SRCL - Stericycle: Metrics Show A Crumbling Moat And No Turnaround

Summary

- In the last few years, Stericycle reported low ROIC, declining margins as well as declining revenue.

- And while third quarter results show signs for improvement, there are not many hints for a turnaround.

- The company still has a terrible balance sheet with high levels of goodwill and long-term debt.

- Without an economic moat around the business, Stericycle seems to be fairly valued at best.

In the past, I have written several articles about Stericycle Inc. ( SRCL ). In my last article published in October 2019 I explained why I sold Stericycle and since then I did not really follow the company closely anymore and did not publish any article. And when looking back more than three years later, it was certainly a good decision to sell Stericycle as the stock is now trading even 5% lower while the S&P 500 (SP500) could gain about 30% (despite the decline in 2022).

Let's take another look at Stericycle. However, I still don't think Stericycle is a business worth investing in. We will not only look at the several challenges the company is facing but I will ask (myself) once again if Stericycle has a wide economic moat and could be a good investment.

No Stability, No Consistency

When looking at Stericycle from a quantitative point of view, I see several issues why the business is probably not worth investing in (at least not for a long-term investor). I usually demand stability and consistency from a high-quality, wide economic moat business that we can invest in for the long term (at least 5 to 10 years). But when looking at Stericycle I see several issues we have to address here.

Valuation Multiples

When I start my research process, one of the steps is usually to look at several different performance metrics over the last ten years (or longer if I can get the data easily) to get a first feeling for a company. And I usually look at the two major simple valuation metrics - the price-earnings ratio and price-free-cash-flow ratio - and the numbers in case of Stericycle are not good.

Both simple valuation metrics are rather useless for Stericycle right now. And it happens from time to time - even for great businesses - that simple valuation metrics don't make much sense (as the company must report rather low earnings or even a loss in one or a few quarters), but the picture Stericycle is presenting is quite messy. Not only is the stock trading for more than 700 times earnings and free cash flow right now, but data is also missing for the P/FCF ratio in 2019 and for the P/E ratio in several years. The company had to report negative numbers in several quarters and therefore useful numbers could not be calculated.

Declining Margins, Low ROIC

We can also look at the company's gross margin and operating margin and will see some consistency - but not the kind of consistency I like to see. Especially in the years between 2013 and about 2020 it seems like gross and operating margin declined pretty consistent and that is problematic.

To be fair, gross margin improved a little bit in the last two or three years and operating margin is also slightly higher again as it was at the beginning of 2018 and one quarter ago. But we can't really make the case for a turnaround when just looking at those two margins. Especially operating margin being about 3.5% in the last twelve months is certainly not great (and the number displayed here might be wrong and operating margin seems to be around 6.5%). But not matter what the actual number is, operating margin is extremely low right now.

And when looking at return on invested capital, the number is also not great. In the last few years, ROIC was clearly below the metrics Stericycle could report in previous years (and we must point out that the numbers before 2015 were also just solid - a 10% ROIC is fine an indicating a good business, but certainly not excellent).

Declining Revenue, Widely Fluctuating EPS

When looking at the company's revenue in the last few years, we see consistency once again, but the wrong kind of consistency. In the last few years, revenue has been constantly declining and only in the last few quarters it seems like Stericycle could break that trend and revenue increased again slightly. And the picture for earnings per share is really messy in the last few years.

When looking at the years from the 1990s leading up to about 2016, we see steady improving revenue as well as earnings per share and when ignoring the last 7 years, Stericycle presented itself as great business.

Hope For A Turnaround?

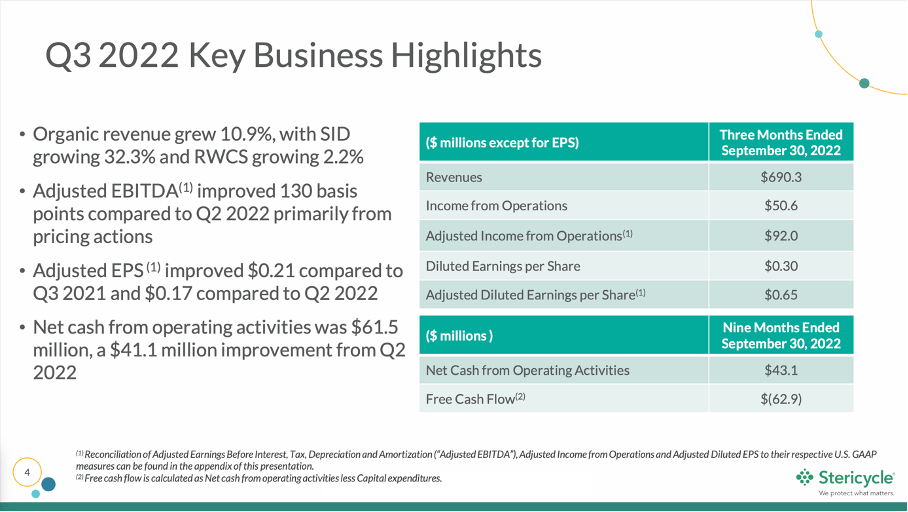

When looking at the quarterly results for the third quarter of fiscal 2022, we see at least some positive trends. Stericycle could generate $690.3 million in revenue and compared to $648.9 million in the same quarter last year this is an increase of 6.4% year-over-year. And not only revenue could improve - instead of an operating loss of $50.6 million in the same quarter last year, Stericycle reported an operating income of $50.6 million this quarter. The bottom line also "switched" from a diluted loss per share of $0.72 in the same quarter last year to $0.30 earnings per diluted share this quarter. And adjusted diluted earnings per share increased from $0.44 in Q3/21 to $0.65 in Q3/22 - an increase of 48% year-over-year.

{kind=link}

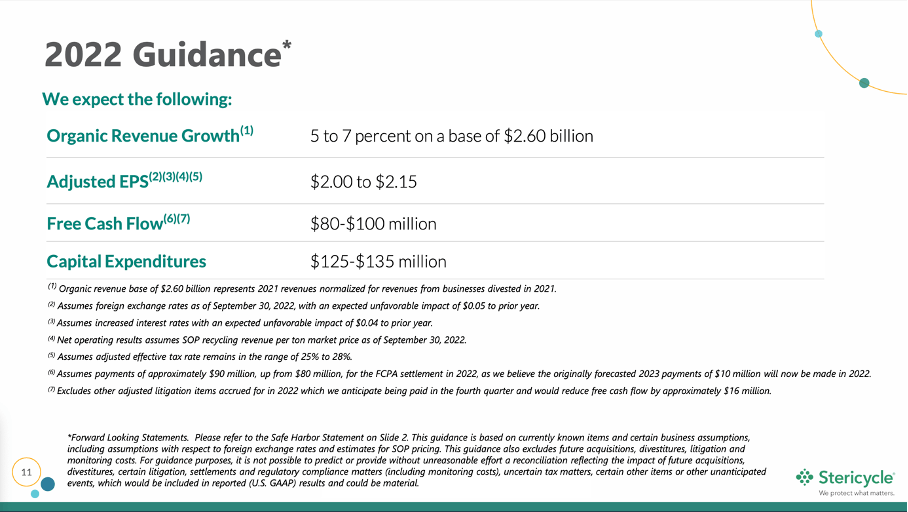

And for the full year of fiscal 2022, Stericycle is expecting organic revenue to increase between 5% and 7% compared to fiscal 2021. Adjusted earnings per share are expected to be between $2.00 and $2.15 and free cash flow is expected to be between $80 million and $100 million.

{kind=link}

Balance Sheet

Another remaining problem for Stericycle is the company's balance sheet. On September 30, 2022, the company reported $17.2 million in short-term debt and $1,652 million in long-term debt. When comparing the total debt to the total equity of $2,326 million, this results in a debt-equity ratio of 0.72. But while that D/E ratio seems acceptable, the picture gets different when looking at further metrics. First, when comparing the total debt to the operating income we get metrics which are not acceptable for an investment. When comparing total debt to the operating income of the last four quarters ($173.3 million), it would take almost 10 times operating income to repay the outstanding debt. We must go back several years to see an operating income high enough to repay the total debt within a reasonable number of years (three to four years). Second, the debt-equity ratio is only acceptable because the company has a total equity due to higher total assets. But when looking closer at total assets, we see $2,749 million in goodwill on the balance sheet (51% of total assets) and these high amounts of goodwill are not only problematic, but when subtracting goodwill from total assets, total equity would be negative.

In 2016, long-term debt and goodwill increased due to the acquisition of Shred-It. Long-term debt was $3.20 billion and goodwill was $3.79 billion. Since then, the company could reduce both its goodwill and long-term debt, but not enough in my opinion. Especially goodwill is still extremely high - despite a goodwill impairment charge of $573.1 million in fiscal 2020.

Lawsuits

In the last few years, Stericycle also faced several lawsuits, which did not only have a negative impact on the business but should also make us cautious about Stericycle as an investment. I already wrote about the most prominent lawsuit Stericycle faced in the last few years in a previous article . Stericycle was accused of fixing prices for many of its customers and agreed to a $295 million deal to end multi-state class action lawsuits.

The company also faced several lawsuits in which the business was accused to violate several clean air rules. These lawsuits were settled for $2.6 million, which is a rather low amounts for Stericycle. And the company also agreed to pay a $150,000 penalty after the EPA found that the company violated terms of its waste-handling and storage permit. But once again, such small penalties are not really a problem for Stericycle. Nevertheless, these continuous lawsuits are not really great for Stericycle and its investors.

Does It Have An Economic Moat?

In my first articles about Stericycle, I was quite convinced the business had a wide economic moat. And in theory, I saw (and still) see several tailwinds for Stericycle. Not only should Stericycle profit from the aging society that will increase the demand for medical treatments, which will increase medical waste, Stericycle is also operating in a highly regulated industry which often makes it difficult for new competitors to enter an industry. And aside from the different regulations, the distribution network of Stericycle - which would take time and money to duplicate for any competitor - is also creating a barrier for entry and leading to cost advantages for Stericycle. These aspects combined made the argument reasonable for Stericycle to have an economic moat around the business.

Stericycle Investor Day 2016 Presentation

{kind=link}

But when looking at the last few years, we seriously must question if Stericycle has an economic moat. And even companies with an economic moat around its business can have one or several years of mediocre performance (for several different reasons). But Stericycle is struggling since 2015 with all the negative aspects I described above - wildly fluctuating earnings per share and reporting a loss for four years in a row, gross and operating margins declining constantly and reporting extremely low return on invested capital numbers. And the biggest problem is revenue declining almost 30% from its previous levels. Free cash flow and earnings per share can fluctuate, but businesses with a wide economic moat should be able to defend its revenue due to the economic moat. And a revenue decline of 30% (without a divesture of huge parts of the business) is problematic and should really make use question if the business has a wide economic moat.

And Stericycle is now underdelivering for a long time. In my 2018 article about Stericycle, I included management's long-term targets and for sales the company expected potential growth rates between 4% and 7% annually. Now - about 5 years later - we know that was far from the truth. And I don't know why I should start turning bullish now - especially as the company does not seem extremely undervalued or like a huge bargain (which could justify taking a calculated risk).

Intrinsic Value Calculation

We started the article by stating that the two major simple valuation metrics - the P/E ratio and P/FCF ratio - are useless. But instead of looking at simple valuation metrics, we can determine an intrinsic value for the stock by using a discount cash flow calculation.

{kind=link}

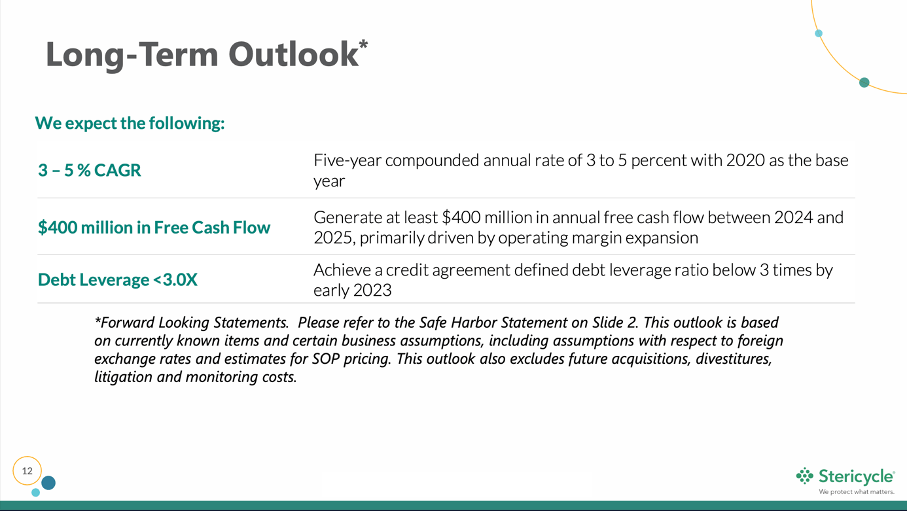

And let's once again work with the guidance and assumptions provided by management. Right now, management is expecting free cash flow to be between $80 million and $100 million and for 2024 it assumes free cash flow to be at least $400 million. When taking these assumptions and 92.2 million outstanding shares and a 10% discount rate, Stericycle must grow about 3% annually from now till perpetuity to be fairly valued.

And while about 3% growth certainly seem realistic, I have my doubts if Stericycle can achieve $400 million in free cash flow. When looking at the last ten years, Stericycle achieved similar numbers in two years, but in most years free cash flow was much lower.

| Free cash flow | Free cash flow | ||

|---|---|---|---|

| 2012 | |||

| $325.6 million | |||

| 2017 | |||

| $365.6 million | |||

| 2013 | |||

| $332.2 million | |||

| 2018 | |||

| $34.9 million | |||

| 2014 | |||

| $362 million | |||

| 2019 | |||

| $53.8 million | |||

| 2015 | |||

| $271.3 million | |||

| 2020 | |||

| $410.7 million | |||

| 2016 | |||

| $424.6 million | |||

| 2021 | |||

| $186.2 million |

This makes me question how Stericycle should be able to achieve $400 million in free cash flow - especially as I don't see a clear path for the business improving. And to achieve these amounts, margins must be much higher in the years to come. When taking the average free cash flow of the last ten years - which was $277 million - as basis in 2024, the company must grow about 5% annually till perpetuity to be fairly valued. And while such a growth rate is possible, is see Stericycle fairly valued at best.

Conclusion

In my opinion, Stericycle is only a hold right now. The downside risk seems limited in my opinion (the price range between $40 and about $45 should be a strong bottom), but I also don't see much upside potential right now. And I certainly see better investments in the market - other companies that are clearly undervalued and with a clear path and upside potential. As the stock market is providing us with the luxury of passing on certain companies and stocks (as there are thousands of alternatives) I will pass on Stericycle.

For further details see:

Stericycle: Metrics Show A Crumbling Moat And No Turnaround