LRN - Stride: Rock Bottom Valuation And Insurance Against Macro

2023-05-18 15:39:39 ET

Summary

- The uncertain macro environment makes Stride Inc. attractive because its low beta protects investors against a recession.

- Stride is priced like a business with a much higher beta, making its low beta a “free insurance policy”.

- Despite Stride Inc. being priced as a mature business, the company has several promising internal projects, and its Career Learning business is experiencing rapid growth.

Stride ( LRN ) is an underappreciated business in the education technology space. Investors seem to be focusing on the General Curriculum part of the business, causing the rapidly growing Career Learning segment of the business to go unnoticed. The General Curriculum business' ugly YoY numbers are a distraction because revenue, for this segment, has recently bottomed out. Additionally, Stride’s fundamentals make it a safe, low-beta business. In this article, my discounted cash flow models reveal that investors are either not pricing in Stride's low beta or Stride's strong revenue growth.

Business Description

General Curriculum

Roughly 60% of Stride’s revenue comes from the General Curriculum segment of its business. Stride’s offerings allow schools to become hybrid (partially virtual) by adding Stride’s courses, which adhere to state requirements, to their course offerings. This part of the business serves students with unique needs, such as student-athletes who need flexibility, college students who want to take extra AP classes, families who are consistently relocating, etc.

{kind=link}

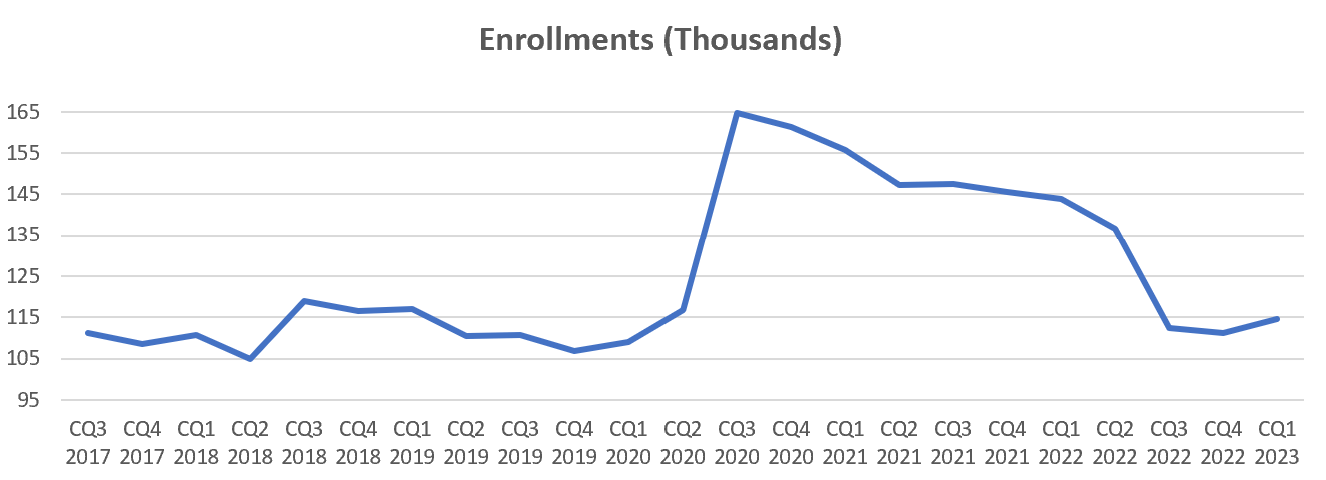

Enrollments sharply increased during the pandemic, but have now reverted to pre-Covid levels. Although the General Curriculum part of the business will continue to generate consistent cash flow, it'll likely experience little growth. The TAM appears to include a small percentage of schools and students because most students prefer in-person instruction.

However, management, in Stride’s latest conference call, mentioned a project they’re working on called the Learning Hub. The Learning Hub provides students with personalized content that aligns with state standards. One of the shortcomings of the education system is that students, who learn at different speeds, are given the same assignments. Personalization has been a trend in the EdTech space because it helps students to learn content more quickly. Teachers, administrators, and parents have already given positive feedback on this product, so it represents an interesting opportunity for Stride to expand its business into more schools and states.

Career Readiness

This is the exciting part of the business with a strong value proposition, under-served customers, large TAM, and explosive growth.

Stride Inc. Investor Relations Page

{kind=link}

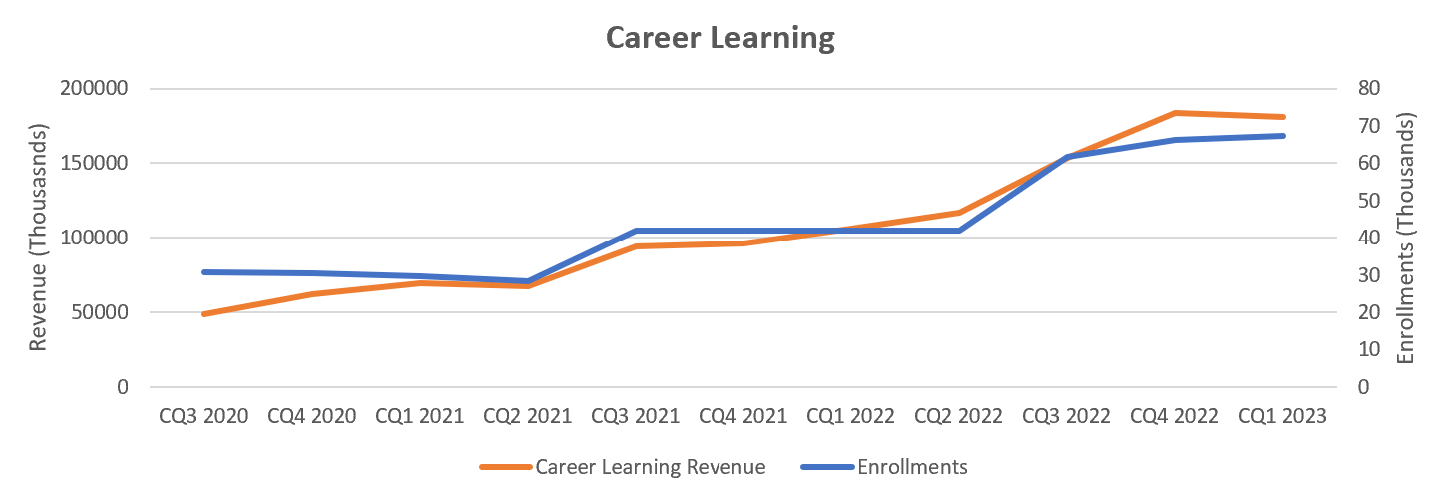

This part of the business has been growing in the high double-digits to triple digits range YoY thanks to its characteristics. Management can effectively market this service to schools due to its strong value proposition. For example, in a survey referenced during Stride's latest conference call , 30% of respondents rated their school's career preparation as satisfactory, 44% indicated that schools only taught basic computing skills, and 37% reported that their school education did not equip them with the necessary technical skills for their intended careers.

As a result, there is significant demand for Galvanize and Tech Elevator, which are software engineering boot camps, and MedCerts, which offers IT training. Furthermore, Stride's programs offer certifications, badges, and credentials. Parents are likely to support these programs because they lead to job placement.

Another opportunity for Stride is the platform Tallo that is currently being developed. Tallo is a platform that connects students to employers who are hiring for entry-level positions. Stride is creating a unique ecosystem where they train and credential their students, who then get hired by companies. Although this opportunity is promising, Tallo appears to be underdeveloped based on the number of job postings on its website.

Favorable Trends/Tailwinds

FQ3 Earnings

Although Stride’s enrollments are down 20+% YoY due to Covid restrictions easing, management has reported relatively strong demand in Q3. Additionally, management has expressed optimism regarding fall enrollments, and their FY2025 guidance indicates a strong outlook. During Stride’s FQ3 conference call, it was also noted that Stride is “tightening its belt”, resulting in 50bps of gross margin expansion.

Macro Environment

Stride is an excellent business to buy given the uncertain macro environment and its 5-year beta of 0.32. The Conference Board currently projects a recession, core inflation has remained high, and the Fed has voiced numerous times that it is taking a data-driven approach (meaning rates will remain high). As a result, the probability of a soft landing seems to have declined. This means that holding low-beta stocks, as insurance against a recession, makes sense right now.

Stride’s low beta is a result of its business fundamentals. Contracts with schools are typically for five or more years , resulting in predictable, recurring revenues. School funding, which Stride relies on, tends to grow at 1-2% per year. Additionally, the adult upskilling/reskilling portion of Stride’s business is arguably a negative beta business because more people may choose to upskill or reskill when laid off during a recession.

Despite having a 0.32 beta, my DCF in this article reveals that Stride is priced like a business with a 1.6 beta. My belief is that investors are predominately using multiples to value Stride, which has the effect of ignoring beta because comparable analysis tables typically don’t include beta. If investors are ignoring beta in their valuations, in a sense, investors are getting a “free insurance policy” against macro risk (stocks with low beta should be more expensive, but Stride is not)

Barriers to Entry

Stride indirectly receives state funds, exposing the company to substantial state regulation and scrutiny. Plus, state laws tend to be different, adding to the complexity of entering the education space. Thanks to the factors just mentioned, consolidation is more likely to occur than fragmentation, resulting in fewer competitors and higher operating margins. Stride also mentioned, in its latest conference call, that it is very open to M&A: management recently stated that it's monitoring a robust pipeline of companies. This causes me to believe that Stride is positioning itself as an industry leader.

General Tailwinds

- The Society for Human Resource Management has reported that companies are increasing budgets for upskilling and reskilling their existing workforce

- Artificial intelligence has the potential to displace workers, forcing them to reskill

- Stride’s general curriculum offering has the potential to alleviate teacher shortages

Valuation

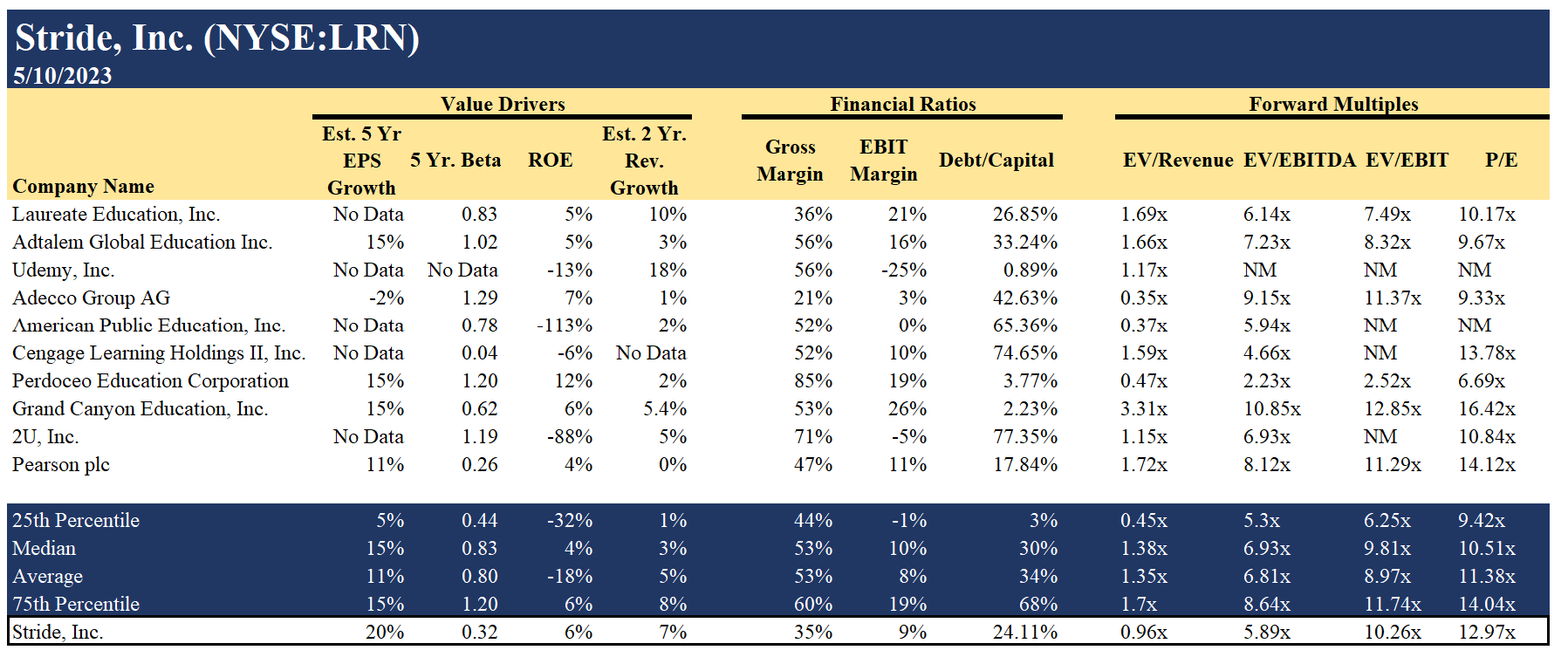

Comparable Analysis

{kind=link}

Commentary:

Considering Stride’s low beta and above-average revenue growth, Stride should be trading at the 75 th percentile Forward EV/Sales ratio ($59.20). However, I would argue that relative valuation techniques do not price in Stride’s consistent, long-term growth and low beta, meaning that more emphasis should be placed on DCF models.

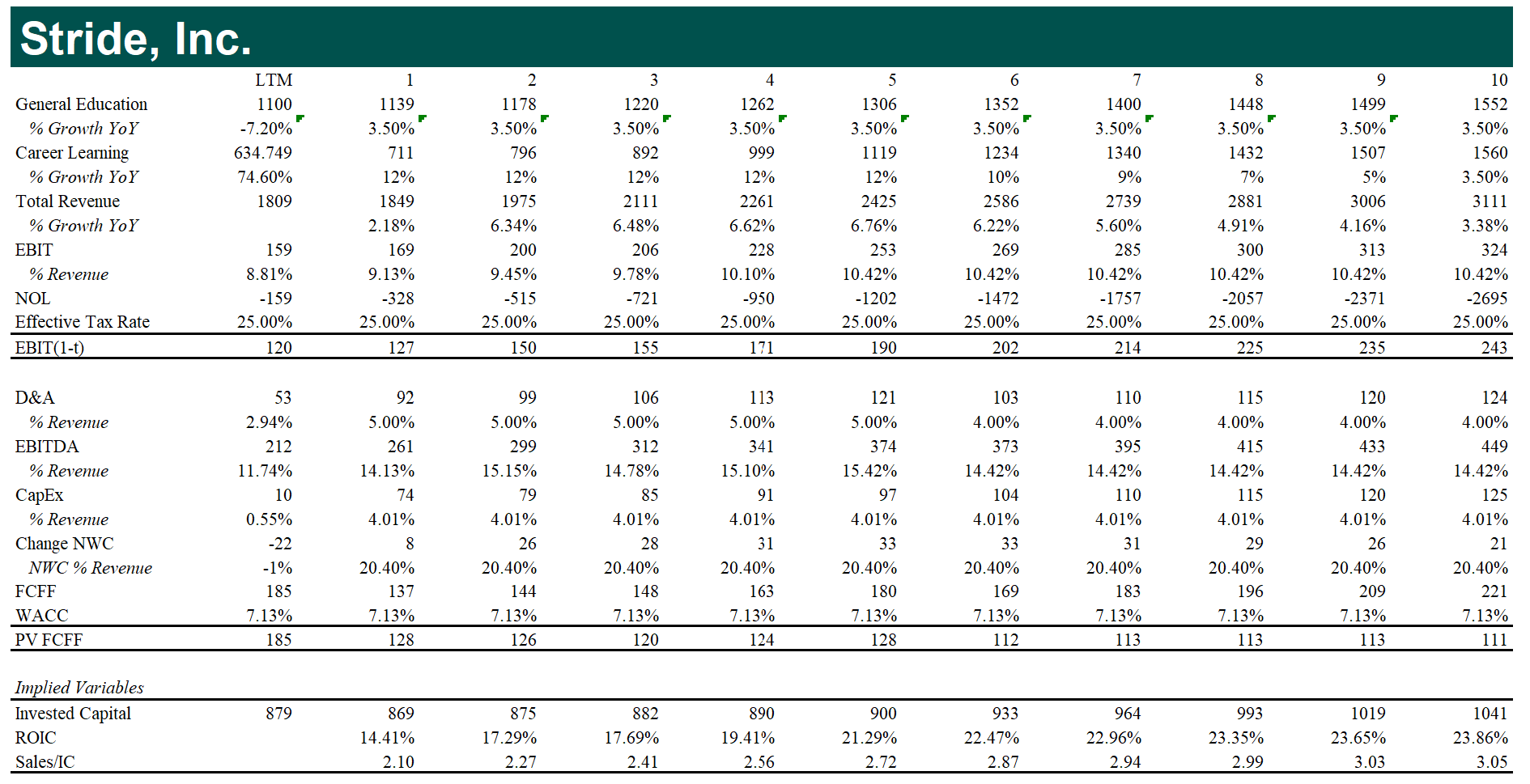

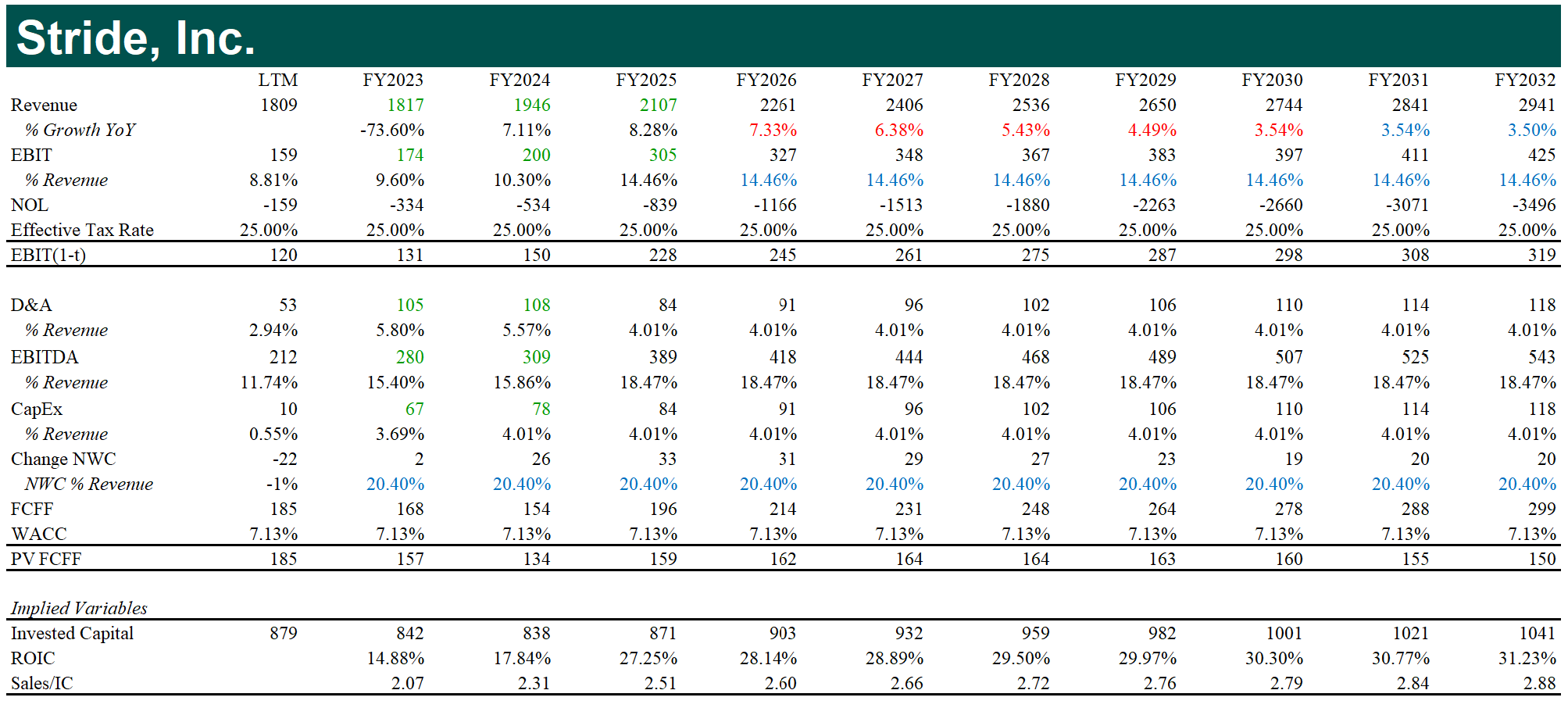

DCF #1: Base Case

{kind=link}

{kind=link}

Note: All analyst estimates were taken from S&P Capital IQ

General Education Revenue:

COVID adjustment : Pre-Covid revenue (CQ2 2019 through CQ1 2020) was 923.6 million dollars. This number must be adjusted 13.27% upward for inflation (the core PCE index was 113 at the start of 2020 and is currently at 128, a 13.27% increase). Ex-Covid enrollments also seem to be slightly higher: enrollments during CQ1 2020 were 108.9 thousand whereas enrollments during CQ1 2023 were 114.6 (an increase of 5.23%). I am attributing this to Stride “getting its foot in the door” because Stride was able to add 11 schools, during Covid, to its general education business (Stride was used in 76 schools during the 2019-2020 school year but was used in 87 schools during the 2022-2023 school year, representing a 14.47% increase). Adjusting 923.6 million for inflation and persistent enrollment growth leads to 1.1B in revenue for the general education business – this is what I kept for the base year (LTM; actual was 1.17B).

Year 1 – Year 10 revenue growth : I kept this at the risk-free rate (10-year T-Bond) which is a proxy for the growth rate of the economy (taught by Professor Damodaran). This assumes that the general education business is mature. Looking at historical school growth, the general education business has grown very little.

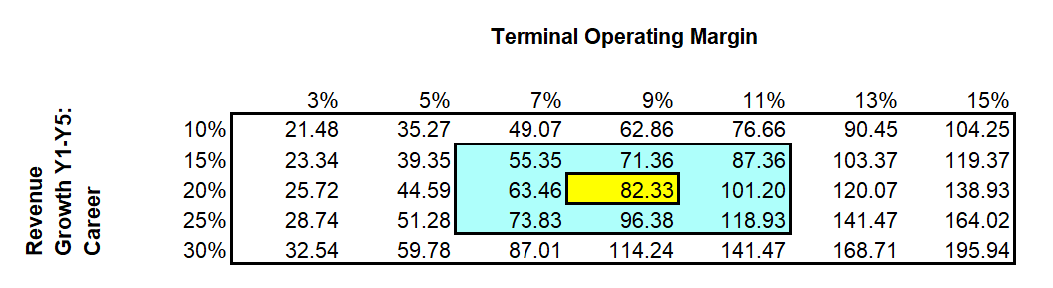

Career learning revenue : Career learning revenue grows at a constant rate for years 1-5. Then the growth rate moves linearly downwards towards the economy's growth rate over 5 years. I chose 12% because the revenues of the career learning business end up converging with the revenues of the general education business. This makes sense because Stride can cross-sell its career learning services to the schools where it already sells general education services. This assumption is probably on the conservative side, so I included a sensitivity analysis in the risks section of this report.

EBIT margins : Operating margins move linearly towards the median operating margin of Stride’s peer group as the firm matures. A sensitivity analysis is provided later in this report.

Capital expenditures : Capital expenditures are 4% of revenue because that is what analysts are roughly predicting for CY2024 and CY2025. This makes sense because Stride is pursuing organic growth with multiple internal projects. 4% is meaningfully above Stride’s historic average of 1% of revenue being spent on capital expenditures.

D&A : D&A being 5% of revenue is roughly what analysts are predicting for CY2024 and CY2025. D&A stays at 5% for 5 years but then declines to 4% of revenue for the last 5 years because D&A should not be greater than capital expenditures in the long run.

Net Working Capital : I used the 5-year historical average NWC/Revenue ratio. NWC for each year is (Change in Revenue)*(NWC/Revenue).

Terminal Return on Invested Capital ((ROIC)) : I added 2.5% to the cost of capital because I believe that Stride will emerge as a major player once the industry begins to consolidate. Usually, 2.5% indicates that companies have some competitive advantages.

Terminal Value: ((EBIT*(1-t)*(1-RIR)*(1+g))/(WACC-g)

t – tax rate (25%, the average global corporate tax rate)

g – growth rate (Risk-free rate)

RIR – reinvestment rate (g/ROIC)

Terminal Growth Rate: Risk-free rate (how Aswath Damodaran teaches valuation. The risk-free rate is known as a proxy for the growth rate of the economy)

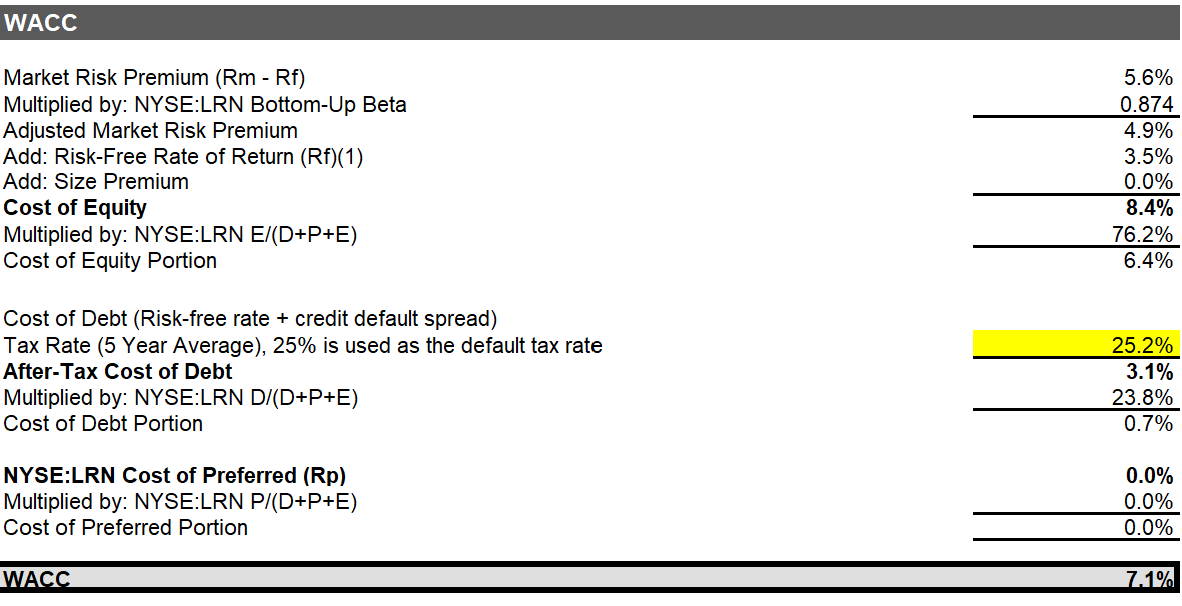

WACC:

Equity risk premium: I use Professor Aswath Damodaran’s implied ERP which can be found on his website.

Cost of debt: I added the AAA corporate bond credit spread to the 10-year t-bond rate. The AAA rating is based on Stride’s excellent interest coverage ratio.

{kind=link}

{kind=link}

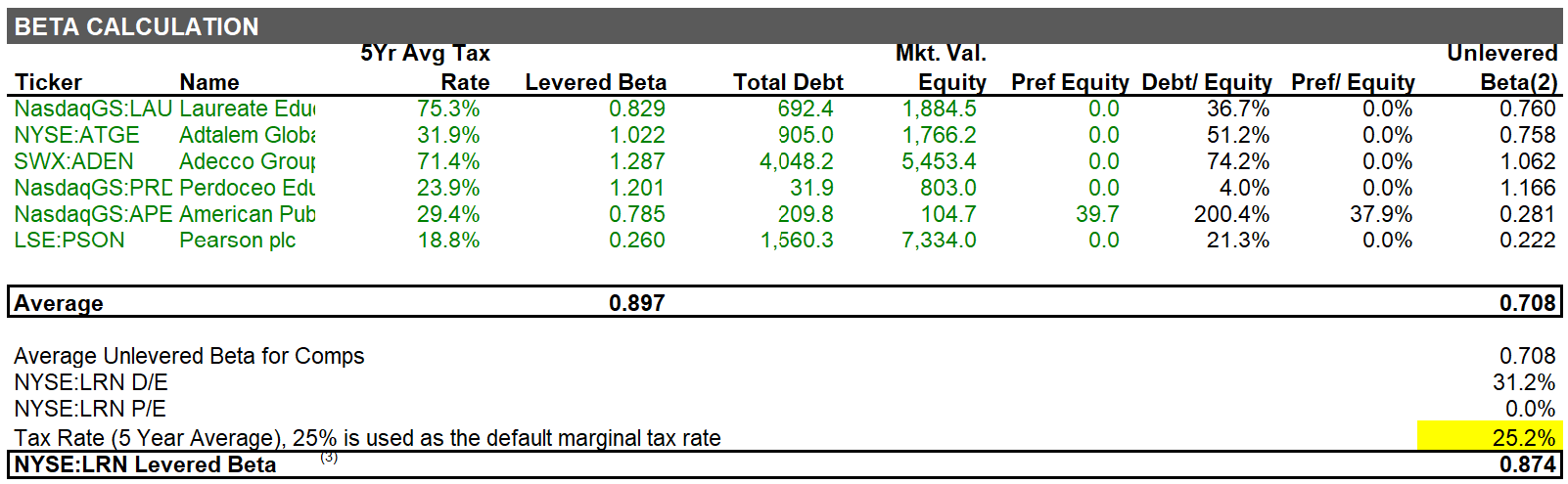

I used a bottom-up beta to be more conservative. Using Stride’s 5-year beta yields an estimated stock price of $178/share. It’s also worth noting that Stride’s stock is still worth $44.24 when the beta rises to 1.6.

DCF #2: Analyst/Management

{kind=link}

{kind=link}

Revenue: Management claims that Stride will generate between $1.9B-$2.2B in revenues during FY2025. Analysts are estimating $2.1B in revenues (slightly above the midpoint of the range). This model uses analyst estimates for FY2023-FY2025. Then, the revenue growth rate moves linearly towards the economy's growth rate over five years to account for Stride becoming a mature company.

EBIT Margins: Analysts estimate 305 million in EBIT during 2025, which is roughly the midpoint of management's guidance (250M-350M). I then keep the operating margin flat in perpetuity.

Capital Expenditures: I use analyst estimates for FY2024 and FY2025. For 2026-2032, I use the 2025 CapEx/Revenue ratio which reflects management investing in internal projects.

D&A: I use analyst estimates for FY2024 and FY2025. For 2026-2032, I use the 2025 CapEx/Revenue ratio because D&A should not exceed CapEx in perpetuity.

Net working capital: Same as last DCF.

WACC: Same as last DCF.

Catalysts

Investors are pricing Stride like a company with no growth. Over the next few quarters, the revenues and enrollments for the General Curriculum business will stabilize, resulting in more favorable YoY comparisons (enrollments were down 20% YoY for FQ3). Simultaneously, the career learning part of Stride will continue to expand, resulting in annual revenue growth of 6.5%+. My view is that investors have been focusing on enrollments declining rather than the Career Learning part of Stride expanding, so enrollments stabilizing should shift investor attention to the growing Career Learning business, resulting in its growth being priced in.

It’s also worth noting that the Career Learning part of Stride’s business used to be 10-20% of Stride’s revenue. Now that it has grown to ~40%, investors will start paying attention to it.

Risks

1. The career learning portion of Stride’s business faces competition from Pearson’s new offering, Connections Academy.

When questioned about this during the latest conference call, management pushed back, stating that there is room for multiple players. Additionally, they insisted that the inclusion of more players could be advantageous as it would enhance the awareness and validity of their services.

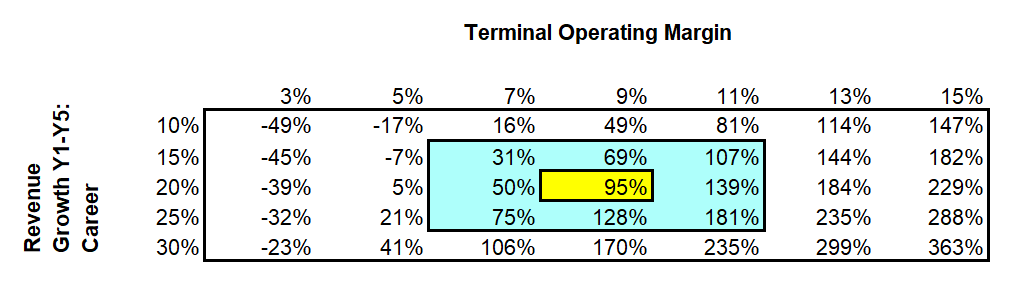

2. Operating margins

Operating margins have historically been in the 3-5% range, but appear to have expanded after Stride acquired MedCerts, Tech Elevator, and Galvanize. TTM margins are currently 8.81%, so margins reverting to their historical average would result in downside. However, significant margin compression does not make sense given management’s strong guidance (~14% operating margins during FY2025).

{kind=link}

{kind=link}

Conclusion

Stride’s current risk/reward profile is attractive because it's trading well below its intrinsic value. Plus, Stride is a great stock to hold, given the current macro environment, because its low beta provides investors with an "insurance policy" against a recession. Strong growth in the near term, excellent fundamentals, and promising internal projects will likely propel Stride’s stock price forward over the next 5 years.

For further details see:

Stride: Rock Bottom Valuation And Insurance Against Macro