SCS - Steelcase: Showing Signs Of A Turnaround

2023-06-26 21:17:44 ET

Summary

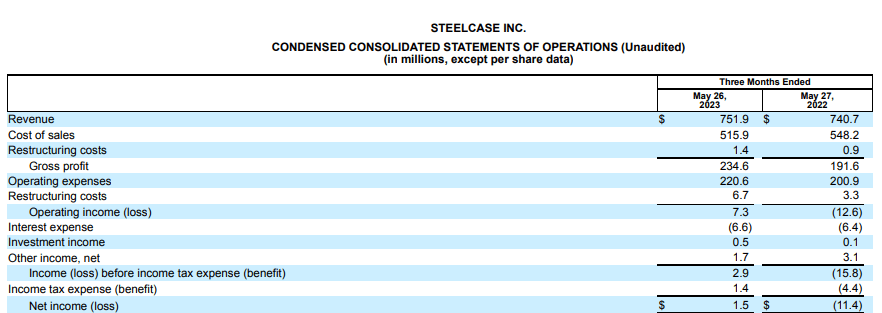

- SCS reported Q1 FY24 revenue of $751.9 million, a 1.5% increase compared to Q1 FY23, with net income of $1.5 million compared to a loss of $11.4 million in Q1 FY23.

- SCS is undervalued based on its P/E and PEG ratios, but its international segment performance remains weak due to economic uncertainty in EMEA and China regions.

- I assign a hold rating on SCS, recommending waiting for the international segment to recover before investing.

Steelcase Inc. ( SCS ) offers a portfolio of architectural and furniture products globally. Their furniture portfolio includes fixed and height-adjustable desks, tables, storage, accessories, and mobile power. They also provide wall coverings, lease origination, and asset management services. SCS recently announced its Q1 FY24 results . In this report, I will analyze its Q1 FY24 results . I believe SCS is undervalued, but there is still some work to do. Hence I assign a hold rating on SCS.

Financial Analysis

SCS recently posted its Q1 FY24 results . The revenue for Q1 FY24 was $751.9 million, a rise of 1.5% compared to Q1 FY23. I believe the revenue increase in the Americas segment was the main reason behind the revenue increase. The revenues from the Americas segment grew by 5% in Q1 FY24 compared to Q1 FY23. I think a high pricing policy and faster order fulfillment patterns were the major reasons behind the revenue growth in the Americas segment. Its gross profit margin for Q1 FY24 was 31.2%, which was 25.8% in Q1 FY23. I believe better operational efficiencies and a favorable pricing policy led to an improvement in gross margins.

{kind=link}

Seeking Alpha

The net income for Q1 FY24 was $1.5 million compared to a loss of $11.4 million in Q1 FY23. In my opinion, the financial performance of SCS in Q1 FY24 was quite impressive. Despite the tough market conditions and bad performance in the international markets they managed to be profitable in the quarter and I believe it was mainly due to efficient management. They implemented a favorable pricing policy and took steps to control the costs, which led to better financial results for the company. I think if the management continues to take such steps in the coming quarters, we might see better top-line and bottom-line growth in the coming quarters.

Technical Analysis

{kind=link}

Trading View

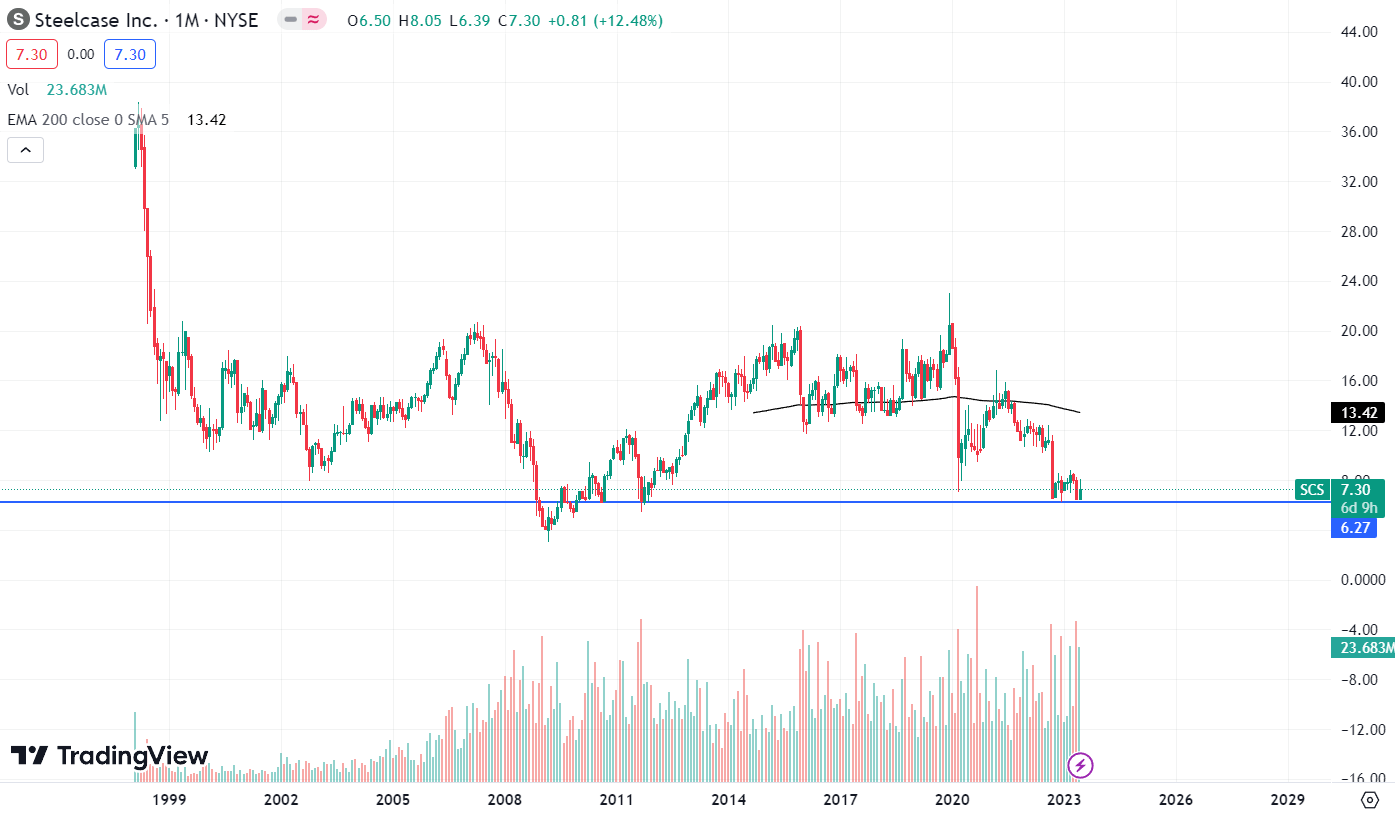

SCS is trading at the $7.3 level. The chart of SCS is quite interesting, and I believe it can be a great rewarding trade in the coming times. Since its IPO debut, the stock has fallen almost 80%, proving to be a wealth destroyer; however, it is currently at an interesting level. I have marked a horizontal line in the chart at the $6.3 level, which has been acting as a solid support zone for the stock. Since 1998 the stock price has breached the support zone just once, which shows the significance of the $6.3 level, and currently, the stock is near the $6.3 level. So, in my opinion, one should wait for the stock to reach the support zone, and once the stock reaches the $6.3 level, then one can start buying the shares with a stop loss of 15% and a minimum target that I think we can expect is 50%. Because of the excellent risk-to-return ratio, I believe this setup is excellent.

Should One Invest In SCS?

First, talking about their valuation. I will use P/E and PEG ratios to judge SCS's valuation. The P/E ratio of a company is calculated by dividing a company's stock price by the EPS, and the PEG ratio of a company is calculated by dividing a company's P/E ratio by its annual EPS growth. SCS has a P/E [FWD] ratio of 11.27x compared to the sector ratio of 16.82x and has a PEG [FWD] ratio of 1.13x compared to the sector ratio of 1.63x. After looking at the ratios, I believe SCS is undervalued.

I think they are still on the path to recovery. For the past two years, high inflation and supply chain disruptions have affected their business, severely affecting their revenue growth. But with these headwinds now under control and the management's constant efforts to control costs, this is now resulting in better margins, and the revenue is now getting to the pre Covid levels. The company is showing signs of a turnaround with good financials and a strong technical chart. In addition, its valuation is also attractive, but I only have one issue, its performance in the international markets, especially in the EMEA and China regions. There is still economic uncertainty in international markets, due to which their revenues in the international segment are declining. The EMEA region's economy is slowing down as a result of various clients talking about a reduction in investment activity in 2023. Hence I would wait for the situation in the international markets to become normal, and once the situation is under control, I think their revenue growth would get a solid boost, and their margins and net income would increase significantly. Hence after looking at several factors, I assign a hold rating on SCS.

Risk

SCS has deferred tax assets totaling $36.5 million and $17.9 million in tax credit and net operating loss ("NOL") carryforwards, respectively, against which valuation allowances totaling $3.1 million have been recorded. Foreign jurisdictions are largely involved with NOL carryforwards. Foreign tax credits and foreign investment tax credits are included in tax credit carryforwards. They might not be able to implement tax, business, or other planning strategies to fully utilize the recorded value of their NOL and tax credit carryforwards or generate enough taxable income from future operations in the jurisdictions in which they maintain deferred tax assets related to NOL and tax credit carryforwards. Because these deferred tax assets are recorded in various currencies that are also subject to foreign exchange risk, their potential realization may be less than expected. Furthermore, they might be unable to use all of their NOL and tax credit carryforwards if future tax rules or interpretation change.

Bottom Line

SCS is doing financially well, and its stock price is near the strong support zone. SCS is showing signs of a turnaround. But there is still some work left to do - its international segment is showing weakness. Hence I think we should wait until their international segment recovers. Hence considering all the factors, I assign a hold rating on SCS.

For further details see:

Steelcase: Showing Signs Of A Turnaround