SPY - Stock Market Bears May Finally Be On The Right Side Of The Narrative

2024-01-17 23:46:27 ET

Summary

- The S&P 500 is struggling to break out higher at the start of the year.

- The market appears to be clinging to 2023 bullish talking points the same way bears held onto the 2022 narrative last year.

- Dollar strength and rebound in bond yields signal a more volatile environment for stocks and risk assets.

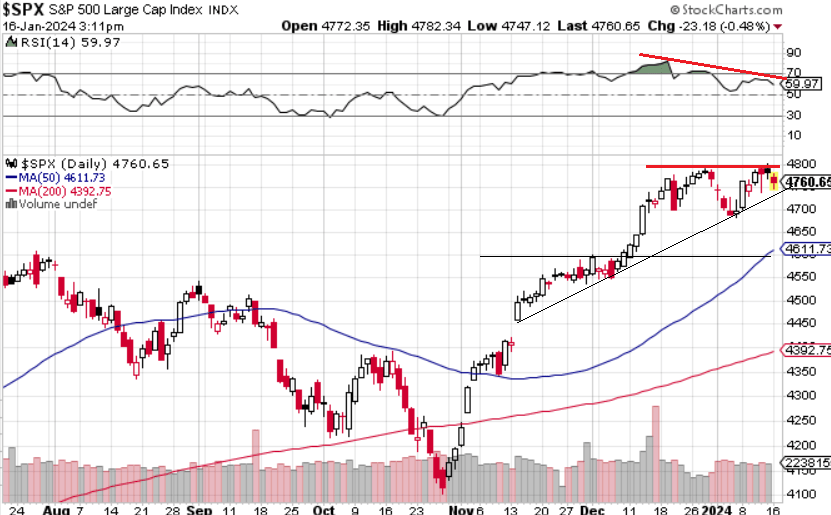

Despite the extreme market bullishness entering 2024, the S&P 500 ( SPX ) has struggled to maintain momentum in the first few weeks of the year and remains a few points short of a new all-time high.

The theme playing out now is renewed questions regarding the pace of expected Fed rate cuts and concerns regarding the underlying strength of the economy. While volatility remains relatively subdued, the sense is that the trading environment has markedly shifted with correlations breaking down and new divergences between winners and losers.

Our last macro note took a decisively bearish outlook on the stock market and we can reaffirm that view here with an expectation that the next big move is lower. As we see it, the rally is tired with bulls clinging to talking points that are essentially last year's news.

In many ways, we see parallels between this current dynamic to the setup in early 2023 where bears at the time failed to recognize the changing market backdrop, likely falling for textbook behavioral biases. Revisiting some of those lessons highlights a need for caution. Bears got it wrong in 2023, but may finally be getting it right.

{kind=link}

Significant Risks To The Narrative

To summarize the market consensus for 2024, the overriding narrative is that the U.S. economy is avoiding a recession with a clear path for inflation to continue trending lower setting up the long-awaited Fed pivot

The idea here is that looming interest rate cuts will help kickstart a new economic growth cycle as a tailwind for corporate earnings, thereby pushing stocks significantly higher. It sounds great and even straightforward, but we'd make the case that anyone buying into that thesis is late to the party.

So going back to our parallel from last year, bears at the start of 2023 pointing to Fed rate hikes and a painful path to get inflation under control as a catalyst for a big selloff were essentially rehashing talking points that would have worked at the start of 2022. In this case, Bulls are driving by focusing on the rearview mirror of events.

Simply put, the market is already thinking about what's next, and it's a mistake for investors to not incorporate new information. In our opinion, risks have never been greater with many of the positives in the outlook already priced in.

In terms of what could go wrong, the following points stand as potential 2024 headwinds that could derail the new bull market:

The risk that the pace and timing of Fed rate cuts get pushed back

If inflationary pressures re-emerge and the CPI remains higher than expected, or the economy appears too strong, the Fed would likely maintain rates at the current level for longer. The eventual first rate cut could also be followed by a pause over several subsequent meetings.

This scenario becomes a risk for stocks given earnings estimates are dependent on expected credit cycle impulse. Lower rates are also necessary to support higher valuation multiples. It's a thin line for everything to go right.

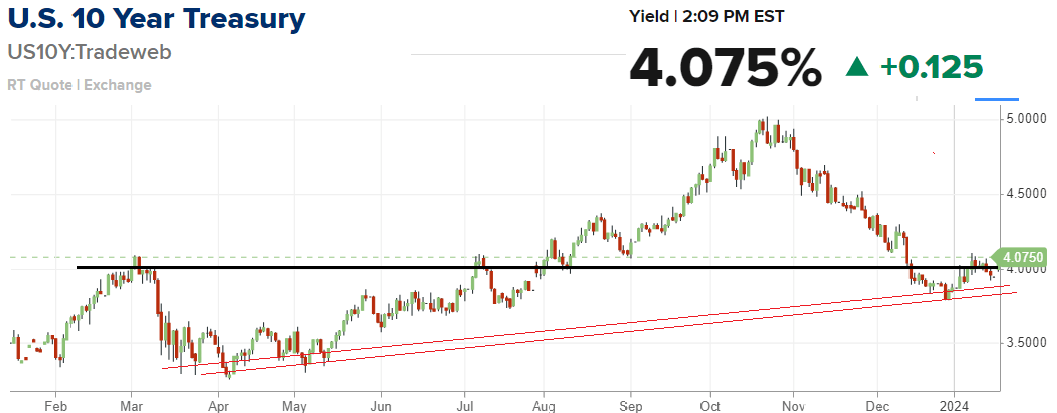

The early warning sign here is the latest climb in bond yields. The 10-year Treasury Rate has moved firmly above 4% compared to a December low of 3.79%. The latest December retail sales came in above expectations pushes back on any urgency for the immediate cuts. The read here is rising uncertainty about the path the Fed will take.

{kind=link}

The risk that economic conditions deteriorate

While the U.S. remained surprisingly resilient despite high interest rates over the last two years, the concern is that conditions could start to roll over into the second half of the year. That possibility would likely be accompanied by the hallmark labor market weakness with sharply higher unemployment.

In this case, even if the Fed moved to cut rates quickly, that dovish pivot would likely be too late to avoid a reset of growth expectations and the corporate earnings impact. We'd say that each month that goes by with interest rates at the current level raises the risk of some type of economic dislocation.

So between those two distinct outcomes, a lot can go wrong to introduce further volatility in financial markets. We can point to disappointing macro data out of China as a headwind for global trade. There is also the ongoing geopolitical crisis in Eastern Europe as well as the Middle East.

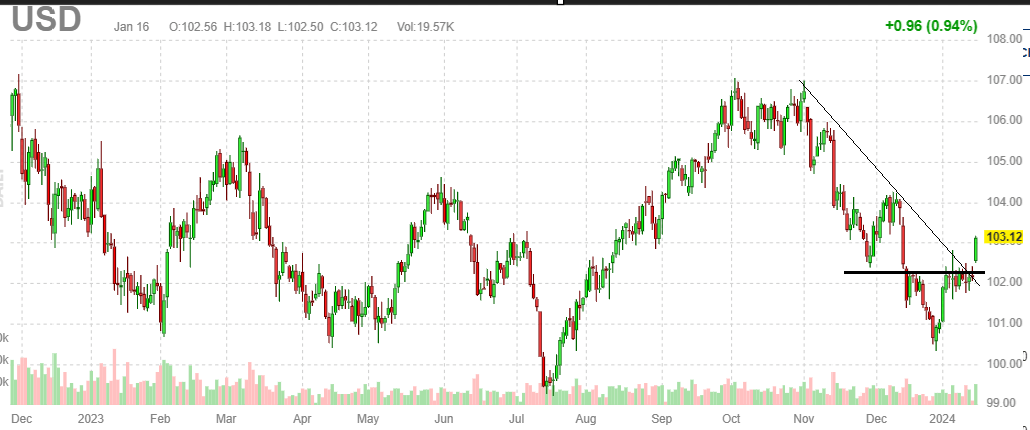

The combination of a stronger U.S. Dollar and rising bond yields also add to risk aversion. Ultimately, the potential that earnings over the next several quarters emerge weaker than expected for any number of reasons would put the bears back in control.

{kind=link}

Rate Cutting Outlook Is Too Aggressive

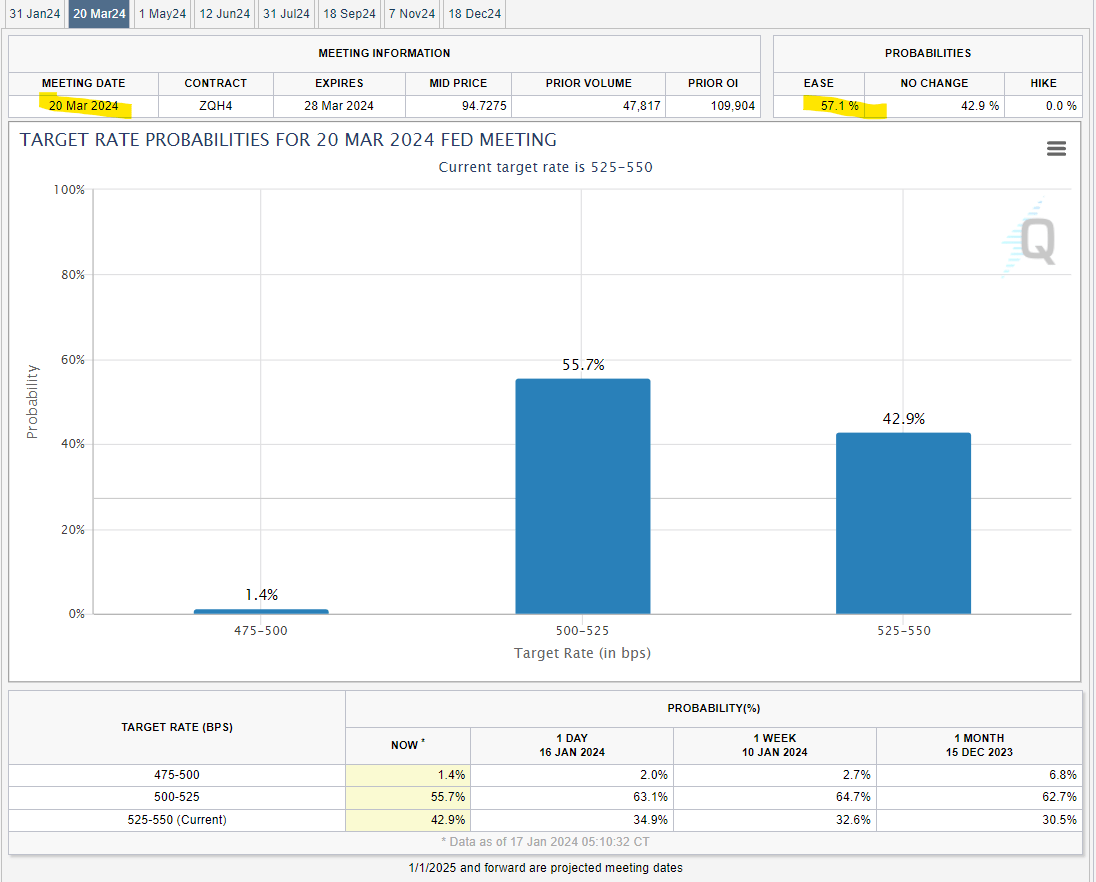

According to the CME FEDWatch Tool , which extrapolates interest rate futures pricing into implied probabilities for the Fed Funds Rate to end a period at a certain level, the market expects the Fed to cut by at least 150 basis points in 2024.

The scenario for six or seven 25bps cuts essentially requires a first move at the March Fed meeting with cuts at each subsequent meeting for the rest of the year. We believe the pace is too aggressive given the circumstances.

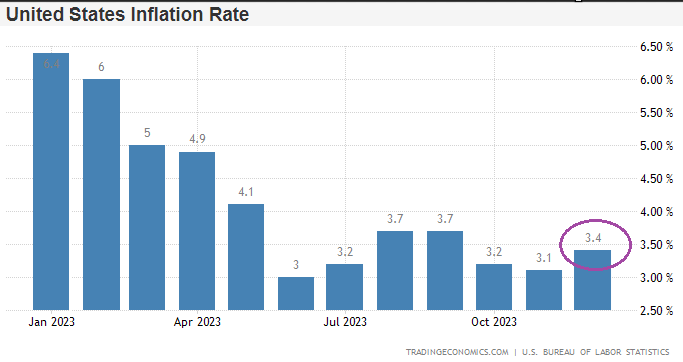

Last week, the updated December CPI data came in a tick higher than expected with the headline rate of 3.4% "bouncing" from 3.1% in November. While there are still some favorable trends playing out within the data including core measures like shelter and vehicle prices seen slowing going forward, the question becomes if the Fed has enough confidence to at least "signal" a March rate cut at the upcoming January 31s FOMC.

{kind=link}

The problem here is that historically the Fed uses a meeting before a major policy change as the opportunity to communicate the framework for that next step to not leave any surprises.

Ideally, the Fed could come into the January meeting with strong confidence the CPI was not at risk of climbing higher, teeing up a series of rate cuts. It appears to us that more time is necessary.

Given the recent mixed data and precedence toward caution over the last two years, including the latest comments from Fed governors like Christoper Waller , it's more likely they take a wait-and-see approach.

There are still two months of critical inflation data and labor market updates until the March meeting, but we conclude that the market-implied odds for a March cut at 57% are overly optimistic.

This sets up the specter of the January Fed Meeting where a proverbial final word from Chairman Powell perceived as hawkish would be met by a major market reaction translating into a selloff for stocks.

{kind=link}

Be Attentive To Behavioral Biases

Recognizing that the difference between 6 or "just 4" rate cuts is not necessarily apocalyptic for the stock market, the lingering uncertainty points to a broader disconnect between the extremely optimistic consensus and a higher level of underlying risks.

Investors should be attentive to potential behavioral biases at play, including belief perseverance as a concept dealing with difficulty in incorporating new information. If the inflation data does not cooperate, the Fed will need to push back.

Much like the bears in 2023 that were dreaming of retesting the mythical S&P 500 October 2022 lows of $3,500, bulls counting on an unabated levitation to $5,000 and beyond may be setting up a disappointment.

There are also emotional biases that can impact the decision-making process. On the heels of a fantastic rally to end 2023, bulls should not assume that the winning streak lasts forever reflected in overconfidence bias.

What's more important is to have a plan and be prepared for anything. There are times when following the trend makes sense and others where taking a contrarian view is optimal. We all "want" our investments to deliver continuously positive returns, but risk is an important part of the equation. What worked in 2023 may or may not work in 2024 as conditions change.

What about Stocks?

Entering into the start of Q4 earnings season, the early themes include financials beating estimates, but bank stocks selling off anyway. The real test will come in the next couple of weeks as the mega-cap tech players have their turn.

Curiously, names like Microsoft ( MSFT ), Meta Platforms ( META ), and Nvidia ( NVDA ) have led higher to start the year which we believe sets a high bar of expectations into their reports. Much like the macro side, the story that defined 2023 for this group is hardly new.

Rebounding growth and firming margins are likely to continue but should hardly come as a surprise. If anything the weakness at the top line playing out suggesting softer than expected demand momentum could be enough to force a selloff.

As it relates to the S&P 500, we see the index trending lower towards $4,600 as the next area of major technical support. The January Fed meeting has the potential to be a major market turning point depending on how the messaging evolves. Overall, the message here is to pare down expectations and avoid chasing momentum names as a measure to reduce risk.

{kind=link}

For further details see:

Stock Market Bears May Finally Be On The Right Side Of The Narrative