CS - SVB Financial Preferred And Common: Potential Value In The Wreckage

2023-06-06 15:39:03 ET

Summary

- The potential recovery of $2.2 billion of cash held by the FDIC provides the bulk of recovery to the bonds.

- Other sources of recovery include a portfolio of securities, warrants in venture companies, the investment bank, and the asset management division.

- NOLs (net operating losses) would also provide future value.

- If the value pool is large enough, preferred holders can see 4x or higher returns.

- It's possible there's value even in the common shares.

Update on SVB Financial Bankruptcy

SVB Financial ( OTCPK:SIVBQ ) the former parent of Silicon Valley Bank has been a fascinating bankruptcy situation to watch. I have stayed mostly on the sidelines since the FDIC took over the bank three months after my December short recommendation, "SVB Financial: Blow Up Risk. " Recent developments, however, have drawn me back in.

Bankruptcy proceedings are very procedure heavy and can get very complicated with a huge amount of nuanced interpretations of valuation. As holders of Credit Suisse ( CS ) AT1 securities discovered, a single sentence in a prospectus can have huge consequences for recovery value.

SVB Financial's bankruptcy is simpler than most bankruptcies, but not without a few wrinkles. Let's start with the general structure of the Holdco and its assets versus liabilities.

SVB Financial was a holding company that owned four businesses.

- Silicon Valley Bank--Taken over by the FDIC and sold to First Citizens (FCNCA).

- SVB Securities--Investment bank bought in 2019 for $280mm, in process of being sold.

- SVB Capital--A $9.5 billion asset management business.

- Boston Private Capital--A wealth management business that was part of the sale of Silicon Valley Bank.

There are also assets in the form of securities and warrants held, and perhaps most importantly, NOLs (net operating losses) generated by the loss equity of Silicon Valley Bank.

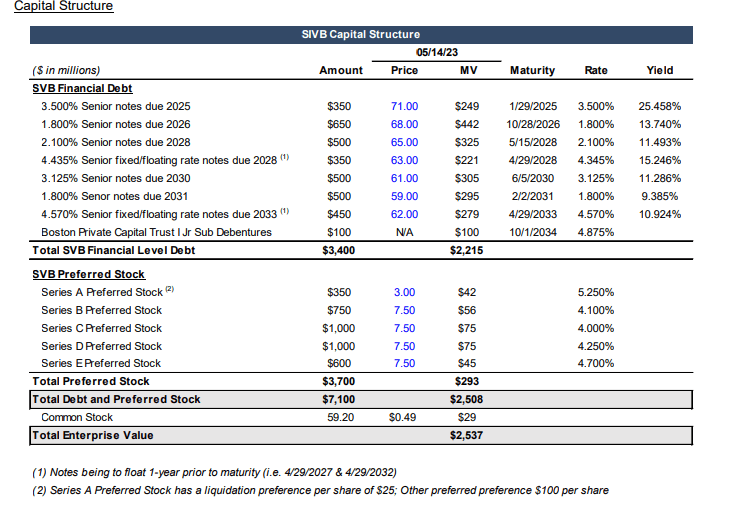

Its capital structure is as follows:

{kind=link}

Sometimes it helps to see assets and liabilities side by side, the breakdown is as follows:

| Assets |

| Par Value |

| Liabilities |

| Value |

| Holdco Cash |

| $2.1 billion |

| Senior Unsecured Notes |

| $3.3 billion |

| NOL's (Net Operating Losses) |

| $16 billion (PV of ~$3 billion) |

| Preferred Stock |

| $3.7 billion |

| SVB Securities |

| Estimated Value $200-$500 million |

| Boston Private Trust Debentures |

| $100 million |

| Asset Management |

| $9.8 billion AUM with a $450 million stake. |

| FDIC (contingent Claim) |

| ? |

| Investment Securities |

| $92.8 million (monetized) |

| Equity Securities |

| $313 (using 25% discount vs. 12/31/22) |

| Equity Warrants |

| $300 million (using 25% discount vs. 12/31/22) |

The biggest uncertainty right now is the $2.1 billion of SVB Financial holdco cash that is currently held by the FDIC. The FDIC has taken the position that the cash belongs to it, since it suffered $16 billion of losses in Silicon Valley Bank's failure. This position seems highly untenable as the FDIC guaranteed all deposits and the holdco cash counts as a regular deposit. This cash is the crux of most of the value here. There is a very small risk, however, that the FDIC wins. If that happens, all bets are off.

Barring that small risk, there is a lot of potential value here. There are two main camps. One group, composed of bondholders, (bonds are trading in the high 60s to low 70s, a little over $2 billion of market value) is arguing that this is a liquidation scenario and there is only enough value to satisfy the bonds. In that situation, preferred and common shareholders are wiped out and bondholders receive all of the proceeds from the liquidation of the estate. In my opinion, this position is fairly flimsy.

Another camp, made up mostly of preferred holders, is arguing that there is enough value to satisfy bondholder claims and that preferred holders receive the residual equity value. The bulk of the argument for that case is that the warrants and NOL values can offer a lot of upside even if the bulk of the liquid assets goes to bondholders. Preferred shares trade $.07-.08 on the dollar in the over the counter market (about $300 million market value) and the listed preferred shares ( OTCPK:SIVPQ ) trade at $1.50 on $25 par implying $.06 on the dollar. These preferred values imply a current value of about $3.5 billion on the estate.

A third and still forming camp (made up mostly of shareholders) has come up with another argument. They say (correctly in my opinion) that bondholders are only entitled to interest until maturity. Since the coupons are all low (none higher than 4.57% and two at 1.8%), if the FDIC cash comes back, the company can easily satisfy $95 million of annual interest payments. The company could then use the cash and proceeds from any asset sales to buy another business or businesses, in addition to continuing to run the $9.8 billion asset management business while utilizing the NOL to shield taxes. This strategy likely maximizes the value of the NOL. In that scenario, bonds are simply reinstated. In yet another scenario, bonds can be bought back at a discount and the NOL utilized to shield the taxes from the gain. In either the reinstatement or the buyback scenario, one can argue that since the preferred shares are not cumulative dividends and dividends only have to be paid if there is a common dividend, that there is value in the common equity. How much is a point of contention and preferred and common shares will have to slug it out for percentages of the reorganized equity, but at $.40-.50 there is less than $30 million of market value of common shares. That is priced as a pure option, and equity holders have organized.

In either the second or third scenario, I think the preferred shares are interesting. It doesn't take a huge leap of faith to see value here above the debt. Preferred shares are saying it's only ~$300 million. Depending on how the NOL is utilized, it could be multiples of that. It's hard to see how the value could be much less than that as long as the cash comes back from the FDIC.

If preferred holders are forced to accept that common shares are not worthless, that will reduce the upside, but the risk/reward is still compelling. Therefore, at $1.50/share, the listed preferred shares are a very interesting long. For those who are willing to go farther on the risk spectrum, the common shares are a fairly cheap option at $.40/share. Note both of these securities are securities of a bankrupted company and trade on the pink sheets so take that risk and liquidity into consideration before making any decision.

Risks

The main risk here is the cash at the FDIC. If the FDIC gets to keep it, then bonds are impaired and there is no value in anything else. The FDIC could also file a contingent claim. That's an unknown risk and impossible to size. I struggle to come up with justification for anything, but it has to be taken into account. There is also a risk to how much of the NOLs can be used and how quickly. Deterioration of the investments in the securities (shares and warrants) and asset management business would also impair value of the estate. Process wise, a long and drawn out battle in bankruptcy court would saddle the estate with fees that would bleed value. Lastly, as mentioned above, everything here is tied to a bankrupt entity and the listed preferred shares and common shares trade in the pink sheets and are naturally risky and illiquid. Over the counter securities have their own risks as well.

Conclusion

I think this situation offers some compelling risk/reward for those willing to delve into a bankruptcy situation and tolerate the risk and illiquidity of over the counter or pink sheet securities or a bankrupt entity.

For further details see:

SVB Financial Preferred And Common: Potential Value In The Wreckage