RUN - Sunrun: The Stock Can Triple Or Go To Zero But Risks Tilted To The Downside

2023-11-13 06:24:02 ET

Summary

- Sunrun has experienced a significant deterioration in many KPIs, including negative growth in customer additions and a 1% growth in solar energy capacity installed from last quarter.

- Due to a sharp slowdown in solar demand, the company is facing a persistent growth decline in its total revenue going into FY2024, coupled with negative EBIT and FCF.

- With $9.5 billion in net debt on its balance sheet and an interest expense accounting for 30% of total revenue in 3Q FY2023, the company is exposed to solvency risk.

- Despite a 60% YTD selloff, the stock's valuation remains expensive, trading at a premium multiple of 5.72x EV/Sales TTM, compared to its peers.

What Happened

Sunrun (RUN) has been underperforming in recent months, with a 60% YTD selloff compared to the iShares Global Clean Energy ETF (ICLN), which saw a 34% decline. Back in April, anticipating a potential growth slowdown due to NEM 3.0, I issued a sell rating on RUN. Since that time, the stock has declined by 55%. My primary concern revolves around the company's high leverage, making it exceptionally susceptible to a sharp decline in demand.

During the latest earnings release , RUN announced a reduction in its solar capacity growth for FY2023, scaling it back to low single digits from the previously projected double digits due to overall sluggish demand. While I maintain optimism regarding the company's long-term growth prospects, I expect persistent headwinds from the NEM 3.0 transition and weakened global demand for solar energy into 1H FY2024.

RUN has consistently been unprofitable, maintaining a negative balance in EBIT. This renders the stock particularly sensitive in the high rates backdrop. Furthermore, the company's balance sheet has continued to deteriorate, reaching a historic high of $9.5 billion in net debt. Therefore, I have downgraded the rating to Strong Sell, as the combination of weaker growth alongside a high leverage profile exposes the company to solvency risks as a very unprofitable company. In other words, this uncertainty creates the possibility of the stock either surging by 3x or plummeting to zero.

Negative Growth on Customer Additions

{kind=link}

In 3Q FY2023, RUN reported mixed earnings results . While beating non-GAAP EPS estimates, the company faced a growth headwind with a 10.9% YoY decline in total revenue, falling short of the consensus. The total customer additions for the last quarter saw a 5% YoY decline, marking the first negative YoY growth in the company's history.

Specifically, the Purchase Customers segment experienced a substantial 56% YoY drop and a 39% QoQ decline. The data shows a significant deceleration in demand growth for the company, at least in the near term.

Significant slowdown in Capacity Installed

{kind=link}

In addition, RUN has experienced a significant deceleration in Solar Energy Capacity Installed during 3Q FY2023, with growth narrowed to just 1% YoY, down sharply from the 20% growth in 2Q FY2023. I believe that the negative effects of NEM 3.0 have started to materialize and will be likely to persist over the next 2 to 3 quarters.

Looking at the 4Q guidance, the company expects a range of 220 to 245 megawatts for its capacity installed. Taking the mid-point of this range implies a growth rate of -15.6% YoY and -10% QoQ in 4Q FY2023. Moreover, the growth rate for FY2023 is expected to be only 2-3% YoY, indicating a significant slowdown from the robust 25% YoY growth in FY2022. Therefore, I believe the timing of the company's growth inflection and FCF breakeven may be pushed out even further due to the prevailing slowdown in demand for solar energy.

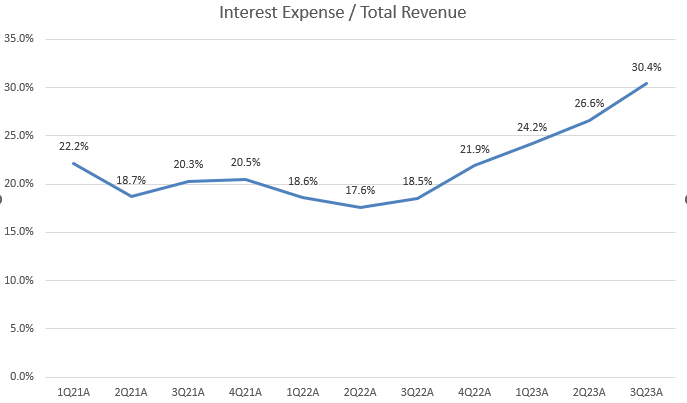

Interest Expense is 30% of Total Revenue

{kind=link}

RUN is a high-leverage company, and this high leverage exposes a significant downside risk, particularly when its top-line growth experiences a sharp decline. Given the persistent negative balance of EBIT over recent years, in a worst-case scenario, the company may confront solvency risk, potentially leading to bankruptcy and rendering the stock essentially worthless. Simply put, in the event of bankruptcy, the fair value of the stock approaches zero.

Due to the company's negative EBIT, calculating the interest coverage ratio is meaningless. So let's take a step back and look at the ratio on the chart, this indicates that the interest expense divided by total revenue reached 30.4% in 3Q FY2023, showing a continued expansion. I believe this is a warning sign for investors, especially considering that the interest expense grew by 46% YoY to $171 million, while the gross profit stands at only $45.2 million. This significant imbalance raises concerns about the company's financial stability and warrants careful consideration for long-term investors.

{kind=link}

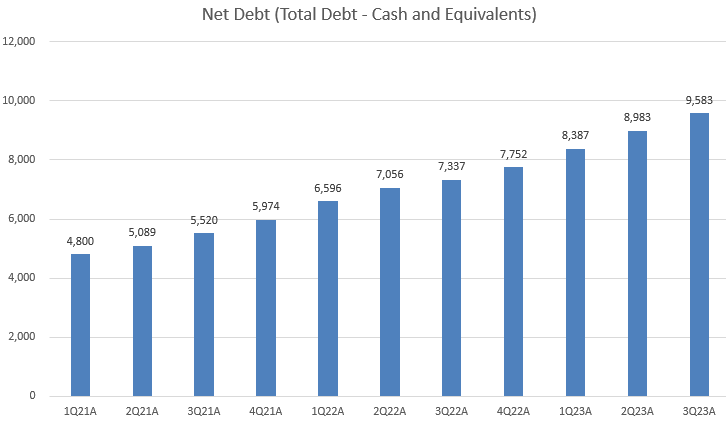

Additionally, RUN's net debt (total debt minus cash and equivalents) surged to $9.6 billion in the last quarter, marking a substantial 31% YoY increase. The company's debt-to-equity ratio for the same period stood at 1.5 which is very high considering the current macro backdrop. This high debt-to-equity ratio raises concerns, particularly given the potential implications of an extended demand slowdown.

Valuation

{kind=link}

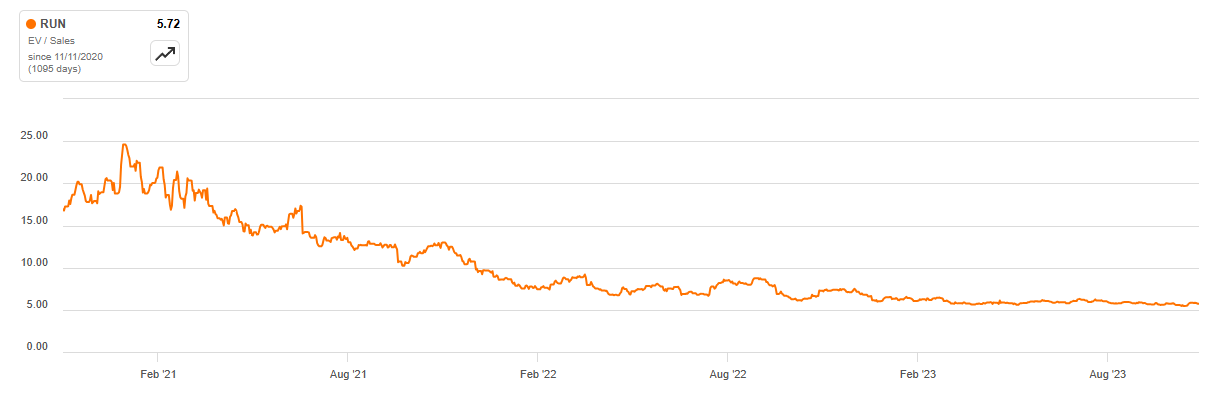

RUN is currently trading at 5.72x EV/Sales TTM, showing a significant contraction from the multiple in FY2021. Despite this contraction, the company's valuation remains high, particularly in terms of the potential negative YoY growth in FY2024 due to a significant slowdown in solar demand. This implies that its EV/Sales Fwd would be even higher than the current 5.72x. Particularly, according to Seeking Alpha Valuation , this multiple is 250% higher than the sector median, which includes First Solar (FSLR) at 3.74x. This indicates that the stock is still very expensive.

Although the EV/Sales Fwd is currently 29% below its 5-year average, investors should still be cautious. The significant deceleration in growth and the looming potential solvency risk justifies a lower valuation multiple. It is crucial to recognize that, despite RUN's potential for long-term growth, the stock's value would be wiped out if the company fails to navigate the near-term growth headwinds. Personally, I choose to stay away from high-leverage companies currently grappling with significant growth headwinds, even if their valuations seem appealing from a risk and reward perspective.

Conclusion

In summary, Sunrun faces substantial challenges as evidenced by its 60% YTD decline and a range of financial indicators highlighting vulnerability. The company's high leverage, negative EBIT, and significant increase in net debt raise concerns about potential solvency risks, particularly if the current demand slowdown persists. Despite a forward EV/Sales multiple below its 5-year average, caution is still warranted given the significant growth slowdown, making the stock still 250% expensive compared to the sector median. Therefore, I downgraded the stock to "Strong Sell". Investors should be very careful about the potential solvency risk, considering the company's ability to navigate near-term challenges, as failure to do so may render the stock essentially worthless, despite seemingly attractive valuations.

For further details see:

Sunrun: The Stock Can Triple Or Go To Zero, But Risks Tilted To The Downside