STLA - Stellantis: I Was About To Sell But Didn't

2023-11-15 23:48:05 ET

Summary

- Stellantis reached an agreement with workers after a 44-day strike, resulting in wage increases totaling 27% over four-and-a-half years.

- Headwinds being signaled by other industrial companies made me think the best days for STLA could be over.

- Digging into the recent report, the picture is quite a bit different.

Introduction

Well, finally the picture is becoming clear. Stellantis ( STLA ) has reached a tentative agreement with the UAW on a new labor contract. In the meantime, the company also reported earnings . In this way, we have lots of new data to look at to assess how the company is doing. In particular, it is to me even more clear that among the Detroit Big Three - General Motors ( GM ) and Ford ( F ) - being the other two, Stellantis enjoys a much financially healthier situation and remains the best pick among automakers.

The UAW issue

When the strike began, I shared my view on the impact it could have on Stellantis. My estimate was that Stellantis would see its cost structure increase by around $700 million because of the new wage raises. To this, we would have to add the impact the strike had on production.

Now things are more clear and we know that the strike has cost Stellantis less than $8 00 million in net income, $3.2 billion in revenue and 50,000 vehicles produced.

The agreement centers around a 27.4% compounded wage increase over the next four-and-a-half years, up from the $31.77 per hour top wage today.

It will be structured with an immediate 11% increase, followed by 3% hikes for the next three years (2024 to 2026). Workers will then get a 5% raise in 2027. In addition, there should also be a $5,000 ratification bonus.

Another victory for workers was the reinstatement of cost-of-living adjustments (COLA), which had been suspended during the crisis of 2009. According to the UAW, this should make the top wage go up by 33% to over $42 per hour. Starting wages should also increase by 67% compounded

The starting wage would increase by 67% compounded with estimated COLA of over $30 per hour.

Stellantis new CFO Natalie Knight didn't provide many details during the last earnings call because the deal still needs to be ratified. However, she let investors understand that the company's additional cost per vehicle should be similar to what Ford disclosed, which is an extra $850-$900.

However, she also pointed out that Stellantis has reached this deal with a better positioning compared to its peers:

We start with UAW.[...] we go into that position, I think, in a very healthy space versus the competition. On the one hand, the US market, it's very important to us, but it's a smaller piece of our overall business than what you see from our US competitors, and it's a place where we start with a very high and healthy profitability level. When we look at kind of where we've ended the negotiations, I talked about the number of shipments and about the €3 billion in terms of revenue hit that we've had this year. When we look at that from an AOI perspective or in terms of margin, that number is less than €750 million. And we also believe it's the lowest of the big three in the market. So that's just kind of getting to where we are today in terms of impact.

These words confirm something we have seen over and over: Stellantis has better operating efficiency and thanks to its synergies and its geographical footprint it sees many of its production plants in lower-wage countries while its main markets are in North America and Europe, where margins are usually high.

However, what I think is more important is Stellantis' next move, as soon as the tentative agreement was announced. Simply put, Stellantis is working on reducing to trim workers in the U.S. More in detail, Stellantis offered buyouts to half of its 12,700 nonunion white-collar workers with five or more years of employment, who have until December 8th to accept. Although this will lead to one-off costs, it is a move that clearly aims at offsetting at least part of the new labor costs the company will have to meet as a consequence of the deal with the UAW.

Assuming these white-collar workers earn on average around $100,000, we are talking about a potential $635 million or so in savings every year. I am not at all surprised by this amount: it is very close to what the company will have to pay to its unionized workers. So, there we have it. Stellantis might not need to increase car prices as much as Ford and GM because it is targeting to finance the new expense mainly by a reduction and a rationalization of its North American workforce.

Considering Stellantis' revenues should be around $210 billion this year and its cost of revenues should be around $165 billion, we are talking about sums that, although meaningful to the workers, are small in the overall picture of this company.

Furthermore, even non-unionized automakers may feel some pressure after the UAW deal with the Detroit Three. Every automaker will probably need to increase wages to the new competitive levels achieved by this deal. Therefore, over the long run, the cost of car manufacturing in the U.S. may even out for most of the industry and this is what plays in favor of Stellantis, which is one of the most profitable automakers thanks to its synergies and its management.

Q3 Earnings

My concerns

I'll admit it. I was quite nervous before this earnings report. In fact, recent reports from automakers, Mercedes ( OTCPK:MBGAF ) amongst all, have made me think quite a bit about my exposure to the industry as a whole.

Some SA readers may know from my past articles I am not fond of the industry because it is highly competitive with low margins. Yet, I am invested in Stellantis because, no matter how I scrutinize the company, I find it deeply undervalued without finding any real reason for this.

However, as interest rates are making financing harder, automakers will be hit because most of their customers need to finance the acquisition of a car. In a similar industry - truck manufacturing - orders have been declining rapidly in the past quarters and this made me nervous about Stellantis.

In addition, I myself was thinking a few months ago about changing my car. But once I saw how much I would have to pay in interest, I decided to simply wait for a better time. This made me think automakers won't go through easy times.

After Mercedes capitulated and tumbled by almost 10% on the day of its earnings, I started thinking about trimming my exposure to industrials in general. But the more I thought about selling Stellantis, the more I couldn't find any true reason linked to the way the company runs its business. In other words, Stellantis seems to me a perfectly healthy company.

So, I understood I was not sticking to fundamentals, but I was being caught in fears linked to macroeconomic conditions. Of course, these are important. If people have a harder time being financed, they will postpone their purchase, just like I did.

In any case, I didn't sell a single share of Stellantis and I decided to wait until earnings to have a better picture of what is going on.

Needless to say, Stellantis caught me off guard once again.

Q3 earnings highlights

Let's look at a few highlights:

- net revenues of €45.1 billion were up 7% vs. Q3 2022, mainly reflecting improved volume and consistent pricing, partially offset by FX

- Shipments were up 11% to 1.427 million.

- Inventories are back to normal levels

- BEV sales are up 37% YoY

- Adjusted Operating Income, AOI margin and industrial FCF make Stellantis emerge as the industry leader among its comparable peers.

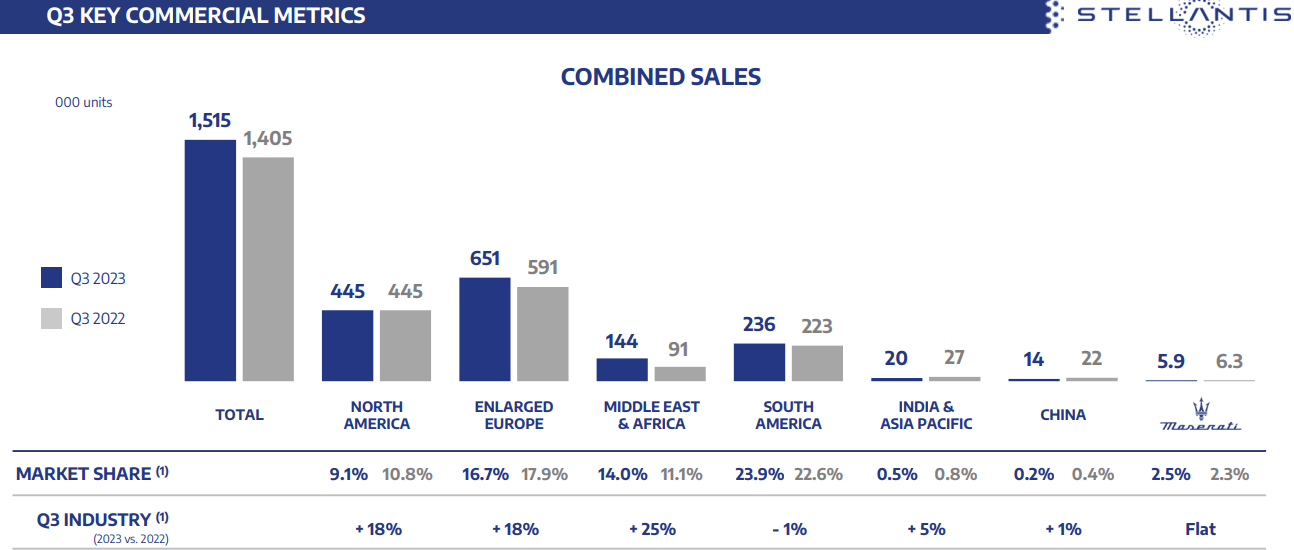

We can see below the key commercial metrics for the quarter. What stands out is the strong performance of Middle East & Africa, where combined sales went up 58% YoY, passing the 100,000 unit mark. Net revenues in the region saw a 128% increase to reach €3 billion helped by positive net pricing and also benefiting from hyperinflation in Turkey.

{kind=link}

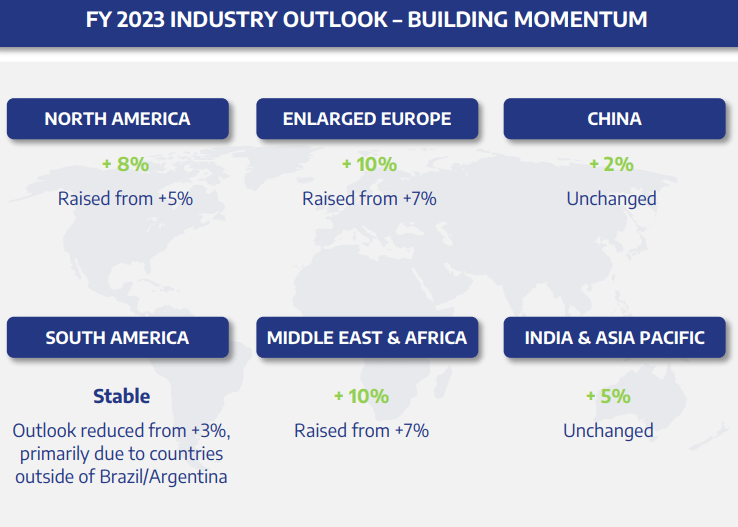

So far so good: automakers are still working because of their backlog. Therefore, this year most of these companies reported very good sales. But what we need to know is not the past, but the future. In this regard, Stellantis didn't lower its guidance, but actually raised it, especially in key markets such as North America and Europe.

{kind=link}

During the Q3 earnings call, the company also reported two important news.

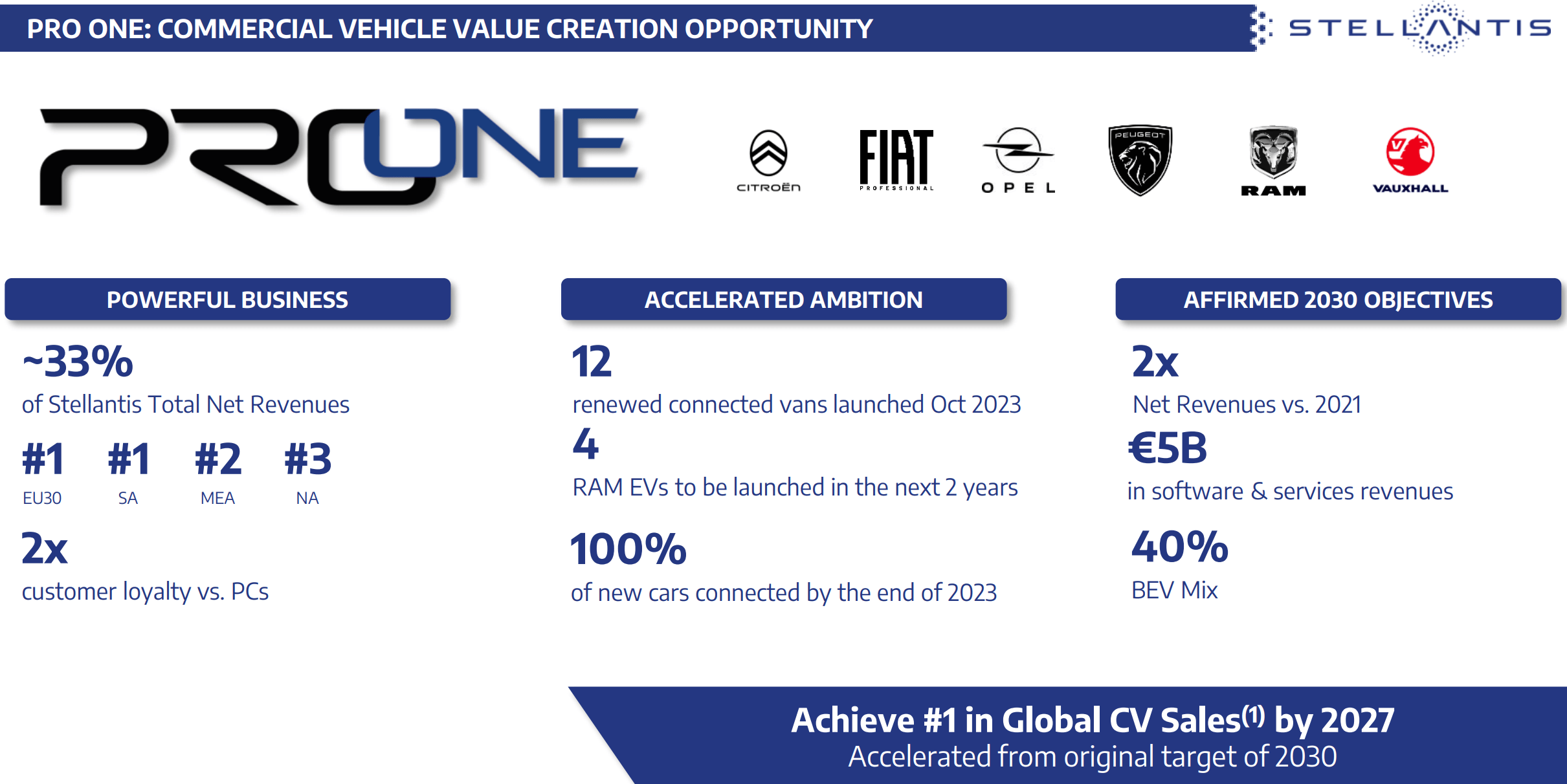

First of all, Stellantis is betting big on commercial vehicles. This is a segment I like a lot and Mercedes is there to show everybody how profitable it is. Moreover, it is less competitive, with fewer players around. Currently, commercial vehicles represent around a third of Stellantis' sales and its customers are very loyal.

The slide below, taken from the last earnings presentation, shows what Stellantis' plans are. What is interesting is that Stellantis currently is the top player in Europe and South America and it plans on being the number one in global commercial vehicle sales by 2027, 3 years in advance of its previous goal.

Furthermore, by the end of this year, every commercial vehicle Stellantis will have sold will be connected. Why is important? Because this is needed to start generating recurring revenue from software and services. In other words, commercial vehicles can become what iPhones are for Apple: an installed base to engage with in order to offer new services and obtain recurring inflows of cash. Stellantis aims at making around €5 billion in software and services revenues by 2030. This is not much considering the company wants to reach €300 billion in sales by then. However, these €5 billion are so valuable because they have high margins. The impact on the bottom line will thus be more meaningful.

{kind=link}

I must admit this focus on commercial vehicles was something lacking until now. And, for sure, it made me reconsider once again my bull-case on the company, adding yet another reason to stay long.

Another important news comes from electric cars. Stellantis regained the number 2 position in BEV sales in Europe.

But what matters most is what lies ahead of us. For automakers, this means two things: inventories and order books.

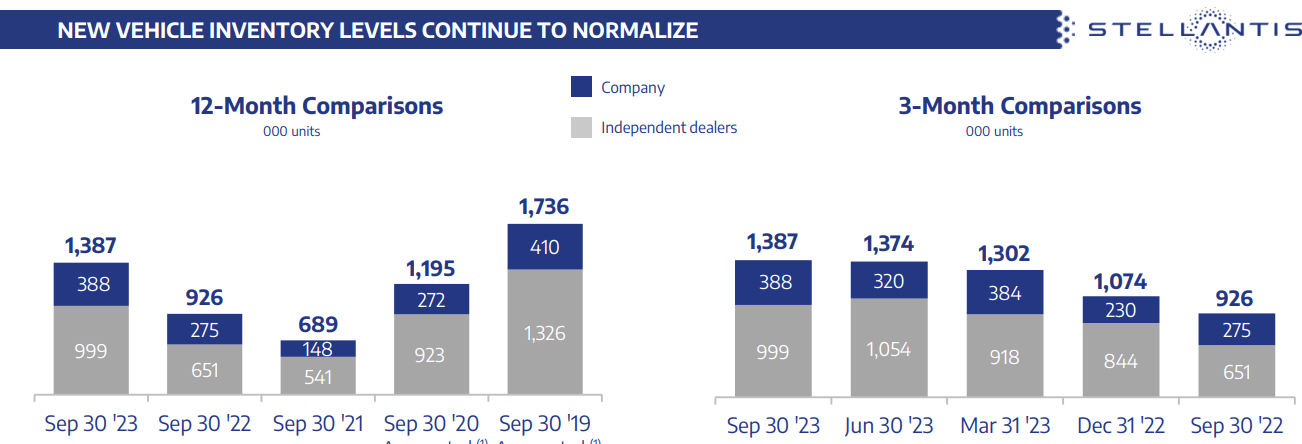

Here, I was positively surprised by the fact Stellantis still seems to be enjoying momentum. First of all, global inventories remained stable and didn't increase.

{kind=link}

The company has repeatedly said it wants to keep inventories around 1.3/1.4 million units and it is at this level now. But what is even more important, inventories didn't increase QoQ, meaning the company has managed well its order book which, in turn, is still quite healthy. Miss Knight also touched on this topic during the call, pointing out that Stellantis' order book "has moved from four months at the end of the second quarter to around three months at the end of this period". So, Stellantis is seeing an order decline compared to shipments, but 3 months is usually the visibility automakers have in normalized times.

In any case, what matters most is that there are no signs of deteriorating financials. Actually, the positive impact of synergies is growing and this year it should contribute another €8 billion after the €5 we saw last year. The company will once again deliver double-digit operating margins and will easily reach around €11 billion in industrial free cash flow, which is remarkable.

Considering Stellantis carries on its balance sheet €52 billion in cash (around $57 billion) and its market cap is €59.6 ($62 billion). Having a total debt of €29.5 billion ($32.2 billion), the company has become known for being the automaker with a negative net debt position. This has led many analysts to ask Stellantis' management what the company plans on doing with this huge pile of cash. Miss Knight was asked this too and said she wants to shift from a "safety-first balance sheet to an efficiency-driven balance sheet". Therefore, she hinted the company could actually think in 2024 to a new shareholder remuneration structure. I wouldn't be surprised to see new buybacks. In fact, Stellantis is currently running a €1.5 billion program, of which €0.5 billion in shares were deployed during Q3 2023. Year to date, Stellantis has repurchased €1.2 billion in shares. So, we know that in Q4 there will be a €300 million buyback to end the program. After that, the company will have to decide what it wants to do.

Valuation and conclusion

After this report, I found myself even more interested in the company. It seems like it can weather tough times better than its competitors both because of its product and geographic mix and because it is managed better, with higher operating efficiencies and synergies. Moreover, its balance sheet is a fortress. Not by chance, Stellantis is up 40% this year while its Detroit peers aren't, with Ford down 5.8% and GM down almost 17%. And yet, it still trades at a ridiculously cheap valuation . A fwd PE of 3, a fwd EV/EBIT of 1.5 and a fwd P/FCF of 2.3 are all ratios deeply discounted compared to the industry average. According to Seeking Alpha, we see a discount ranging from 75% to 89%. Ford, for example, trades at a fwd PE of 8, while GM trades at a 4. Does it make sense, considering Stellantis is much more in financial shape than the other two? I don't think so.

Now, I am not advocating Stellantis should trade at a 12 PE or so. We need to discount the industry it belongs to. However, I find it not particularly compelling to expect a PE around a 5. With the TTM EPS currently at $6.86, we are talking about a price target of $34, which is a 67.7% upside from where the stock is currently trading.

For further details see:

Stellantis: I Was About To Sell, But Didn't