ACTV - SPX: The Fed Is Acting To Burst The Bubble It Created

2023-05-05 11:15:03 ET

Summary

- While the equity bubble created by the Fed's post-Covid easy money policies made an equity market crash likely, the extent and pace of its tightening cycle have increased that risk.

- Over the past year, the Fed has engaged in its most aggressive tightening cycle since the Great Depression, with money supply suffering its largest contraction since the 1930s.

- This combination of tight policy and still-extreme equity prices suggests it would take a 75% fall in the S&P 500 to restore the equity risk premium to its long-term average.

- With equity market breadth deteriorating and cracks appearing in the corporate bond market, these are the conditions under which investors in the past have shifted from buying the dips to panic selling into them.

- It would likely take a huge market crash in order to trigger an aggressive Fed easing cycle and, more importantly, the kind of improved earnings yield and negative market sentiment that would allow any easing to create a sustainable market bottom.

I rarely like to attribute equity movements to Federal Reserve policy as there are so many factors at play driving markets and little historical evidence to suggest central bank policy is a dominant factor. However, over the past year, the Fed has engaged in perhaps the most aggressive tightening cycle since the Great Depression.

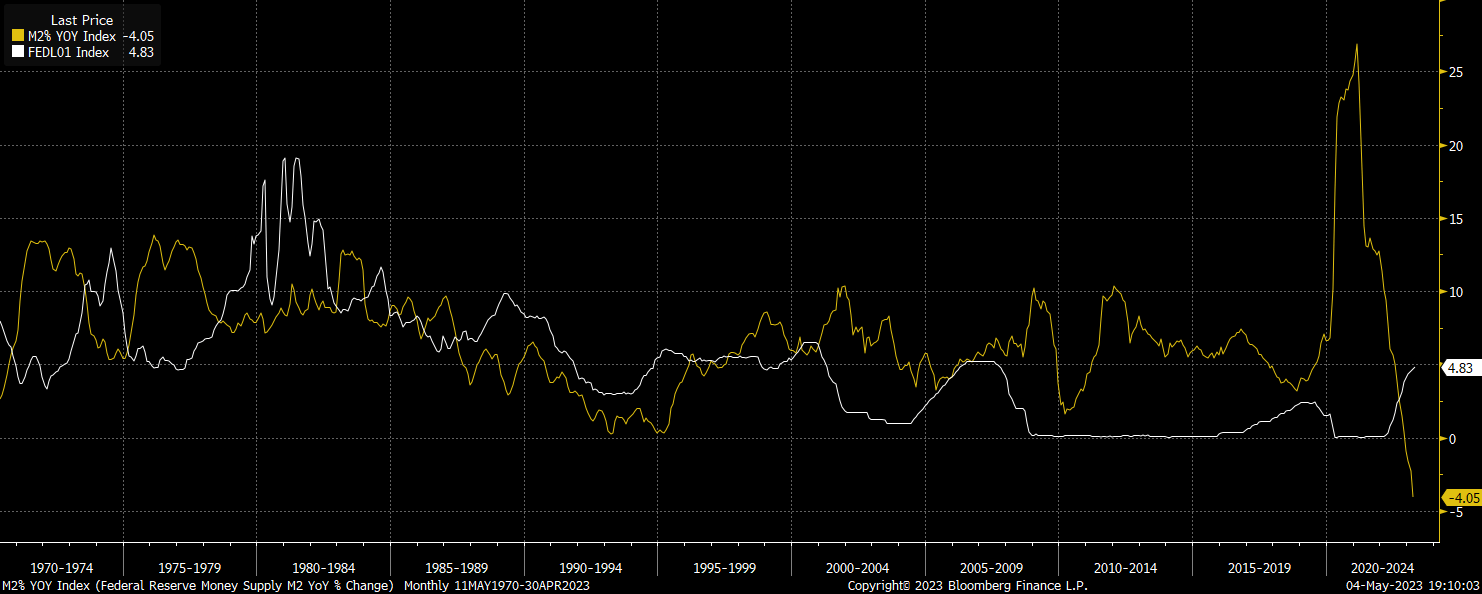

Since my last article on the SPX on March 3 (see ' A Profit Recession Could Be Coming '), the index has edged higher, yet earnings have weakened and monetary policy has become even more extreme, adding to the risks facing the market. The Fed funds rate is now 2.6% above long-term inflation expectations, while M2 money supply is contracting at its fastest pace since the 1930s. This restrictive policy has marked a record quick policy reversal from one of the easiest periods of monetary policy in history. While a market crash was always going to be a likely result of the speculative bubble easy money created, the breathtaking pace of the reversal has increased this probability.

Fed Funds Rate And M2 Growth (Bloomberg)

{kind=link}

The Fed Always Fights The Last War

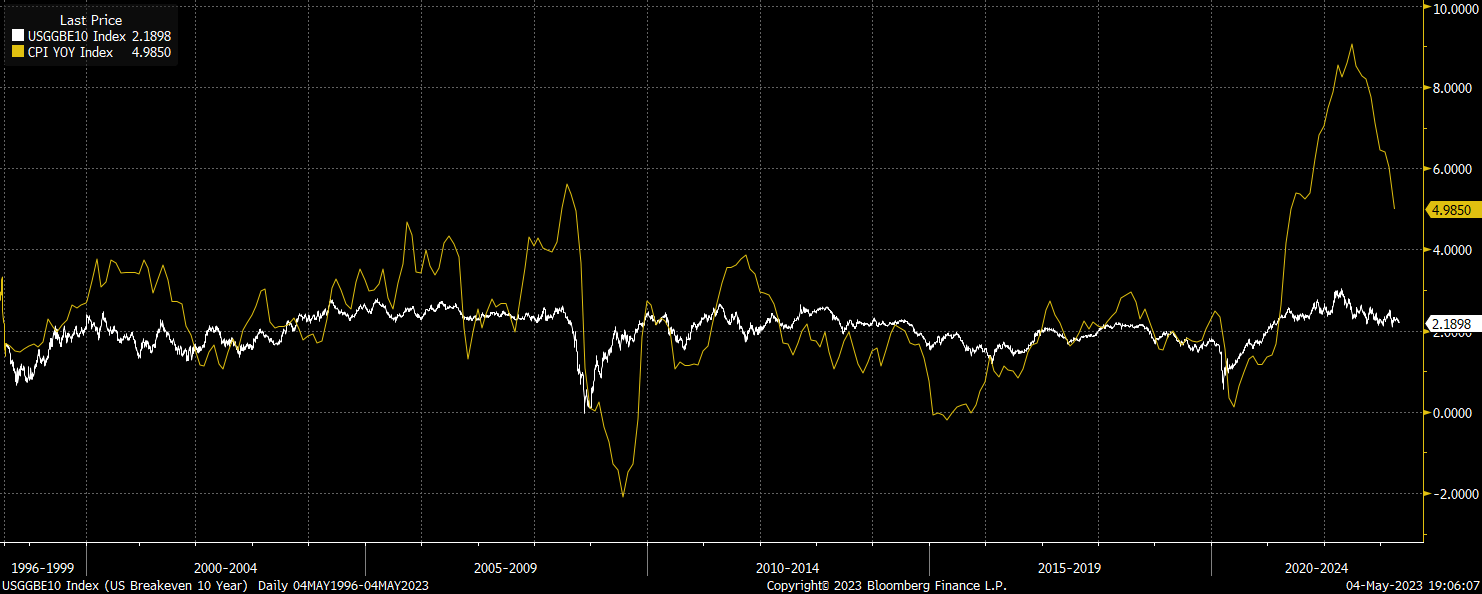

The Fed's focus on unemployment and inflation means that it is routinely behind the curve when it comes to real-life market and economic conditions, as both these variables are highly lagging in nature. Policymakers were too slow to tighten in recent years as headline inflation remained low, and the unemployment rate remained elevated. The recent tightening reflects the fact that headline CPI remains elevated, and unemployment remains low. However, forward-looking measures are painting a completely different picture.

Headline CPI Vs 10-Year Breakeven Inflation Expectations (Bloomberg)

{kind=link}

In the case of inflation, while headline CPI remains high, 10-year breakeven inflation expectations - a very accurate predictor of future inflation in the past - sit at just 2.2%. Meanwhile, while the unemployment rate is near record lows, the Conference Board's Leading Indicator Index is at levels never seen outside of recession.

This combination of extremely tight monetary policy, weakening economic activity, and an extremely overvalued equity market were seen at the start of the bear markets that began in 2000 and 2007, and there is no reason to expect a different end result this time.

A 75% Decline Would Be Needed To Restore Long-Term Average Equity Risk Premium

Despite the retreat in valuations from their peak, the decline in free cash flows has seen the free cash flow yield on the S&P 500 fall back to just 3.8%, meaning that investors can get a full percentage point more on cash than on US stocks, even if companies were to pay out all their free cash flows as dividends. As it happens, the share of free cash flows that S&P 500 companies pay out as dividends and net buybacks is less than half, putting the dividend yield at just 1.7%, more than 3pp below the yield on cash.

For a fairer comparison between the yield on cash and stocks, we must take into account the potential for nominal GDP growth to drive up nominal cash flows and dividends, either through real output growth or rising prices. As I argued in ' Zero Percent Long-Term Growth Is A Real Possibility ', with 10-year inflation expectations at 2.2% and real GDP growth likely to converge towards zero, 3% long-term nominal GDP growth seems like a fair assumption.

If free cash flows and dividends per share were to grow at this pace, the S&P 500 would still be expected to return around the same as cash, which should be of huge concern to bulls given that over the long-term stocks have returned around 5pp more than cash. This means that at current interest rates and 3% dividend growth expectations, the S&P 500 dividend yield would have to rise by at least 5pp to 6.7%, which would require a 75% market decline.

Note that this is not a prediction, nor is it a worst-case scenario. It is simply the price decline that would have to occur in order for future equity returns relative to cash to rise back in line with their long-term average based on reasonable growth assumptions.

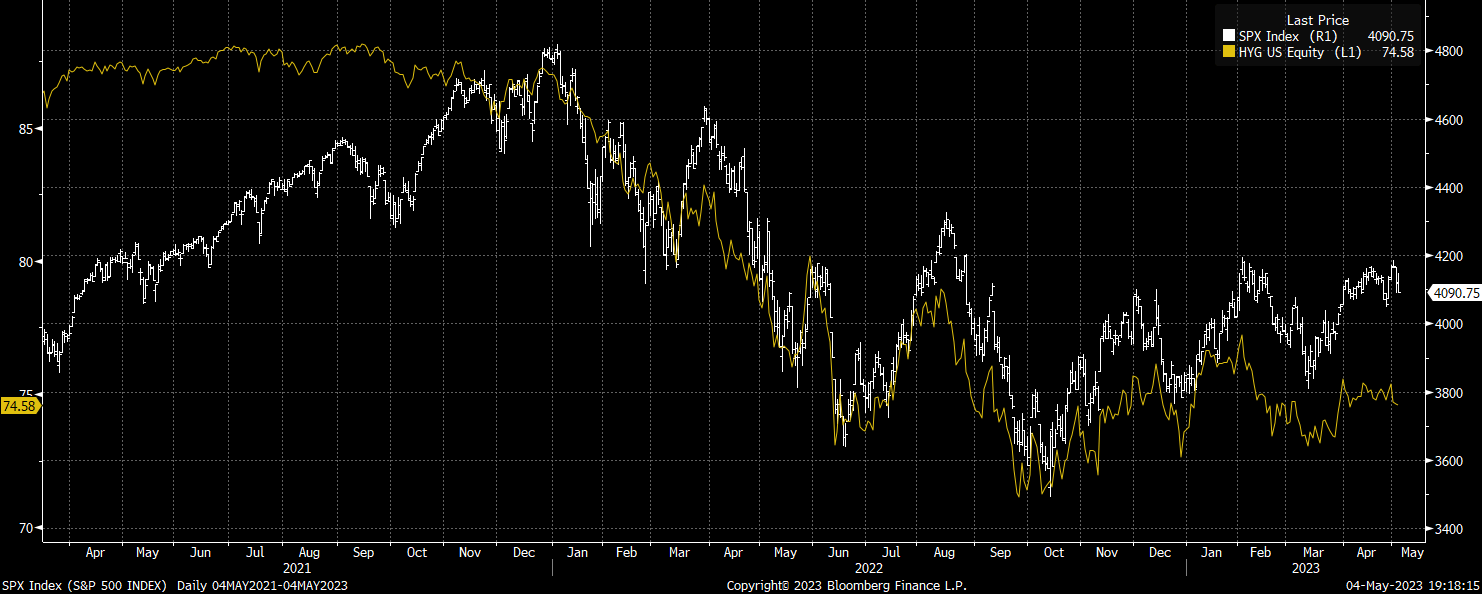

Of course, most investors do not look at the markets in this way. My guess is that the average investor is more concerned with short-term trends and market narratives than they are about valuations and equity risk premiums. However, with equity market breadth deteriorating and cracks appearing in the corporate bond market, these are the conditions under which investors in the past have shifted from buying the dips to panic selling into them to avoid further losses.

S&P 500 vs HYG High Yield Corporate Bond ETF (Bloomberg)

{kind=link}

Fed Cuts Will Be Too Little Too Late

The consensus view in the market at present seems to be that any Fed policy reversal would provide a boost to stocks. However, this faith in lower rates supporting stocks is not supported by the data. The Fed cut rates aggressively in 2000-2002 and 2007-2009, and this did nothing to prevent market losses. Even during the Covid crash, which is widely seen as an example of the power the Fed has to prevent market declines, it took a 33% decline in stock values before sentiment was bearish enough that low rates helped stimulate a recovery. My guess is that with the Fed still focused on inflation, it would take a huge market crash in order to elicit an aggressive easing cycle and, more importantly, the kind of improved earnings yield and negative market sentiment that would allow any easing to create a sustainable market bottom.

For further details see:

SPX: The Fed Is Acting To Burst The Bubble It Created