DM - Stratasys: Merger With Desktop Metal Is Worth More Than The Standalone Entities

2023-07-06 10:33:16 ET

Summary

- SSYS is set to acquire DM in an all-stock deal, creating a combined entity with a broader market reach in the additive manufacturing industry.

- The merger strengthens SSYS' presence in polymer printing, extends its reach into the dental market, and equips it with crucial capabilities in metal, composite/carbon fiber extrusion, and binder jetting printing.

- Despite potential integration risks, I am optimistic about the potential upside from the current share price and have revised my recommendation for SSYS from hold to buy.

Investment thesis

My previous post on Stratasys ( SSYS ) highlighted to stay on the side lines until there is more proof of accelerating operating leverage and FCF conversion improvement. I had expected this to start showing up in 2H23 when the economy turns for the better (inflation comes down). However, after considering the merger with Desktop Metal ( DM ), I have decided to change my recommendation for Stratasys from hold to buy. SSYS has made significant headway in repositioning itself to take advantage of prospects in additive manufacturing over the past few years. SSYS' expertise in hardware, materials, and software, as well as its extensive go-to-market reach, combined with DM's additional essential 3D printing capabilities, I believe, will allow the merged business to address a broader set of opportunities in manufacturing. I have a high degree of optimism for the merged company and am upgrading my recommendation.

The deal

SSYS is set to acquire DM through an all-stock transaction, anticipated to be finalized in the fourth quarter of 2023. The combined entity, on a pro forma basis, achieved approximately $845 million in trailing twelve-month revenues, while reporting a negative adjusted EBITDA of -$63 million. Both companies have reiterated their revenue and adjusted EBITDA guidance for 2023. SSYS projects adjusted EBITDA in the range of $35 million to $50 million, with revenues anticipated to reach $630 million to $720 million. DM, on the other hand, has reaffirmed its full-year adjusted EBITDA guidance of -$50 million to -$25 million, alongside revenue expectations of $210 million to $260 million.

Combined entity has a much better competitive position

I have a bullish view on the combined entity. Firstly, SSYS, a prominent player in polymer additive manufacturing, is poised to expand its offerings by incorporating DM, thereby solidifying its position as a comprehensive solution provider for customers seeking diverse additive manufacturing technologies and materials in production environments. DM, boasting a customer base of over 1,200, has made significant headway in the aerospace and automotive sectors with its systems capable of scaling the production of end-use parts. By integrating DM's portfolio, which emphasizes the manufacturing of end-use parts, I anticipate that the acquisition will expedite SSYS's strategy to capture a greater share of revenue from manufacturing and mass production applications.

Moreover, this combination is expected to fortify SSYS's established presence in polymer printing, extend its reach into the rapidly growing dental market, and equip it with crucial capabilities in metal, composite/carbon fiber extrusion, and binder jetting printing. Similarly, DM is poised to benefit from SSYS's extensive reseller network, leading to revenue synergies. The combined entity is projected to have around 300 channel partners and a customer base exceeding 27,000 in the industrial sector. Furthermore, the consolidated company would hold approximately 2,400 active patents, reflecting a combined research and development expenditure of more than $500 million over the past few years. Behind this R&D capital spend is the knowledge and experience acquired through the years, that when combined together, should result in a significant step forward in R&D innovation.

The integration is also expected to yield cost synergies due to substantial overlaps in their business models. Management has outlined an anticipated annual cost synergy of $50 million, with half of the savings attributed to eliminating redundant costs associated with being public companies, while the remaining savings will stem from efficiencies in raw materials and operations.

SSYS SSYS

Valuation

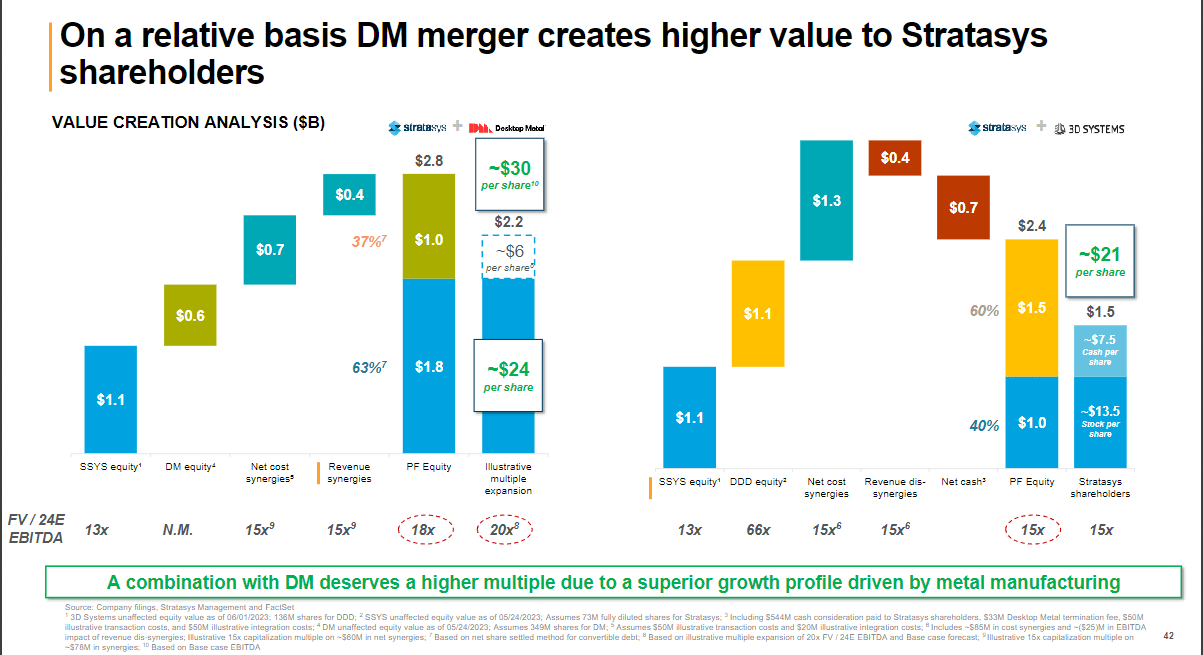

Revenue for the merged company is projected to be $885 million in FY23 on a pro forma basis, growing to $1.1 billion in FY25 with gross margins above 45% and adjusted EBITDA margins in the region of 10%-12%. I believe the combined entity is worth much more than the standalone parts given the revenue and cost synergies. Based on the relative valuation analysis conducted for this merger, the merged entity would be worth $30 when valued at 20x EBITDA. I believe this is a very attractive upside from the current $17 share price.

{kind=link}

Risks

The risk with this merger is integration risks as any mis-step here could result in potentially higher-than-expected operating expense levels, and failure to capture revenue synergies. While DM is not a very big company at $200 million revenue, it is still quite a big target for SSYS as it is 30% of its revenue. Also, DM is SSYS’s first large acquisition, so I would be slightly concern on any mis-execution here. However, I take comfort in that SSYS is an early investor in DM, so management should know the company well.

Conclusion

Considering the strategic combination with DM and the potential benefits it offers, I have revised my recommendation for SSYS from hold to buy. SSYS has successfully positioned itself in the additive manufacturing industry, and the addition of DM's 3D printing capabilities enhances its competitive position as a comprehensive solution provider. The merged entity will have a broader market reach, particularly in manufacturing, aerospace, automotive, and dental sectors. However, integration risks and the reliance on the success of the acquisition pose challenges. Nevertheless, with SSYS's early investment in DM and knowledge of the company, I am optimistic about the potential upside from the current share price.

For further details see:

Stratasys: Merger With Desktop Metal Is Worth More Than The Standalone Entities