SCS - Steelcase: Shares Remain Cheap Based Off Forward EPS Estimates

2023-04-19 08:58:05 ET

Summary

- Company reports excellent numbers in its fourth quarter.

- Gross profit rise and better supply chain conditions result in an excellent cash flow performance.

- Technically, shares recently made a higher high. We believe this trend will continue.

Intro

We wrote about Steelcase Inc. ( SCS ) roughly 10 months ago when we stated that we believed higher prices were on the horizon for the furniture supplier. Although we remain bullish on Steelcase, shares though at their current level of $8.12 remain down approximately 24% since we penned our piece. The announcement of the dividend cut (To $0.10 per quarter) was not taken well by the market back in September of last year, which basically tied in with a slew of spending cuts when Steelcase's second-quarter numbers were announced.

Furthermore, Q3 guidance at the time was less than impressive, as inflation and supply chain impediments were expected to continue to eat into the company's margins. Although Steelcase was managing to offset higher costs by sustained pricing efforts on the front end, investors were reading into lower spending trends, confirmed by the announcement of 180 positions to be let go by the company.

So essentially, investors on the long side in Steelcase at the time received a double whammy here, which were the spending cuts (Due to the subdued trend at the time concerning corporates returning to the office) and the $0.05 quarterly cut in the dividend. However, when we fast-forward six to seven months, we see a whole different technical arrangement regarding Steelcase where the company's fourth-quarter earnings seem to have been the instigator for another potential bull run to the upside.

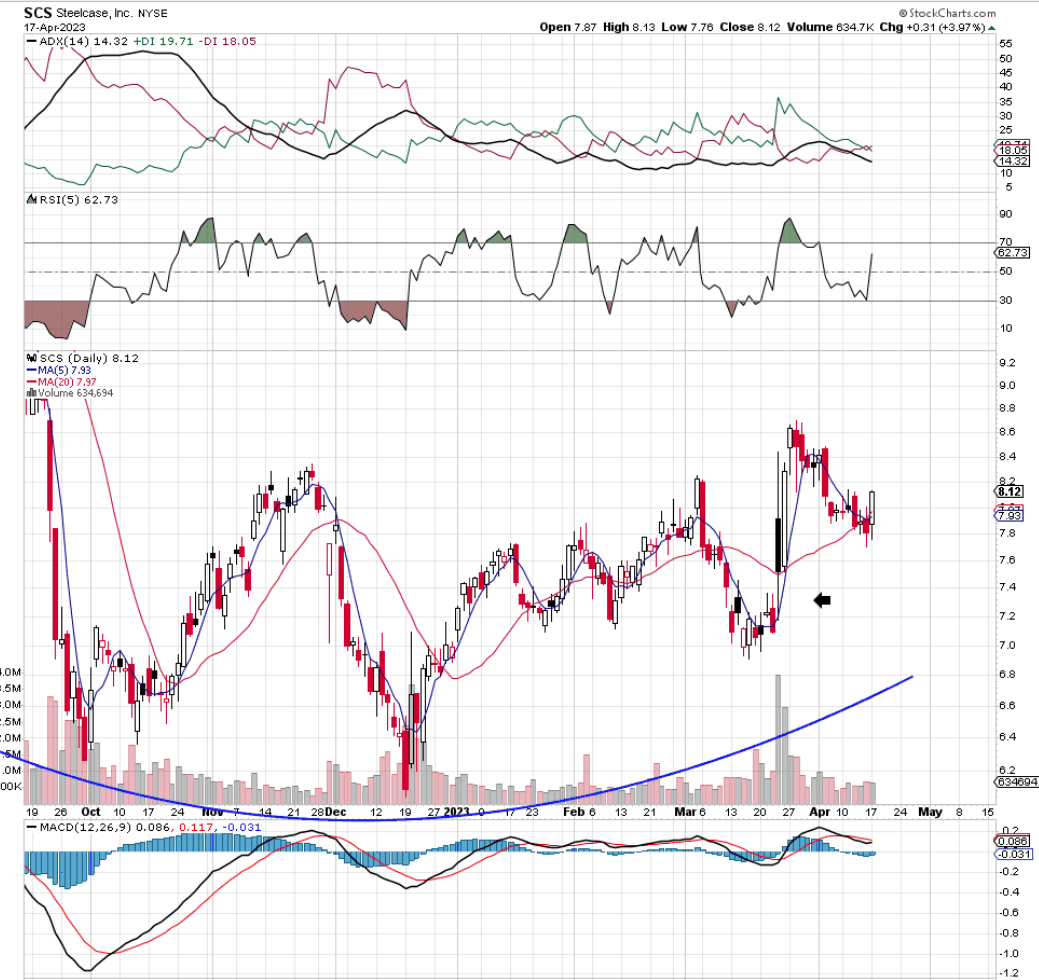

Steelcase Technical Chart (StockCharts.com)

{kind=link}

Q4 Strength

As we see above, shares rallied on strong volume on the announcement of Q4 numbers, with the key takeaway being that the rally had enough momentum to take out the stock's November 22 highs. This higher high was key in that now we have a strong possibility that shares are undergoing a technical bottoming pattern. In fact, the company's fourth-quarter numbers and forward-looking trends seem to be pointing to the same.

Considering what had gone before in Steelcase (Especially on the sales side), few would have predicted the company's resounding Q4 beats in both the company's top-line sales and earnings. Steelcase reported $0.19 in earnings per share for Q4 ((Beat of $0.08) on sales of $801.7 million ($50.32 above the estimate). Elevated demand and higher pricing were the core reasons for the impressive results in the quarter. Furthermore, there were a few key trends in the quarter that demonstrated that the "environment" for sustained increases in Steelcase's profitability should continue for some time here.

Gross Profit On The Rise

Firstly, gross profit of $239 million resulted in a higher gross margin print of 29.83% for the quarter (Trailing 12-month average of 28.52%). This led to the elevated $15.7 million net profit number for the quarter, which in turn ended up generating $88 million of operating cash flow (which incidentally was the best quarterly cash-flow number for quite some time). Suffice it to say, Steelcase's growing gross margin and higher cash-flow generation all point to a stronger outfit where management is expected to have the wherewithal to keep investing aggressively behind its most pressing initiatives, which in turn should lead to higher profitability

In fact, companies normally increase their returns by either turning over profits quickly or by increasing margins. Steelcase actually managed to execute on both of these in its recent fourth quarter. Sale prices as mentioned increased and supply chain enhancements led to much-improved fulfillment rates, resulting in more shipments being captured in the quarter.

Volumes Increasing In Health & Education

Management also tempered its full-year guidance for fiscal 2024 due to where the backlog (14% Lower) is starting off the year compared to the start of fiscal 2023. While this may mean that fewer orders are booked in the near term, Steelcase's growth in the likes of health and education should be able to offset the decline in sales from the bigger corporates to some degree. Furthermore, although the large corporate side is expected to decline in fiscal 2024, the trend here again is favorable as more workers seem to be beginning their return to the corporate offices.

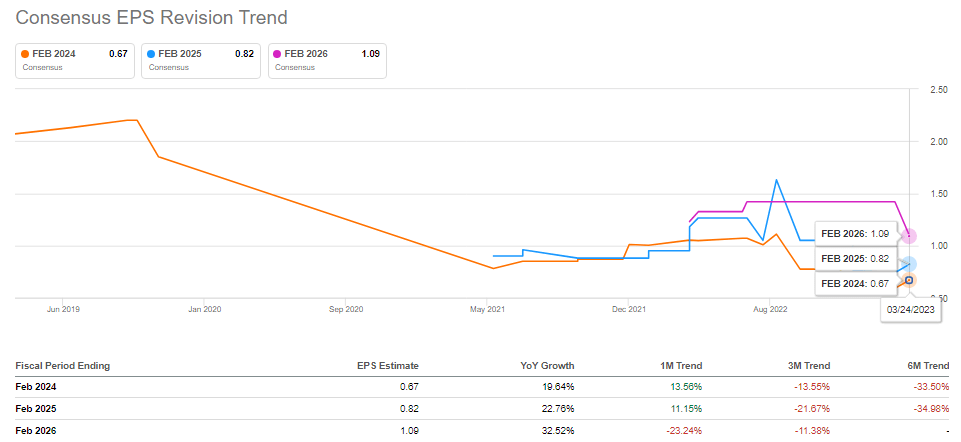

Therefore, when one boils everything down, multiple growth trends have analysts expecting up to 20% bottom-line growth in fiscal 2024 followed by up to 23% the following year. We will be watching closely to see if Steelcase's momentum (Concerning forward-looking EPS revisions ) can indeed continue.

Steelcase Forward-Looking EPS Revisions (Seeking Alpha)

{kind=link}

Conclusion

To sum up, Steelcase's increasing gross margin, stronger cash flow & keen valuation all tie into the bullish case in this stock. Let's see if shares can now take out their recent March highs over the upcoming sessions. We look forward to continued coverage.

For further details see:

Steelcase: Shares Remain Cheap Based Off Forward EPS Estimates