SCS - Steelcase: A Turnaround Story (Rating Upgrade)

2023-04-19 23:35:17 ET

Summary

- SCS posted an outstanding fourth quarter as the company nearly doubled its earnings estimates.

- SCS's fortunes seem to be on the rise as a result of many companies implementing return-to-office protocol.

- SCS appears to be undervalued based on various valuation methods.

Intro

Steelcase ( SCS ) is a well-established player in the office furniture industry that has been in business for over a century. The company designs and manufactures a wide range of furniture products, including chairs, desks, and storage solutions.

Its products are widely used in commercial, educational, and healthcare settings, among others. Despite facing stiff competition from other players in the industry, Steelcase has managed to maintain its market leadership position through a combination of innovation, customer-centricity, and operational excellence.

Recently, SCS posted an outstanding fourth quarter as the company nearly doubled its earnings estimates. In this article, we will delve into Steelcase's outstanding quarter and estimate the company's intrinsic value to help investors determine whether SCS stock is a sound investment opportunity in today's market.

Performance

Steelcase's recent earnings report showed positive results, with revenue and earnings growth driven by year-over-year pricing benefits. The company's Q4 Non-GAAP EPS of $0.19 beat expectations by $0.08, and its revenue of $801.7M (+6.5% Y/Y) beat expectations by $50.32M. These are welcomed results from investors of the Grand Rapids company as SCS has lost nearly two thirds of its market cap since the beginning of the COVID-19 Pandemic in 2020.

The COVID-19 pandemic has had a significantly negative impact on SCS, as a leading manufacturer of office furniture and workspace solutions. The pandemic forced many companies to implement work-from-home policies, which resulted in a sharp decline in demand for office furniture and related products. As a result, SCS experienced a significant decline in revenue and earnings during the early stages of the pandemic.

However, SCS's fortunes seem to be on the rise as a result of many companies implementing return-to-office protocols. The percentage of Americans working remotely was 43% in January 2022, which is a decrease from the 55% reported in October 2020.

This positive trend is reflected in the company's operating margin , which has improved by 330 basis points compared to the previous year. Furthermore, the company's year-over-year order declines showed a significant improvement in the fourth quarter, with a decline of 8% compared to 17% in the third quarter, which shows a more positive business environment for the company.

Additionally, SCS's first-quarter guidance points to further year-over-year earnings improvement, while the company aims to achieve fiscal 2024 earnings growth driven mainly by pricing increase from higher demand. This means that the company plans to increase its revenues and profits by leveraging its pricing strategy, rather than by relying on volume growth alone. This is an encouraging sign for investors, as it suggests that SCS is confident in its ability to maintain a competitive edge and drive demand for its products.

However, it's worth noting that achieving earnings growth driven largely by pricing increases is not without its risks . If SCS's competitors respond with aggressive pricing strategies of their own such as lowering their pricing, SCS may need to adjust its own pricing strategy, which could affect its revenues and profits.

Additionally, SCS might not be able to keep offering their products at the higher price points if they can't stay ahead of their competition. For example, if they fail to develop new products that support hybrid work, protect privacy, and enhance productivity, they may lose their edge and their ability to maintain the higher pricing. Nonetheless, SCS's guidance and plans for earnings growth are positive developments for a company that has been beaten down in recent years.

Valuation

While SCS's strong performance in the fourth quarter and its promising outlook for fiscal 2024 earnings growth may be encouraging for investors, it's important to remember that a company's financial health must also be considered in relation to its current stock price. Therefore, as intelligent investors we will employ a couple of different valuation techniques to estimate SCS intrinsic value to help determine if the company is a smart buy in today's market.

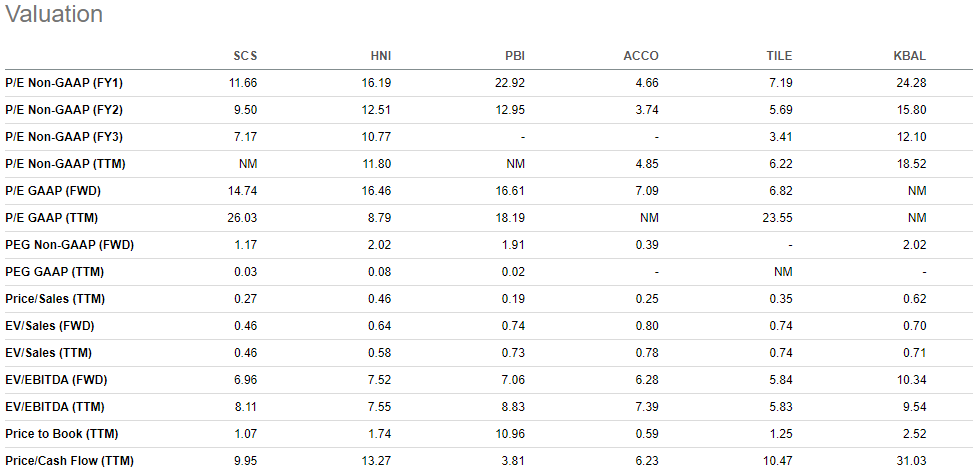

We will begin by comparing SCS's current valuation against its industry rivals to see if SCS's is priced favorably compared to its competitors. On Seeking Alpha's "Peers" page, investors can compare SCS against its industry competitors by using a range of popular valuation ratios, such as the price-to-earnings ratio (P/E), price-to-sales ratio (P/S), and price-to-book ratio (P/B), among others.

All of these ratios have one thing in common, lower ratios indicate better value for the company. By calculating the average of all these ratios listed in the image below, investors can identify the most undervalued company by finding the company with the lowest score.

{kind=link}

Just like in golf, the lowest score wins, or in this case the lowest score indicates the most undervalued company. Based on the data, the company with the lowest score is ACCO Brands Corporation ( ACCO ) with a score of 3.59. ACCO is a multi-faceted company that specializes in designing, manufacturing, and selling products that cater to various needs of consumers, schools, and offices.

On the other hand, Kimball International Incorporated (KBAL), which designs and manufactures furniture for the office and hospitality industries, ended up with the highest score of 10.68, which indicates that it may be overvalued compared to its peers.

Finally, SCS had decent results finishing third in this exercise with a score of 6.97. This suggests that SCS may be better than average in terms of being undervalued compared to its industry rivals. The full results are below.

1) ACCO - 3.59

2) TILE - 6.01

3) SCS - 6.97

4) HNI - 7.36

5) PBI - 8.07

6) KBAL - 10.68

It is worth noting that this valuation exercise has its limitations, as only the PEG ratios above directly take into account the company's future growth prospects, which are essential in determining a company's intrinsic value. Therefore, to provide a more comprehensive analysis, we will use another valuation technique that considers a company's growth potential: the discounted cash flow analysis.

We will start the DCF by using the average free cash flows of SCS from the previous five years, which is $57 million. We will then use a growth rate of 10% per year for the next ten years, considering the average analyst growth estimates for the next few years.

We will assume a growth rate of 2.5% per year following the 10th year to find the company's terminal value. The discount rate used to discount the cash flows will be 10%, which is based on the long-term return of the S&P 500 when dividends are reinvested. With these inputs we can conclude that the estimated intrinsic value of SCS is $11.93 which represents nearly a 47% increase from the company's current share price. Therefore, SCS appears to be significantly undervalued based on this DCF analysis.

{kind=link}

Takeaway

SCS has reported an outstanding fourth quarter, which saw its non-GAAP EPS of $0.19 and revenue of $801.7m beat expectations. Despite the impact of the Covid-19 pandemic, the company's fortunes appear to be improving due to return-to-office protocols implemented by many firms. SCS plans to achieve fiscal 2024 earnings growth through pricing increases rather than volume growth alone. While this approach is not without its risks, the company's guidance and earnings growth plans are positive developments.

A total valuation analysis using data provided by Seeking Alpha suggests that SCS may be undervalued compared to many of its peers in the office furniture industry. In addition, a discounted cash flow analysis seems to confirm these results that SCS is currently an undervalued stock. I had previously written about SCS last Fall and at the time I gave the company a sell rating, but SCS seems to be turning its business around and data now signals buy.

For further details see:

Steelcase: A Turnaround Story (Rating Upgrade)