SCS - Steelcase: Q3 2023 Shines Little Light On Future Growth Prospects

Summary

- Steelcase has surpassed EPS expectations for the last three quarters, the company looks towards hybrid workspace solutions, cost-cutting and diversifying revenue but with little promise of future growth.

- Steelcase is no longer the leading office furniture company and Q3 2023 reports that orders across all segments have decreased 17% YoY.

- Cautious of downward trending fundamentals, annually increasing debt, negative cash flow, insufficient equity to pay off dividends and lack of innovation.

Last year 110-year-old Steelcase Inc. ( SCS ) lost its long-term position as the globe's largest office furniture company by revenue to MillerKnoll ( MLKN ). The COVID-19 pandemic crashed the office furniture industry space and required companies to make dramatic changes. MLKN acquired a dominant competitor, and invested in design, the gamer market and its online presence. SCS has yet to make any significant moves, and its lack of growing revenue is worrisome.

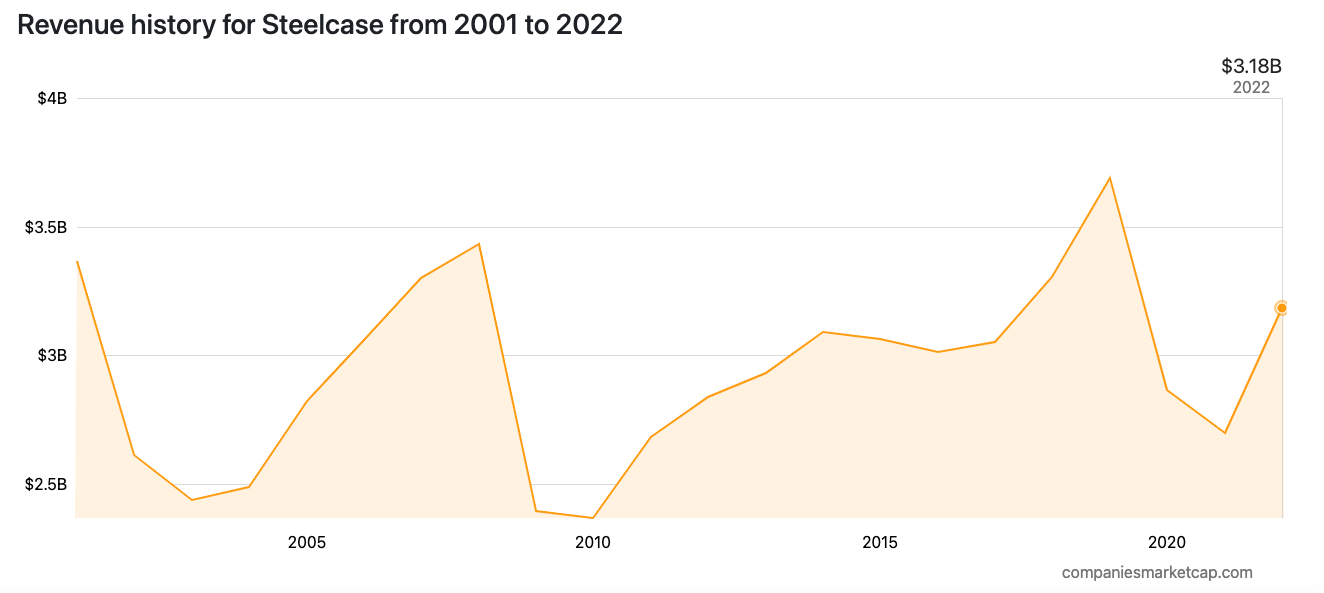

Revenue history (companiesmarketcap.com)

{kind=link}

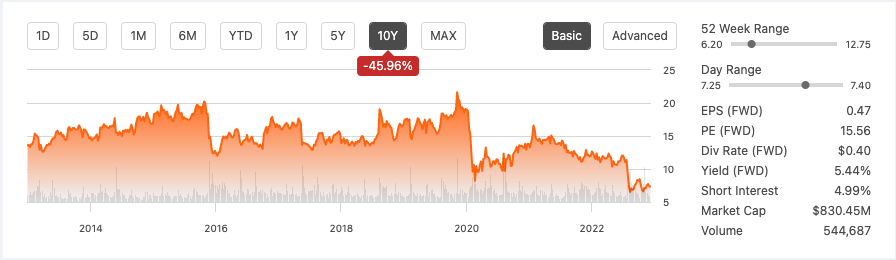

With a high debt of $727.30 million and a small market cap of $830.45 million, investors should tread cautiously. The stock has been trending downward for the last ten years.

Ten-year stock trend (SeekingAlpha.com)

{kind=link}

The workplace has gone through a significant shift. Most significantly, it has changed from where people are required to attend to one they choose to follow. While SCS remains one of the leading office furniture companies, it is focused on cost-cutting, diversifying its revenue into highly competitive markets such as education and selling directly to consumers. Although the stock has a long history of paying dividends, its earnings do not cover the payout. The management team have painted an incomplete picture of future growth opportunities and orders have only continued to decrease. For this reason, I rate SCS as a cautious hold.

Company overview

SCS, founded in 1912 and IPOd in 1998 , provides furnishings and solutions for workspaces, such as office chairs, desks and sofas. It is an international player with over 800 dealer locations in 17 countries, although until now 2/3 of total revenue is from the USA. SCS has much-loved brands , with frequently rated the number one office chair. It has fifteen manufacturing locations, eight of which are outside of North America. It generates revenue from three main segments, Americas, EMEA and other categories. If we zoom into the Americas segment we can see that most of the revenue is from corporate / other, followed by education and healthcare markets below.

Revenue Mix for US market (Investor Presentation 2022)

The corporate vertical is decreasing and not predicted to recover to pre-COVID-19 numbers. SCS is focused on providing hybrid solutions and diversifying its revenue streams. Education, B2C, EMEA and APAC are seen as potential growth markets. It also plans to leverage technology to improve customer experiences and increase direct-to-consumer selling. Traditionally the office furniture industry is heavily face-to-face. SCS would even fly its potential customers in on company planes . Furthermore, the company is taking on tremendous cost-cutting efforts. It is closing down its Denver regional distribution centre and selling the aviation division for $3 million and long-term savings of $11 million.

Industry and competitor shift

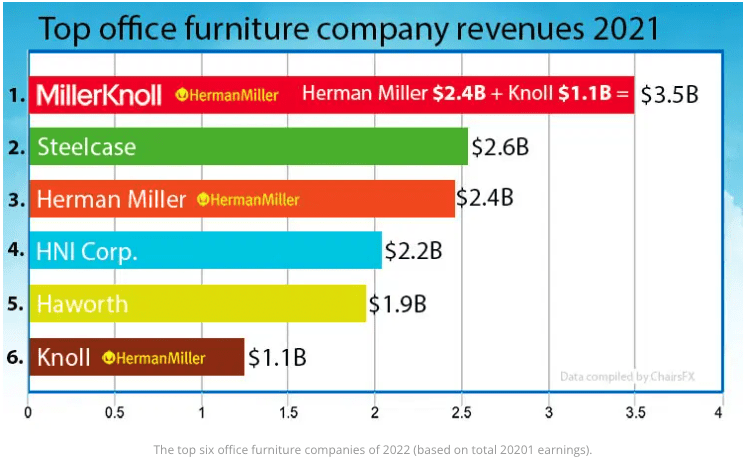

Office furniture companies all took a significant hit in 2020, and it was clear the workplace industry took on a disruptive change. Until 2021, although SCS was not experiencing significant growth as a business, it was comfortably the largest global office furniture company. In July 2021, a substantial acquisition of Knoll by the second largest player, Herman Miller, created MillerKnoll, building a new face to take on the changed industry.

Top office furniture companies by revenue (chairsfx.com)

{kind=link}

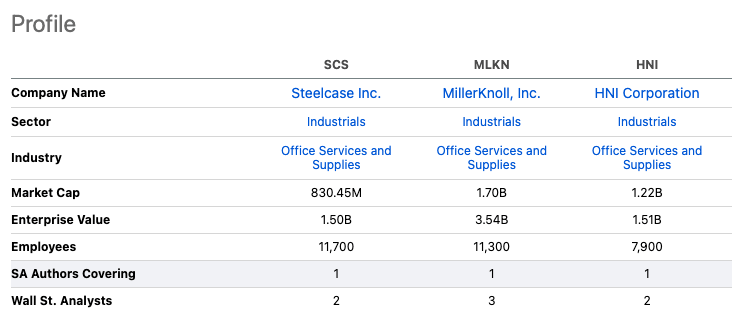

People are not looking to work in uncomfortable work environments and these furniture companies will succeed in luring workers back into the corporate space while also tapping into the home office environment through hybrid solutions. If we compare SCS to its two most dominant peers we can see that it is trailing behind with a smaller market cap of $830.45 million and a smaller enterprise value of $1.5 billion which is made up of a significant amount of growing debt.

Peer comparison (SeekingAlpha.com)

{kind=link}

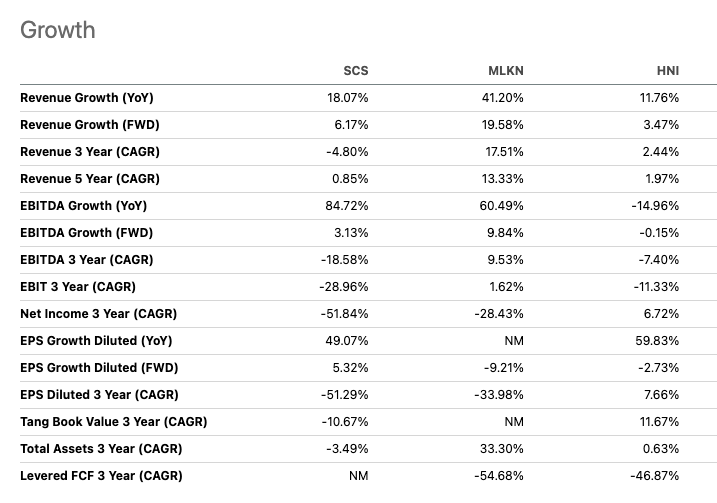

If we look at revenue growth ToT and a 5 year CAGR, MLKN has taken on a much better growth strategy than SCS.

Growth comparison (SeekingAlpha.com)

{kind=link}

Financials and valuation

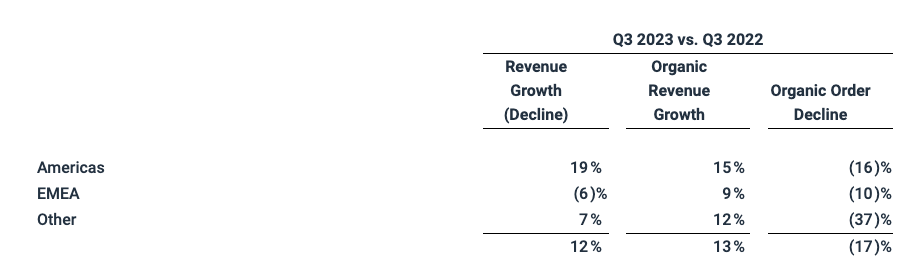

SCS is not producing particularly uplifting results, and its future consists of significant cost-cutting efforts and diversifying its revenue streams. The company has not made impressive growth trends in over a decade. In December 2022, SCS released its Q3 2023 quarterly results with revenue of $826.9 million and net income of $11.4 million. Both of these increased YoY; however, we cannot ignore how quickly orders are decreasing across all segments.

Order decline in Q3 2023 (sec.gov)

{kind=link}

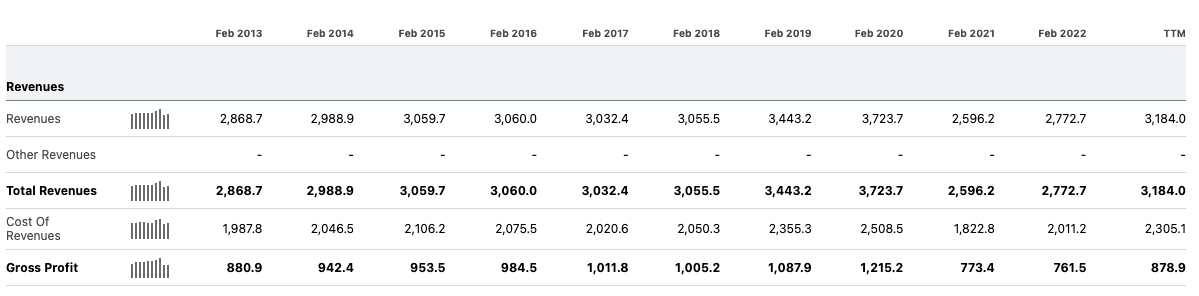

If we look at the annual revenue, we see a downward trend, ignoring FY2020. This year the company has a TTM of $3.184 billion, mainly due to price inflation. The gross profit margin has also been downward, trending to under 30%.

Annual revenue and gross profit (SeekingAlpha.com)

{kind=link}

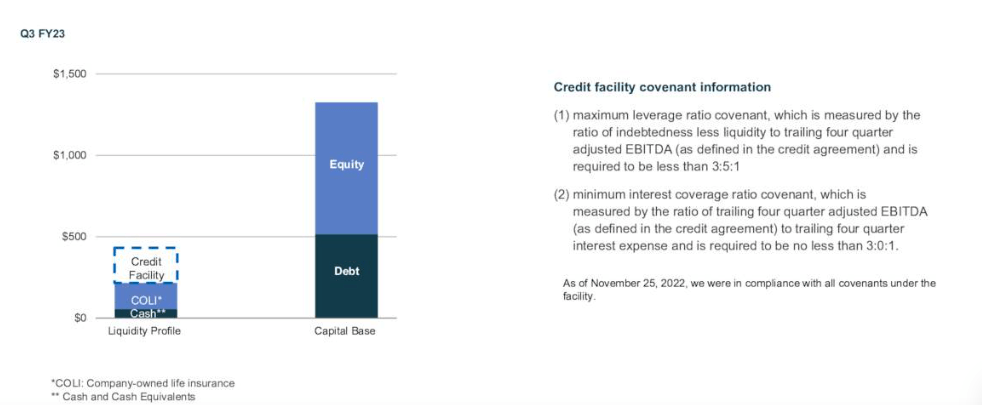

If we look at the balance sheet, we can see that total debt has been increasing annually and is currently at $727.30 million, and the company only has $55 million in cash and short-term investments. If we look at the company's liquidity, we can see that it has a current ratio of 1.35. However, its quick ratio is below one at 0.69, meaning there are not enough liquid assets to pay short-term liabilities. Below we see that the company uses a credit facility and company-owned life insurance to maintain its liquidity profile.

Balance sheet liquidity profile (Investor presentation 2022)

{kind=link}

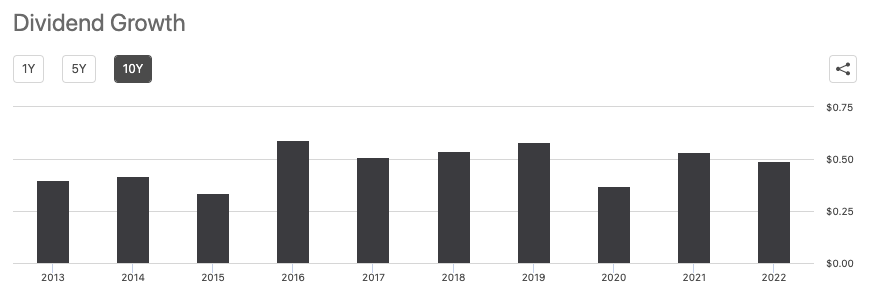

SCS has a quarterly dividend program and pays a fwd dividend of 5.44%. Its last payout was $0.10 per share on 13 January 2023, with no new ex-dividend date. Its payout ratio is worryingly high at 157.35%, as it does not have enough earnings to cover the payout, so the company would have to take out debt if it wants to maintain it. We can see that the dividend was cut significantly during the COVID-19 year.

Dividend growth history (SeekingAlpha.com)

{kind=link}

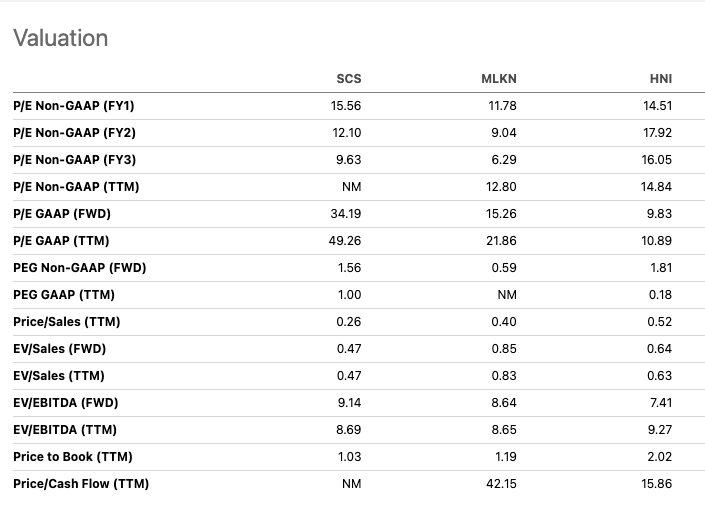

SCS has a price-to-earnings ratio of 15.56, which is higher than its peers, and if we include growth, SCS does not look attractive compared to MLKN, although at 1.56, it is valued lower than HNI at 1.81. SCS has a very attractive price-to-sales ratio of 0.26, but we should consider that the company has significantly seen fewer orders across all segments and expects this to continue shortly. Analysts have mixed reviews on the stock, Seeking Alpha's Quant rating is a 3.02 Hold, and it is currently trading under its average price target of $9.

Relative valuation (SeekingAlpha.com)

{kind=link}

Risks

Although there is weight to the fact that this company has existed for over 100 years, its fundamentals have been downward trending for over a decade, and it has not recovered from COVID-19 losses or performed well under the weakening economic market of 2022. Based on financials, SCS is heading into challenging waters. There is a risk to investing in companies that are not showing growth. We also see negative cash flow in FY21; TTM levered cash flow is currently 20.81 million. This means there is no money to put back into the business and pay out dividends. However, the company will make substantial cost cuts, such as selling off aviation, which should increase cash substantially.

Levered annual cash flow (SeekingAlpha.com)

Final thoughts

Although SCS has been around for 110 years and is a reputable brand with quality products, we can see that even before COVID-19 disrupted the workspace forever, SCS was not significantly growing its top and bottom line. Gross margins have been diminishing, orders across all three segments are decreasing, and the company is now focused on staying afloat by taking on significant cost-cutting while diversifying revenue in smaller markets such as education. It has lost its position as a market leader since 2021, and its main competitor is growing much faster. While the company has surpassed EPS expectations for the last three quarters, and the cash situation is likely to improve with the cost-cutting efforts, fundamentals are downward trending and management has not given a clear growth route. For this reason, I recommend a hold rating.

For further details see:

Steelcase: Q3 2023 Shines Little Light On Future Growth Prospects