SURG - SurgePays Looks Ready To Scale

2023-06-16 17:54:47 ET

Summary

- SurgePays focuses on underbanked communities, offering prepaid financial services and mobile broadband, and plans to expand its network of partner shops.

- The company turned profitable in Q1 2023 and aims to grow from 8,000 stores to have 13,000 stores by the end of 2023 and 25,000 by 2024.

- I believe the stock is undervalued as the market is still focused on historical results and not pricing in the benefits of scale that management has guided for 2023.

SurgePays, Inc. ( SURG ) is a technology and telecommunications company focused on the underbanked and underserved communities. The company offers a comprehensive suite of prepaid financial services, including mobile broadband through SurgePhone Wireless, as well as prepaid debit cards and other payment solutions.

The company's revenue streams come from two main sources: customer fees for its products and services, such as monthly subscription fees for its mobile broadband service, and royalties from its network of partner shops. SurgePays also has plans to expand its network of partner shops in order to create a bit of a virtuous cycle that will help drive more customers to their products and services.

After being held back by supply chain issues in 2022, SurgePays has set itself up to scale rapidly, planning to more than double its presence in low-income neighborhoods while increasing profitability. The benefits of scale were already beginning to show in Q1 2023 results as the company turned profitable, both in EBITDA and Net Income. I believe the stock is undervalued as the market is still focused on historical results and not pricing in the benefits of scale that management has guided (and started delivering on) for 2023.

Driving Scale Through The "Corner Store"

SurgePays has driven most of its growth by leveraging the Affordable Connectivity Program . The ACP is a federal initiative in the United States to provide affordable internet access to low-income households. The program offers a $30 monthly subsidy to eligible families to help offset the cost of broadband service provided by participating internet service providers. In addition, the program provides a one-time discount of up to $100 for a laptop, tablet, or desktop computer purchased through a participating retailer.

SurgePays offers its services to consumers through neighborhood convenience stores, which is the cornerstone of its strategy to scale. As discussed in the Q1 2023 earnings call , SurgePays has 8,000 stores online now and expects to have 13,000 by the end of 2023. They are also staging to have 25,000 stores by the end of 2024.

Management noted in the Q1 2023 earnings press release that growth in 2022 stagnated due to supply chain issues with the tablets SurgePays provides convenience store owners. The supply chain issue was resolved, and SurgePays has also cut the cost of tablets by almost half, setting the company up to onboard thousands of retailers this year. In addition, management noted that they resolved supply chain issues with pre-paid mobile devices, allowing them to onboard customers to pre-paid plans with "unthrottled sales capacity." This explains why 2023 performance and scale will look so different from the stagnant performance in 2022.

EBITDA Has Turned A Corner And Continues To Improve

SurgePays turned profitable in Q1 2023 on $34.8 million in revenue, posting a net income of $4.5 million and EBITDA of $5.0 million. This was an eye-popping improvement from the full year 2022 which generated a net income of ($0.7) million and EBITDA of $1.6 million.

In the Q1 2023 earnings release, management provided revenue guidance for 2023 of $190 million or roughly $47.5M per quarter. Since Q1 was only $34.8 million, the growth is heavily backloaded, as management confirmed in the earnings call. While they wouldn't provide specific EBITDA guidance, they indicated in the earnings discussion that it would scale at a similar rate from Q4 2022 to Q1 2023. This would give an EBITDA range of $26 to $30 million across the full year or a 14-16% margin at the low end.

Valuation Multiples Don't Reflect Growth Trajectory

Given the rapid growth and quick turn to profitability, you would expect fairly strong valuation multiples. However, that is not at all the case. The Wireless Telecommunications Sector overall is made up of more mature, slower-growing companies. Yet, SurgePays has a P/E ratio of 60% below the sector, an EV / Sales ratio of 69% below the sector, and an EV / EBITDA ratio of 29% below the sector. Depressed valuations made sense in 2022 as growth stagnated, but the market has not reacted to the business momentum in 2023.

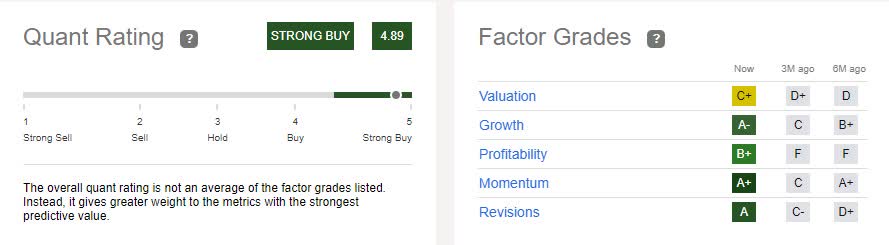

Looking at the quant ratings, SurgePays is given a Strong Buy rating even with the company having just turned profitable. As discussed above, momentum and growth ratings are especially strong, with valuation lagging.

{kind=link}

Downside Potential

First and foremost, relying on government programs is always tricky. If funding for the ACP program is cut by future legislation, it could have an effect on SurgePays’ customer base and revenue.

Second, there are numerous competitors in the market. SurgePays may be one of the frontrunners now, but that doesn’t mean they won’t face increased competition soon. It will be important to keep up with technological advances and maintain strong customer relationships to avoid being outpaced.

Lastly, the success of SurgePays is highly dependent on its ability to scale rapidly. If they are unable to recruit new stores successfully and hit their target of 25,000 stores, then their revenue and profitability could be impacted.

Verdict

SurgePays has taken a unique approach to scaling by focusing on neighborhood convenience stores and has already seen success with its 8,000 stores online. They will have 13,000 stores by the end of 2023 and 25,000 by 2024. Profitability is improving as well, with improved EBITDA and revenue growth. Valuation multiples are very depressed for a company driving this type of profitability, making it an attractive investment opportunity. However, there are risks to be aware of, particularly in relying on government programs and the potential for increased competition.

Despite the risks, I believe that the stock is undervalued as the market hasn't given SurgePays credit for its demonstrated ability to scale and the profitability improvements in the Q1 2023 results. I rate this stock a buy, as I think the growth potential and momentum in 2023 outweigh the long-term risks.

For further details see:

SurgePays Looks Ready To Scale