TELL - Tellurian: Odds Of Success At Driftwood Slip Again

Summary

- Tellurian failed to lock down Driftwood during peak LNG mania.

- Now, it faces lower international prices, tighter financing markets, and weaker cash generation.

- A key deadline with Gunvor approaches.

Despite the prognostications of many, the outlook for Tellurian ( TELL ) and its prospective Driftwood LNG project was not all that great even during the summer of last year. Despite still low interest rates, rabid interest in liquefied natural gas, and a great outlook for profitability from its internally owned natural gas production, management was unable to secure the financing and contracts necessary to really push forward with the project.

Here we are less than one year later and the energy landscape has been turned on its head. While still above mid cycle levels, liquefied natural gas prices have fallen heavily from the stratospheric levels of the summer. So too have domestic natural gas prices. Corporate borrowing rates and risk tolerance from lenders have weakened, making the entire project more expensive than it would have been all else equal. And we are now one week away from a key critical deadline with Gunvor - the sole remaining sale and purchase agreement remaining in place. Long story short, Tellurian is not in a great place.

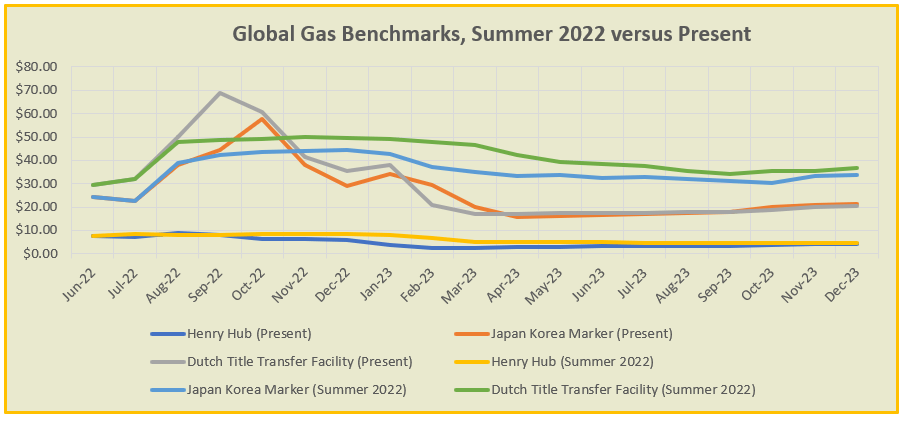

Falling Natural Gas Prices

{kind=link}

Since the early summer - which even precludes the largest spike in prices - international benchmark prices for natural gas have come in significantly. The Japan Korea Marker (Asian benchmark) has fallen by more than half, Dutch Title Transfer (European benchmark) by two thirds. Recall that management was targeting a pricing model that was not fixed price tolling like most other LNG facilities, instead giving it exposure to the difference between international prices less free on board costs. That works just fine in the type of hot market we had in 2022, but the opposite is true now.

When I spoke to management in early 2022 at a conference, we were supposedly just months away from secured financing and a plethora of deals. Despite runaway LNG prices and rabid interest from investors in this area of the energy markets, Tellurian was unable to secure the financing it needed to start construction. The question investors have to ask themselves is a simple one: If Tellurian could not get Driftwood off the ground in mid-2022 during the hottest market for LNG arguably ever, how likely are they to do so in 2023?

Unfortunately, all of this is a bit of self-fulfilling. Tellurian was expected to need to front around 30.0 - 40.0% of the equity for Driftwood, with the rest being debt-funded. Even under the smaller two train, 11.0 mmtpa design, the price tag is going to run close to $9.0B. Tellurian was going to need billions of dollars in equity funding without a partner - which it does not seem to be getting - and that was going to require hundreds of millions of shares in dilution. Most analysts expected the outstanding share count to triple by the time the project came online, and that's only worse now given the share price.

The outlook for internally funding some of this is also poor. Tellurian exploration and production operations performed well during 2022, delivering significant EBITDA. However, Henry Hub looks set to come in at less than $3.00 per mmbtu in 2023 given the forward curve; levels half of that of 2022. Once generating some free cash flow on a corporate level excluding any construction costs, Tellurian now likely slips into cash burn.

Gunvor Contract

Tellurian lost several of its sales and purchase agreements, and the sole remaining contract with Gunvor is for ten years, with them offtaking 3.0 mmtpa. However, that agreement is predicated upon a full notice to proceed to the Driftwood contractor (Bechtel) and securing all the necessary financing. This deadline has already been pushed back twice and the company assuredly fails this again on the coming February 28 deadline. Tellurian is then going to find itself with no sales and purchase agreements at all, and there is absolutely no way to secure financing without them.

Takeaways

Long story short, the outlook looks absolutely dismal. Odds of a successful Driftwood LNG project completion now stand at between 5.0 - 20.0% odds according to most analyst models on Wall Street. While the shares probably are undervalued under most circumstances if the project can get off the ground, this has turned into a situation where shareholders are going to lose their capital under nearly all scenarios. The risk just isn't worth it on the small off chance of a homerun in my opinion.

For further details see:

Tellurian: Odds Of Success At Driftwood Slip Again