SPSC - SPS Commerce Needs To Exceed Expectations

2023-07-25 08:10:06 ET

Summary

- SPS Commerce, a supply chain management software provider, has seen steady growth over the years both organically and through acquisitions.

- The company, which counts Amazon, Walmart, and Kroger among its clients, is well-positioned within the growing supply chain management industry.

- SPSC has a healthy balance sheet with no interest-bearing debt and $233 million in cash and short-term investments.

- Despite SPS's impressive growth and strong financials, I believe the stock is overvalued at $181.39 per share, pricing in too much future growth.

SPS Commerce Inc. ( SPSC ) provides companies with supply chain management software. The company has had a steady and impressive growth run throughout the years, but as the company's growth has been achieved partly through acquisitions instead of organic growth, and the company's valuation currently prices in a hefty amount of growth in the bottom line, I have a sell-rating for the stock at the current price of $181.39 per share.

The Company

Founded in 1987, SPS's software allows businesses to fulfil omnichannel orders. The company's offering also helps businesses to manage sales and logistics across all sales channels. The offering helps companies to digitalize and track their inventory in an efficient manner. SPS has an impressive list of clients, as clients include huge companies such as Amazon, Walmart, and Kroger. The company's clients are categorised in five main verticals, being retail, grocery, eCommerce, distributors, and logistics:

{kind=link}

SPS also partners with multiple companies to bring its offering into life - these partners include Oracle, Shipstation and QuickBooks.

The company has been active in acquisitions to further boost its growth, and to have a wider offering for its customers - for example, in 2022 the company bought GCommerce in July and InterTrade Systems in October , spending around $94 million in total. This is far from an exception, as the company has had seven acquisitions since 2016 . The company currently offers a wide range of solutions:

SPS's Products (www.spscommerce.com)

Supply chain managements should be an industry with reasonably good growth, as Valuates Reports estimates the industry's compounded growth rate to be 10.9% from 2023 to 2032, as new verticals such as healthcare organizations have a growing need for the software. SPS is well positioned to take its growth from the industry, as the company is already established with some of the largest companies in the world.

Financials

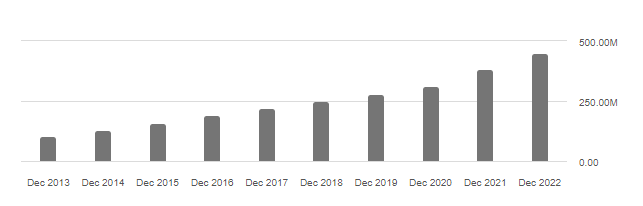

SPS's revenues have steadily grown over the years with an impressive compounded annual rate of 17.7%:

SPS's Revenue Growth (Seeking Alpha)

{kind=link}

It is important to note, though, that the company has had numerous acquisitions in this period as mentioned before, boosting its growth non-organically. I believe the company's growth story should continue into the foreseeable future.

As a software company, SPS Commerce should be able to achieve high operating margins, and I believe their margins should scale as the company grows. The company's trailing EBIT margin stands at 15.1%, but with a gross margin of almost 66%, the company should scale well. Furthermore, the company communicated in its Q1 earnings call that SPS targets a gross margin above 70%, as SPS's CFO and Executive Vice President Kimberly Nelson told:

So if you think about where we're at from a gross margin, we're at, call it, sort of that mid-ish to maybe a little bit above mid-ish 60s from a gross margin perspective. Longer term, we believe that can be in the low 70s. The biggest driver of how that will change over time to get us to the low 70s is really primarily going to be around scaling. Cost of goods sold is an area we've made a lot of investments in, in the overall customer experience. And over time, we believe we'll be able to grow into a lot of those investments."

This coupled with the fact that SG&A expenses should come down as a portion of revenues because of revenue growth, the company could show largely greater operating margins in a few years.

SPS doesn't currently hold any interest-bearing debt - I believe a healthy amount of debt would create shareholder value as the company could access cheaper capital. This does mean, though, that SPS's current balance sheet lowers the risk for investors. Further, the company has a cash balance and short-term investments totalling $233 million.

Upcoming Earnings

SPS will reports its Q2/2023 earnings on the July 27th in after-market hours. The company is expected to have a stable growth of 17.9%, slightly lower but in line with the previous quarter's growth of 19.7%. The company's revenues should not deviate from expectations, as the company has guided towards a revenue between $128 million and $128.8 million - a very shallow range. Also, the company has an EBITDA guidance of $36.4 million to $37 million, as their cost structure is also stable.

As the quarter's financial metrics are already quite well known, the main factor to look for in the upcoming earnings is the company's guidance for Q3 and the entire year. I believe their guidance for the rest of the year should be in line with current growth - a higher guidance could be very positive for the stock.

Valuation

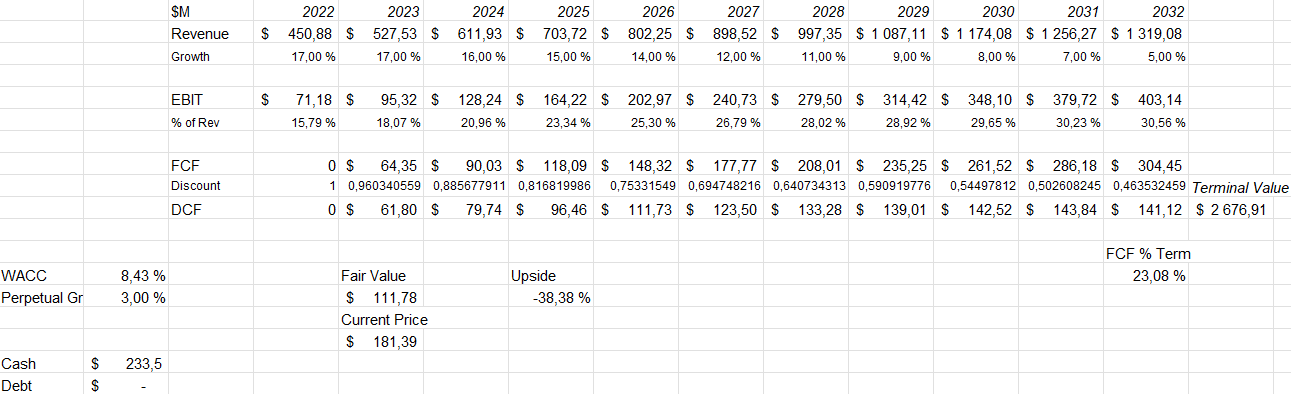

The company has a trailing price-to-earnings ratio of 116 and an EV/EBIT of 90. These ratios price in a significant amount of growth - an amount that I don't think the company will succeed in delivering. A discounted cash flow model with reasonable assumption tells the same story of the company's valuation, as with my estimates the stock has a downside of -38%:

DCF Model of SPS (Author's Calculation)

{kind=link}

The revenue estimates are near consensus estimates, pricing in a good amount of growth that is near the company's historical organic growth. I believe the growth should slow down as time goes on, if SPS doesn't utilize further acquisitions - for 2032, I expect the company to only grow a very small amount of five percent.

As told before, I believe SPS's margins should grow impressively. This is represented in the model as I expect SPS to reach margins in the range of 30%. Their offering is quite defined, so needs for capital expenditures shouldn't exceed the company's rate of depreciation - I believe the company's accounting earnings should be converted well into cash flows. I used a WACC of 8.43% which is derived from a capital asset pricing model:

CAPM of SPS (Author's Calculation)

The company doesn't currently have outstanding interest-bearing debt, but I believe the company should at some point withdraw a modest amount of debt - I'm pricing in a 10% debt-to-equity with an interest rate of 6%.

For the cost of equity, I use the United States' 10-year bond yield to determine a risk-free rate, with the yield currently being 3.84%. The equity risk premium of 5.91% is taken from Professor Aswath Damodaran's July estimates for the United States. With a beta of only 0.8 according to Tikr, the company is perceived as a quite low-risk investment in terms of systemic risk. Finally, I'm adding a 0.3% liquidity premium, as I believe the company is quite liquid. This forms a cost of equity of 8.87% and a weighted average cost of capital of 8.43%.

Closing Remarks

At $181.39 per share, I believe the stock market is pricing in too much growth for the company. Although its revenues are quite low-risk and the company has achieved remarkable growth with giant clients, the valuation of P/E 116 and a DCF model downside of -38% doesn't create a good risk-to-reward ratio for the investment in my opinion. If the company exceeds analysts' expectations or executes acquisitions that create a large amount of shareholder value, I believe the stock could be currently a reasonable investment. As I don't believe that to be the base scenario, I have a sell-rating for the stock for the time being.

For further details see:

SPS Commerce Needs To Exceed Expectations