DM - Stratasys: Belle Of The Ball

2023-07-18 11:45:24 ET

Summary

- Stratasys is positioning itself for mass production use cases and is pursuing an acquisition of Desktop Metal in support of this strategy.

- At the same time, a bidding war is emerging between 3D Systems and Nano Dimension. 3D Systems is best placed to acquire Stratasys, but its offer isn't that compelling.

- If 3D Systems' offer is rejected, Stratasys' stock could drop significantly, although this may be in the best interest of shareholders long-term.

Stratasys ( SSYS ) is a leading provider of additive manufacturing solutions, but the company has a long history of disappointing financial and share price performance. Despite this, Stratasys' management team seems to believe that additive manufacturing has reached an inflection point, and as a result are trying to position the company to benefit from mass production use cases. In support of this, Stratasys is trying to acquire Desktop Metal ( DM ) for its metal 3D printing technology.

At the same time, there is an emerging bidding war for Stratasys between Nano Dimension ( NNDM ) and 3D Systems ( DDD ). Stratasys appears to be seriously contemplating the latest offer, but the outcome remains highly uncertain. Stratasys is clearly not entertaining Nano Dimension as a suitor, and has taken a dim view of 3D Systems' business in the past. In addition, the offers received so far are far from irresistible.

Market

In the past, additive manufacturing has primarily been used for applications like prototyping, but Stratasys believes that the technology has matured to the point where it will increasingly be adopted for mass production.

Additive manufacturing is suited to use cases where:

- Products are customized.

- Lead times are short.

- Production run volumes are relatively small.

- Parts are complex.

Additive manufacturing can also help to reduce waste and enables distributed manufacturing, which can reduce supply chain costs.

Adoption is held back by the fact that:

- Tolerances aren't as tight as methods like CNC machining.

- There is less industry knowledge about implementing additive manufacturing.

- Print sizes are limited.

- Print speeds are often prohibitively slow.

The technology continues to improve though, with printers becoming faster and less expensive. A greater range of materials are now also available with improved properties. Newer technologies can also eliminate the need for support structures, opening up new use cases. These types of technology improvements are expected to open up new use cases and lead to significant market growth.

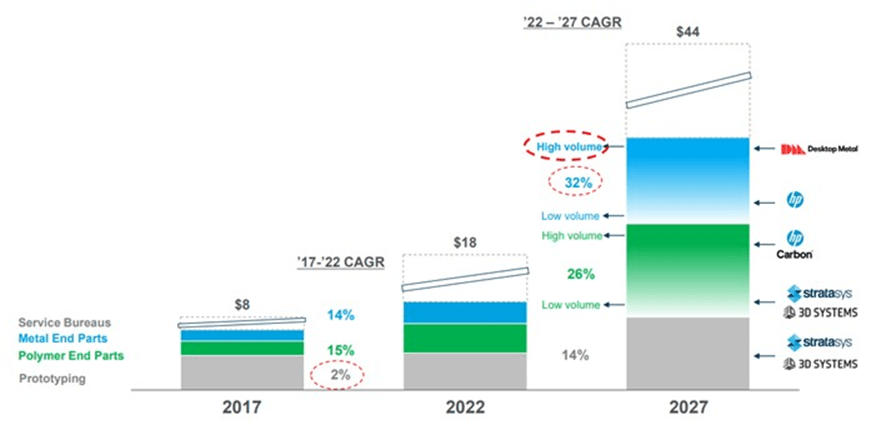

Figure 1: 3D Printing Market Size - billion USD (source: 3D Systems)

Additive manufacturing has seen relatively rapid adoption in medical applications as they are generally highly customized, high-value applications that offer benefits to patients and clinicians that conventional manufacturing technologies cannot match. Within this field, Stratasys is focused on the dental market. Stratasys believes that dental could be a 50 billion USD opportunity for additive manufacturing, with dentures alone providing a 5 billion USD market in the US. The manufacturing of dentures is currently labor intensive and Stratasys believes that it can provide a higher quality solution.

Stratasys' current portfolio skews toward polymers, but the company is trying to increase its exposure to metal additive manufacturing through a proposed combination with Desktop Metal. The use of metal additive manufacturing is still generally low, but is growing rapidly and is expected to be worth as much as 10 billion USD by 2030 to 2035. Current barriers to adoption include the high costs of metal powder and 3D printers for large-scale production, as well as significant constraints on the dimensions of printed parts. Additionally, most printers cannot mix materials within one item.

Stratasys

Stratasys is a leader in polymer-based 3D printing solutions. The company offers five different 3D printing technology platforms, each of which is optimized for specific industry applications. Stratasys also has a technology-agnostic software platform and offers a range of materials and professional services. While the company reaches a range of end markets, targeted verticals include industrial, healthcare and consumer.

Stratasys' 3D printing technologies include:

- Extrusion-based FDM.

- Inkjet-based PolyJet.

- Powderbed-based SAF.

- Photopolymer-based P3.

- Stereolithography.

Stratasys has market-leading systems in FDM and polyjet, new technology offerings in P3, sub and stereolithography, and the broadest set of polymer materials in the industry.

Stratasys is focused on expanding the use of additive manufacturing to higher volume use cases and believes that its P3 and SAF technologies are an important part of this. These technologies could increase the volumes at which additive manufacturing is competitively advantageous up to tens of thousands of units.

Programmable PhotoPolymerization (P3) technology is an evolution of Digital Light Processing. DLP uses a projected light source to cure an entire layer of material at once, allowing parts to be formed layer by layer in a relatively rapid process. P3 is a similar process but software controls printing parameters (light, temperature, pull forces and pneumatics) to optimize results. P3 improves part quality and surface finish using an expanding range of materials.

Selective Absorption Fusion ((SAF)) is a type of powder bed fusion 3D printing. SAF uses an infrared absorption fluid to fuse particles of polymer powder together in layers to build parts.

Stratasys also offers software, and this appears to be a focus area for the company. Through its GrabCAD Additive Manufacturing Platform, Stratasys is trying to create a connected software ecosystem. The company offers SDKs which enable integration with a range of partner solutions. Stratasys has one platform across its technologies, based on GrabCAD Print with packages added onto it as needed.

Stratasys is not focusing on the MES part of the business though. Instead, it has chosen to concentrate on additive manufacturing and providing customers the ability to manage additive manufacturing workflows. A manufacturing execution system is used to orchestrate the manufacturing process from end-to-end.

Stratasys believes that the integration of hardware and software provides it with an advantage as it has access to logs which provide insight into customer needs. The company's large installed base is a potential advantage in this regard. Conversely, a lot of AM equipment relies on vendor-specific software, with little integration between different machines and other manufacturing control systems. This complicates the use of additive manufacturing technology, particularly in a production environment.

Stratasys believes it is beginning to make progress in software on the back of several years of investment. The expansion into software is also helping to create opportunities within systems and materials.

Stratasys also has exposure to desktop 3D printers, which is a market that has undelivered relative to expectations over the past decade. The company believes that the proliferation of 3D modelling software and scanners could reinvigorate this market though. 3D printing technology is also improving, and entry-level systems have become more affordable. To support its 3D printing business, Stratasys has invested in UltiMaker, a company created from the merger of MakerBot and UltiMaker.

Stratasys is also making progress in healthcare applications, recently introducing a monolithic multi-colored dental solution using its TrueDent resin. This is the company's first FDA-cleared medical device. TrueDent enables the creation of realistic looking dentures in one continuous print. While this business is still nascent, it is expected to be a revenue contributor in the second half of 2023.

Regenerative medicine is another area that Stratasys is looking to leverage its additive manufacturing technology, through a partnership with CollPlant ( CLGN ). The two companies have a joint development and commercialization agreement which is focused on bioprinting solution for regenerative breast implants, a 2.6 billion USD market opportunity . Regenerative breast implants are designed to regenerate an individual's natural breast tissue without eliciting an immune response. Stratasys is contributing its P3 technology-based bioprinter and CollPlant is providing plant-based collagen bioinks. CollPlant recently announced the successful completion of a large-animal study using its 3D bioprinted regenerative breast implants. The study demonstrated tissue regeneration with no adverse events reported.

Acquisitions

Stratasys has made a number of acquisitions in recent years to expand its portfolio of solutions. This is part of a broader consolidation trend within the industry where larger players are trying to create scale through acquisitions.

Stratasys acquired Origin in 2021 for its photopolymer solutions, which target mass production-oriented applications. P3 technology appears to be one of the main focus areas for Stratasys, with management expecting it to add up to 200 million USD incremental revenue annually within five years. Total consideration was up to 100 million USD in cash and stock.

Stratasys acquired RPS in February 2021 for its stereolithography 3D printers, which expand Stratasys' polymer suite of solutions across the product life cycle. The Neo line of printers feature dynamic laser beam technology that enables build accuracy, feature detail, and low variability across the full extent of a large build platform.

Stratasys acquired the remaining outstanding shares of Xaar in November 2021. This move was aimed at accelerating Stratasys' growth in production-scale 3D printing. Xaar has powder-based SAF technology which is designed to deliver cost-competitive parts at production-level throughput.

Stratasys signed an agreement with Covestro in August 2022 to purchase its AM materials business. This expanded Stratasys' material offerings in stereolithography, DLP and powders. The deal included R&D facilities, global development and sales teams, and a portfolio of 60 materials.

Desktop Metal

Stratasys recently made an offer to merge with Desktop Metal, a leading provider of metal additive manufacturing solutions. The merger would strengthen Stratasys' metal printing business and aligns with the company's mass production vision. Stratasys' go-to-market capabilities could also help accelerate Desktop Metal's sales.

Figure 2: Additive Manufacturing Market by Material and Application - Billion USD (source: Stratasys)

{kind=link}

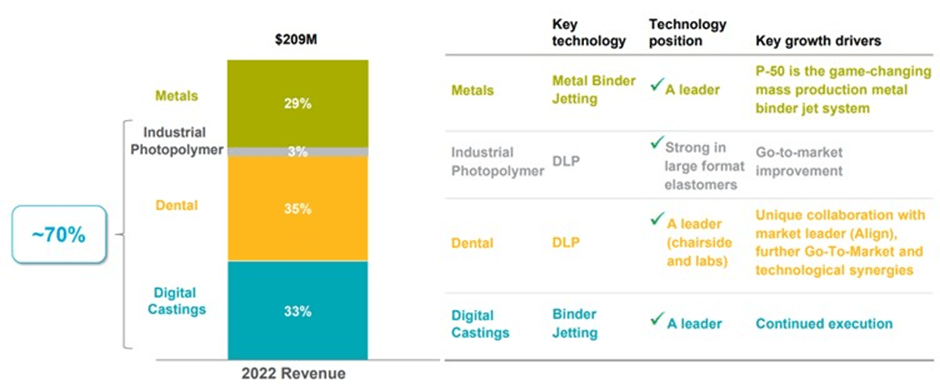

Stratasys believes that Desktop Metal has the most advanced metal technology for mass production. This is supported by the fact that Desktop Metal's market share has been increasing rapidly. Desktop Metal's binder jet technology processes metal, sand and ceramics. The company also has unique sintering and software simulation capabilities.

Figure 3: Desktop Metal Revenue by Segment (source: Stratasys)

{kind=link}

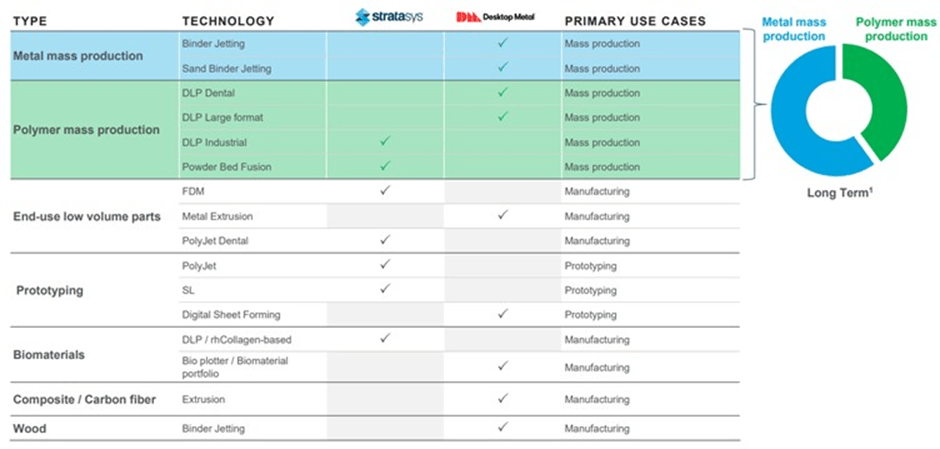

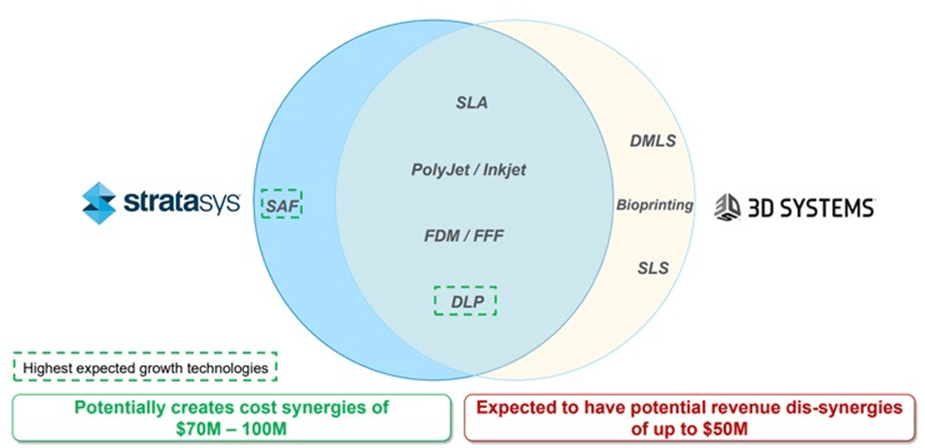

In addition to gaining exposure to metal mass production, Stratasys believes combining the product portfolios of the two companies is attractive as there is broad coverage of the market with limited overlap.

Figure 4: Combined Company Product Portfolio (source: Stratasys)

{kind=link}

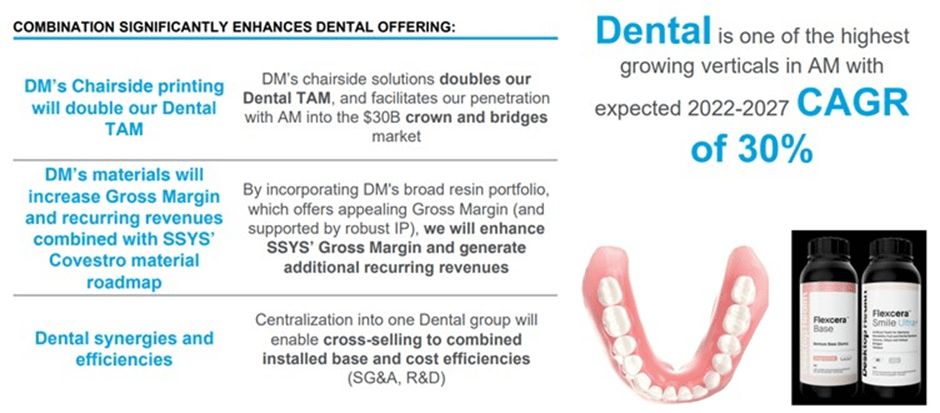

The acquisition of Desktop Metal, along with the materials acquisition from Covestro, would also significantly strengthen Stratasys' dental business.

{kind=link}

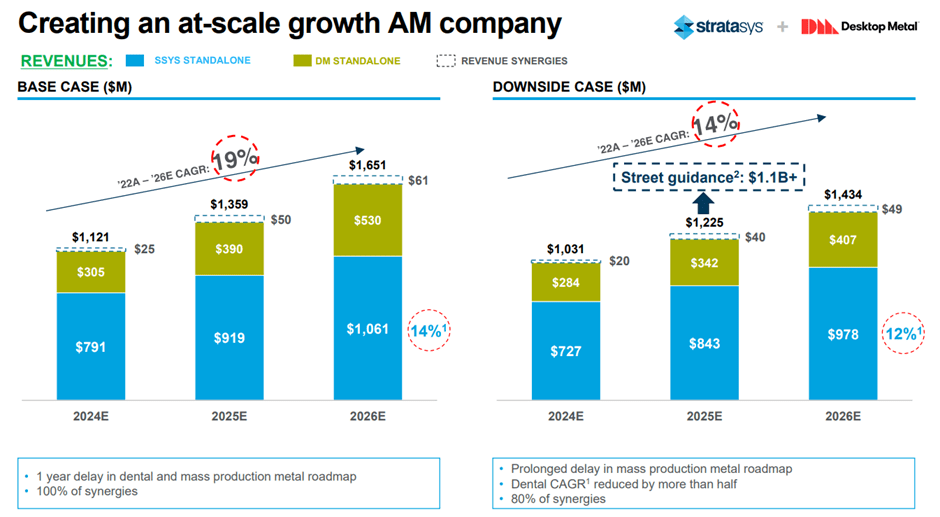

Stratasys believes that the merger will accelerate growth and significantly increase revenue. This is important as additive manufacturing companies have generally had difficulties reaching sufficient scale to achieve profitability.

{kind=link}

{kind=link}

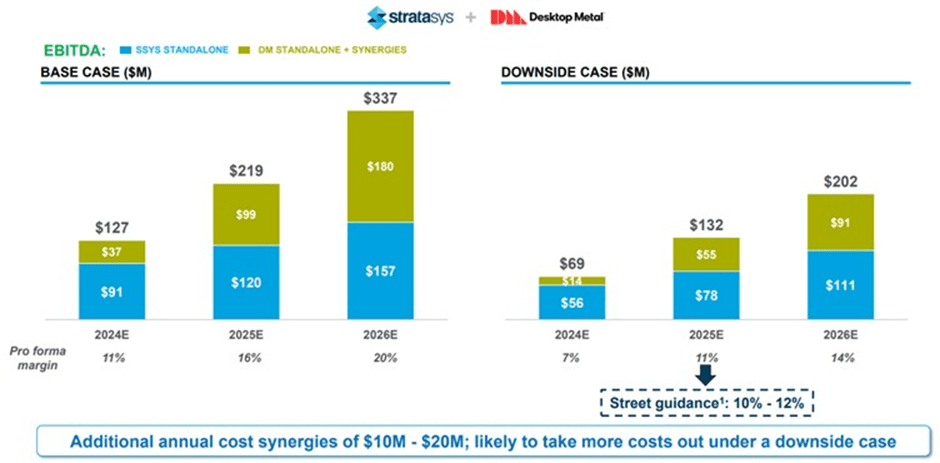

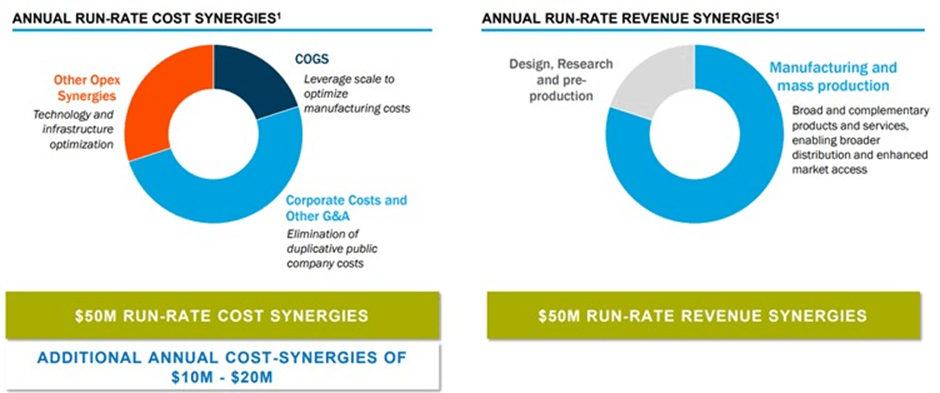

Stratasys also expects to realize significant cost and revenue synergies through the merger. Elimination of duplicated overhead costs and utilizing Stratasys' distribution footprint to accelerate Desktop Metal's sales are key drivers of expected synergies.

{kind=link}

Acquisition Offers

Stratasys is also currently the target of takeover attempts by Nano Dimension and 3D Systems, with a bidding war beginning to emerge. In recent months Stratasys has received offers worth 18, 19.55, 20.05 and 24 USD per share .

3D Systems' latest offer is 7.5 USD cash and 1.544 newly issued shares of 3D Systems common stock per ordinary share of Stratasys. Stratasys is reportedly considering this offer and views it as superior to Nano Dimension's offer. The key issues with the Nano Dimension offer are that it is only a partial tender and Stratasys does not trust Nano Dimension to manage the company properly.

While Stratasys is considering 3D Systems' latest offer, it has also displayed skepticism towards 3D Systems' product portfolio in the past. 3D Systems' would provide the combined company with scale and cost synergies, but it would lack metal technology which Stratasys believes is necessary for mass additive manufacturing.

Stratasys thinks there is a risk that DLP technology will disrupt 3D Systems' dental business in the long run. Given the importance of this business to 3D Systems, this would be devastating. Stratasys also believes that 3D Systems' SLS technology is not competitive with HSS technology at scale. The market doesn't appear to share these views though, as Stratasys trades at a sizeable discount to 3D Systems.

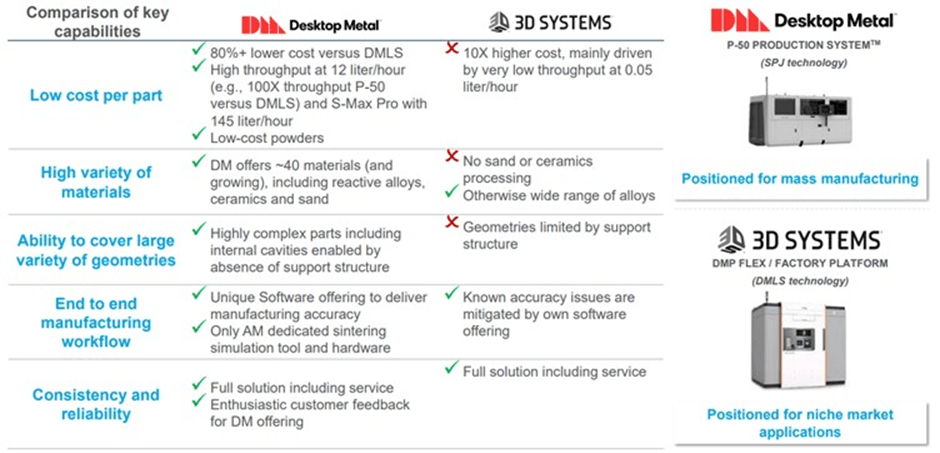

Figure 9: Comparison of Desktop Metal and 3D Systems Metal Solutions (source: Stratasys)

{kind=link}

Stratasys has also stated that the significant product overlap between the two companies could cause significant revenue losses.

{kind=link}

Given that 3D Systems' offer is largely in the form of stock and places a lower multiple on Stratasys' business than 3D Systems' current valuation, it is not clear if Stratasys will accept the offer. Stratasys has made quite negative statements about 3D Systems' business, but this may have just been a negotiating tactic.

Financial Analysis

Stratasys is currently facing a difficult macro environment, and in this light its recent performance has been reasonable. Conditions are pressuring CapEx budgets, leading to longer sales cycles and in some cases the deferral of orders. This environment is expected to persist throughout 2023.

Revenue declined by 8.6% YoY in the first quarter of 2023, or 2.6% adjusted for divestitures and FX movements. OEM revenue was relatively flat YoY in the first quarter, adjusted for FX and divestments, which is unsurprising given the macro environment. Product revenue declined by 10.7%, or 5.1% excluding divestitures and on a constant currency basis.

Table 1: Stratasys First Quarter Product Revenue Growth (source: Stratasys)

Services revenue including FDM was down 3.9% YoY, and up 2.4% excluding FDM. While new printer sales have been a significant headwind, system utilization remains robust driving growth in consumables and services.

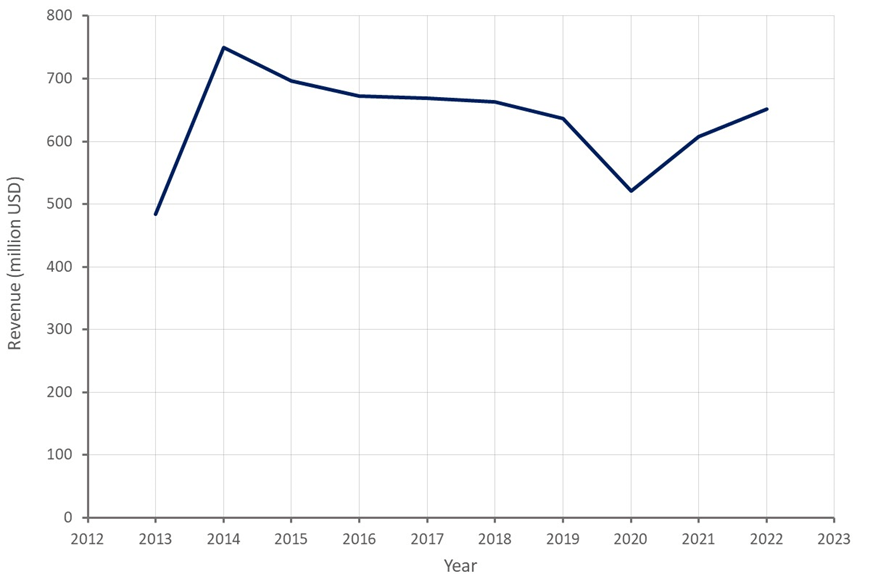

Stratasys is guiding to 630-670 million USD revenue in 2023. The deal with Covestro closed in early April, and hence will impact the financials from Q2 onwards (primarily consumables). Initial revenues for the dental business are expected in the second half as Stratasys is progressively building the business. Demand has been strong in aerospace and is increasing in automotive.

Figure 11: Stratasys Revenue (source: Created by author using data from Stratasys)

{kind=link}

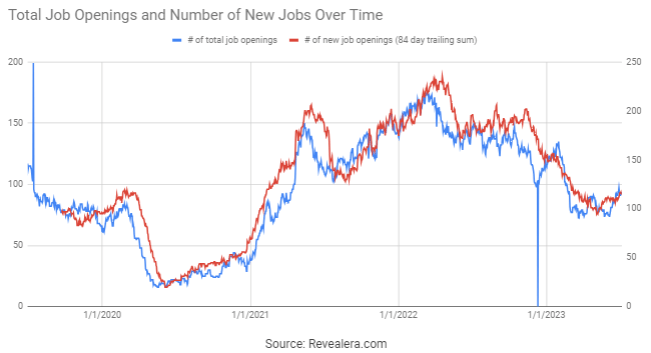

Hiring data also seems to suggest strength in Stratasys' business, with job openings picking up somewhat in recent weeks. The number of job openings remains above pre-COVID levels, even after a significant pullback over the past 12 months.

{kind=link}

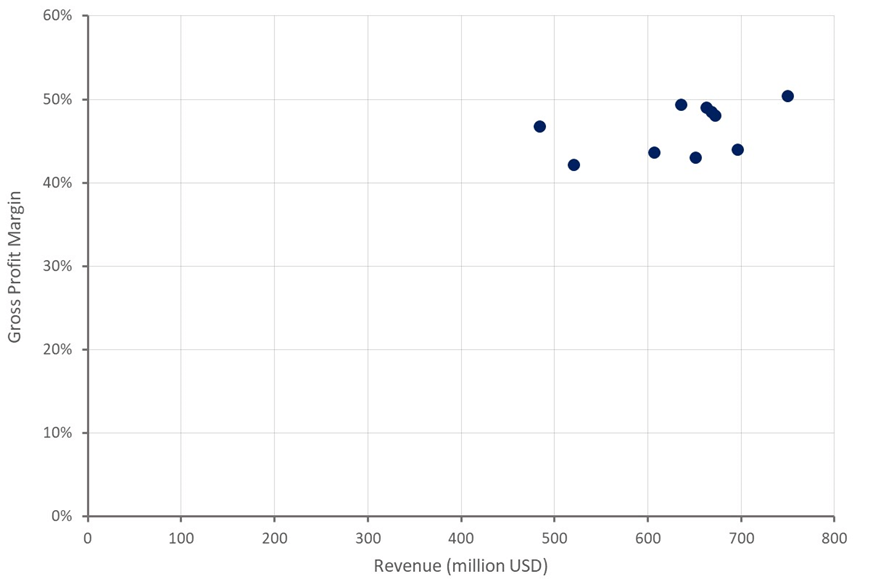

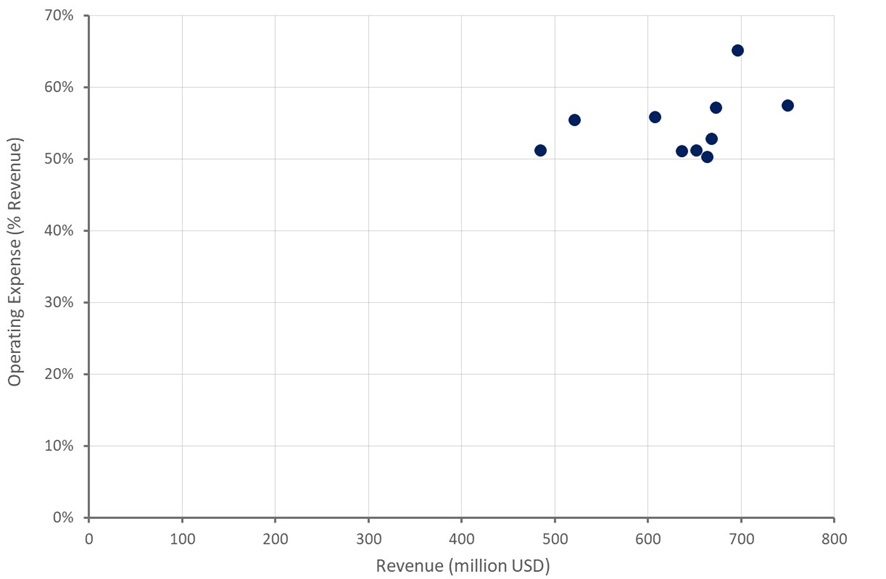

Stratasys is guiding to non-GAAP gross margins in excess of 50% and positive free cash flow in 2024. This guidance should probably be viewed with skepticism though, as Stratasys has demonstrated limited ability to improve margins over time. Gross margins appear to be expanding slightly with scale, but this has so far been offset by rising operating expenses.

An increased focus on costs and greater scale is likely to lead to profits in time, but growth may be difficult to come by while the broader manufacturing industry is struggling.

Figure 13: Stratasys Gross Profit Margins (source: Created by author using data from Stratasys) Figure 14: Stratasys Operating Expenses (source: Created by author using data from Stratasys)

{kind=link}

{kind=link}

Stratasys is targeting adjusted EBITDA margins of over 15% and 1 billion USD revenue in 2026. The ability of the company to meet these targets will depend on the success of its dental business and the adoption of additive manufacturing in mass production. Stratasys is also optimistic about regenerative medicine over the next three to five years, although this business still involves significant technical risk.

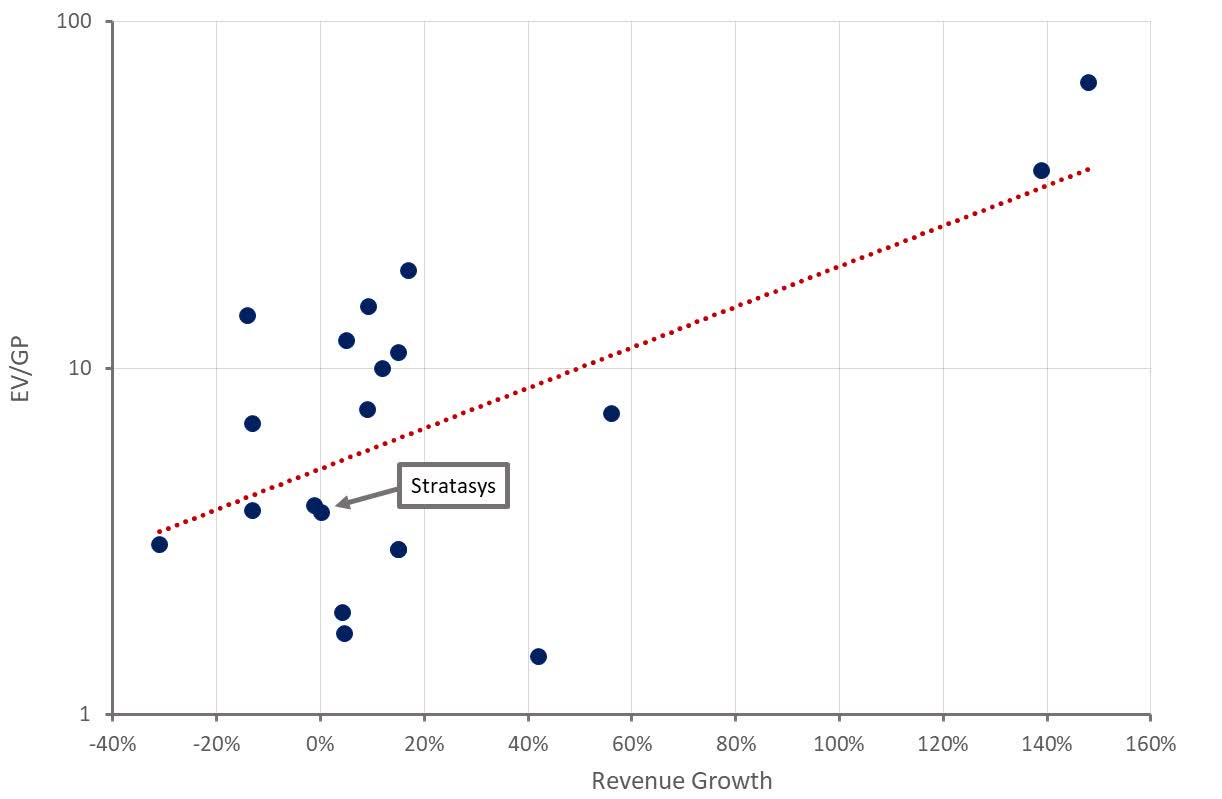

Valuation

Even after the recent share price run-up, Stratasys' valuation is still relatively modest. This is a reflection of the fact that Stratasys has struggled in the past to create growth or profits for shareholders. Wider adoption of additive manufacturing technology and expansion of the dental business could help Stratasys turn the company's fortunes around though.

The company's fundamentals are somewhat irrelevant to the stock price until a decision is made about which deal to pursue. 3D Systems' offer may be the most attractive at this point, particularly in the near term, although it could be argued that the Desktop Metal deal offers more upside.

Stratasys is currently trading at a modest discount (5-10%) to 3D Systems' latest offer, which could indicate the market views a deal as probable. The company's stock was trading below 15 USD per share prior to receiving any offers, meaning a significant drop is likely if 3D Systems' offer is rejected.

Figure 15: Stratasys Relative Valuation (source: Created by author using data from Seeking Alpha)

{kind=link}

For further details see:

Stratasys: Belle Of The Ball