GM - Strike May Last Longer But Stellantis Will Be Fine

2023-09-28 11:14:45 ET

Summary

- Stellantis N.V. is best positioned to absorb the impacts of the UAW strike among the big three.

- Key factors include its more diversified product portfolio and geographical exposure, which can help mitigate the impact of a prolonged strike.

- Stellantis also has higher profitability and stronger financial strength, thus is better poised to fund the transition to EVs and absorb the costs of the strike.

- Cheaper valuation adds another layer of margin of safety.

- The dividend may be cut, though, both to preserve cash and to simply avoid a bad image.

STLA: better positioned to absorb strike impacts

The United Auto Workers (“UAW”) continues to and may even further expand its scope against the three big automakers in Detroit. In my view, it is a very likely scenario that the UAW strike can expand and also last longer than expected. At a fundamental level, the gap between the two parties is just too big currently. At a practical level, the UAW has a strong strike fund to keep paying eligible members $500 per week for up to 11 weeks. The UAW also has a history of long strikes. The 40-day strike against GM in 2019 is a recent example.

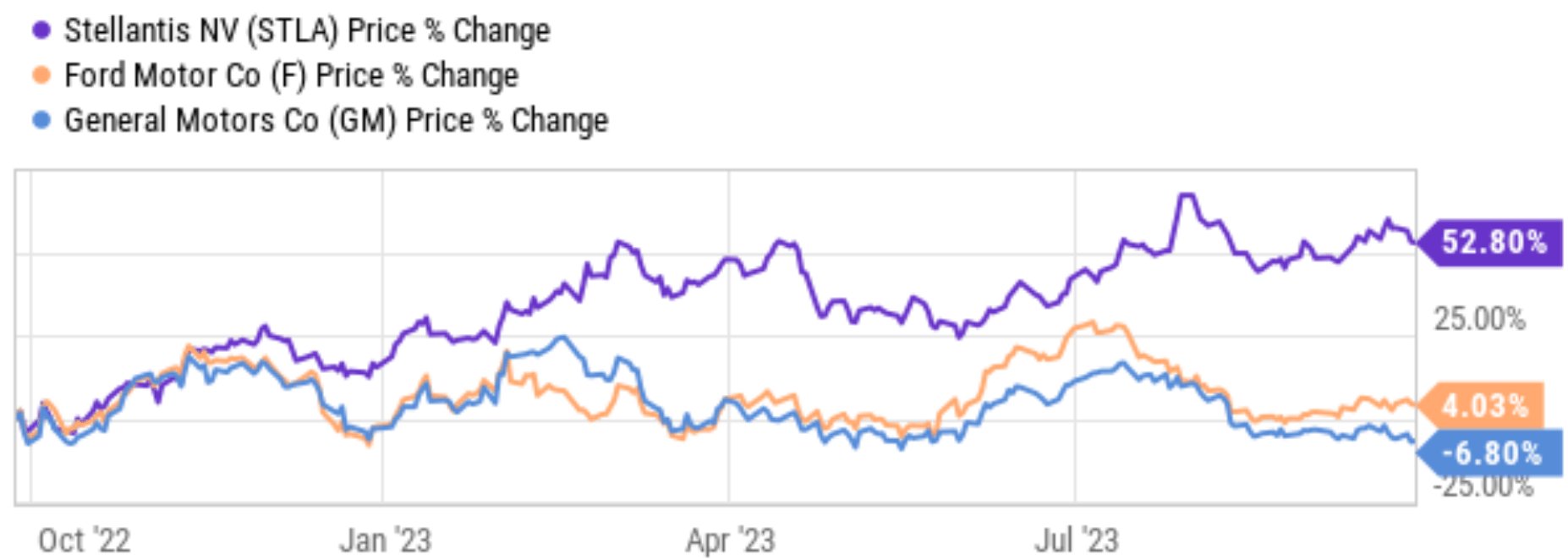

Under this context, the goal of this article is to show why Stellantis N.V. ( STLA ) is better positioned, probably best positioned, among the big three to absorb the impacts from the strike. The top considerations are Stellantis’ more diversified product portfolio, more diversified geographical exposure, and also stronger financial position. I will detail my arguments in the rest of the article. Here I just want to quickly point out that the stock price reactions reflect these strengths, in my view. As you see from the chart below, stock prices from all three automakers have been under large selling pressure since July when the negotiations started and the possibility of a strike emerged. However, STLA’s stock prices have shown the best resilience, and its total returns YTD actually outperformed the S&P 500 (SP500) by a large margin.

{kind=link}

Why is STLA better positioned?

As just mentioned, I think STLA is in a better position to absorb the impact of the strike compared to the other two. The top two considerations in my mind are Stellantis’ more diversified product portfolio and more diversified geographical exposure. STLA produces a wider range of vehicles than Ford (F) and General Motors (GM), including commercial vehicles, Jeeps, and luxury cars. This diversification could help to mitigate the impact of a prolonged strike on any one particular product line. The company was the result of a merger of Peugeot and Fiat Chrysler back in 2021. As such, STLA has a stronger presence in Europe than both F and GM. Currently, it is one of the largest automakers in Europe and operates a number of manufacturing plants there. This European presence could help to offset any lost production from North American plants due to the strike.

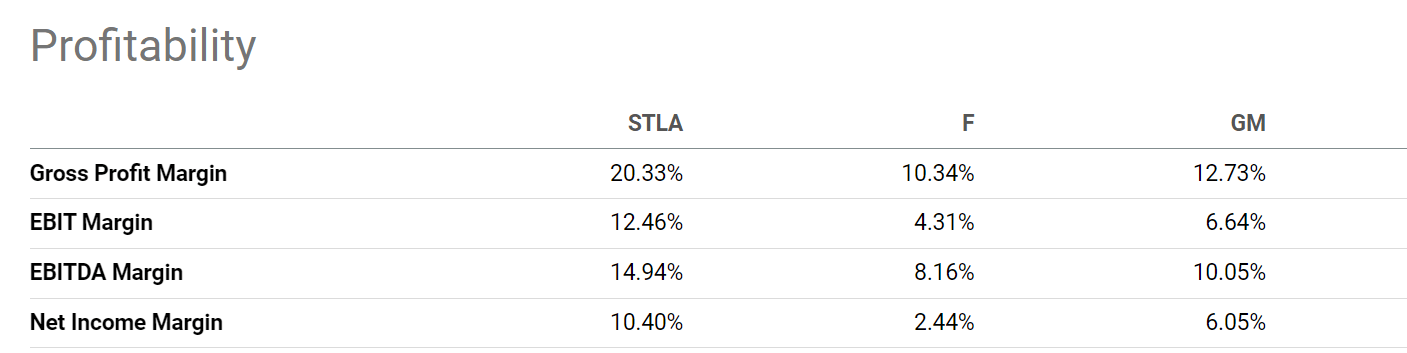

Thanks to the diversified product line and geographical exposure, STLA has been enjoying much better margins to respond to the demands from the UAW. As an example, the chart below compares the profitability of the three big automakers in terms of their margins (from Gross Profit Margin all the way to the Net Income Margin). As seen, Stellantis’ margins are not only the highest of the three automakers but also higher than the other two by a large degree. Its Gross Profit Margin of 20.3% is almost double that of the other two. And its Net Margin is about 4x higher than F.

{kind=link}

Stronger financial position

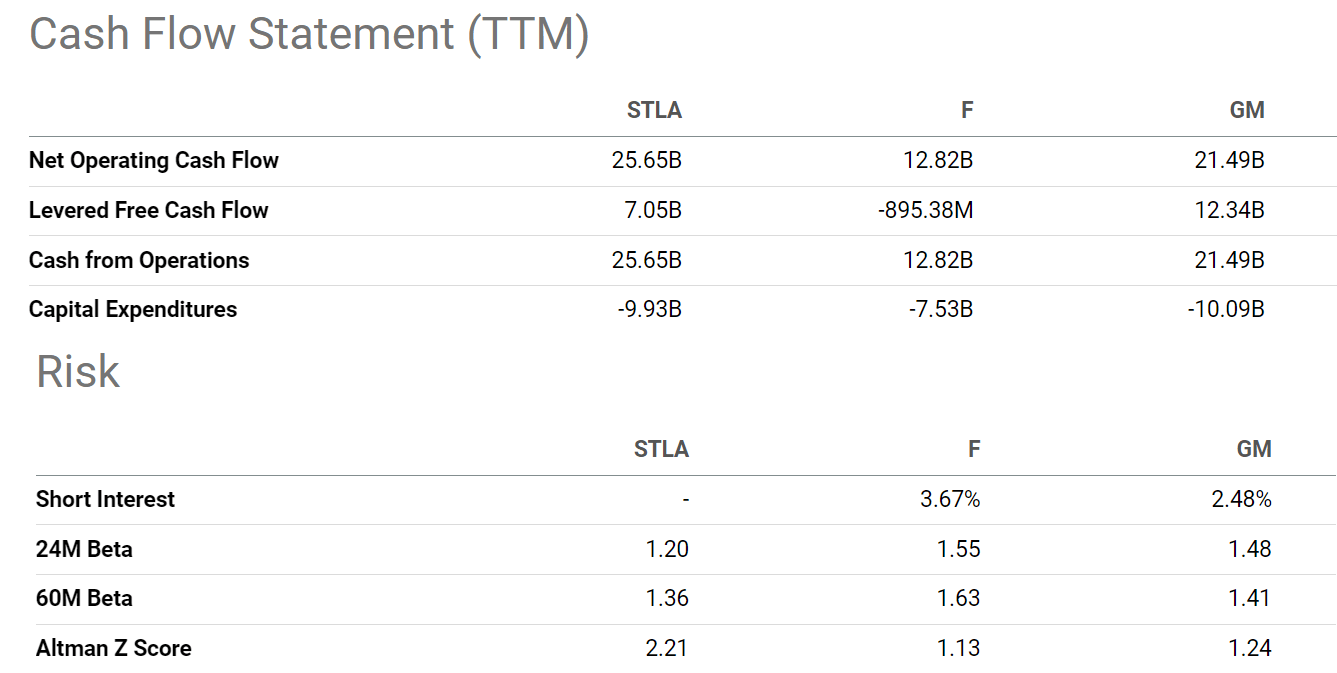

Thanks to its superior profitability, the company is also in a better position to fund the CAPEX requirements for the transition to the electric vehicle ("EV") future. As shown in the top panel from the chart below, STLA generated a total of $25.65 billion net operating cash flow (“OCF”) in the trailing twelve months and spent $9.93 billion on capital expenditures, translating into about 38% of its net OCF. In contrast, both F and GM have a much larger fraction of their OCF on CAPEX. Finally, as seen in the bottom panel of the chart, overall, STLA is also in a strong financial position as reflected in its higher Altman Z-score. Its Altman Z-score is 2.21, almost double that of F and GM (1.13 and 2.24, respectively). For readers new to the concept, the rule of thumb for manufacturing businesses is that an Altman Z-score above 2~3 indicates solid financial strength (and close to zero signals nonnegligible bankruptcy risks).

{kind=link}

Valuation, other risks, and final thoughts

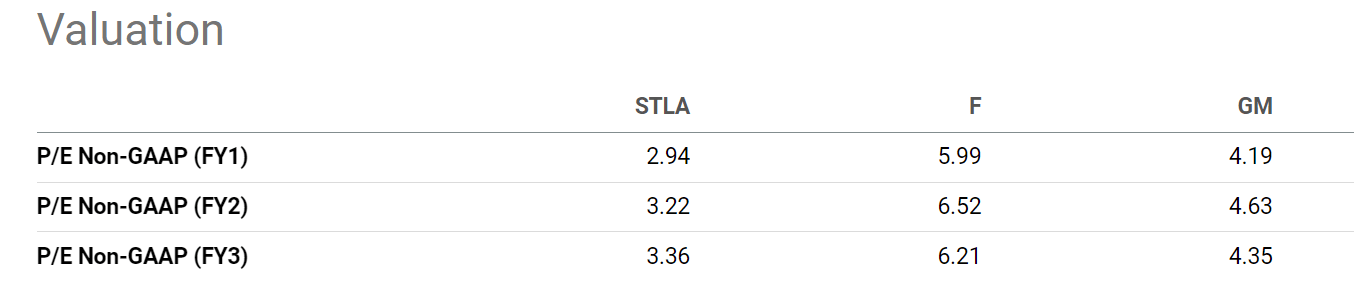

Besides the considerations mentioned above, the stock’s current valuation is also the lowest among the three. Its FY1 P/E is only 2.94x as seen in the next chart. It is cheap both in absolute and relative terms. Its P/E is discounted from F (FY1 P/E of ~6x) by more than 50% and discounted from GM (FY1 P/E of ~4.19x) by about 30%. Yet STAL enjoys better profitability and stronger financial strength as my results have shown above. The large gap between its P/E multiples and fundamentals provides a wide margin of safety.

{kind=link}

Finally, there are some downside risks to be considered too. The ongoing strike is of course the most imminent risk. I expect STLA will have to meet some, if not all, of the UAW’s demands eventually. This will then lead to higher costs and compressed margins for STLA. According to this Bloomberg report, the union’s demands as they are would increase the costs by $80+ billion for EACH of the three big automakers. As such, STLA may be the one best positioned to absorb the impacts, such a large increase in its costs could make it less competitive against foreign automakers and non-unionized domestic players like Tesla (TSLA).

Besides the potential impacts of the strike, STLA also faces a few other risks. The transition to EVs is the main one. STLA is investing heavily in EVs, but it is playing catch up in my view against pure EV players like Tesla. Its transition faces many complex and challenging issues, ranging from technical issues to the development of infrastructure.

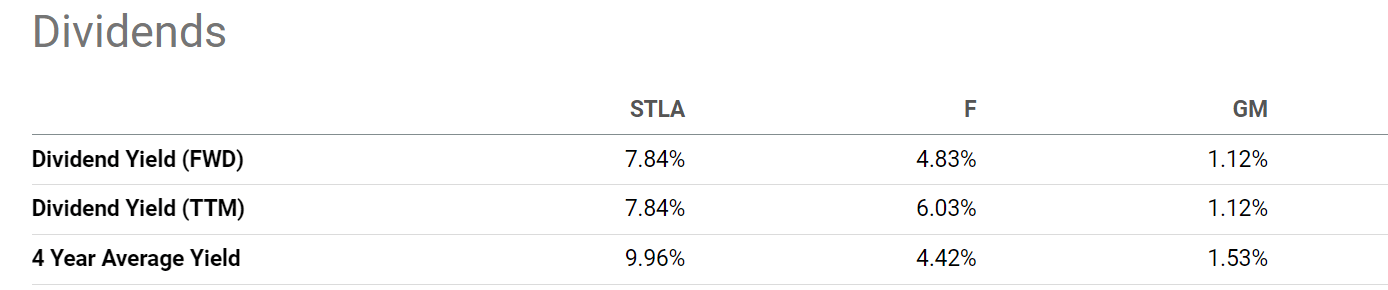

One last risk – its dividend. For investors drawn to its generous dividend, I see good reasons for STLA to cut its dividend as a result of the autoworker strike. As seen in the chart below, STLA currently has the highest dividend yield of the three automakers with an FWD Dividend Yield of 7.84%. As mentioned, the strike is likely to have a large impact on its cost and thus cutting the dividend could help the company to conserve cash. Furthermore, I view it as simply a bad political image to keep paying generous dividends to shareholders while maintaining a tough position with the union workers at the same time.

All told, I see a few reasons for the scope of the strike to expand and its duration to persist longer. As such, there is no doubt in my mind that all three automakers will have to meet some, if not all, of the demands of the union workers. However, I view STLA as the one best positioned among the big three to absorb the impacts. To reiterate, the main factors in my thesis are STLA’s more diversified product lineup, more diversified geographical exposure, and also stronger profitability and financial strength.

{kind=link}

For further details see:

Strike May Last Longer, But Stellantis Will Be Fine