WGO - Take A Ride In Winnebago For High Long-Term Returns

2023-04-20 07:46:13 ET

Summary

- We recommend WGO stock as a Buy for long-term oriented value investors.

- WGO has visionary management and strong competitive positioning with high-quality brands in an oligopolistic industry with high barriers to entry.

- The work-from-anywhere trend and more workers retiring are driving increasing demand for outdoor activities.

- WGO has strong profitability and solid future cash flow potential.

- We believe investors have priced in overly pessimistic long-term growth prospects due to near-term concerns about recession, inflation, and interest rates, which provides a very attractive valuation entry point for long-term investors.

Editor's note: Seeking Alpha is proud to welcome The Profit Detective as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

We rate Winnebago Industries, Inc. ( WGO ) a Buy because of its strong competitive positioning, solid long-term growth potential and very attractive valuation.

Aided by the Covid lockdowns encouraging work-from-anywhere trends and retiring Baby Boomers, consumer demand for outdoor experiences is increasing. We believe this will clearly benefit WGO, which has very strong brands in the oligopolistic outdoor vehicle industry.

Due to the rise in interest rates over the past year and signs that the economy will likely go into a recession this year, investors have priced in unreasonably pessimistic long-term growth assumptions into WGO stock, in our view.

For patient investors, we believe WGO stock provides an excellent opportunity for limited downside risk in the near-term and substantial upside potential longer-term when the economy recovers.

Business Overview

WGO is a leading North American manufacturer of recreation vehicles ("RVs") and boats, which are used primarily in leisure travel and outdoor recreation activities.

The company was founded in 1958 in Forest City, Iowa, which is in Winnebago County. In 1966, Winnebago started selling motorhomes at half the price of competitors, which led to massive popularity in the RV community. The Winnebago brand became so ubiquitous that it became used as a generic name for motorhomes, similar to how the Kleenex brand is used for tissues. This strong brand equity has endured and has been key to Winnebago's success ever since.

We like companies with visionary management and we believe WGO has that. Michael Happe was named President, CEO and a Director of WGO in January 2016. Happe has successfully transformed the company from the single Winnebago brand platform to a portfolio of premium outdoor brands with the acquisitions of Grand Design RV in 2016, Chris-Craft boats in 2018, Newmar premium motorhomes in 2019 and Barletta boats in August 2021.

WGO now sells three main products: towables, motorhomes and boats.

According to the company's description, towables are recreational vehicles without motors that are towed by cars and other motorized vehicles. Towables range in price from roughly $30,000 to $150,000. Motorhomes range in price range from around $115,000 to $1,600,000, while boat prices range from around $60,000 to $780,000.

In their fiscal year 2022 (ended August), Towables were 52% of revenue (versus only 9% in FY16), Motorhomes were 39% and Marine was 9%. Their goal is to increase Marine to about 15% of revenue by FY25. Towables and Marine are higher margin product lines than Motorhomes.

WGO has multiple production facilities in Iowa, Indiana, Minnesota and Florida. Products are generally made to order, which minimizes inventory problems and discounting. They sell their products to about 750 independent dealers in the US and Canada, who then sell the products to consumers.

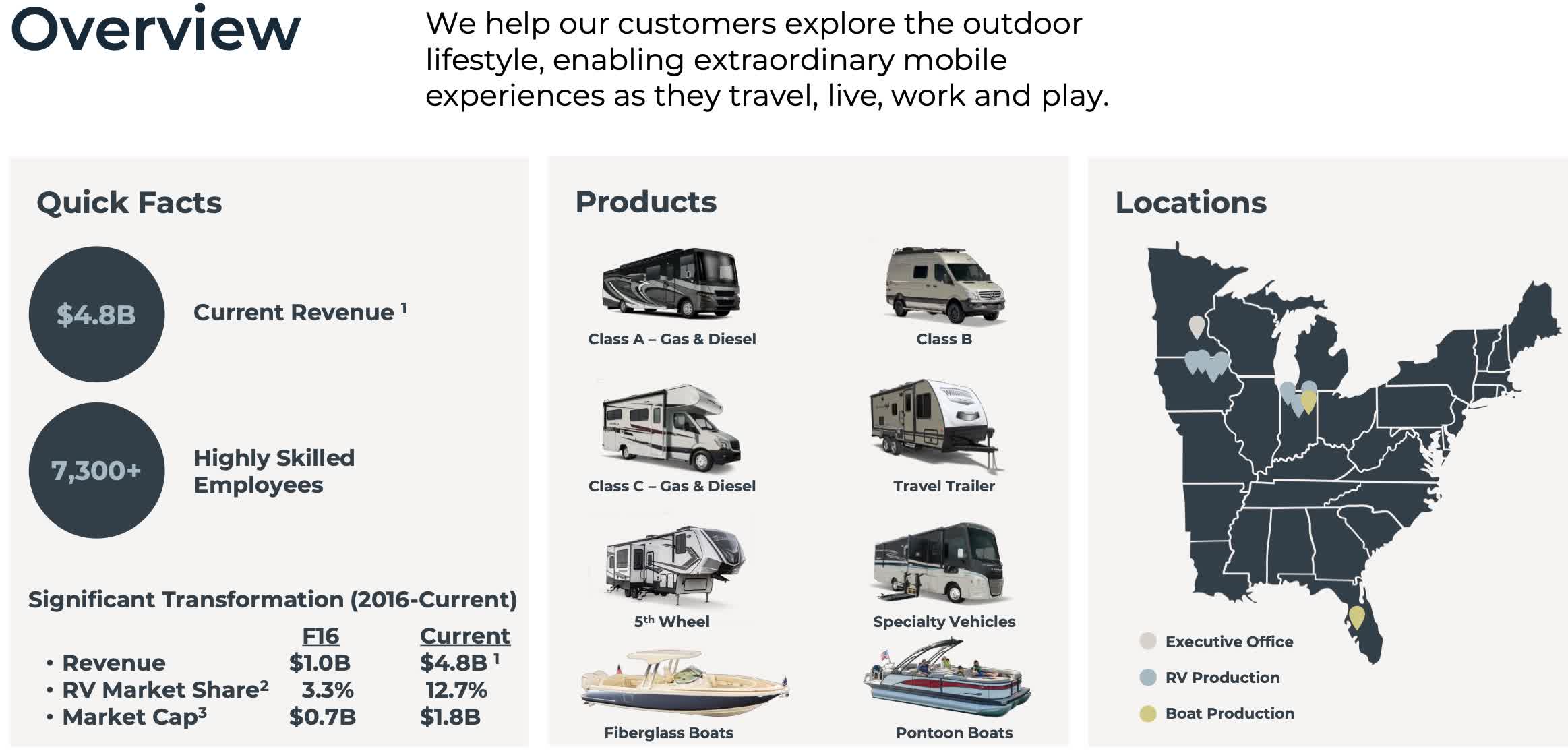

This slide below provides an overview of the company's mission, products and locations. It also shows the significant transformation of the company since CEO Happe took over in 2016, increasing revenue by nearly five-fold, RV market share by nearly four-fold and market capitalization by 2.5 times. We believe WGO can continue to grow revenues, market share and market capitalization going forward.

{kind=link}

Industry & Competition

We believe WGO has a strong competitive economic moat that will enable them to continue to gain market share and generate high returns on capital and strong free cash flow over time.

We believe the key factors that have built their economic moat include:

- strong brand names with decades of history

- large capital investment required to design and construct RVs and boats

- already established broad dealer network

- oligopolistic industry with WGO, THOR Industries ( THO ) and Berkshire Hathaway's ( BRK.A ) Forest River controlling 90% of the RV market

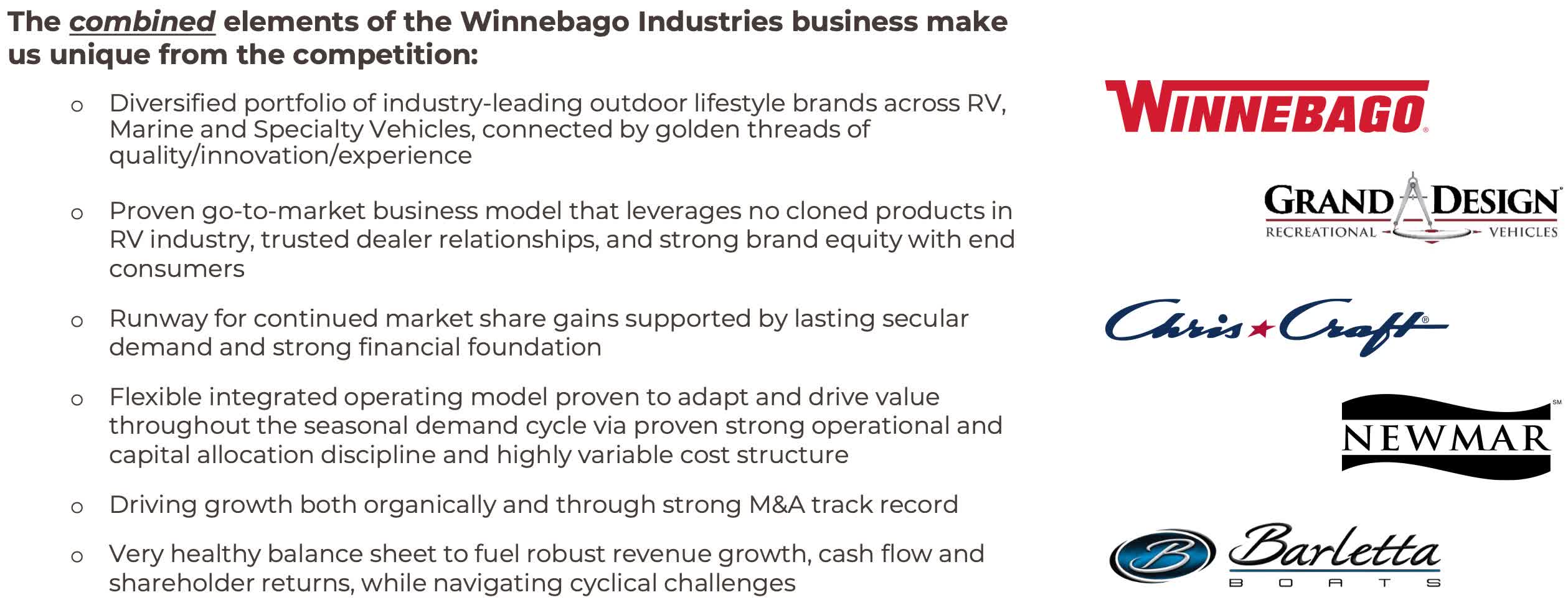

The slide below provides a summary of the investment thesis for WGO.

{kind=link}

Since RVs and boats are expensive and highly personal items for consumers, it is important that they provide high quality and good value. WGO's motorhomes are highly regarded for their premium amenities and fuel-efficient technology. In fact, they are the only motorhome manufacturer to win the RV dealer quality award every year since 1996.

We like the fact that WGO has a broad target customer base, since most people like to enjoy the outdoors. Nearly 9% of US households own an RV and 12% own a boat.

There are 94 million active camper households in the US, including 9.1 million who were first-time campers in 2021. First-time campers since Covid are younger and more affluent, with about 60% of them under the age of 40 with a household income over $100,000, as compared to only 29% for all campers. Over 80% of first-time campers have children and 25% are Black and Hispanic.

In addition to enabling consumers to enjoy the outdoors, RV travel is also very cost-effective. For a family of four, gas prices would have to rise to more than $12 per gallon to make RV travel more expensive than other forms of travel.

Boating also has broad appeal across generations. About 28% of boat owners are Baby Boomers, 37% are Generation X and 31% are Millennials.

Growth Drivers

WGO growth drivers include industry growth, market share gains, new product innovation (including new electric vehicle products) and acquisitions, as well as margin improvement from sales leverage and faster growth in their higher margin Marine segment.

Over the past three fiscal years, WGO has grown their Towables revenue by 29.5% annually, motorhomes by 39.3% annually and Marine by 76.7% annually. This very rapid growth was driven by strong execution by the company, as well as increasing consumer demand for outdoor experiences.

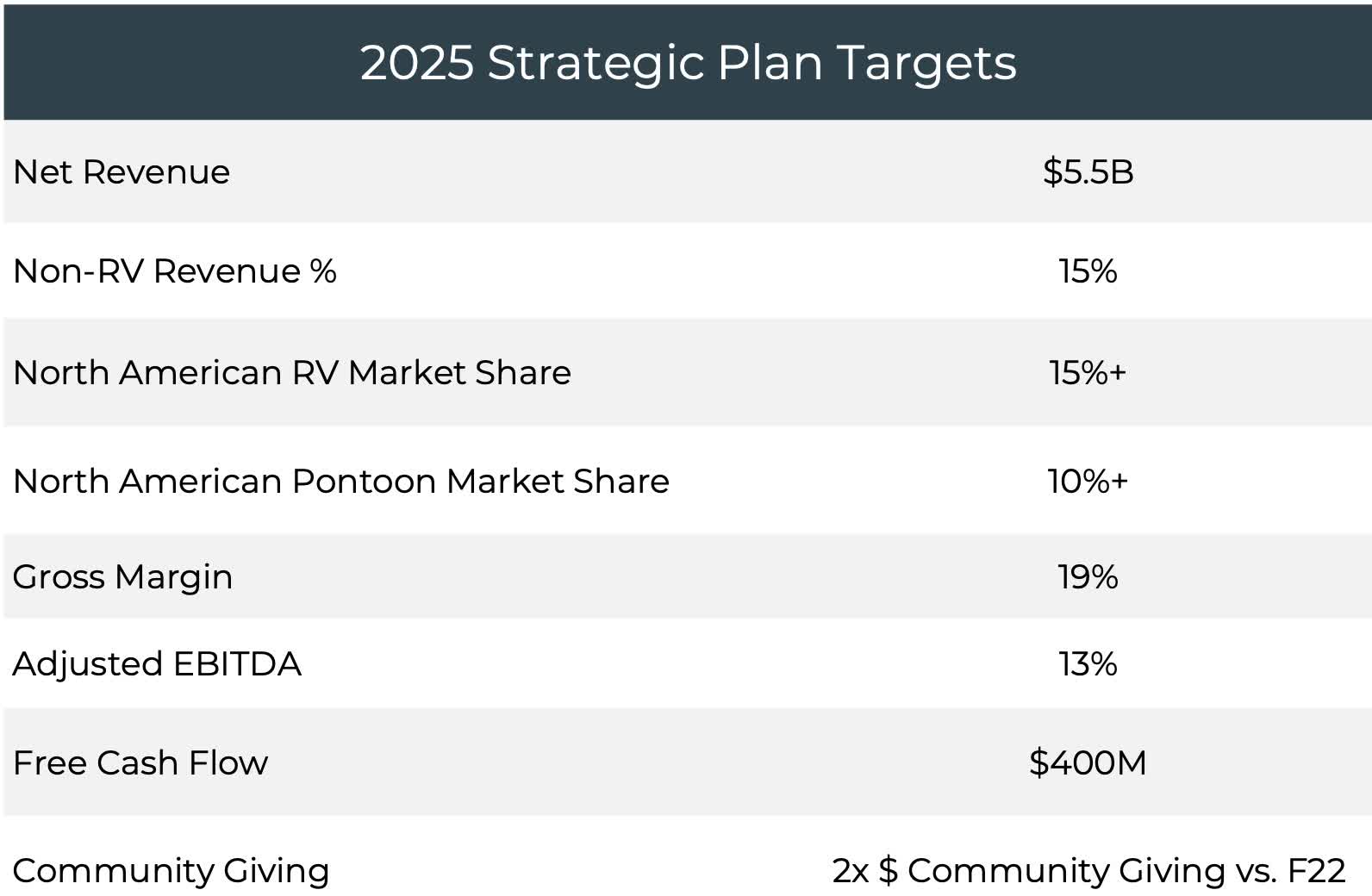

WGO's FY25 targets are for annual revenue growth of 3.5% to $5.5 billion and annual free cash flow growth of 8.5% to $400 million in FY25, as shown below.

{kind=link}

We believe those targets are conservative, given their strong track record of growth, as well as solid industry growth projections. However, a potential recession creates substantial uncertainty in the near-term.

According to the Bureau of Economic Analysis , RVing grew 10.3% and Boating grew 5.3% annually from 2017 to 2021. From 2021 to 2027, the RV market is expected to grow 6.4% annually and the boating market is expected to grow 5.1% annually, according to market intelligence firm Mordor Intelligence .

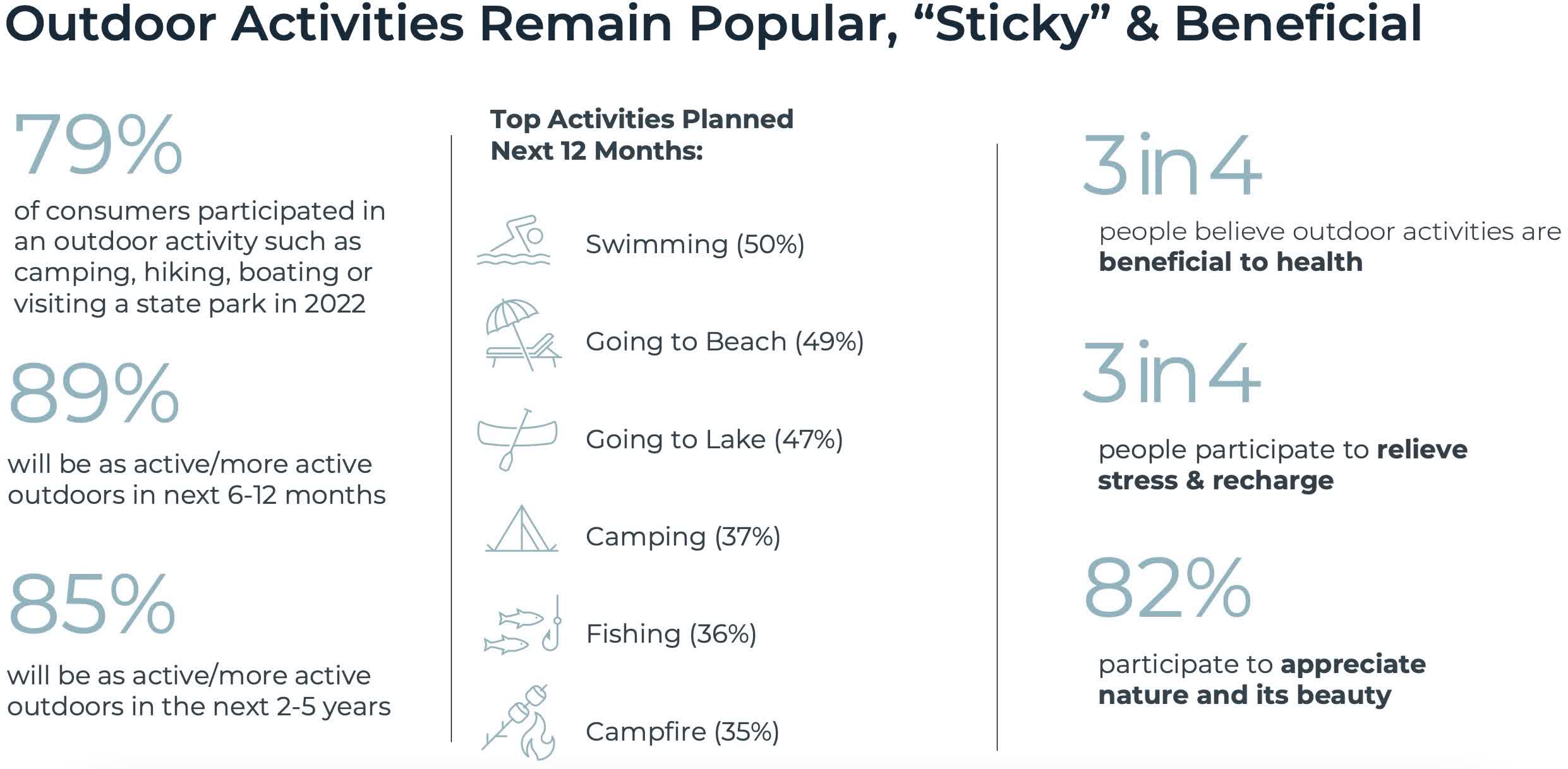

We believe the outdoor industry has clear secular growth prospects, as most people enjoy outdoor activities and plan to pursue them going forward, as shown below. The work-from-anywhere trend and rising retirement rates are also driving industry growth.

As shown in the slide below, 85% of consumers surveyed said they plan to as active or more active in the outdoors as they are now over the next 2-5 years. The primary reasons consumers want outdoor experiences is to improve their health, reduce stress and appreciate nature and its beauty.

{kind=link}

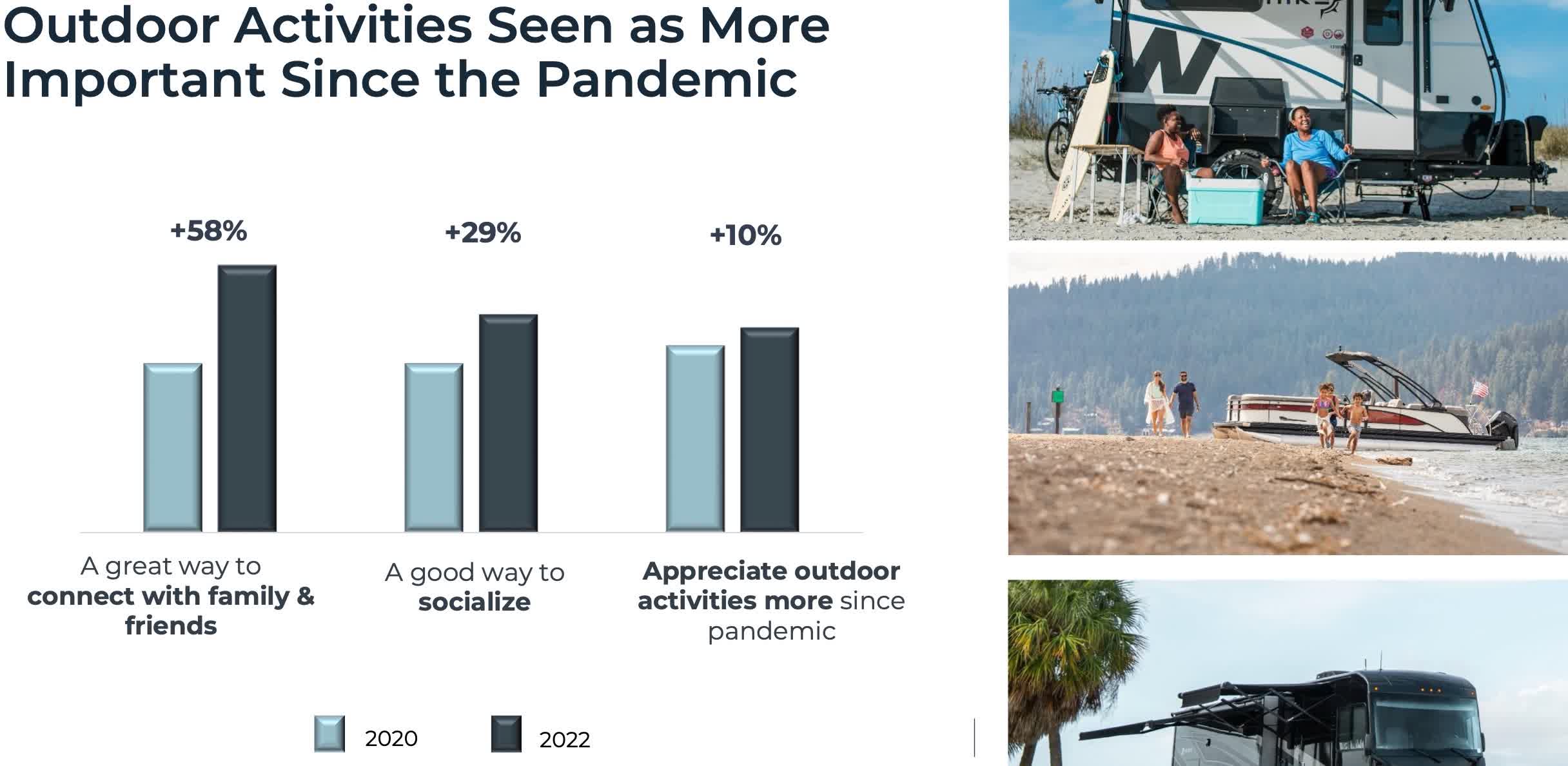

The lockdowns during the Covid pandemic drove particularly strong demand for outdoor recreation. WGO was a clear beneficiary of this phenomenon, as their revenue fell 1.5% in FY19, but rose 19% in FY20, 54% in FY21 and 37% in FY22, according to the financial data on Seeking Alpha . The chart below shows the pandemic helped drive a huge 58% increase in consumers' view that outdoor activities are a great way to connect with family and friends, as well as a 10% increase in appreciating outdoor activities more.

{kind=link}

There is strong consumer interest in RVs, in particular. Based on consumer surveys , 98% of first-time RV buyers say they will buy again, 68% of RV owners plan to buy again in the next 5 years and 31% of those who don't own an RV are interested in buying.

Over the past six years, WGO's RV market share has nearly quadrupled to 12.7%, while their motorhome market share has increased from 17% to 21% and their towable market share has doubled to 12%. We believe there is significant market share remaining for WGO to continue to gain share going forward.

WGO's planned RV innovations include off-road towables, more Newmar luxury brand models and features enabling more off-the-grid camping and year-round RV use.

WGO is also pursuing electric vehicles. They recently acquired Lithionics Battery, a lithium-ion battery solutions provider to recreational equipment and specialty vehicle markets.

We believe WGO has significant growth potential in boating. Their Marine division is benefiting from strong demand in the Chris-Craft brand and in Barletta pontoons, which is only in 40% of the addressable pontoon market. Chris-Craft is planning new smaller models and Barletta is planning new premium and value models. Chris-Craft recently built a new facility that increases their production capacity by 50%.

WGO plans to continue to pursue acquiring high-end brands in the $860 billion outdoor activity market. WGO acquisition strategy is to buy premium brands with high margins, rather than turnarounds. We like this strategy as it is congruent with their experience and skill set.

Economic Sensitivity

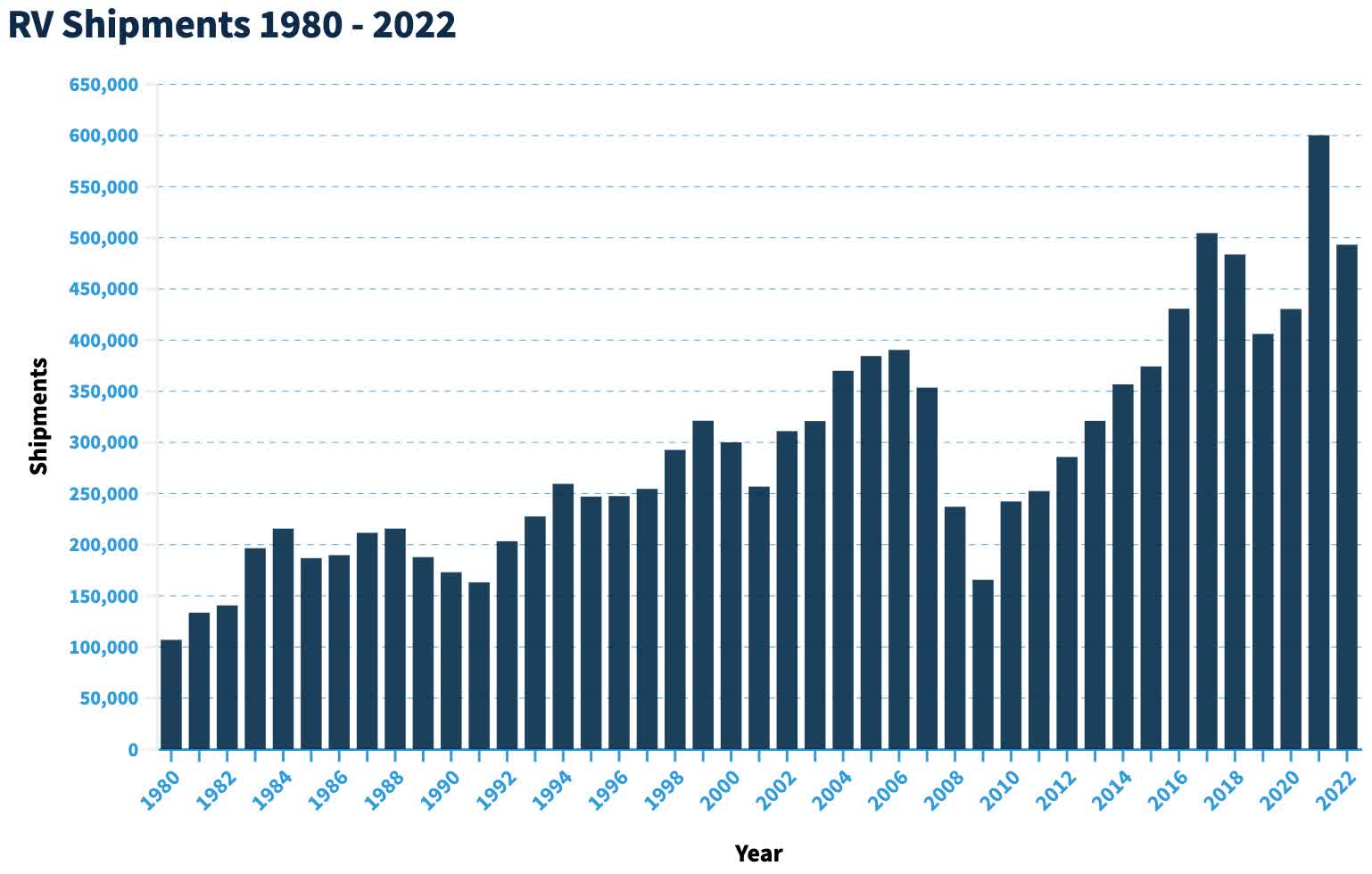

WGO is highly sensitive to the business cycle, since it sells a high-ticket consumer discretionary products. As shown below, RV volumes fell 58% during the Great Recession, from 390,362 in 2006 to a low of 165,709 in 2009.

{kind=link}

RV sales are expected to decline in 2023 due to the slowing economy, high inflation and rising interest rates. RV industry trade group RVIA forecasts sales of 334,100 RVs in 2023, down 32% from 493,300 in 2022 and almost 50% from the record high of 600,240 units in 2021. But this is off from a very high level, as the 2021 high was nearly 50% above the 2019 level of 406,070.

WGO backlogs grew significantly due to higher Covid demand and slow supply chain issues, so we do not believe it is surprising that they are falling now as demand slows and supply chains improve.

In their latest quarter, WGO's Towables backlog fell 77% from last year due to higher dealer inventories and Motorhome backlog fell 34% due to normalizing dealer inventories. However, Marine backlog grew 24% due to dealer inventories replenishing and signing new dealers.

WGO's stock beta is 1.32, which means that all else equal, WGO will usually outperform the overall stock market in a bull market and underperform in a bear market.

Since the stock market has been in a bear market over the past year, interest rates have been rising and leading economic indicators suggest a recession is coming, there is clear near-term risk for WGO's sales.

While a recession is an obvious risk for WGO, we believe their growing Marine segment and 85% variable cost structure will help mitigate downside earnings risk. Importantly, they do not manufacture a product until it has been ordered, so that minimizes discounting and margin risk.

Financial Analysis

According to the financial data on Seeking Alpha, WGO has grown revenues by 35.7% and EPS by 49.8% annually over the past 3 years. That is very strong growth, but what matters to a stock is future growth.

Wall Street expects FY23 revenue to fall 25% and EPS to fall 45%. This decline is primarily due to facing very difficult comparisons and weakening consumer demand. In FY24, revenue growth is expected to fall 1.5% and EPS growth is expected to fall 0.1%.

WGO has consistently beaten quarterly EPS estimates , with a 51% upside surprise in the most recent quarter. However, FY23 earnings estimates have been cut by 15.5% over the past six months, as backlogs have shrunk and the economy has weakened.

WGO has strong profitability , with operating profit margins of 10.5%, return on equity of 24.6% and return on capital of 15.5%. These profitability metrics are higher than competitor THO and they have improved in recent years. We believe this impressive profitability illustrates the power of WGO's brands and the strong execution of WGO's management team.

In our view, WGO allocates its capital well for the benefit of shareholders. Free Cash Flow ("Cash Flow From Operations less Capital Expenditures") was $312.5 million in FY22, which helped fund $24 million in dividends and $214 million in stock buybacks.

The FCF yield ("FCF/Market Capitalization") is 16% and the dividend yield is 1.84%. They have had 4 consecutive years of dividend growth and the annual dividend growth rate over the past five years has been 19.9%. They have a $350 million share repurchase program that does not expire.

We like that WGO has maintained a strong balance sheet , which should help them weather a recession well. Net Debt/Enterprise Value is only 17% and Net Debt/EBITDA is only 0.6x.

Valuation Analysis

Due to obvious concerns about slowing growth, rising interest rates and a likely recession, investors are valuing WGO very attractively relative to its future free cash flow potential, in our opinion.

WGO looks very cheap to us using valuation multiples . WGO's forward P/E ratio is only 7.8x, which is 43% lower than competitor THO. Similarly, its forward EV/EBITDA ratio is only 5.9x, which is 20% lower than THO.

We believe our Discounted Cash Flow ("DCF") analysis provides a more detailed look at how inexpensive WGO is relative to its likely future growth potential.

Our DCF analysis is based on the following key assumptions, using financial data from Seeking Alpha:

- FY23 revenue growth falls 30% due to difficult comparisons and slowing demand. This is more conservative than consensus expectations for a 25% decline.

- FY24 revenue growth is 0%, FY25 revenue growth is 2% and FY26 and FY27 revenue growth is 3%. This is more conservative than expected annual industry growth of 5%+, which we believe WGO can exceed with market share gains. However, we are being more conservative in our growth estimates due to the likelihood of a recession.

- FY23 operating margin is 10%, well below FY22 margin of 11.8% due to deleverage from falling revenues.

- Operating margin improves to 10.5% in FY24 and 11% in FY25/FY26 with cost controls and improving sales growth.

- Discount rate is 10%, which assumes an investor wants to earn a 10% annual long-term return on WGO, which we view as reasonable given the risks involved.

- Year five Terminal Value = [Year 5 FCF * (1 + Perpetuity Growth Rate)] / (Discount Rate - Perpetuity Growth Rate).

- Our Base Case assumes a 1% Perpetuity Growth Rate, which we view as conservative given industry growth prospects and WGO's likely market share gains, but given the cyclicality of the industry, we believe it is wise to be conservative at this point.

- Our Upside Case assumes a more optimistic 3% Perpetuity Growth Rate.

- Our Downside Case assumes a negative 5% Perpetuity Growth Rate, which we view as a very negative long-term outlook that would likely require significant changes in the industry and/or consumer behavior (such as living in the metaverse all the time!).

As shown in the table below, our Base Case stock valuation is $72.84, which is 24% upside. Our Upside Case valuation is $90.43, which is 54% upside. Our Downside Case valuation is $48.20, which is 18% downside.

The current price implies a negative 1.7% Perpetuity Growth Rate, which we believe reflects investors pricing in current negative trends into an unreasonably pessimistic long-term outlook.

Author's Calculations using data from Seeking Alpha

Due to its deep valuation discount to THO and its significant upside potential based on our conservative free cash flow assumptions, we believe WGO is very attractively valued.

Risks

The primary near-term risks WGO faces are difficult comparisons, high inflation, rising interest rates and a possible recession. These risks could cause earnings to be much worse than consensus estimates, which could cause significant downside in the stock.

However, based on our DCF analysis, FY23 revenues would have to fall 45% and operating margins would have to fall to 9% to cause the stock to be worth 15% less than it is now. That is far worse than the 25% revenue decline consensus expects. Thus, we believe the stock already discounts significant earnings risk due to recession fears and other concerns which are top of mind for investors.

Seeking Alpha's Dividend Grades framework implies that WGO is at risk of cutting their dividend. However, we believe risk of a dividend cut is low. WGO's annual dividend is less than $40 million and their capital expenditures are less than $100 million. Cash flow from operations was $371 million over the past year. Thus, cash flow from operations would have to decline over 60% before WGO would have to consider cutting either capital expenditures or their dividend. That is possible if there is a deep recession, but WGO's dividend cut will hardly be the only risk investors will face if there is a recession that bad.

The main factor that would cause us to become bearish longer-term on WGO is a fundamental change in consumer behavior leading to less interest in outdoor activities. That could happen if the work-from-anywhere trend reverses and/or people lose interest in outdoor activities and prefer to stay home to save money, live in the metaverse or some other unforeseen reason.

Investment Recommendation

We rate WGO a Buy due to its strong competitive positioning, increasing consumer interest in outdoor activities, market share gain potential, strong profitability and very attractive valuation relative to peers and future free cash flow potential.

While a recession may make for a bumpy ride in the near-term, investors with a longer-term outlook should enjoy smooth sailing as WGO stock creates wealth that can enable them to relax and enjoy the great outdoors.

For further details see:

Take A Ride In Winnebago For High Long-Term Returns