STLA - Stellantis: Why I Am Close To Go All-In On This Deep Value Pitch

2023-10-31 08:13:22 ET

Summary

- Stellantis reports strong Q3 performance with 11% YoY increase in car shipments and 7% YoY growth in revenue.

- The company is expected to achieve double-digit operating income margins and over $20 billion in operating profits for 2023.

- Stellantis is poised for more than $20 billion of operating profits for the full year 2023 - against an enterprise value of about $31 billion.

- With robust financial results and a substantial net cash position, Stellantis is well-positioned for capital distributions to investors.

- Stellantis is my top pick, a deep-value idea.

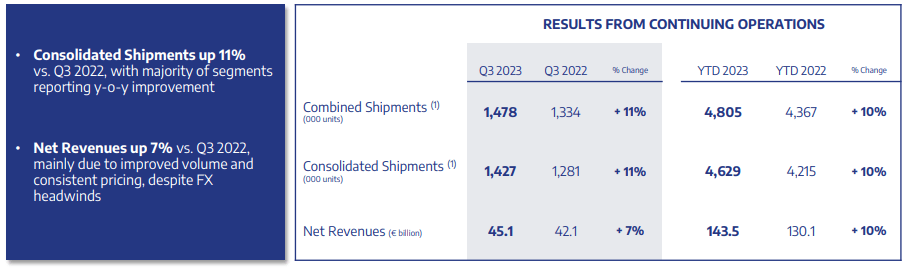

Stellantis (STLA) stock continues to present itself as a deep value opportunity to investors on the backdrop of strong financial performance. Defying macroeconomic headwinds, as well as UAW strikes, in the third quarter of 2023, the automotive conglomerate reported the shipment of 1.4 million car units, an 11% YoY increase compared to Q3 2022, and notably above analyst consensus estimates. Revenue was up 7% YoY.

Expecting that the company will continue to claim double-digit operating income margins, Stellantis is poised for more than $20 billion of operating profits for the full year 2023 -- against an enterprise value of about $31 billion. In case you have been wondering what deep value looks like; this is it.

Based on solid management execution in a challenging macro environment, strong financials, and a very cheap valuation, I reiterate my "Strong Buy" thesis for Stellantis stock. In fact, STLA shares remain my top pick.

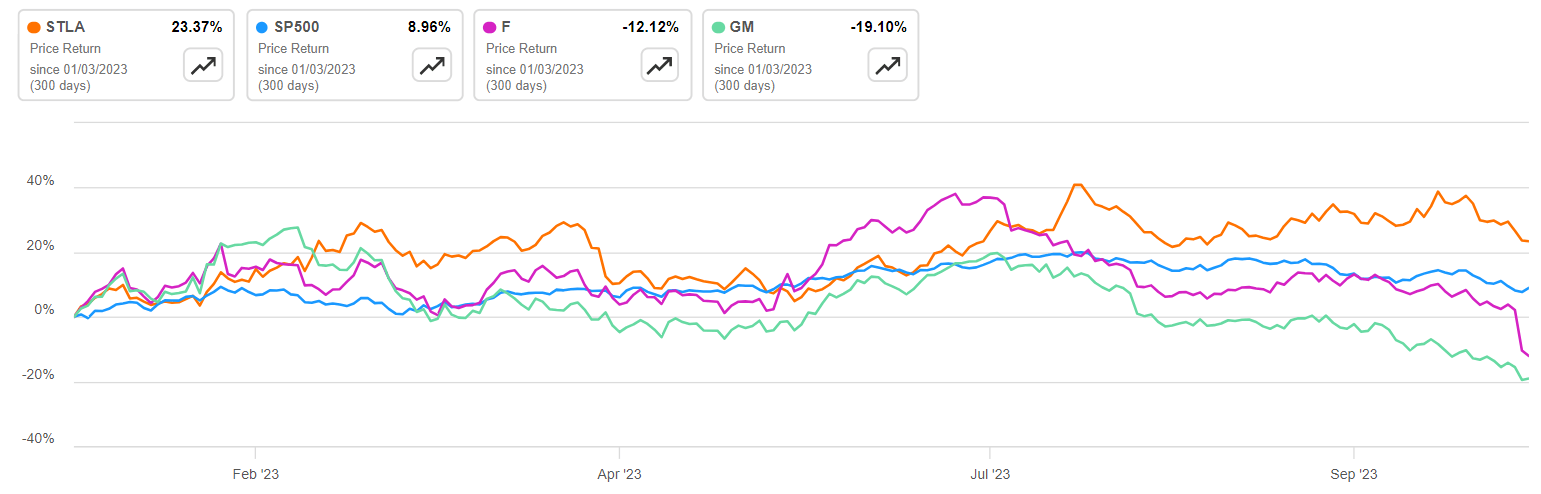

For reference, Stellantis stock has strongly outperformed YTD, both vs. U.S. competitors Ford (F) and General Motors (GM), as well as the broader stock market: STLA shares are up about 23%, compared to a gain of approximately 8% for the S&P 500 (SP500) and a loss of 12% and 19% for Ford and General Motors, respectively.

{kind=link}

Stellantis Topps Q3 '23 Expectations

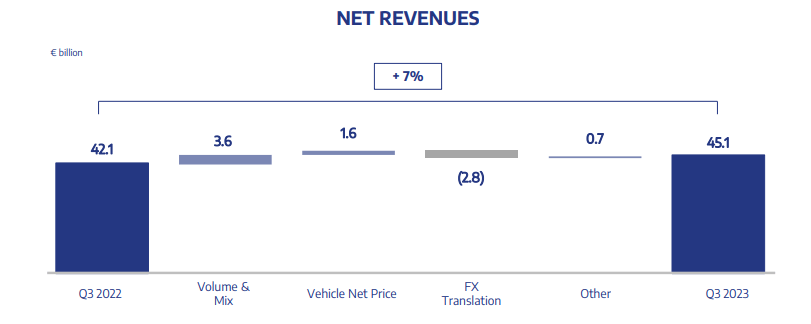

Stellantis reported a strong set of Q3 2023 results , beating analyst consensus estimates on shipment and revenue estimates. During the period spanning from June to the end of September, the European auto conglomerate recorded group revenues of EUR 45.1 billion, marking a 7% YoY increase from the EUR 42.1 billion achieved during the same period in the previous year. Notably, the result surpassed analysts' expectations by approximately EUR 1.6 billion, according to data collected by Refinitiv. As a side note on Stellantis performance, I point out that Stellantis YoY top-line growth for Q3 was stronger than for Tesla. The U.S. EV leader only achieved a 5% YoY expansion in automotive revenues, while the European cost leader Stellantis achieved a 7% YoY growth.

Stellantis' strong topline performance can be attributed primarily to higher shipments, with stable/ slightly supportive pricing.

{kind=link}

From a geographical perspective, Stellantis commented on broad and strong improvements in Europe, the Middle East & Africa, North America, as well as South America. Only China and APAC were a headwind to topline, as consolidated shipments for the region were down 33% YoY, highly likely as a consequence of regional competition with Chinese automakers. However, the Chinese market is by far the smallest end market for Stellantis, with only 48,000 shipments in Q3 2022. So, the impact of lower volume in Q3 2023 is almost forgettable.

{kind=link}

Commenting on the EV transition, Stellantis secured the #2 position in EUR 30 Battery Electric Vehicle (BEV) sales, with a 33% YoY increase in shipments. Notably, the company's "Third Engine" net revenues surged by 25% YoY.

With regard to profitability, Stellantis did not disclose precise numbers. But the company reiterated its guidance of a double-digit adjusted operating margin, which would suggest EUR 20-22 billion of annualized operating income. Additionally, it's worth noting that Stellantis' optimistic outlook is reinforced by an order backlog, equivalent to about three months of full-capacity production, according to company estimates.

Projecting The Earnings Headwinds On Preliminary Estimates

A major event for Stellantis in Q3 has been the UAW strikes and negotiations, something that has been broadcast quite loudly by the press. According to Stellantis Q3 reporting, work stoppages negatively impacted net revenues by approximately EUR 3 billion compared to planned production through October. According to Stellantis' Chief Financial Officer, Natalie Knight, the approximately six weeks of strikes related to wage issues have negatively affected the company's profitability by nearly €750 million.

With that said, it is important to note that Stellantis impact on profitability is relatively smaller compared to what American competitors Ford and General Motors have suffered. This is partly because of Stellantis' laser-focused efforts to reduce costs, but also because of the company's more diversified regional exposure compared to Detroit peers. Anyways, Stellantis has now reached a tentative agreement with the UAW, which, pending approval by Stellantis union members, offers employees a 25% pay raise over a four-and-a-half-year period, as well as the return of cost-of-living adjustments.

For investors who are concerned about the negative impact of the wage hikes on Stellantis structural profitability, I would like to calculations made by equity analysts at Deutsche Bank, who are estimating that the company will likely suffer a $6.4 billion earnings loss over the contract period ( Deutsche Bank: Automotive industry equity research note, dated 26 October ).

{kind=link}

When looking at it on an annualized basis, according to Deutsche Bank's projections, Stellantis should see EUR 1.3 billion of incremental expenses. This should roughly represent less than 7% of the carmaker's adjusted operating income and may be partially offset by price increases during the 4.5-year period of the new wage contract, as well as synergies unlocked through the execution of the Fiat/ Peugeot merger.

Deep Value Thesis - Reiterated

Looking ahead, Stellantis management has expressed strong confidence in their belief that the company will maintain adjusted operating income margins exceeding 10% with positive topline CAGR through 2025. This robust financial backdrop should easily support about EUR 20-22 of annual operating income over the forecast period. On a post-tax basis, this would suggest about EUR 15-16 billion of distributable earnings, on an estimated 25% effective tax rate.

Now, it is important to note that Stellantis is currently valued at a EUR 55 billion market capitalization. The carmaker's annual post-tax earnings yield is thus implied at almost 30%. Needless to say, 30% is very attractive. However, the number still does not fully reflect Stellantis' value thesis. Investors should consider that Stellantis is quite unique in the world of automotive because the company is not indebted. In fact, as of Q3 2023, Stellantis' net cash position on its balance sheet has likely topped EUR 25 billion. Accordingly, taking the unlevered perspective (enterprise value), Stellantis implied annualized earnings yield is closer to 50%!

In my view, Stellantis' substantial net cash reserve positions the company for accelerated capital distributions to investors. On the backdrop of a EUR 25 billion net cash position, paired with EUR 20-22 billion of annual operating incomes, Stellantis management should soon shift to returning capital to shareholders at a more aggressive pace. Personally, I now anticipate that for FY 2024, Stellantis may soon announce a significant share buyback program or a special dividend.

Investor Takeaway

Stellantis continues to offer a compelling deep value opportunity for investors, backed by impressive financial performance. Despite prevailing macroeconomic challenges and UAW strikes, the company's performance in Q3 2023 surpassed expectations. They shipped 1.4 million car units, marking an 11% YoY increase compared to Q3 2022, and reported a 7% YoY growth in revenue. Anticipating sustained double-digit operating income margins, Stellantis is poised for over $20 billion in operating profits for the full year 2023 against an enterprise value of around $31 billion.

With robust financial results and a substantial net cash position, Stellantis is well-positioned for capital distributions to investors. In my opinion, a significant share buyback program or special dividend announcement could be on the horizon for FY 2024. Reiterate the "Strong Buy" recommendation.

For further details see:

Stellantis: Why I Am Close To Go All-In On This Deep Value Pitch