BMO:CC - SPY: Is December CPI Optimism Setting A Sneaky Bull Trap?

Summary

- Everyone seems to be taking a good CPI report this week as a given, but history suggests inflation tends to stick around for a while!

- The weakening dollar, falling yields, January pay increases, and fiscal cost-of-living adjustments will all push inflation up in the near term.

- My best guess is that inflation has another 12 months before monthly price rises are fully consistent with the Fed's 2% annual core inflation target.

- Even if CPI comes in soft, bears like Morgan Stanley's Michael Wilson have suggested that a weaker CPI will be accompanied by weaker earnings and weaker profit margins than expected.

- December CPI will be released on Thursday, January 12th at 8:30 AM Eastern Time.

Markets cheered the nonfarm payrolls report on Friday, with the broad S&P 500 index ( SPY ) rising over 2% on the day, with a big follow through on Monday as of my writing this. It seems to me like another case of algorithms gone wild, as the move was preceded by a selloff the day before on the ADP payrolls number. These are small data points, but at stake are the larger questions of where the Fed is likely to take interest rates–and whether the U.S. economy will pull off a soft landing or descend into recession after the pandemic's money-printing binge. The market is pricing in several rate cuts over the next 12-18 months, while the Fed has indicated they want to hike rates more. With the S&P 500 trading on the high end of its historical range at about 17.5x 2023 consensus earnings estimates of $225, the market needs to hit a parlay here. Highly valued stocks need a Fed pivot, and they need the pivot to come without an underlying collapse in earnings (i.e. a recession). This assumption will be getting a huge test this week with December CPI, released at 8:30 AM Eastern on Thursday. This data release will be key to understanding whether the current bear market in stocks will continue to grind lower or not. Markets may be overly complacent about CPI, with the optimism over CPI and the recent rally setting what could be a sneaky trap for investors.

Is Inflation Done? History Says Maybe Not

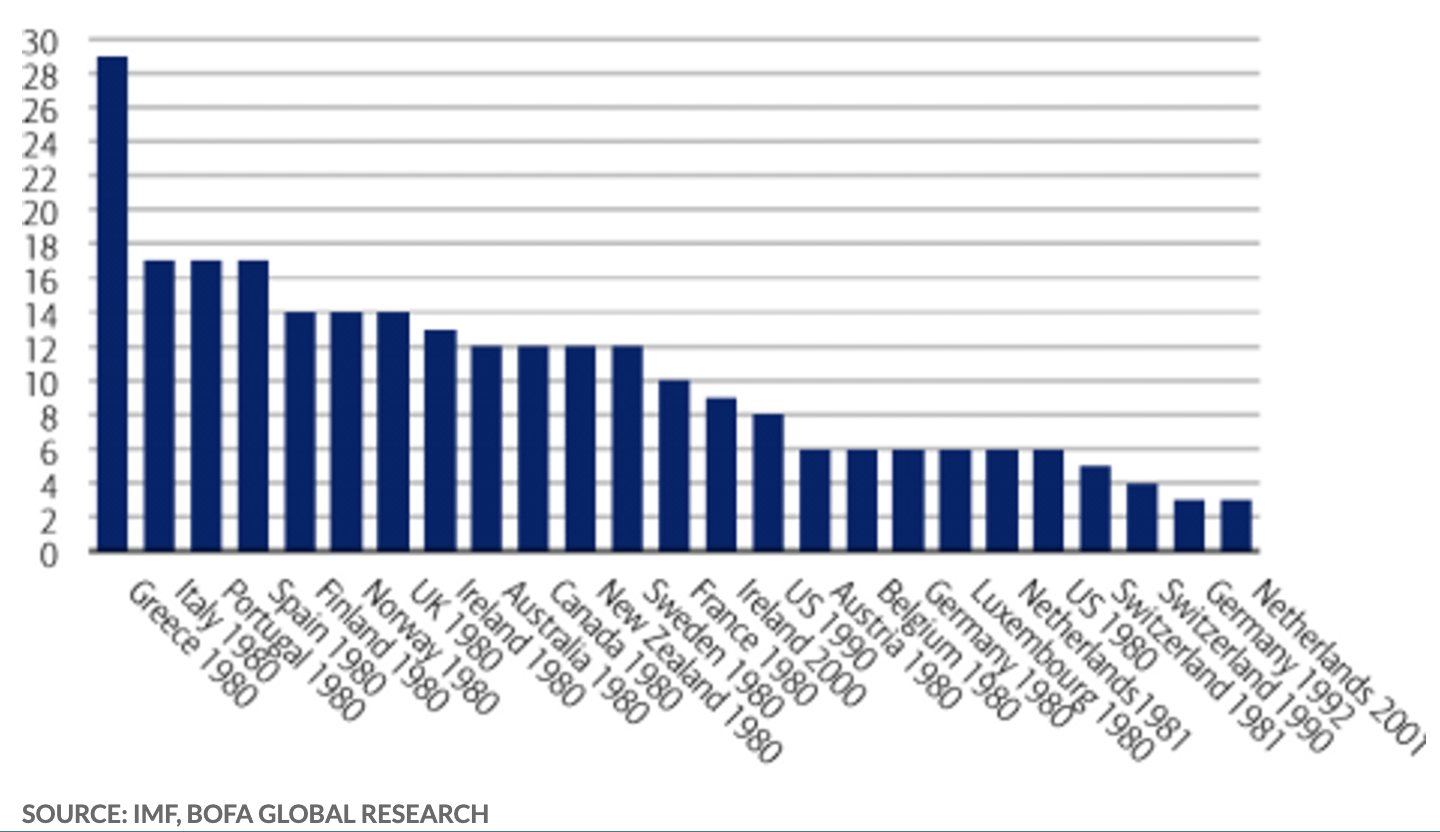

Strategists at Bank of America ( BAC ) did a study in 2022 inflationary environments in different time periods and different countries. Their question– when the rate of inflation rises above 5% annually, how long does it take for it to fall back to 2%? The Y axis here is in years, and the average is about 10 years. If you toss out countries in Southern Europe that took the longest, you're still looking at 6-12 years in many scenarios historically. The study only seems to go back to the late 1970s and early 1980s, but the post-WW2 inflationary bout didn't see US inflation return to 2% annually until 1949 (it then spiked again in the Korean War).

{kind=link}

This round of inflation started in early 2021, and inflation first breached our 5% threshold in May 2021. If inflation is down to 2% annually in 6 months like many in the market believe, it would be the fastest disinflation in modern history. If we take a relatively benign parallel from the early 1990s inflation bout, we'd still be looking at 6 years.

To be fair, explicitly targeting 2% inflation has only been done since the Clinton years in the US, after successful trials in some other countries a few years before. But what history clearly demonstrates is that inflation is an ongoing process that does not go away on its own, and that even with best practice it sticks around for years. Otherwise, there would be all kinds of examples of transitory inflation in history that went away after a couple of years, and there aren't. Stocks and bonds are priced assuming that inflation comes down quickly and monetary policy stays rather loose, so if this is not the case then the market will need to adjust prices downward.

Why Inflation Tends To Stick Around

There are many reasons inflation tends to stick around. Some are mechanical, and some are more behavioral.

Mechanical reasons inflation sticks around are interesting, and we're about to see some of them kicking in now. The most famous is called a "wage-price spiral" , where demands for COL increases are met by companies, who pass on prices to customers, which makes the cost of living collectively go up more. Social Security COLA increases are another example of this. For 2023 Social Security is increasing by 8.7%. Social Security alone is 5-6% of GDP, so this increase alone will increase the 2023 money supply by about 0.5%. Behavioral reasons are interesting as well, we've seen them in the housing and used car markets in recent years. When buyers buy so they can get in before prices go up even more, it causes prices to rise. This is also how asset bubbles get going, and it can work in reverse as well when the bubbles pop. Generally, businesses' expectations of future inflation tend to correlate with future inflation, and even things like basic contracts get rewritten to add annual price increases.

Another reason that inflation tends to stick around is that central banks previously had a poor understanding of when inflation was truly beaten– like gardeners who simply trim weeds rather than pull the roots. In the 1970s, the Fed cut rates after inflation had superficially fallen, only to see it come back stronger than ever. Jerome Powell has repeatedly referenced this to push back against market expectations of rate cuts, but the market continues to defy him. What tends to happen is that the Fed will back off, the dollar weakens, interest rates fall, and stocks go up, all of which fuel inflation. This has all happened recently, with 10-year Treasury rates about 60 bps off their highs, the dollar down about 10% off its highs, and stocks rallying off of the lows. To this point, the rally in stocks and interest rates and the selloff in the dollar is putting upward pressure on inflation, leading to the possibility that the rally will soon be reversed. The most recent Fed minutes alluded to this , but the market still is ignoring what's right in front of it and continues to fight the Fed.

Wage Inflation Is A Symptom Of A Messed-Up Economy, Not the Cause

The market obviously got very excited about the nonfarm payrolls number on Friday, but the reaction was way overdone. If you look at wage growth over the past few years, it was never a key driver of inflation. Over the last 12 months, real earnings for workers are down about 3%. This is instructive. Economist Milton Freidman quipped that inflation was "always and everywhere a monetary phenomenon," and while it's not 100% true, it's the best way of thinking about the current inflation. Big wage increases and strikes are not the main driver of inflation in and of themselves, but they're an inevitable result of pumping an excessive amount of money into the economy.

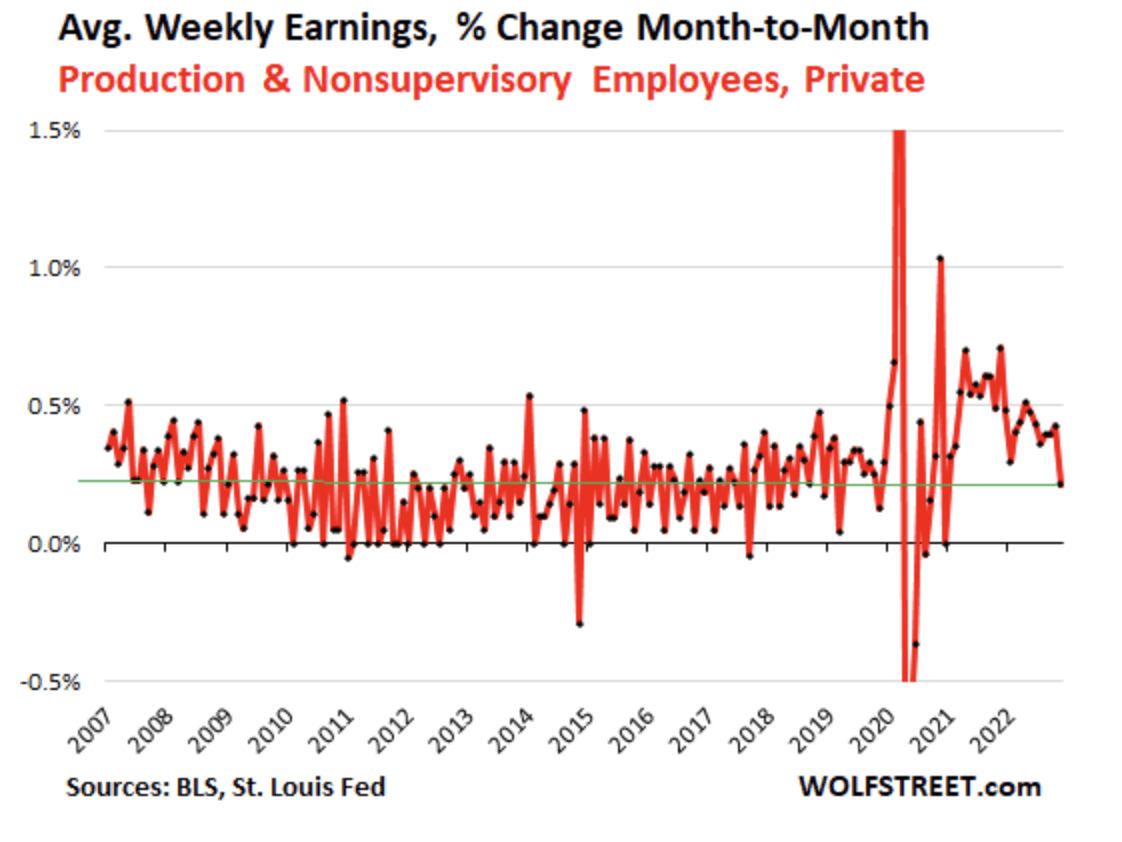

Just this morning, I woke up to an article that 7,000 New York City nurses are going on strike today. Some of this is healthcare industry-specific, but it follows strikes and contract renegotiations in places as far and wide as airlines, railroads, and dockworkers. The most recent nonfarm payrolls report shows a deceleration in wage gains, but the labor market continues to tighten, with payrolls rapidly outrunning population growth and the unemployment rate falling back to 3.5%. Wolf Richter took a deep dive into the payrolls report on his blog , but I thought I would share this graph to show that the weekly earnings numbers tend to be rather volatile.

Average Weekly Earnings (Wolf Street)

{kind=link}

The Fed's problem here in my mind is that price increases are outrunning wages, which in turn are outrunning productivity. This is totally backwards, and it is a clear warning against the idea that we're going to have an easy soft landing for the economy. A lot of the workers entering the "labor force" are self-employed gig workers who were getting W-2 jobs and getting big pay increases.

Labor force participation overall is well below pre-pandemic levels.

And why are prices increasing faster than wages? Because consumers got a ton of stimulus money in 2021, and now are spending down savings and running up debt to continue to consume.

Consumers have some cushion left from pandemic savings, but when it's gone, it's gone, and probably in Q2 or Q3 . The savings number is even crazier than it looks because it doesn't take into account the resumption of student loans, but it does take into account the free money to millions of Americans who refinanced their mortgages to ultra-low rates.

The problem is debt, and that's how recessions always start. Middle and upper-middle-class people (and sometimes companies and governments) borrow too much money based on their expectations for the future, and when the future comes in below expectations they've got too much debt service. Same thing here– ultra-low rates caused a boom in all kinds of borrowing– personal, corporate, and government, and a lot of that money was not invested productively but rather went into meme stocks, altcoins, single-family houses in the desert, or plain old conspicuous consumption.

The root cause of this inflation is massive government spending. The US ran deficits of 14.9% of GDP in 2020, 12.3% in 2021, and 5.5% in 2022. There are only two ways to deal with this, you either go to the private market and sell the debt at a market price, or you have your central bank print money to buy the debt, which almost always will lead to a bunch of inflation. This happens all the time in emerging markets, but the last congress in the US was the wildest spending congress in history. It never ends well. What's clear is that the new Congress is going to crack way down on spending. The optimistic way to view this is that Republicans are not going to make any more choices that lead to short-term benefits for long-term pain. The more cynical way to view it is that they have no incentive to spur the economy before the 2024 presidential election, so it's better to pull the plug now and let the inevitable recession happen on Biden's watch rather than their own.

Where Will Stocks Go From Here?

If the S&P 500 breaks above 4,000, it'll officially be round 3 of pivot mania after the first round in July/August and the second round in October/November. Morgan Stanley's ( MS ) Mike Wilson has argued for the past few months that CPI will come in below expectations, but earnings and margins will be significantly worse than the market thinks, pushing the S&P 500 to around 3000 . Former Treasury Secretary Larry Summers has argued that the expectations for a low-inflation economy are too optimistic. Michael Burry has argued that the US will enter recession, leading to more stimulus and another huge inflation spike. However, if you look at history, the market tends to bottom well after the Fed starts cutting rates, sometimes over a year later (this implies stocks won't bottom until 2024).

The near-term direction of stocks will be heavily influenced by the CPI report this week. There are some forces pushing inflation down, such as the popping used car bubble and the popping housing bubble. However, there are also powerful forces pushing it up, such as a weakening dollar, renewed risk appetite for stocks, and yearly cost of living boosts that come this time of year.

The Cleveland Fed's econometric model is calling for CPI of 0.1% (cheaper gas!), but a stubbornly high core CPI of 0.48%. The Fed typically pays more attention to the core. The model traditionally outperforms professional forecasters but has come in low the past couple of months, largely due to a quirk in the way CPI calculates the cost of health insurance. If the Cleveland Fed is on the money about a 0.5% month-over-month inflation report, stocks are likely to take it very harshly. Conversely, an in-line number is likely to allow stocks to continue their latest rally. However, the Fed is concerned about loosening financial conditions, so any rally in stocks may be talked back down by Fed speakers, knowing in the back of their minds that the weaker dollar and decline in rates are likely to complicate their inflation fight. If CPI comes in hotter than expected, the Fed is likely to go 50 bps at their meeting at the end of the month, and if it comes in cooler, then 25 bps is more likely. The main debate at the Fed continues to be how much inflation is transitory and how much is entrenched because it affects how high interest rates will need to go. If you think half of core inflation (excluding food and energy) is transitory, the current Fed rate of 4.5% is about right under standard econometric models (the legitimate ones, not the ones politicians like to quote) . This seems low though, and assuming one-third of inflation is transitory gets you a Fed funds rate of 5.5% or higher.

For an idea of how much stocks could fall, a 15x multiple is more typical for this type of high-rate environment, which would take the S&P 500 to 3400 if earnings estimates hold up at $225 and to 2900 if they don't and fall to $195. For many highly valued tech stocks and the broad market, the prospect of more Fed tightening is terrible. But for US banks and brokerages like Truist ( TFC ), Bank of America, and Morgan Stanley, things look better. If you have a higher risk appetite, Canadian banks like Bank of Nova Scotia ( BNS ) and Bank of Montreal ( BMO ) have more yield but more downside exposure to a recession. Insurers are interesting as well because they benefit from higher yields on their premiums, some stocks like Prudential ( PRU ), Travelers ( TRV ), Allstate ( ALL ), and Tokio Marine ( TKOMY ) are the subject of some nice investor debate. For a one-fund solution for bullish investors, consider the iShares Small Cap S&P 600 Fund ( IJR ).

Key Takeaways

- Investors are optimistic about Thursday's CPI report, but history and econometric models continue to suggest that inflation is not yet conquered. A hot CPI report is likely to be taken very harshly by markets.

- If CPI is cooling because the economy is rolling over into recession, strategists like Morgan Stanley's Mike Wilson have suggested that investors may win the battle but lose the war in 2023.

- With stocks trading for over 17x earnings while cash rates are expected to top 5%, investors aren't getting very good compensation for buying stocks–they can earn 5% risk-free.

- Massive deficit spending was the key driver of the pandemic boom, but the current Republican House of Representatives is already signaling that it will put some serious pressure on government spending, while the Supreme Court is likely to dismantle the student loan pause. This could lead to a recession with little to no fiscal support. In the end, it would balance the economy and pop the asset bubbles, but the American consumer's record-spending run would be dead and gone.

- If you're itching to buy stocks, I believe the financial sector is the best place to be sector-wise because of low valuations and the fact that earnings from financial stocks will benefit from interest rates being higher for longer than the market expects.

- Do you agree or disagree? Bullish readers may be interested in my recent piece " Be a Better Bull ," for tactics. Bearish investors can help get the most from their cash from my recent " Be a Better Bear " piece.

For further details see:

SPY: Is December CPI Optimism Setting A Sneaky Bull Trap?