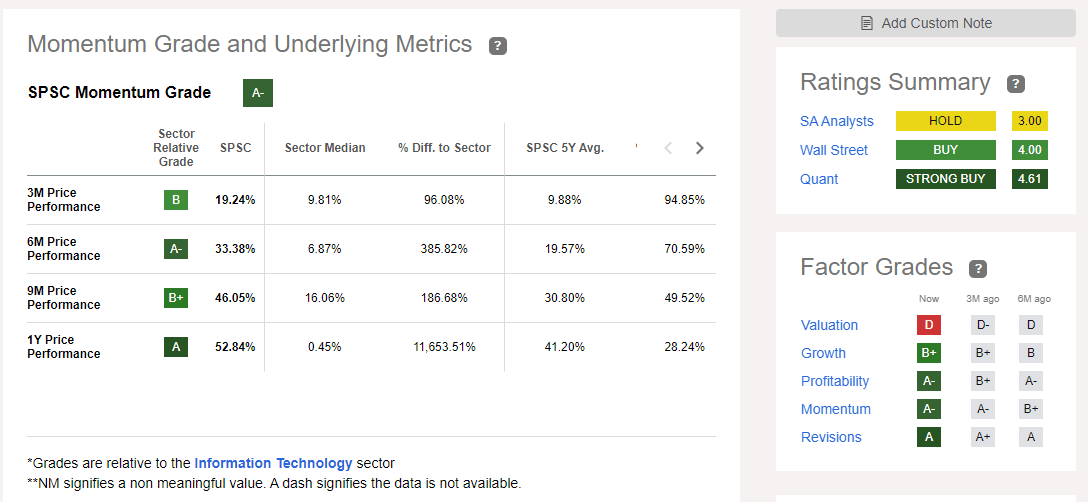

In addition to impressive growth figures and profit margins, SPS's stock currently has great momentum, outperforming the sector median handily over the past 3, 6, and 12 months, which is why it is considered a "strong buy" according to Seeking Alpha's quant scores.

SPS Momentum and Quant Ratings (Seeking Alpha)

{kind=link}

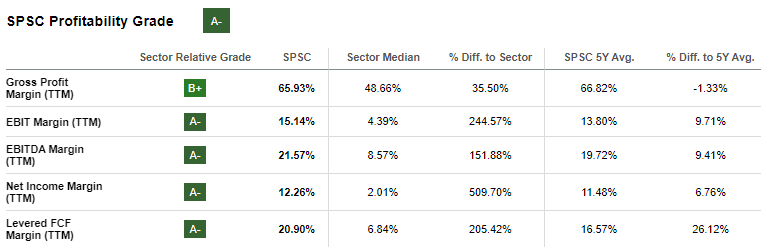

The company has recorded in the trailing twelve months gross profit margins of 65%, EBITDA of 21% and levered cash flow margins of 22%. Its EBIT margin of 15% is 244% higher than the sector median.

SPS Profitably Grade (Seeking Alpha)

{kind=link}

The company also has ambitious plans to continue growing profits - with a long-term EBITDA target of 35%. Although quite a stretch, based on its track record, it would not be surprising if they achieved it.

The company is set to report earnings on post-market on July 27, and it is probably a safe bet they will deliver. They have beaten EPS and sales targets every year since 2010. I tend to put more weight on beating sales targets actually, given that EPS numbers can be manipulated by moves like buybacks. In any case, the track record is awe-inspiring.

SPS Earnings Surprises (Seeking Alpha)

Based on all the performance metrics available, one can see that there is a good reason why the stock is trading at insane multiples.

Valuation

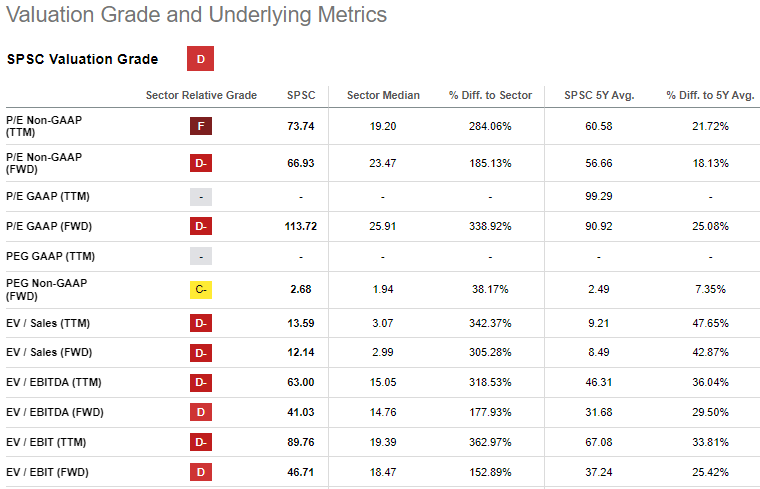

Is there really ever too much of a good thing? In this case, there might be. Despite the company appearing stellar in every conceivable way, the stock is just too expensive for my tastes from both a relative and intrinsic valuation perspective. SPS is trading at 113x forward earnings and 46x EV/EBIT.

SPS Valuation Grade (Seeking Alpha)

{kind=link}

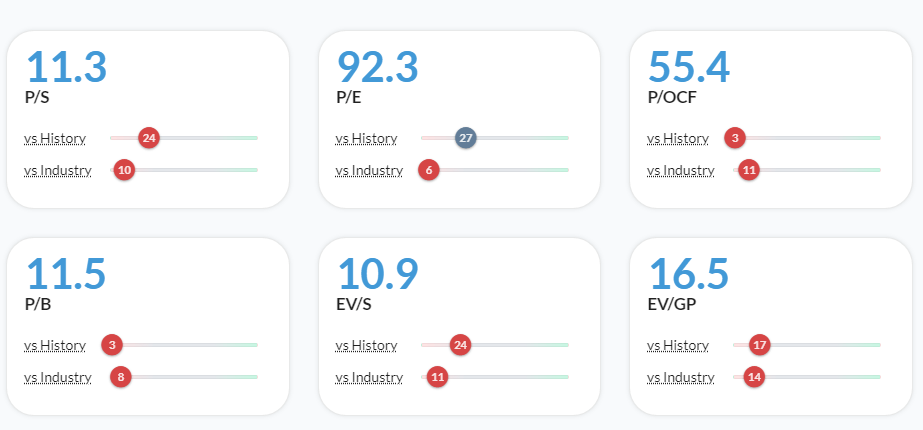

The folks at Alpha Spread's layout on this, shown below, really underscores the overvaluation. Based on an 11.3 P/S ratio, for example, SPS's stock is priced cheaper than only 10% of companies in the technology industry. Put another way, SPS's stock is more expensive from a relative standpoint than 90% of tech industry companies, based on the price to sales ratio. Despite the impressive profit margins, the EV/gross profit ratio of 16.5 implies that only 14% of tech companies are trading at a cheaper price.

SPS Valuation Metrics (Alpha Spread)

{kind=link}

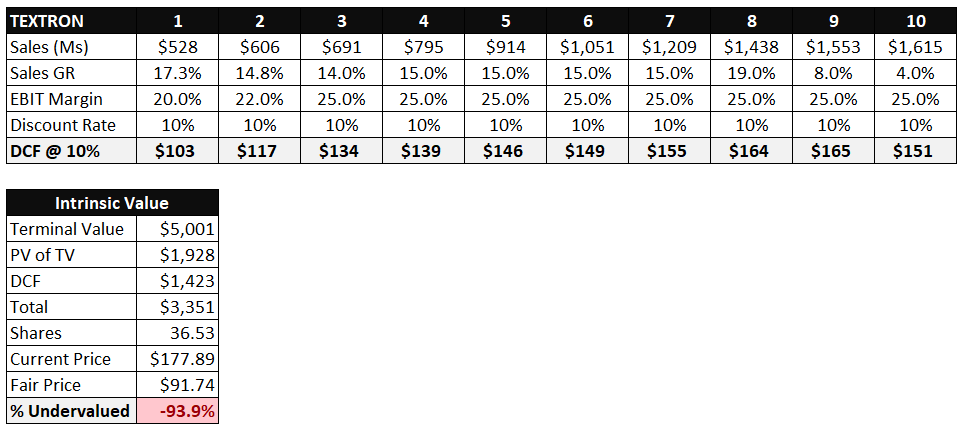

And based on a DCF analysis, the stock looks overvalued by over 90% if I use a discount rate of 10%, which is roughly the unadjusted 30-year annualized return of the S&P 500 (dividends included). I assume double-digit sales growth through year seven before gradually lowering and I assume SPS will hit their ambitious profit margin goals, so I pushed EBIT to 25% for years 3-11.

SPS DCF Analysis (MH Analytics)

{kind=link}

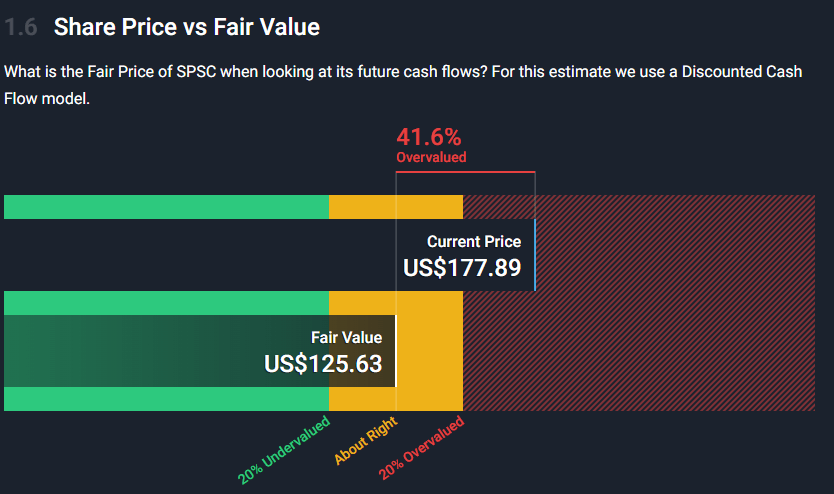

If we want to factor in the debt/equity ratio, which is only 2.85 percent, as Simply Wall Street does, by levering the unlevered sector beta, we could use a discount rate of 8%. This would still leave the stock overvalued by 39%. And Simply Wall Street came up with a similar end result, finding it 41.6% overvalued.

SPS DCF Calculation Based on 8% DR (Simply Wall Street)

{kind=link}

Risks

There is a significant risk involved with holding onto this stock given how overvalued it looks, under the presumption that intrinsic value and stock price at some point will merge, be it months from now or a year or more from now. Some other issues to think about - this company has no long-term contracts that lock-in a major stream of revenue like in other industries so enhancing forecasted renewal rates is critical.

In order to continue growing profitably, they need to regularly add new customers and sell additional products to existing customers. Failure to do this consistently will adversely affect financial results, the company itself has pointed out in its 2022 filing . And convincing new clients to adapt to cloud based services may not always be so easy - with some worried about loss of control over user data and the steep investment in the non-cloud products they currently use.

In order to keep growing, the company must expand internationally, and by doing so will be faced with risks they've never dealt with before, from exchange rate, to foreign regulations, different technology standards. So, there is certainty a risk, in theory, that the company may not be able to sustain this growth.

Conclusion

SPS has delivered in ways that should make any investor happy: industry leading momentum, double digit growth in profits and revenue - both historical and forecasted, along with an unparalleled track record of beating earnings targets. But, it always comes down to the price. And this stock is much too expensive for my tastes from both relative and intrinsic valuation perspectives.

However, the stock is also still worth holding onto. SPS is too well positioned for growth in the world's largest retail cloud services network, consisting of 115,000 customers - including stalwarts like Walmart and Costco. And it has shown no signs of letting up. If this momentum keeps up - and the narrative continues to hold - it is hard to justify dumping this stock at the moment.

For further details see:

SPS Commerce: High Quality Company Set For Explosive Growth, But The Stock Is Just Too Expensive