SRT - Startek Inc.: Unsophisticated Strategies

2023-10-26 11:57:11 ET

Summary

- Startek is an unattractive investment based on my view of its weak fundamental picture and uncompelling valuation.

- I posit the company's diversification strategy may not be effective due to low net margins and a lack of core operational efficiencies.

- The company's financial health is one of my concerns, with a significant portion of revenue generated by a limited number of clients.

- Due to the all-round lack of financial and operational strategy promise, my rating is Strong Sell.

Introduction

Startek, Inc. ( SRT ) is an unattractive investment based on my view of its weak fundamental picture and uncompelling valuation. I wanted to perform a comprehensive analysis to give potential investors my take on why I will definitely not be buying shares. Significant issues include a horrible WAAC-to-ROIC ratio, stagnant revenue growth metrics and weak net margins. I can see relative positives in some progress against further historical weakness, but I am making my analyst rating Strong Sell based on my perspective on its weak fundamental picture, poor valuation profile and an uncompelling 2022 annual report .

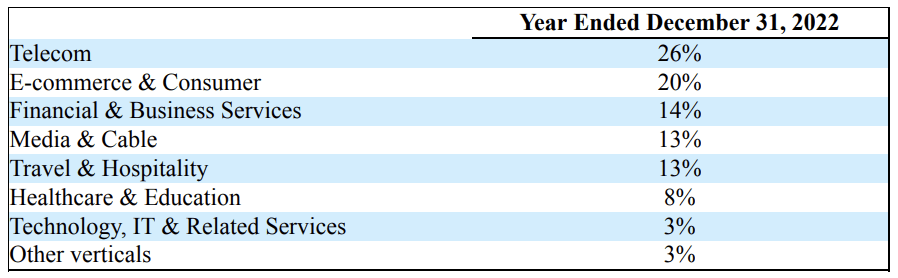

Diversification Against Weak Margins

The business is significantly diversified both by business segment and geographically:

Startek Revenue by Business Segment (Startek 2022 Annual Report) Startek Revenue by Geography (Startek 2022 Annual Report)

{kind=link}

{kind=link}

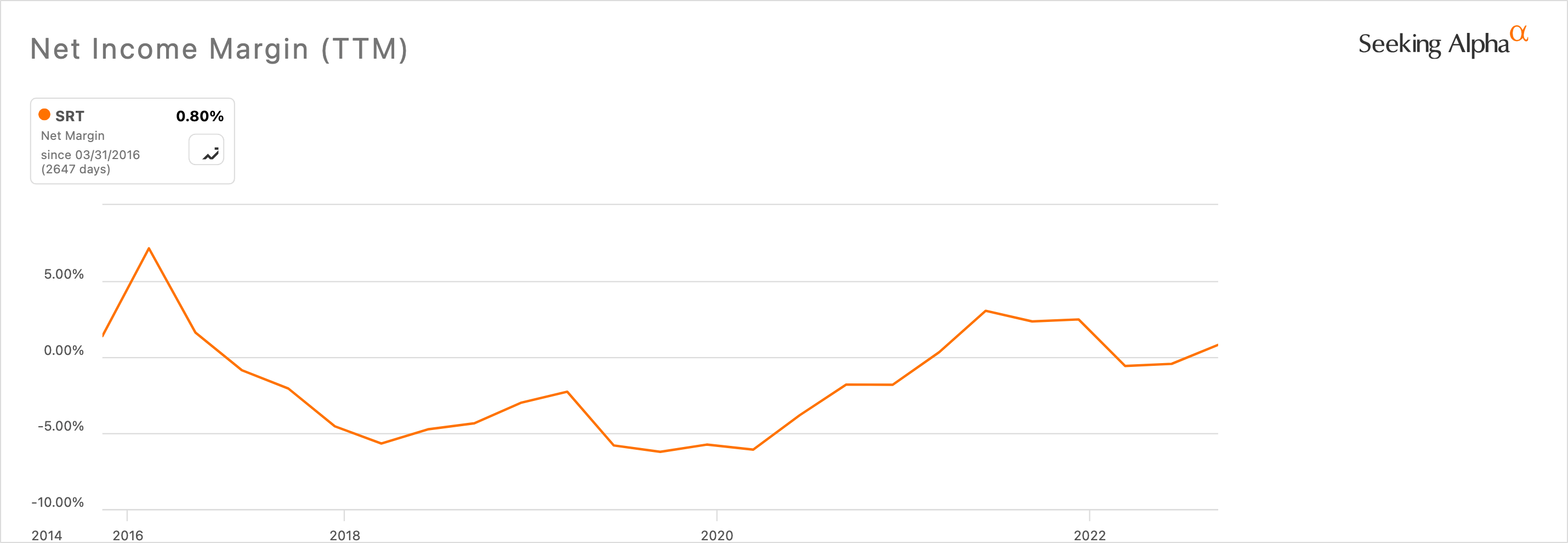

However, I wonder just how effective this diversification strategy is when the net margins are so low and have been for some time:

Startek 10-Year Net Income Margin (Seeking Alpha)

{kind=link}

I propose that the organisation could deeply stress core operational efficiencies in their dominant markets rather than beginning global reach when they have yet to identify areas of strength to successfully replicate.

The company even states on page 10 of the 2022 annual report that:

A substantial portion of our revenue is generated by a limited number of clients. The loss or reduction in business from any of these clients would adversely affect our business and the results of operations... We may not be able to retain our principal clients. If we were to lose any of our principal clients, we may not be able to replace the revenue on a timely basis. Several factors other than our performance could cause the loss of a client or reduction of business from a client... We depend on several large clients concentrated in a few industries, as well as clients located in a few geographies. Economic slowdown or factors that affect these industries could reduce our revenues and harm our business.

It is promising to see the company acknowledge its risks, but I am still wary about how their stress on diversification may realistically ease any portfolio concentration concerns. I don't see evidence that the organisation is creating sufficient business moats around its core clients, but may in fact be trying to protect itself from downside risk by overly diversifying. Wouldn't it be more prudent to focus on increasing value with core clients and generating significant defences around potential downturns to bolster what are already quite depressed performance metrics across the board?

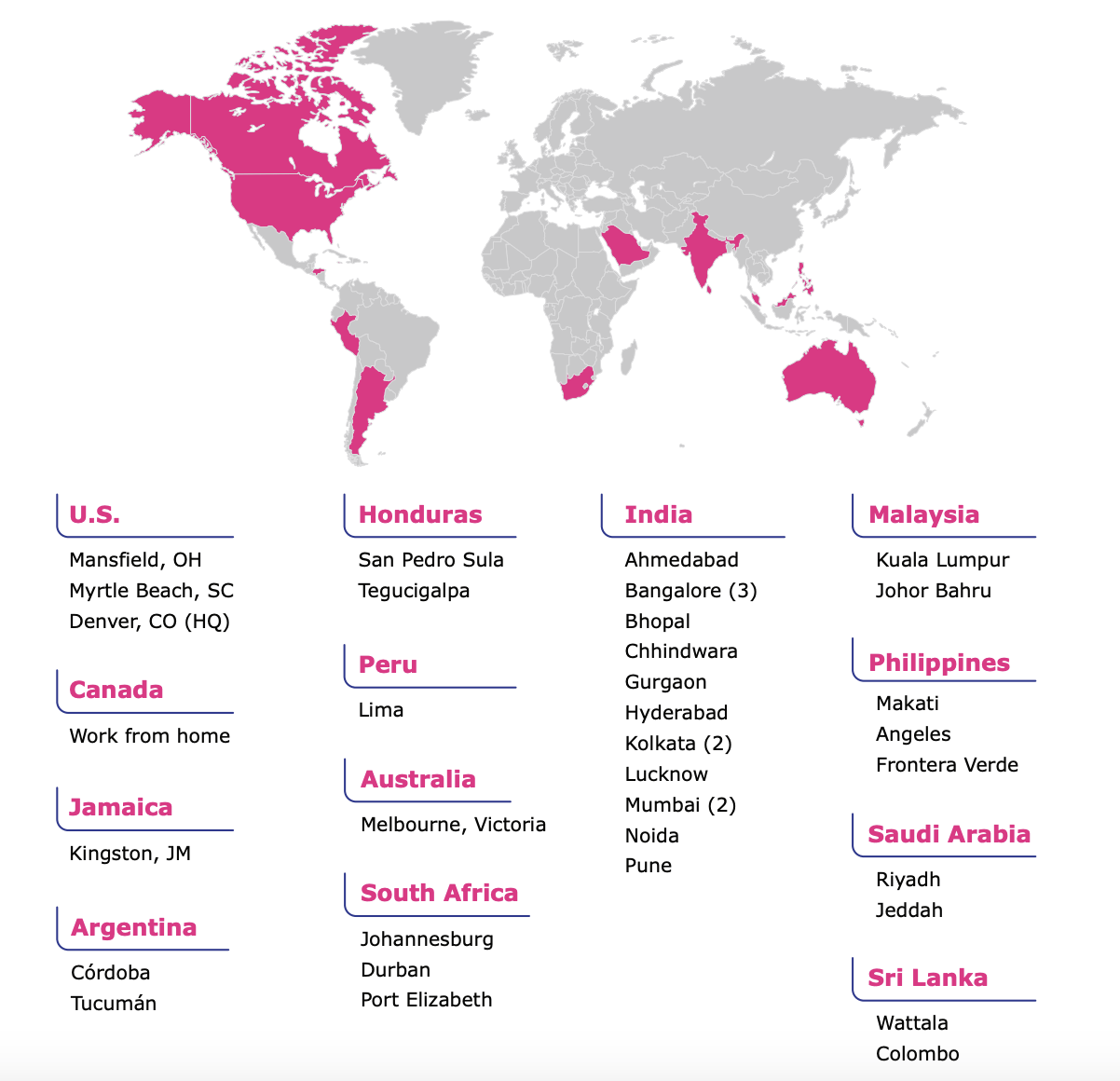

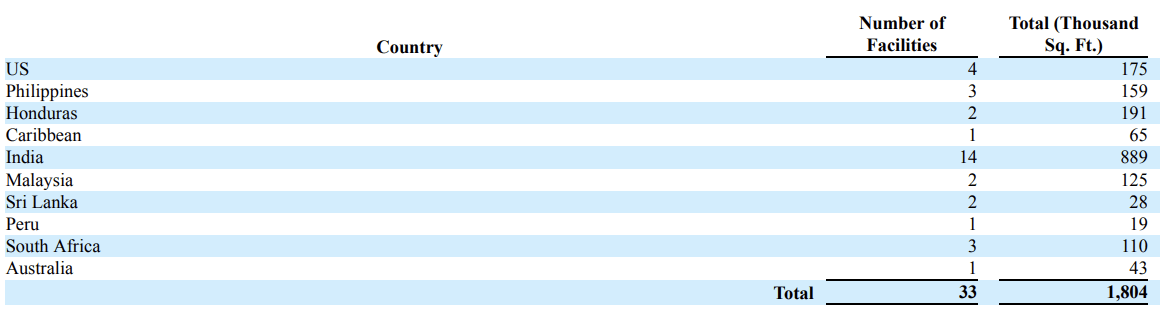

Startek Operational Facilities by Geography (Startek Annual Report 2022)

{kind=link}

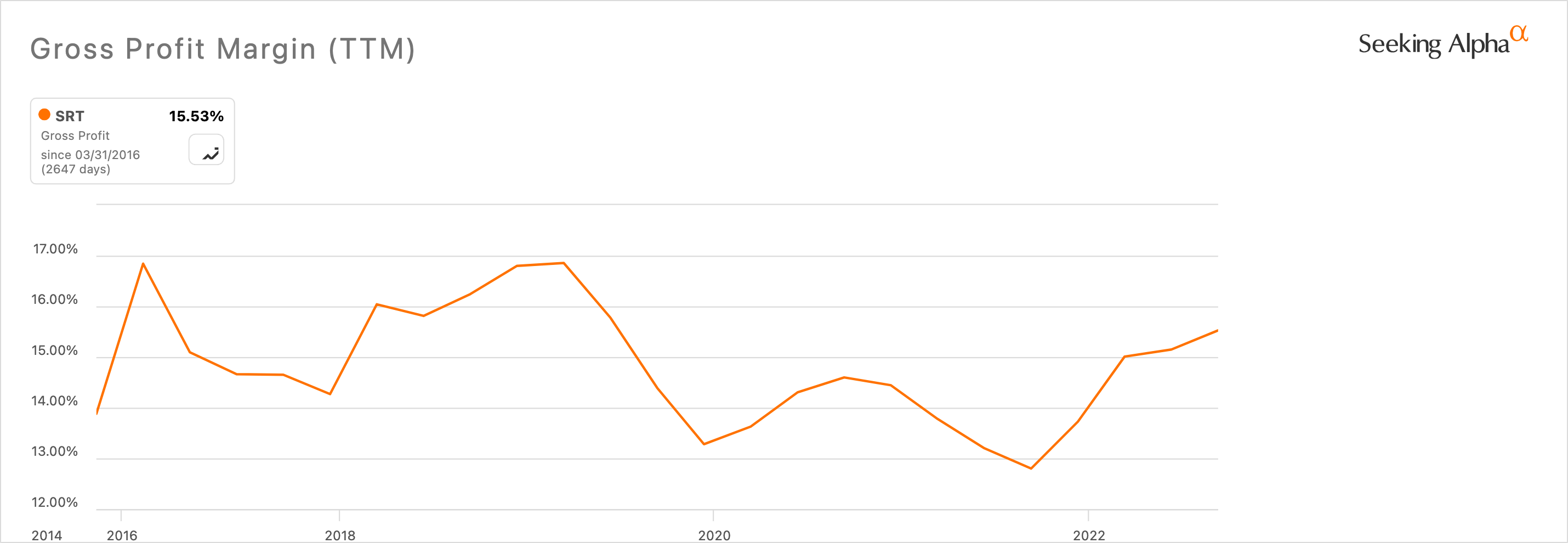

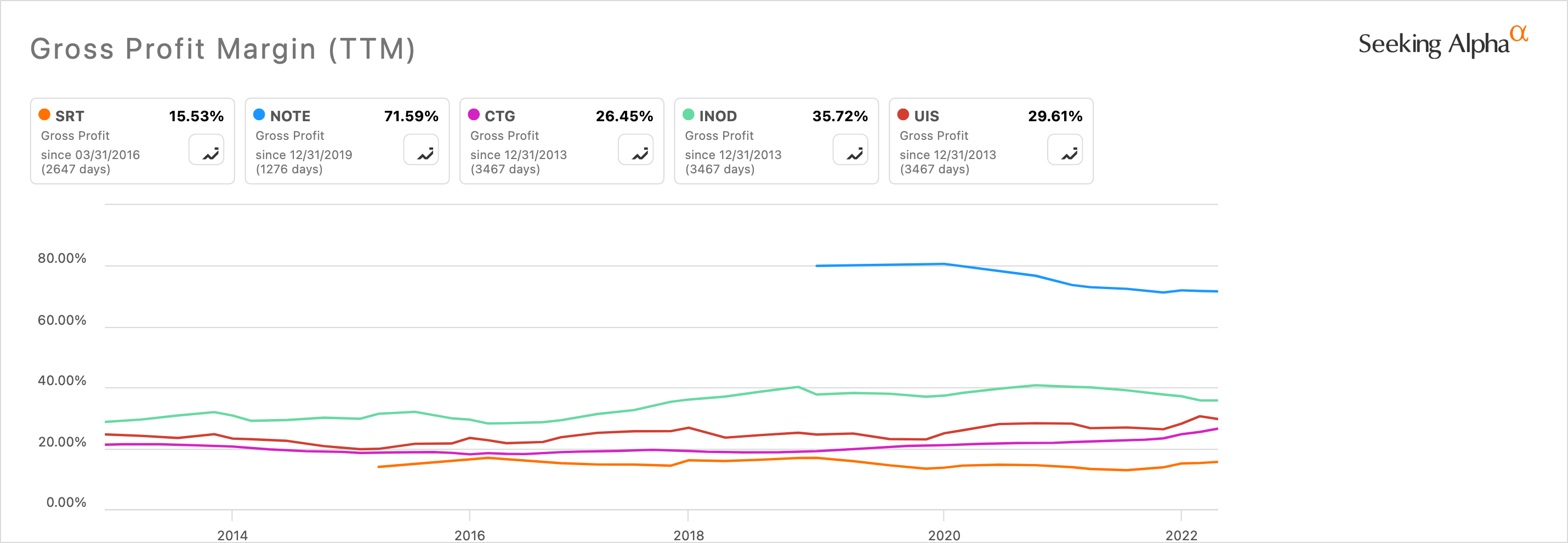

While net margins are typically the easiest place to see an increase in operational efficiency, unfortunately, the gross margins reveal the worst of the problem:

Startek 10-Year Gross Profit Margins (Seeking Alpha)

{kind=link}

To put this into perspective, Startek's gross margins are ranked worse than 83.22% of 2611 companies in a Software industry comparative dataset I used. To extrapolate and for a more refined peer comparison, FiscalNote Holdings ( NOTE ), Computer Task Group ( CTG ), Innodata ( INOD ) and Unisys Corp ( UIS ) all have higher gross margin readings than Startek:

Startek 10-Year Gross Margin Peer Comparison (Seeking Alpha) Startek 10-Year Market Cap Peer Comparison (Seeking Alpha)

{kind=link}

{kind=link}

The positives here are that the gross margins are currently close to all-time-high readings, but I don't see that as a great indicator of future success due to the past volatility showing a lack of concern for, or understanding of how to, actually maintain and promote gross margins and then boost efficiency to positively impact all other margin metrics. If the company were to successfully implement operational strategies to cause this, I'm convinced the organisation would have better hope of a strong future for shareholders. The issue is there is no immediate evidence that the company is making such changes or even aware of the necessity to do so.

Revenue & Strategy Misdirection

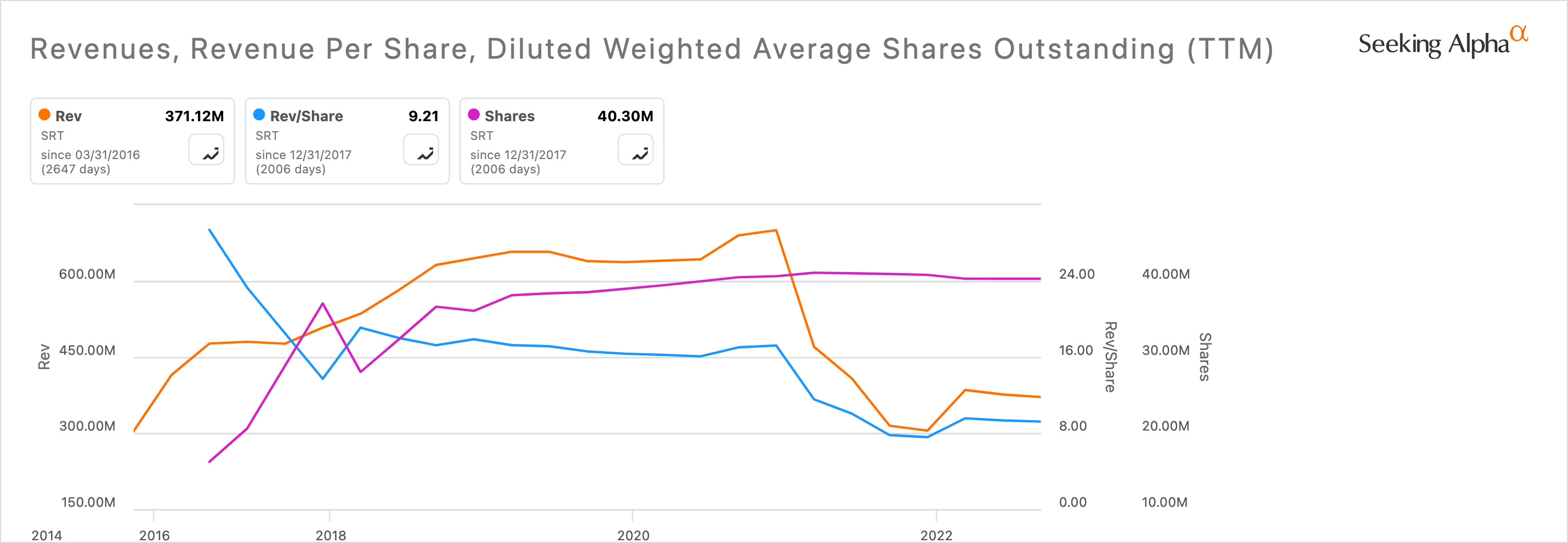

Long-term revenue has had a slow upward trend until recently:

Startek 10-Year Revenue (Seeking Alpha)

{kind=link}

We could forgive the recent setback due to the relative uptrend, but the revenue per share picture is much worse:

Startek 10-Year Revenue & Revenue Per Share (Seeking Alpha)

{kind=link}

And when analysed against the increase in outstanding shares over time, we can see exactly why:

Startek 10-Year Revenue, Revenue Per Share & Shares Outstanding (Seeking Alpha)

{kind=link}

This is a weak company that has been ineffective in creating meaningful shareholder value. I sincerely believe from my fundamental analysis that the issue can only be one thing: bad management.

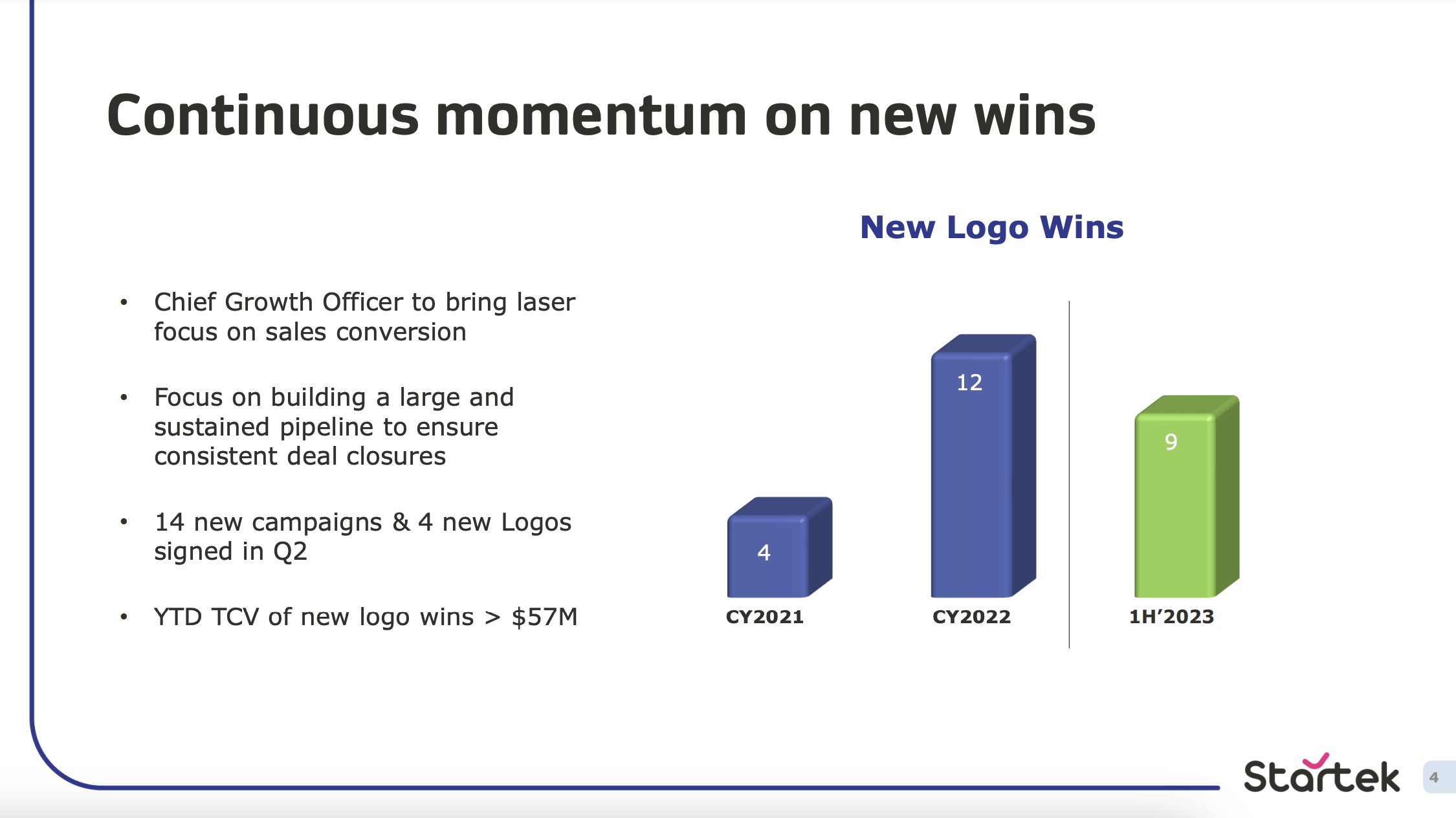

If we look at page two of the 2023 Q2 Investor Presentation , you can see evident misdirection in the stress on 'geographies', and 'new logos... delivered offshore'.

Second Quarter 2023 'Highlights' (Startek Q2 2023 Investor Presentation)

{kind=link}

Wouldn't the company be far better served, as stressed by my already clear analysis of poor operational efficiency, to again, stop focusing on 'new wins' and focus instead on bolstering the already uncompetitive core clients and business operations?

Startek 'New Wins' Q2 2023 (Startek Q2 2023 Investor Presentation)

{kind=link}

The more I have read of the reports, earnings presentations et al. along with the financials the more I am convinced the organisation is run rather like a small-scale private enterprise than a competitive, investor-attracting public company. The organisation continues to make conglomerate-like declarations and moves when instead it needs to get back to basics and focus on generating a healthy profit and loss statement and a much better balance sheet.

With a current cash-to-debt ratio of 0.29, I'd be surprised if the company can even pull off a successful turnaround at this stage. I'm not in the camp who thinks it can.

Startek 10-Year Cash & Equivalents Vs Total Debt (Seeking Alpha)

{kind=link}

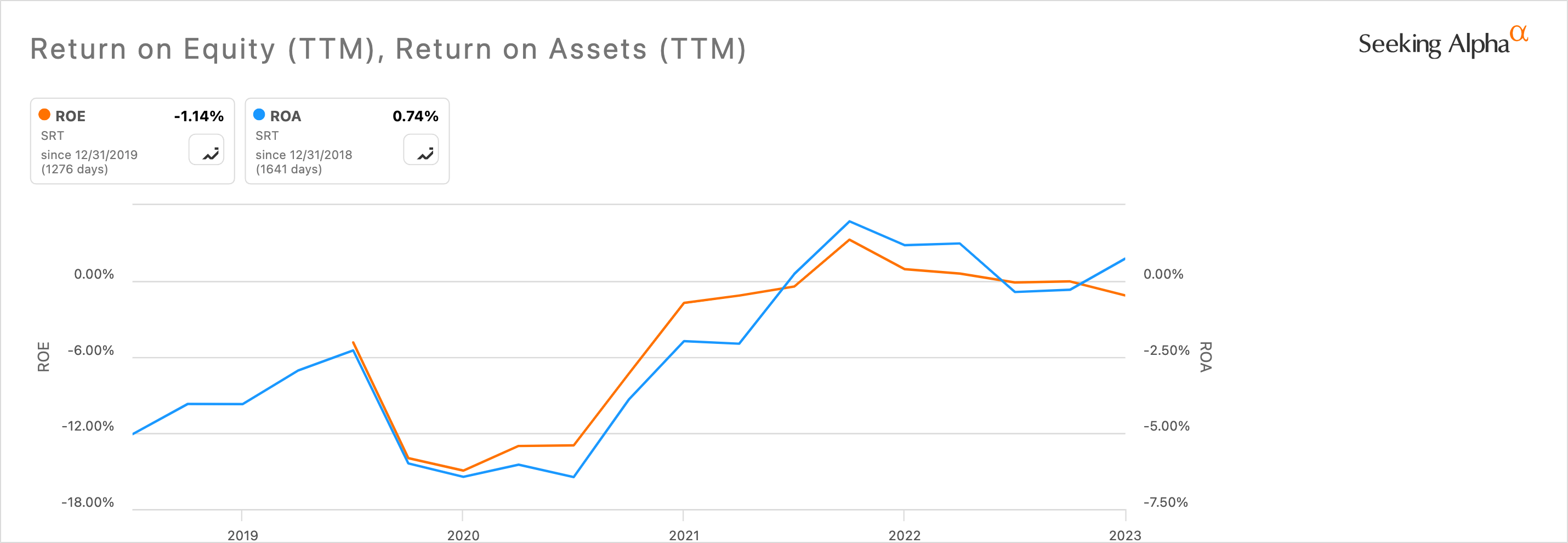

There's an immense amount of work to be done by the company. One of the core ways it could attempt to increase its situation is to increase its ROIC % (1.58%) versus its WACC % (6.43%). There's some light at the end of the tunnel when it comes to analysing the ROIC because against historical prices the trend is actually up quite significantly. Equally the ROE % is significantly up over time as is the ROA %.

Startek 5-Year Return on Equity & Return on Assets (Seeking Alpha)

{kind=link}

I'm still not convinced this is evidence enough that the company can successfully pull off strong future financial health. Particularly when I consider the current interest coverage, which is currently 0.54 and worse than 97% of industry competitors in my dataset of 1583 companies in the Software industry. Startek's interest coverage is also very poor based on the company's own historical downtrend, resulting in an unfavourable forward-looking debt profile.

Again, for a refined look at industry peers when comparing Startek on interest coverage, Computer Task Group has an interest coverage of 3.09, Unisys an interest coverage of 2.28 and a third contender, CSP ( CSPI ), has an interest coverage of 9.00.

If the metrics I have outlined were better it is indeed true that the stock price would be higher. In that respect arguably the price at current is relatively fair. However, my issue as a value and growth investor isn't that the stock is trading above or below fair value necessarily. Even if a company is trading below fair value, it has to be a compelling all-around fundamental and operational investment to seek reliable alpha over the long term. Unfortunately for Startek, based on my analysis its shares are neither trading at a decent intrinsic valuation nor do the management have reliable strategies and financial metrics to predict strong future success.

Valuation

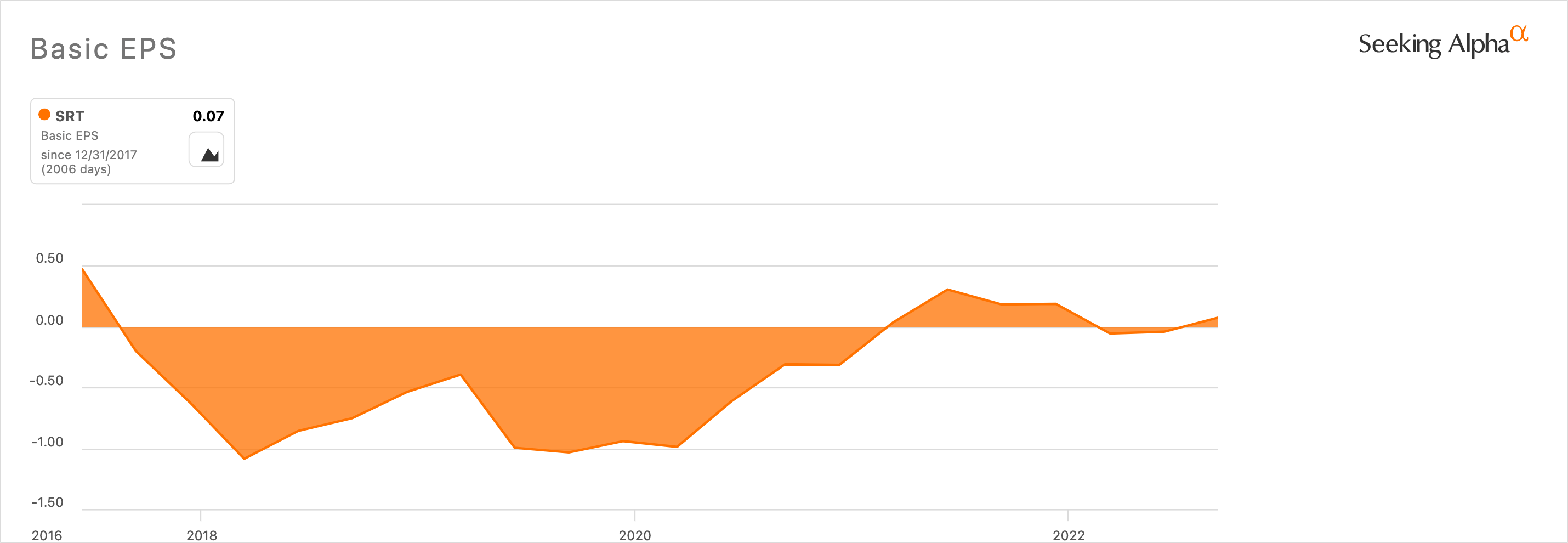

I also don't see the valuation of the company as a note of promise. The main reason is that the earnings per share are so inconsistent that we have barely any predictable growth rates to work off on a discounted cash flow basis.

Startek 10-Year Basic EPS (Seeking Alpha)

{kind=link}

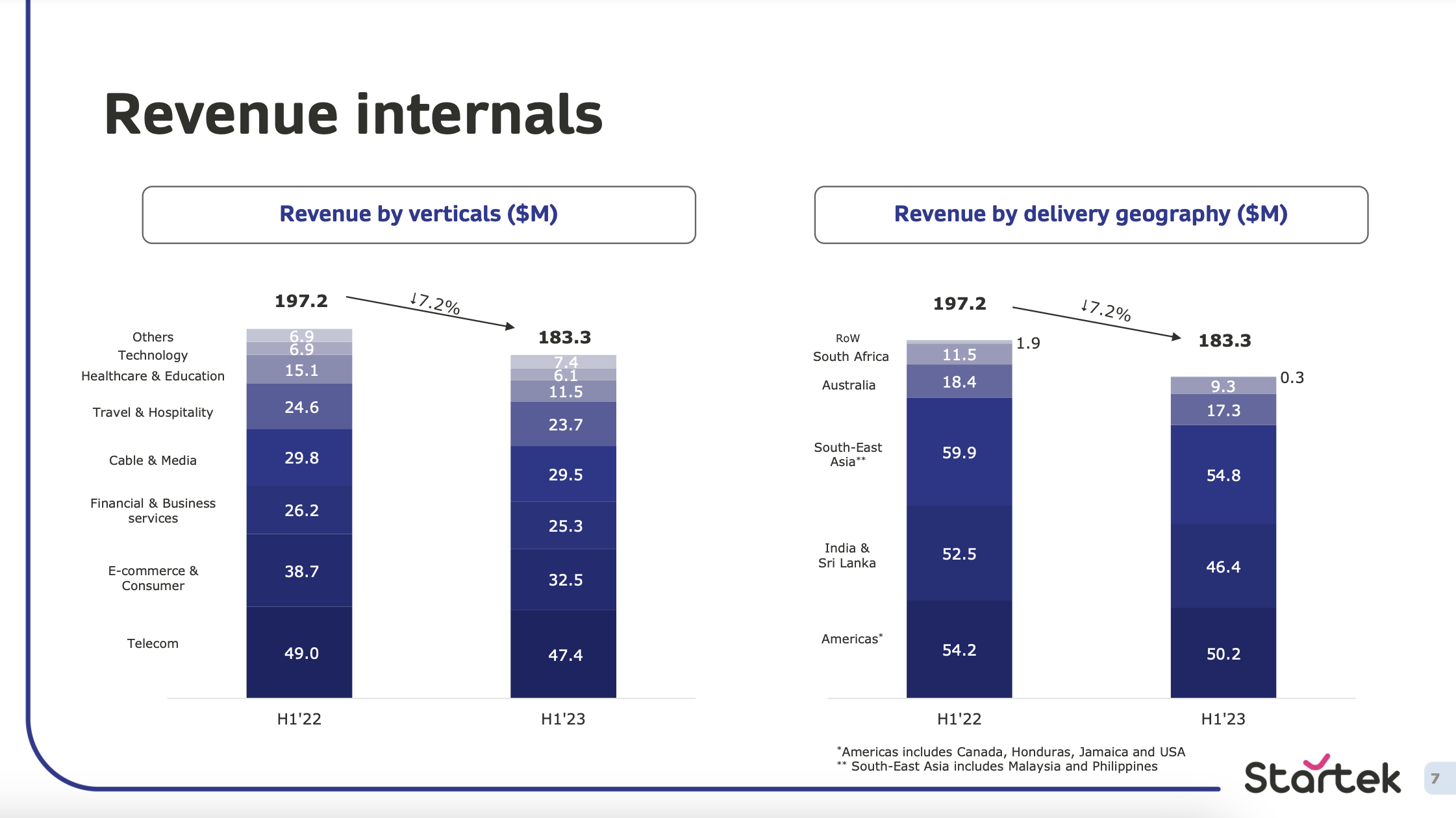

If I consider a 5% 10-year growth-stage rate for a discounted cash flow analysis, which is both defensive based on short-term metrics and generous based on long-term metrics (I think the company deserves a defensive approach) the margin of safety is -236.22%, with a fair value of $1.27 against a current stock price of $4.27. That also takes into consideration a 4% 10-year terminal stage and an 11% discount rate. Considering many consecutive years of negative earnings, I don't see a compelling reason to believe that earnings will remain in the green for the foreseeable future. Especially considering the 'sustained margins even with the decline in revenue base' outlined in the 2023 Q2 Investor Presentation .

Startek H1'22 Vs H1'23 Revenue (Startek Q2 2023 Investor Presentation)

{kind=link}

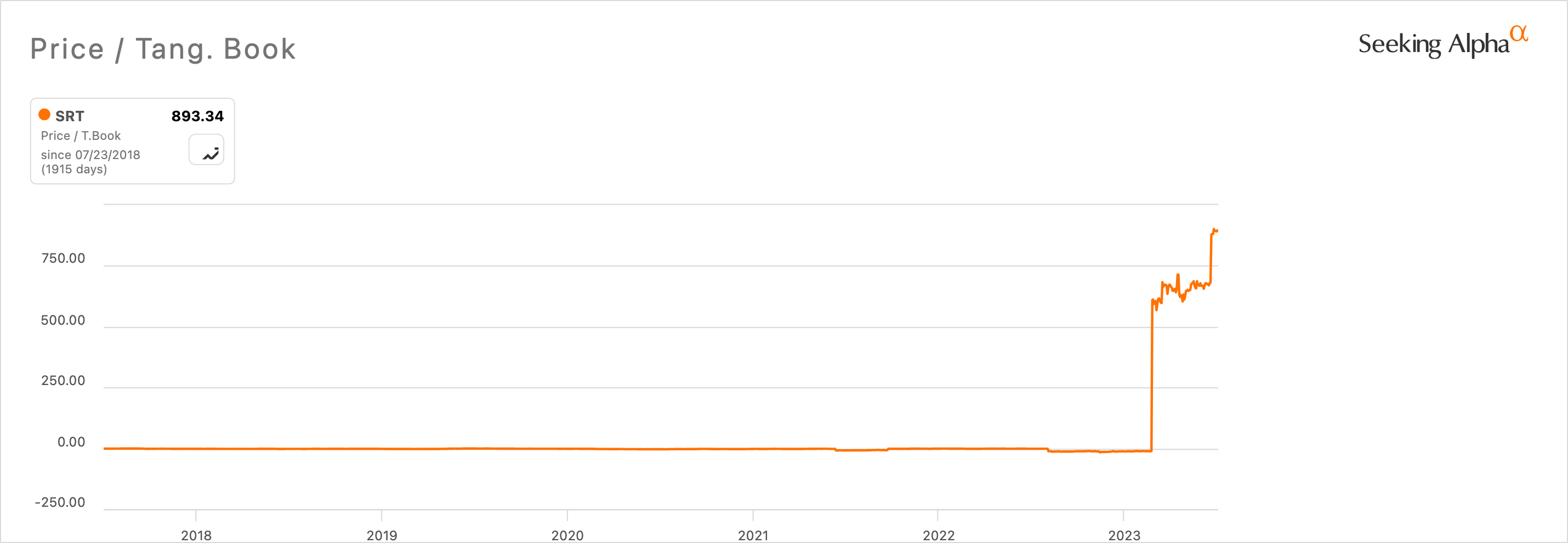

The price-to-tangible book situation is no better and is at the top of my concerns as a value investor, especially considering the terrible debt profile outlined earlier. The company currently has essentially no tangible book value, which based on my analysis reinforces that I am not buying anything of real value at all with an investment in Startek. Personally, as a defensive investor, who also wants to see strong, efficient and well-positioned operations for growth and momentum, I wouldn't pay above $1 per share. Even then, the investment would have to be a turnaround, which I'm not convinced the company is positioned to make.

StarTek 10-Year Price / Tang. Book (Seeking Alpha)

{kind=link}

Conclusion

I'm staying well away from Startek, Inc. I have seen very little compelling evidence from both operational strategy moving forward and past financial performance to even consider an investment. My rating is a firm Strong Sell.

For further details see:

Startek, Inc.: Unsophisticated Strategies