THC - Tenet Healthcare: Compressed Multiples Appear Justified

Summary

- Tenet Healthcare has caught a strong bid since October FY22', extending its rally into the new year.

- The question we sought to answer is if THC represents a value proposition that aligns with our core investment principles.

- We'd note the company invested $6.2Bn to generate an additional NOPAT of just $307mm from 2012–FY22E'

- Hence, whilst its compressed multiples are attractive at face value, these appear to be justified by the lackluster growth and ROIC profile.

- Net-net, rate hold.

Investment Summary

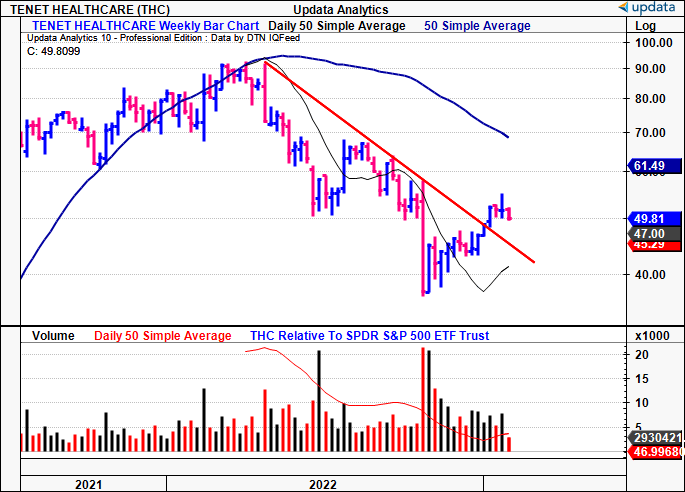

Since we last reported on Tenet Healthcare Corporation ( THC ) market conditions have balanced, with the broad indices rolling into the new year with newfound strength. Still, THC shares are down ~19% since the last report [we encourage you to read it by clicking here ]. Despite this, the stock caught a reasonably strong bid in October FY22' and has broken out of its longer-term downtrend [Exhibit 1].

Noteworthy, is that Greenlight Capital took a "medium-sized" stake in THC in Q4, participating in this rally by sizing in until January. The firm is constructive on its new cost and growth profile, and saw an attractive entry point at the FY22' lows. Assuming one scenario where the firm entered at ~$40, with no leverage, the position could be up 26-30% at the time of writing. Alas, for those active investors taking tactical positions in FY23', short-term rallies like this bouncing from lows are strong source of alpha.

Exhibit 1. THC breakout above FY22' downtrend

{kind=link}

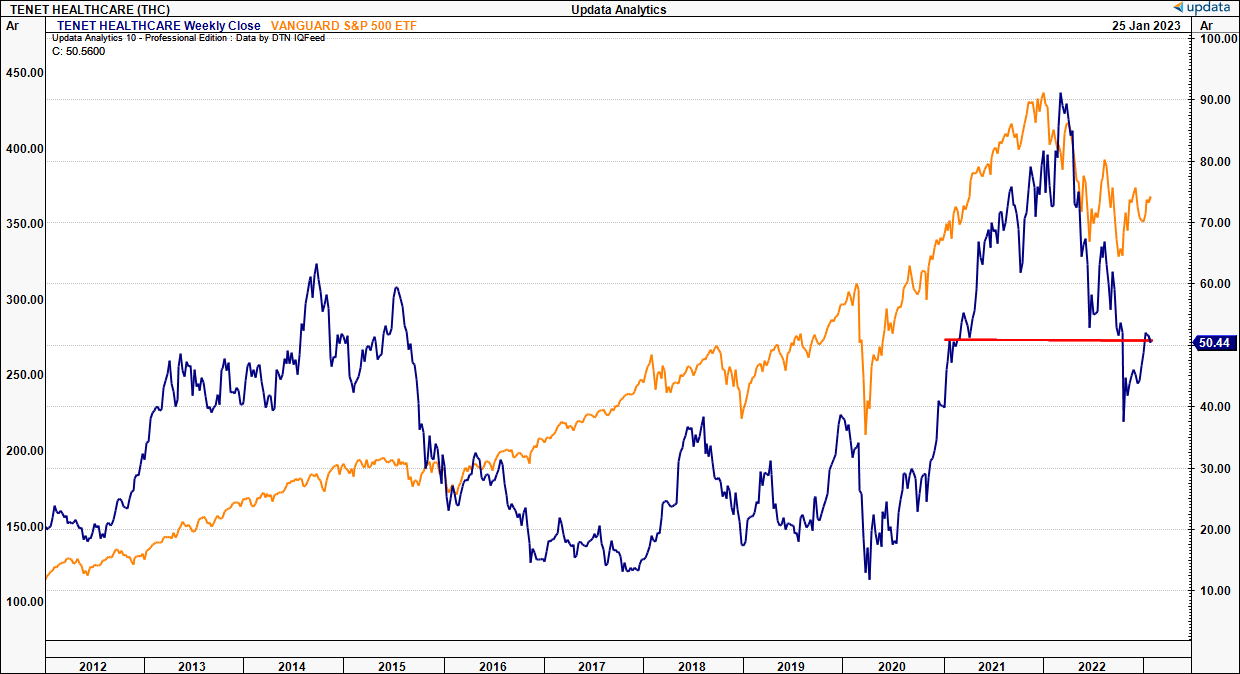

The question now is, is THC a value proposition, or can we expect further challenges for shareholders. It's first worth noting the stock had a tremendous run across the 'pandemic era', climbing from ~$18-$89, a ~395% total return. Note, this is a company that's still valued at $22.6Bn in enterprise value, with $15Bn in debt.

But let's take a step back for a second a look at this from a more pragmatic approach. I'll do this by taking a longer-term view of the company in this report. First, is that the bolus of US listed equities rallied at rapid pace in FY20-21'. Second, intelligent investors are looking to pay a fair price for a stock, quantified by a company demonstrating the core tenets of economic growth. As such, as market and macro-level fundamentals finally caught up to speed [inflation, central bank tightening, potential earnings recession], the high-beta trade has completely unwound, such that the bulk of high-performing names have re-rated toward pre-pandemic range, THC included.

Exhibit 2. THC has given away the bulk of gains in FY22'.

{kind=link}

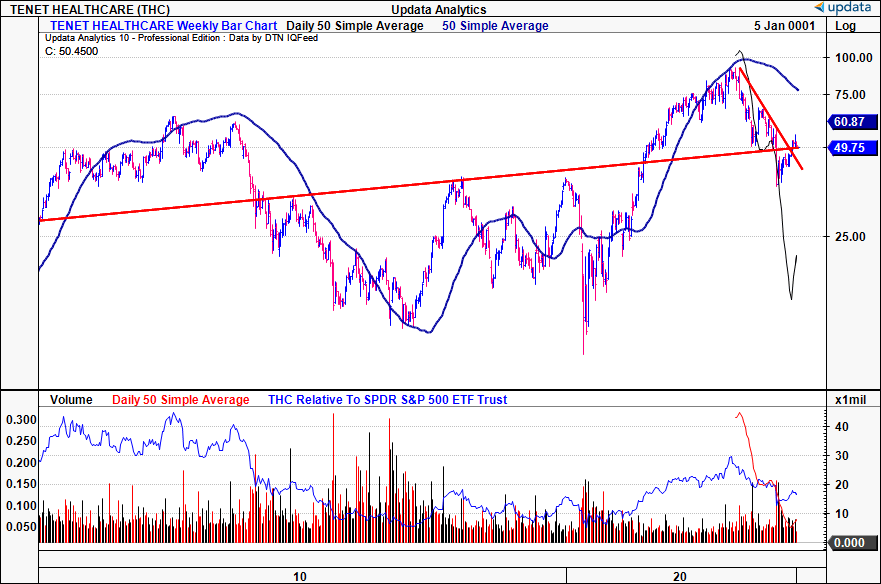

Moreover, looking at the 10-year growth rate of the THC share price, you'll also note it's been flat, and bottom-heavy, even when factoring in the FY20-21' rally [Exhibit 3]. Here I'll explain why we believe this to be the case, and answer why we are cautious on its growth prospects looking ahead. Net-net, we continue to rate THC a hold.

Exhibit 3. 10-year growth rate in THC share price

{kind=link}

THC requires high capital to grow, but generates low returns

The two main drivers of intrinsic value are growth [sales, operating income, earnings, cash flows, etc] and return on invested capital ("ROIC"). Different combinations of growth and ROIC can create the same level of value. We rigorously analyze companies on this premise to understand how much a company can/needs to reinvest into its business to grow, what the return will be on this investment, and what distributable cash is left for shareholders.

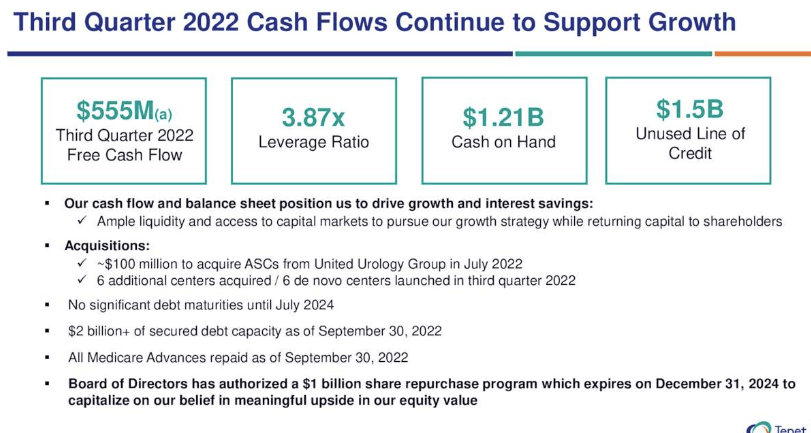

Turning to THC's most recent earnings, the company highlighted that it's growth percentages have shown marked improvement since FY17 to FY22' full-year estimates. Adjusted EBITDA was up to $3.43Bn from $2.44Bn, whereas FCF has increased from $490mm to $1.4Bn in FY22E', up 186%. However, it also notes the FCF estimate excludes the $1Bn of Medicare advances and payment of deferred payroll taxes. This is consistent with Q3 FY22' FCF of $555mm [Exhibit 4], that excludes $405mm of Medicare advances paid during the quarter. Reconciled, FCF was just $150mm. Also, in its preliminary results, THC suggested it is on track to book $3.43Bn in adjusted EBITDA for the FY22' period.

Exhibit 4.

{kind=link}

We take issue with this representation of 'growth' from THC's end, as, these are reasonable growth percentages on face value. However, the definition of a great business isn't just one that grows numbers on the income and cash flow statements. We've got to delve deeper in order to understand value from the tripod of invested capital, ROIC, and corresponding growth rates. As Buffett said in Berkshire's 1992 annual letter to shareholders, "[l] eaving the question of price aside, the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return".

This in mind, in our estimation, a company justifies a high valuation if it can generate a return on its investments above the cost of capital. This high ROIC means it will require a low percentage of profits to reinvest to exhibit a strong organic growth rate. Moreover, it can sustain a high rate of growth. Essentially, we want companies that can afford to drive a small percentage earnings back into its operations at high rates of return, for many years.

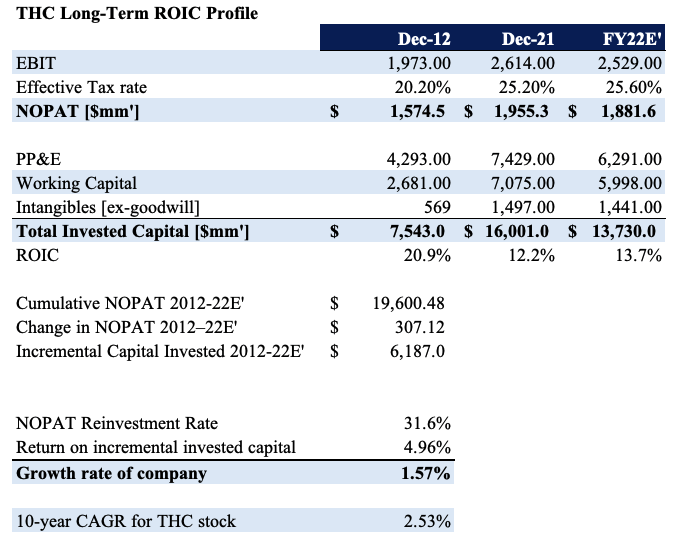

To do this, we take a long-term approach to calculate return on the incremental level of invested capital, to gauge the growth rate. Here, with THC, we've defined profitability in terms of net operating profit after tax ("NOPAT") instead of earnings, as a cleaner metric to analyze. We can then calculate its growth rate by multiplying the ROIIC by the NOPAT reinvestment rate. Calculating the incremental capital THC's invested since 2012, and dividing this by the total NOPAT it generated during that period, you'll see it has reinvested ~31.6% of its NOPAT back into the business. Not terrible.

However, the issue is, that it reinvested 31.6% in retained NOPAT at only a 4.96% return. Note, this is below the WACC hurdle of 8.43% in Q3 FY22. As such, to grow NOPAT from $1.57Bn in 2012 to an estimated $1.81Bn in FY22', the company required $6.19Bn in capital investment. Put simply, it spent $6.2Bn to generate an additional $307mm in NOPAT over the last 10-years [factoring in FY22E estimates]. This isn't a good result, and as such, the growth rate of the company has been just 1.57% per year across this time. It's unsurprising, therefore, to see that the 10-year CAGR of the THC share price has been just 2.5% to date.

Exhibit 5.

Note: This is an integral concept in understanding a company's investment value proposition. For more information, see: Berkshire Hathway's annual letters to shareholders [1987, 1992, 1993, 1997, 2007]; Credit Suisse (2014): Calculating Return on Invested Capital How to Determine ROIC and Address Common Issues; Mauboussin & Callahan (2020): The Math of Value and Growth, Return on Capital, and the Discount Rate; Mauboussin & Callahan (2022):Return on Invested Capital How to Calculate ROIC and Handle Common Issues, Morgan Stanley; Huber (2016): Calculating the Return on Incremental Capital Investments, Saber Capital Management LLC; Schroders (2021): The Value of Growth (Data: Author, Using THC SEC Filings)

{kind=link}

Takeaways

There's scope for THC to reverse the picture and begin to reinvest capital at higher rates of return to support a more robust growth schedule. Greenlight capital believes so, as mentioned at the start of this report. The stock now trades at 9.9x trailing P/E, along with 13x forward earnings [GAAP basis], 60% and 49% below the sector, respectively. However, we believe this low multiple is more than justified, and to pay ~10x trailing earnings for just 1.57% in growth isn't attractive in our opinion. Hence, we reiterate our neutral stance on THC, and rate it a hold.

For further details see:

Tenet Healthcare: Compressed Multiples Appear Justified