TSLA - Stellantis: Great Business With Significant Potential Upside

Summary

- Stellantis is a combination of Italian Fiat and French PSA. The Group has double-digit market share in over 12 countries.

- We see headwinds derived from a deterioration in market conditions and a stagnation of sales in Europe and North America.

- Positives include a strong EV offering and superior margins compared to their peers. The business makes up for its lack of strong growth with profitability.

- The business holds €14.63-per-share in cash, which exceeds their share price. On a net basis, this amounts to €5.96-per-share.

- Stellantis is bizarrely trading at 1x EBITDA, 5x below its peer average. The business is completely mispriced by markets, and we very conservatively value the upside as 63%.

Company description:

Stellantis N.V. ( STLA ) is an automotive business which design, engineering, manufacturing, distribution, and sale of automobiles and light commercial vehicles, engines, transmission systems, metallurgical products, and production systems worldwide. It provides luxury, premium, and mainstream passenger vehicles; pickup trucks, sport utility vehicles, and commercial vehicles; and parts and services, as well as retail and dealer financing, leasing, and rental services.

The business was formed in 2021 as a 50-50 merger between Fiat Chrysler and PSA Group and is listed on the Italian Borsa and French Euronext. This makes Stellantis the 5th largest automaker in the world.

Stellantis owns several regionally significant brands including Vauxhall, Fiat, Dodge and Citroen. As well as luxury brands with Alfa and Maserati.

{kind=link}

Stellantis Brands (Stellantis)

What initially drew our interest in Stellantis was its absurdly low valuation. It is so low that there must be something incredibly wrong with this company. If this isn't the case, Stellantis could be one of the best investments made in 2023. Within this paper, we will look to conduct an overarching analysis of the business, including an assessment of current economic conditions, key trends in the automotive industry and an assessment of their current financials. We will conclude with a relative analysis against peers, with an eye on valuation.

Economic considerations:

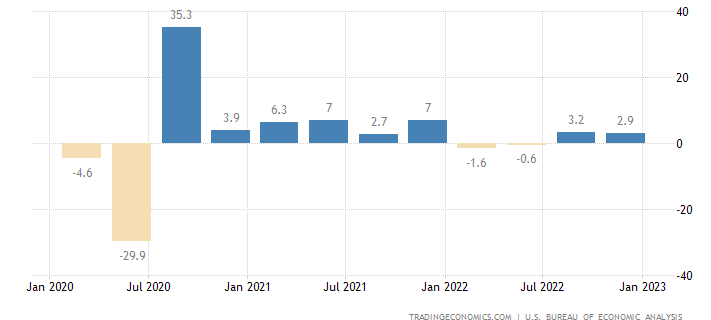

Economic conditions began to deteriorate in 2022, with GDP growth beginning to slow, and in many cases decline. The US saw two successive quarters of negative growth in 2022, although did bounce back in H2'22.

{kind=link}

US Economic Growth (Trading Economics)

The leading contributing factor to this is increasing interest rates around the world. Greater rates make it far more expensive for consumers to borrow, while also increasing their cost of living. This has been purposely done to cool demand, as inflation is currently at unsustainable rates. This continues to be driven by supply chain issues and rising energy prices. This has been very hard on many consumers, as they see their income deteriorate on both fronts.

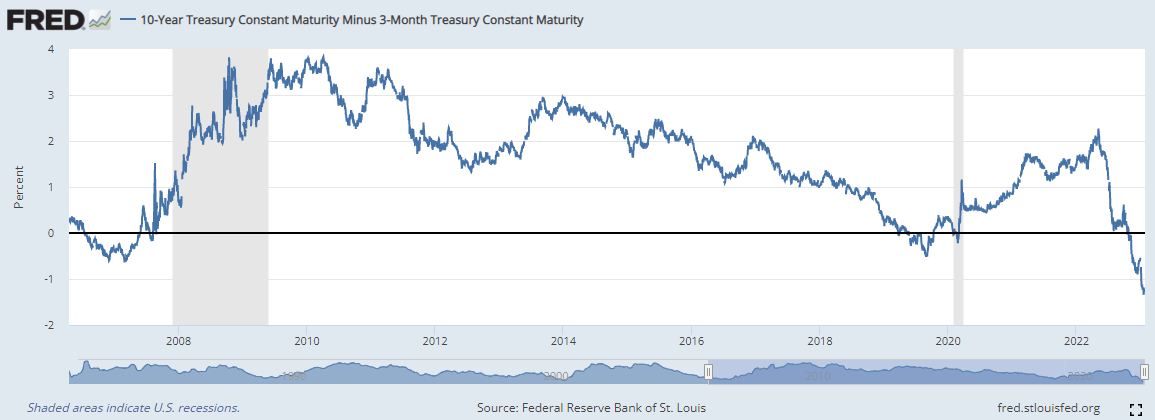

Going forward, we expect things to continue to weaken. Inflation expectations remain high in many nations with interest rates forecast to grow further in the US , UK and Eurozone . The 10-year / 3-month yield curve inverted in late 2022, suggesting a recession may be impending. This will further depress consumer sentiment and drive a further decline in demand.

{kind=link}

10Y/3M Yield Curve ((FRED))

This is likely to be an issue for Stellantis as if consumers are struggling to meet their current obligations, discretionary spending / significant outlays will be deferred or cancelled. Those who must purchase an automobile will likely go for a cheaper option, being the second-hand market.

Change in the market fundamentals:

The automotive industry operated historically as a two-tiered system. New cars would be readily available and subsequently sold into the second-hand market, losing value. This has not been the case post-COVID. Now, many consumers are unable to get their hands on even base model vehicles, having to wait several months to over a year. This has led to price-gauging and a boom in the secondary market, in many cases exceeding the RRP price. A contributing factor to the change in characteristics is supply chain issues. Vehicles are becoming more complex and require a greater number of chips. Not only vehicles but everything with technology in society currently, leading to a serious shortage in many other items .

Semiconductor shortage (McKinsey)

McKinsey sees automotive businesses ordering 10-20% more chips than they need but this has yet to have an impact. Long-term, we expect chip management to be better and a normalization of this craziness, but that is several years in the future yet.

So, what does this mean for Stellantis? Well, we see this as a "soft-landing" mechanism. What we mean by that is the rules of engagement have changed, vehicle demand has exceeded supply for at least 2 years, with many consumers either waiting or looking at other vehicles. Many will have purchased a Stellantis Group car because they couldn't get their preferred choice. Further, those who have waited may finally get the chance to purchase in 2023 and feel compelled to take up the option. Should we enter a recessionary environment, we envisage the change in demand Y/Y to be less drastic when compared to prior occurrences.

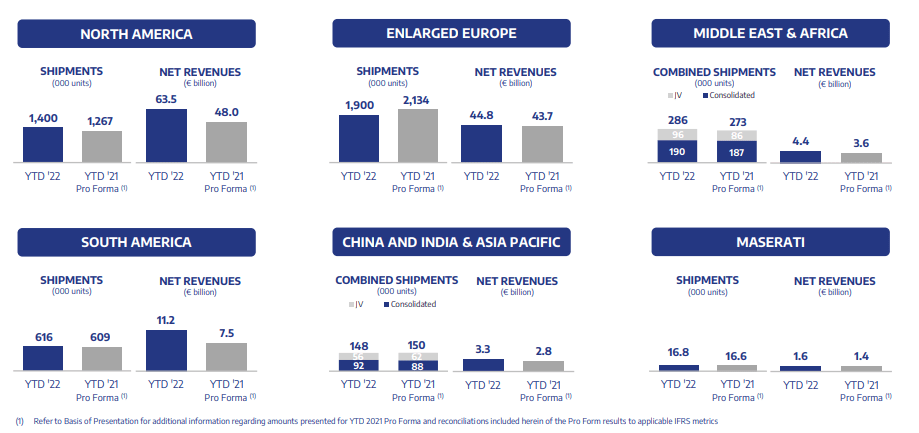

When we look at shipments, this seems to support our hypothesis. YTD shipments remain relatively flat when compared to a period with heightened demand.

{kind=link}

Q3 Investor reporting (Stellantis)

Geographical and brand considerations:

Brand:

One of Stellantis' weaknesses is that they do not own any market leading brands. If we consider some of the many categories for vehicles, Stellantis is always on the second tier.

- Hatchback - Ford ( F ) Fiesta and Volkswagen ( OTCPK:VWAGY ) Polo are superior to the Vauxhall Corsa and Fiat 500.

- Sedan / Saloon - Toyota ( TM ) Camry and Honda Civic are superior to the Peugeot 508 / Vauxhall Insignia.

- Luxury Sedan / Saloon - BMW ( OTCPK:BMWYY ) 3/4 Series are superior to the Alfa Romeo Giulia.

- SUV - Chevrolet ( GM ) Silverado is superior to the Ram pickup.

- Luxury - Ferrari ( RACE ) Roma is superior to the Maserati MC20.

We do not consider this a bad thing and did not go through the exercise as a criticism, just that we must understand Stellantis' relative position in the market when compared to others. Stellantis offer fantastic vehicles but do not blow the market away. They are a jack-of-all-trades but master of none.

Geography:

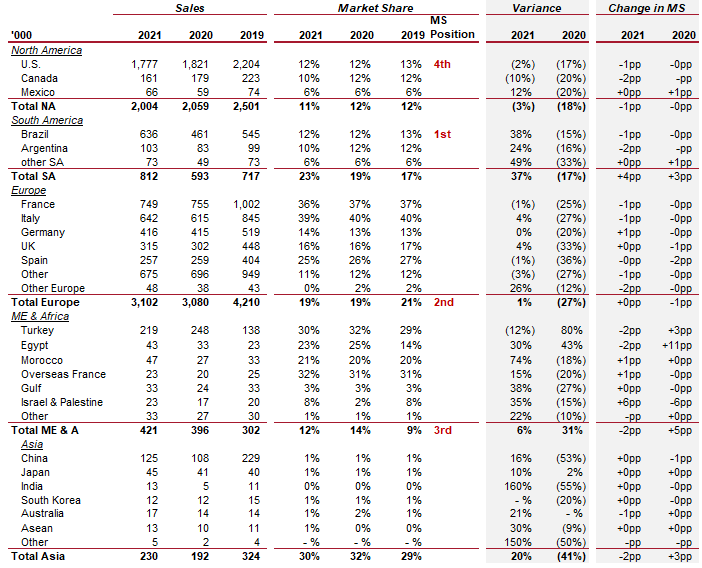

Stellantis earned c.82% of YTD'22 revenues from 2 key markets, North America and Europe. Growth geographically has come from Stellantis' smaller markets, with NA and Europe stagnating somewhat.

We should note that Stellantis was not materially impacted by pulling out of Russia, following its invasion of Ukraine.

{kind=link}

Net revenue by location (Q3 Investor pack)

Stellantis has significant market share in all 4 of its key markets. 2020 is an outlier year and so comparing sales would be a folly, we have yet to return to pre-COVID levels clearly. Looking at the regional split, we definitely see this stagnation and growth split. When we consider this on a market share basis, we see growth in SA, which is impressive, but the stagnation in NA and Europe look to be at least partially driven by a decline in market share.

Asia is clearly not a market that is a priority of Stellantis, and we think this is a shrewd decision. Competition in the region is rife, these firms have greater financial resources and in some cases are nationally protected.

{kind=link}

Stellantis sales breakdown (FY21 accounts)

We are not too concerned with the stagnation in Europe and NA, the markets are mature, and competition is high. We would like to continually see growth in SA, as this is an area to exploit, given their already impressive market share.

EV revolution:

Many nations have committed to the complete cessation of petrol / diesel powered vehicles on the road within the next few decades. Led by Tesla ( TSLA ), automotive businesses are racing to develop EVs that consumers want to buy. Consumer's requirements come in the form of a business which can easily replicate all the benefits of a combustion engine vehicle, with none of the downsides. The biggest requirement is ease of charging and battery life. From a business perspective, this of course means the development of an electric engine and battery, but also the connectivity to readily accessible battery stations.

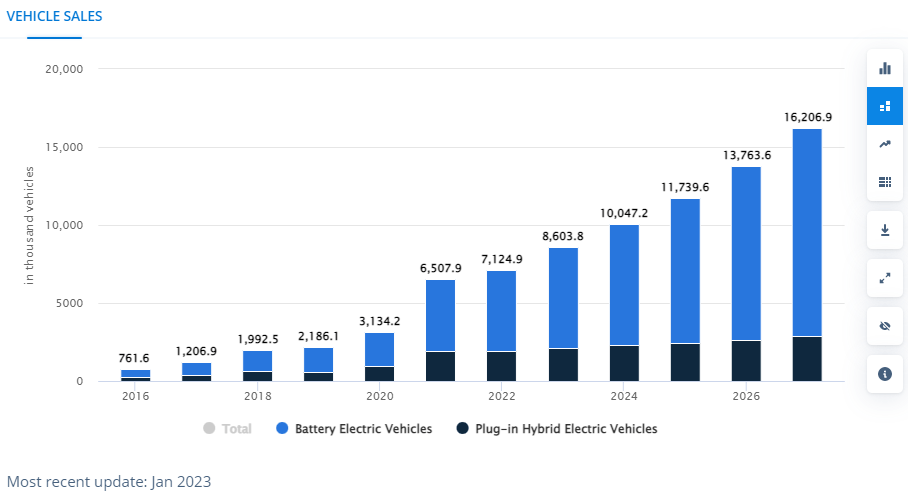

Stellantis have done a great job with this, having grown its BEV (Battery electric vehicle) sales 41% Y/Y, with impressive growth in LEVs (Low emission vehicle) too. The Fiat 500 BEV is the leading vehicle in Europe, with an estimated 20% market share , having overtaken Tesla . Further, Management intends to launch a further 4 EV by 2025, including the first ever full-electric Jeep.

Looking ahead, EV growth is forecast at a CAGR of 17%, which will only increase as we approach the end of the combustion engine era.

{kind=link}

EV sales (Statista)

We see this as a great opportunity for growth, as Stellantis can utilize its strategic approach to the Fiat 500 and roll this out across its other leading brands. This certainly has the ability to revitalize the brand's growth efforts in NA and Europe.

Financials:

Stellantis - Financials (Tikr Terminal)

Given the transaction date, there are not any real historical financials to compare. Looking at the previous iteration of this combination, we see:

- Fiat - Revenue grew at a CAGR of 9.5% but stagnated for 3 years. EBITDA followed suit, growing 11.1%. FCF-Y was -1.7% and ROE was 0.1%. Long story short, pretty disappointing.

- Peugeot - The business struggled post-COVID but performed far better in the latter half of the period.

( Source: Tikr Terminal ).

The current version looks far more impressive. The business has grown revenue well into the LTM period and earns a NI margin of 9%. Management attribute this to greater efficiency stemming from the business combination. Much of this transfers straight into FCF, allowing for sustainable funding of dividends and buybacks.

From a balance sheet perspective, the business boasts an impressive 28% ROE. This equity balance comprises 50BN in intangibles, leaving asset value of c.€15BN.

Inventory turnover has decreased due to greater inventory held by the business in the LTM. This reflects a gradual slowing down we have experienced since the post-COVID period. This has not impacted cash management in any material way, although does increase the risk of the ability to move stock should demand aggressively fall.

The Group holds a mammoth €47BN in cash, which is equivalent to €14.63 per share. For context, the current share price at the time of writing is c.€14. On a net cash basis, this is c.€5.96 per share. Investors can in effect purchase this business for less than €10-a-share. There is of course the risk that management wastes the money, but investors have the ability to mitigate this risk.

Given the cash identified, it is no surprise that we do not see any credit risk with the business. They have great coverage of their interest payments and are cash generative.

Outlook:

Analyst consensus forecast (Tikr Terminal)

Analysts forecast very steady revenue growth in the next 4 years, with margins expected to contract from 14% in the LTM period to 13% in FY26F. Further FCF-Y is expected to decline also, falling to 3%.

This is likely driven by 2 factors. Firstly, greater investment will be required in the development of more EVs and better technology. We have already seen above that R&D spending is increasing period-on-period. Secondly, the business will likely need to trade some margin in order to remain price competitive in the market.

With Stellantis' cash balance, we do not see this is a concern. Dividends / BB can be maintained while cash flow is reinvested.

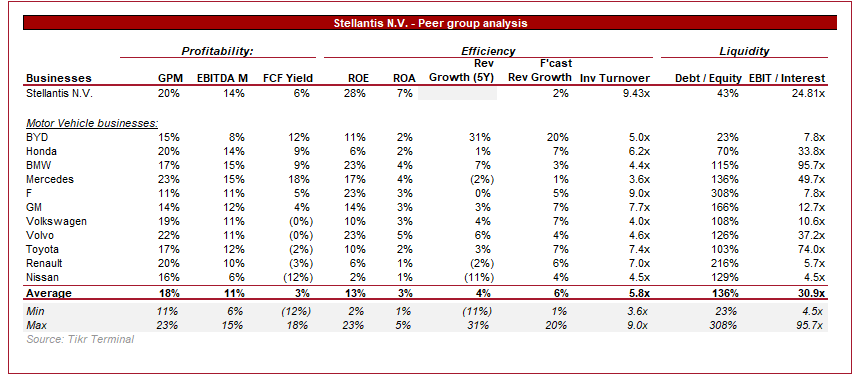

Peer group analysis:

{kind=link}

Peer group analysis (Tikr Terminal)

What initially stands out when comparing Stellantis to its peers is the superior profitability. The business is far more profitability on every metric. Even if we compare analyst forecast metrics of margin decline, Stellantis remains superior. A portion of this is inevitably due to the fact the business is far more conservatively financed.

Where the business lacks is in growth. Analysts forecast Stellantis to be one of the weakest going forward, which suggests their relatively strong performance in the EV space is not going to be enough. We concur with this assessment as the driving force of growth is the relative attractiveness of the cars. We've already established that Stellantis' fleet is not a market leader.

Overall, if one balances superior profitability with inferior growth, the net should be a business which trades around the average of its peers.

Valuation:

peer group valuation (Tikr Terminal)

Finally, we reach what piqued out interest in the business, a 1x EBITDA multiple. The business is trading at a level far below its competitors on every metric. If Stellantis traded in line with its peers, which realistically will not happen via price expansion, the upside would be 871%.

We are looking at this business and struggling to apply a fair value, markets seem to have completely mispriced this asset. Taking a conservative view and considering the average EV/EBITDA multiple in the last 1.5-years, we get an upside of 63%.

What we must also acknowledge is the current dividend rate, which, based on the current share price, suggests a yield of 7.4%. With the amount of cash the business has and the lack of risk over FCF positivity, this can be maintained.

Risks:

This investment does not come without risks, we identify the following as potential areas of concern:

- Inflation deteriorating margins if the business cannot pass on rising costs.

- Dilution of shares, which Fiat had done for many years in its history.

- Greater capex in order to push forward with the shift to EV.

- Current energy prices putting off combustion engine purchases.

Conclusion:

Stellantis is the perfect example of an above average business. It has a great fleet of brands and covers the entire spectrum of automobiles. The business combination looks to be a success, with the group boasting market leading margins.

The problems we see are with slowing demand from economic conditions and the stagnation of sales in NA and Europe. One of these factors is short-term and may be soft due to robust demand for vehicles which has not been satisfied. The second point is a systemic problem, but our hope is that their EV offerings revitalize their brands. At least for now, however, we can reflect both risks by demanding an attractive valuation.

Stellantis' upside potential we see is their growth in South America, the large cash balance, margin superiority and successful foray into EVs.

It is difficult to comment on valuation because it is the definition of an outlier. To say there is upside on the table goes without saying, but it is difficult to say how much. Our view is that if Tavares is given the time and ability to execute a relatively good transition into the EV era, this stock will increase significantly. If this doesn't occur, enjoy the dividends and FCF.

We rate this stock a strong buy.

For further details see:

Stellantis: Great Business With Significant Potential Upside