STLA - Stellantis Stock Can Double From Here

2023-12-12 02:53:35 ET

Summary

- Stellantis is a major global automaker formed from the merger of Fiat Chrysler Automobiles and PSA Group.

- The company is facing challenges in catching up with the electrification trend and competing with leading EV makers.

- Stellantis is implementing an EV strategy through partnerships and acquisitions, including a joint venture with Chinese EV startup Leapmotor.

Formed in 2021 from the merger of Fiat Chrysler Automobiles and PSA Group, Stellantis ( STLA ) has grown into one of the world's largest automakers. The company owns renowned brands like Jeep, Ram, Peugeot, and Alfa Romeo and has a strong presence in the North American and European markets.

However, Stellantis finds itself at an inflection point. The auto industry is undergoing a profound transition towards electrification. As a latecomer to EVs, Stellantis must play catch up with huge investments planned over the next decade. Simultaneously, the company must navigate near-term economic turbulence, pricing pressure, changing consumer preferences, and onslaughts from new competitors.

{kind=link}

Financial Snapshot

Stellantis reported revenue of €193 billion over the trailing twelve months. Thanks to strong vehicle pricing and diverse product mix, the company has achieved profitability with a 20% gross margin; €38.6 billion in gross profit, and €19.8 billion of net income.

The balance sheet is solid, with €29 billion of net cash. A chunk of that came from the merger between the two firms. Account for debt and investments and the enterprise value is around €35.8 billion. So although Stellantis is behind in certain aspects relating to electrification, the company is still in a good position to course correct. Importantly, the company has continued to produce consistent free cash flow. Stellantis reports bi-annually but free cash flow has remained above two billion since October 2021 and currently stands at €14 billion for the last 12 months.

{kind=link}

Sure, Stellantis is embarking on a prolonged period of capital expenditure. Even so, consistent free cash flow is not something that can be said about most pure-play EV makers.

On traditional valuation metrics, shares look tantalizingly cheap at just 3.3x P/E and 2.5x EV/FCF. The stock also pays an attractive 6.5% dividend yield.

Lagging in Electrification

The singular risk hanging over legacy automakers like Stellantis is their unpreparedness for the global transition to EVs. Despite the company's strong free cash flows today, Stellantis trails leading EV makers in technology, sales volume, and future competitiveness. Indeed, the company's early outlook towards electric vehicles was one of caution.

Last year Stellantis sold only 288,000 electric vehicles globally putting it well outside the top EV makers. The rapid influx of smart EVs from China threatens the European company’s domestic stronghold. Chinese electric vehicle factories literally cannot deliver the vehicles quick enough such is the current demand.

Despite Stellantis' initial reluctance the company is now fully committed to electric and plans to have 47 EV models on the road by the end of 2024. Of course, such a target is easier said that done. Stellantis must invest tens of billions over the next decade to electrify its vehicle portfolio and manufacturing footprint. In company conference calls and presentations that sum has been clearly earmarked at €50 billion . Successfully executing this complex evolution is the key risk and question surrounding Stellantis stock.

The EV Strategy

A large part of Stellantis' new EV strategy revolves around partnerships. Agreements have been made with a number of companies including Chinese battery firm CATL. But Stellantis also announced a €1.6 billion investment to acquire a 20% stake in Leapmotor , an emerging Chinese EV startup.

Through a new joint venture called Leapmotor International, Stellantis gains exclusive rights to sell Leapmotor vehicles outside of China starting in late 2024. Leapmotor brings EV technology and production capacity from its manufacturing facility in China and plans to sell over 1 million EVs annually in China by 2030.

For Stellantis, this partnership provides vital access to affordable EVs to compete in the European market as emission regulations tighten. It also taps into the booming potential for Chinese EV exports. Stellantis is targeting over 500,000 Leapmotor vehicles exported annually by 2030. These EVs are expected to hit cost-competitive price points below €20,000.

{kind=link}

Intensifying Competition

The auto industry was already brutally competitive before factoring in EVs. With electrification, the battlefield becomes even more challenging. Tesla leads in batteries, efficiency, charging infrastructure, and autonomous driving. Meanwhile, Chinese rivals like BYD and NIO can produce capable EVs at far lower costs thanks to China's vertically integrated supply chains and dominance in batteries. But lower prices are affecting companies at all levels. Chinese car maker NIO repeatedly called out the impact of price wars in its latest earnings call. Mercedes and BMW have cut prices by as much as 30%

In this environment, vehicle pricing will continue to come under sustained pressure. Margins will continue to erode and there will be numerous bankruptcies as new leaders emerge.

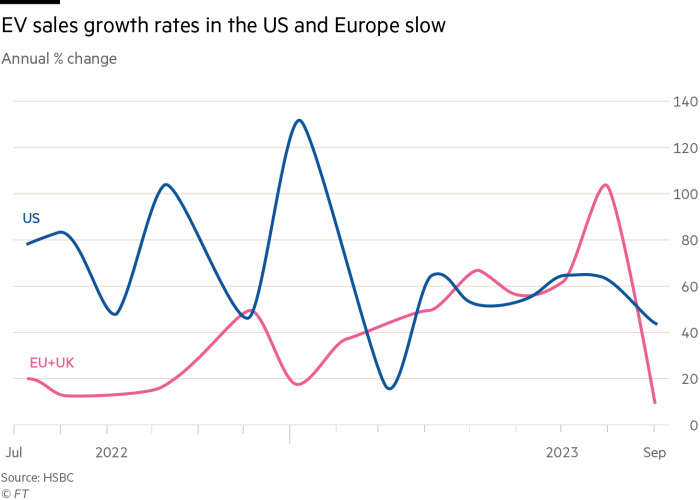

Decelerating EV Demand

Complicating this already complex picture is a surprising slowdown in demand for EVs themselves. There's no doubt EVs represent the future, but consumers continue to be concerned about battery range. As a result, near-term demand has softened considerably across North America and Europe. And it's not just range anxiety that is putting customers off. Consumers face high sticker prices, limited model availability, lack of public charging, and questions around safety and reliability.

{kind=link}

Gasoline vehicle bans have also been pushed back in some markets. Most notably, in March 2022, Germany reached an agreement with the European Commission to allow the continued sale of vehicles that run on "e-fuels" or synthetic fuels after the proposed 2035 ban on internal combustion engine vehicles.

E-fuels are synthesized using renewable energy sources and can power traditional combustion engines in a more climate-friendly way. Proponents argue e-fuels allow legacy vehicles to become carbon neutral. However, critics argue that battery-electric vehicles are much more energy efficient overall. The production process for synthetic e-fuels also currently remains expensive and energy intensive.

However, this speed-bump on the road to full electrification plays into Stellantis' favour. It buys more time for Stellantis to manage the transition since most of its vehicles will be fine to run on eco-fuels. Ultimately, that's going to protect at least some of Stellantis' cash flows over the next few years and suggests the current valuation is pricing in too much bad news.

Back Of Envelope Valuation

At the current share price, Stellantis trades at extremely low multiples - just 3.3x P/E and 2.5x EV/FCF. No doubt the company faces risks, but negative sentiment appears overblown. Carlos Tavares is a capable CEO who turned around the Peugeot Group. Tavares believes the company can sustain €20 billion in free cash flow by 2030 which seems like a reasonable and obtainable target.

Importantly, if Stellantis can hit that target the stock price can more than double. How? Currently, Stellantis trades at an enterprise value of €36 billion which is just 2.5 times trailing twelve month free cash flow. If the company gets to €20 billion of free cash flow by 2030 we can assume that fears over the company's demise will have largely been expelled. Therefore the company would no doubt trade at a substantially higher multiple. We can also assume the company will have generated meaningful amounts of cash during that period.

Cash generation of just €40 billion before capex between now and 2030 and Stellantis may arrive in 2030 with net cash of around €19 billion with annual FCF generation of €20 billion. With a 4.5x multiple the company would then be worth €90 billion. That's more than double the current enterprise value while taking into account €50 billion of capex over the next 7 years. Crucially, that's without factoring in dividends which would push the rate of return even higher.

Any valuation of Stellantis at this point is difficult because there are so many moving parts and different scenarios that could play out. But fundamentally, the stock is cheap and a modest improvement in prospects is likely to see a strong return.

Valuation Risks

Clearly, with a company like Stellantis there are numerous risks to the investment case. If the company can't sustain cash generation of ~€40 billion between now and 2030, the investment case starts to fall apart. And that means the company will have trouble funding its transition to electric vehicles. Such a situation could transpire for any number of reasons. Electric vehicle demand could take off over the next couple of years which would put Stellantis in a difficult position and impact cash from operations.

Competition is another key factor with so many automakers attempting to take market share. Although Stellantis owns a number of well-known brands, those brands (for the most part) are not considered high quality. Brands like Peugeot, Citroen, Alfa Romeo and even Maserati do not carry the same weight as other brands. So that will be another key challenge that Stellantis management will need to navigate.

Moreover, the execution risks here are enormous. The company is planning to get 47 EVs on the road by the end of next year. Not only does it need to keep introducing new models, it needs to invest smartly without taking undue risk or destroying profit margins. Certainly, the difficulty is an order of magnitude higher than a company like Tesla which has already mastered the profitable production of its vehicles. Making smart investment decisions that drive the company forward while the market is flooded with cheap Chinese vehicles won't be easy and none of this is easy to predict.

All said, if Stellantis can achieve that execution then the rewards on offer will be plenty. In that sense, a lot comes down to the savvy leadership of Tavares.

Key Takeaways

Stellantis presents an intriguing contrarian opportunity. The company generates consistent cash and operates brands with significant legacy value. There are risks and a huge amount of investment is needed. But long-term investors will be rewarded if Carlos Tavares successfully navigates the treacherous road ahead. Stellantis shares are pricing in the worst but there are many scenarios in which an investment will pay dividends (in more ways than one). As a result, we rate the stock a solid buy

For further details see:

Stellantis Stock Can Double From Here