AMD - Taiwan Semiconductor: Taking The Temperature Of AI

2023-11-14 09:00:00 ET

Summary

- Taiwan Semiconductor Manufacturing Company Limited is vital to AI investment research as it produces the leading-edge chips powering all AI hardware.

- This allows me to gauge the AI semiconductor market and understand how particular customers like Nvidia Corporation are faring.

- But even as a necessary vendor of AI chips, the AI market is still too small to power Taiwan Semiconductor's growth in the coming quarters.

- On a two-year basis, there won't be any revenue growth until 2H 2024 due to customer inventory, while AI won't be a meaningful driver of growth for the foreseeable future.

There aren't many avenues to understand the temperature of artificial intelligence ("AI") proliferation and how supply and demand are faring. One could look at Nvidia Corporation (NVDA) and see demand is through the roof, while at the same time, look at Intel Corporation (INTC) and wonder if AI has a pulse. But going to the central location of all things AI at Taiwan Semiconductor Manufacturing Company Limited (TSM), aka TSMC, brings all aspects of the AI world together. But even with a good read on AI's temperature, is there enough life to support Taiwan Semiconductor's growth over the next year? Based on the still small and cornered market of data center AI, it doesn't appear so. It'll take a rebound in its non-AI HPC and mobile markets to bring back meaningful growth.

Taiwan Semiconductor is the leading provider of CPUs and GPUs worldwide. Apple (AAPL), Nvidia, AMD, Qualcomm (QCOM), and Broadcom (AVGO), among other popular names, are all customers. So, when Taiwan speaks of shifts or changes in the industry, it's a pretty telling data point.

In late July, I broke down the various aspects of AI revenue for my subscribers with Nvidia's contribution to TSMC's AI revenue. It was also a read-through on Nvidia's demand and how long supply may take to ramp up before it meets demand. As they know, with Nvidia's blowout quarters and guides, it's outperforming my numbers, even if there's some price hiking happening on Nvidia's side.

But on TSMC's side, growth has been lackluster, with negative revenue growth for three straight quarters and another coming, based on guidance.

The bottom line is, has anything on the AI front changed for Taiwan Semiconductor - and the entire industry - and is it enough to reinvigorate its overall revenue growth in 2024?

Slight Shifts In The AI Outlook

Taiwan Semiconductor's management was asked several times about the AI outlook after not mentioning much during its prepared remarks. From this lack of enthusiasm alone, I gathered AI is not as meaningful of a driver as investors hope it is. If AI were truly TSMC's way of returning to meaningful growth, it would be touting it more.

This isn't to say TSMC doesn't have great AI technology on the front or back end, supply chain management, or business relationships. But, if it's mainly Nvidia providing the revenue, that's not enough to support the company on a needle-moving basis. Especially when you dig down and find the massive revenue Nvidia can rake in is due to the margins Nvidia can add to the relatively cheap TSMC-based component it needs to put the GPU-based systems together.

Things remain tight on the supply side on this front, and there's even a hint of improving supply beyond previously expected. For example, the company on the FQ3 call said it's going to more than double its capacity (emphasis added):

We are working very hard to increase the capacity more than double , but today is limited by my suppliers' capability or their capacity . So we still maintain that we will double our CoWoS capacity by the end of 2024. But the total output actually is more than double from 2023 to 2024 because of a very high demand in -- from our customer.

- Dr. C. C. Wei, CEO, TSMC's Q3 '23 Earnings Call Q&A .

This is a slight departure from FQ2's call, where it said "probably" two times the capacity (emphasis added):

...for the back end, the advanced packaging side, especially for the cohorts, we do have some very tight capacity to - very hard to fulfill 100% of what customer needed...

I will not give you the exact number, but let me give you a roughly probably 2x of the capacity will be added

- Dr. C. C. Wei, CEO, TSMC's Q2 '23 Earnings Call Q&A .

This isn't a huge shift, but it does tell me things remain robust on the demand side, and the supply side doesn't have much greater capability to expand in the near term. While missing out on revenue, the backlog isn't falling apart since there's nowhere else to source the leading node chips and CoWoS packaging required on the back end (at least at scale).

This means Nvidia's AI demand remains robust, and there won't be any surprises from Nvidia to the downside in the next quarter. This is good for TSMC, as demand isn't destroyed by lack of supply as it remains constrained.

AI Isn't Large Enough (Today) To Boost Growth

So AI is pressing forward; this is good for Nvidia, STMicroelectronics ( STM ), Micron ( MU ), and Arista Networks ( ANET ), among others, playing the picks and shovel side of AI. However, the problem is this AI niche (I use that term loosely) is too small financially to overcome the broader smartphone HPC (high performance computing) sectors Taiwan Semiconductor services.

While AI-related demand continues to be strong , it is not enough to offset the overall cyclicality of our business. We expect our business in the fourth quarter to be supported by the continuing ramp of our 3-nanometer technology, partially offset by customers' continued inventory adjustment.

- Dr. C. C. Wei, CEO, TSMC's Q3 '23 Earnings Call (emphasis added).

This is, while the company expects AI server growth of 50% CAGR over the next five years. But, it only expects AI revenue to grow to low teens from 6%. So, while it could double in terms of revenue share, it remains a very small part of the company for the foreseeable future.

...server AI processor demand...accounts for approximately 6% of TSMC's total revenue. We forecasted this to grow at close to 50% CAGR in the next 5 years and increase to low teens percent of our revenue.

- C. C. Wei, CEO, Taiwan Semiconductor's Q2 '23 Earnings Call.

Yes, other AI applications will bring this internal revenue share up, but this is why year-over-year growth will continue to be negative. Until PC OEMs clear inventory and smartphone manufacturers see demand return (I'm not talking seasonally like it does in third quarters), Taiwan Semiconductor will continue to see depressed growth. Moreover, the CPU data center side is currently being reprioritized for AI-centric servers. This is why Advanced Micro Devices ( AMD ) and Intel's data center revenue has been, at best, flat this past year, reeling from high inventory. That high inventory is coming from a lack of use by customers since they are working AI hardware instead.

Therefore, things continue to look fairly bleak outside of AI.

This is why Taiwan Semiconductor, while the global leader in advanced nodes for logic chips, doesn't have a great growth outlook for the next few quarters. The expectations for returning to growth depend on lapping 2023's weak quarters and the return of demand from weak sectors that may not have the demand they once saw as chips turn toward more AI-based products.

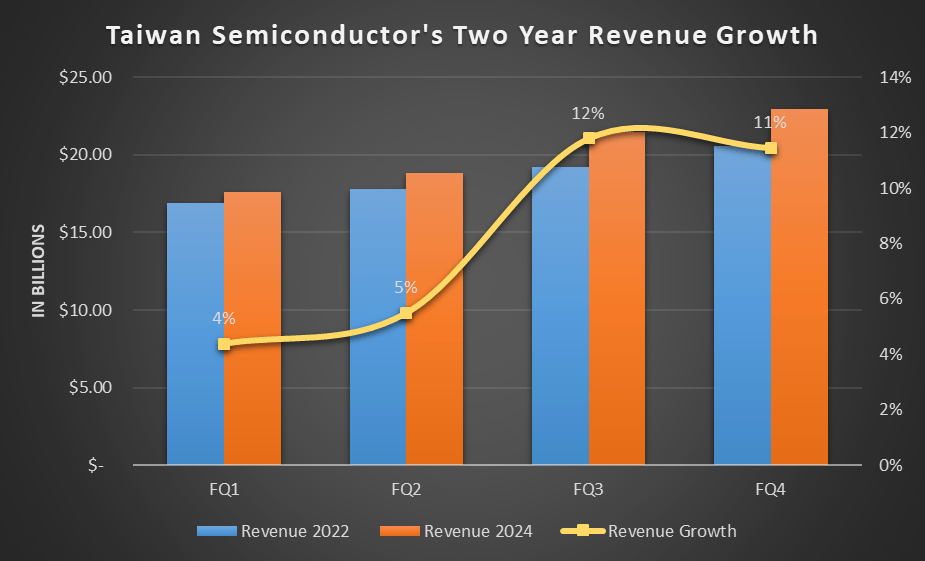

Even on a two-year growth basis, revenue won't meaningfully inflect until FQ3, when it makes it to very low double-digit growth.

{kind=link}

This portends further weakness in the industry outside of AI as 2022 growth pulled forward quite a bit, which is now the inventory in 2023 being worked through. In other words, inventory work-through won't ease until, at best, 2H 2024, as revenue will only be marginally higher on a two-year time frame in 1H.

The Best But Not The Time

Taiwan Semiconductor is a technological force in chips unmatched by even larger competitors like Samsung (SSNLF), but the industry as a whole is transitioning to a new paradigm of computing via AI. This isn't restricted to just Nvidia or just data centers; smartphones and IoT will have AI capabilities and will require the leading-edge node to provide power efficiency and computational capacity. However, this transition is still too young to provide a meaningful boost as technological creative destruction takes its toll on server CPUs, industrial applications, and smartphones.

The lead Nvidia has created in data centers is the exception to the rule of AI right now, but it's the signal of the start. For AI to be more meaningful to TSMC's revenue, it'll require more time for the industry to catch up to what Nvidia has been working on for a decade. It's already coming to fruition, but outside of data center, no other vertical has had its "AI moment." When they do, TSMC will more readily feel the financial effects. Until then, the industry moving through this transition will cause weakness in status quo product demand and a reprioritization of CapEx spend at hyperscalers.

Ironically, while TSMC is at the center of AI chip production, the companies on the other end designing and/or selling the finished product see the best returns - the margins on these end products are the highest they ever will be. Creating a singular - yet extremely important - component of the system is valuable, but it's not where the capital returns lie. At least not today.

For further details see:

Taiwan Semiconductor: Taking The Temperature Of AI