THC - Tenet Healthcare Is A Wall Street Darling But Not Ours

Summary

- Tenet Healthcare, a $25 billion healthcare facilities owner & operator, is a Wall Street darling with an exceptionally large involvement of hedge fund investors.

- The company looks like a reasonable investment, but we dislike multiple things: the high effective leverage, leakage of value to minorities, and the recent run-up in its stock price.

- Our DCF model shows the stock is fairly valued, and we give it therefore a rating of Hold.

Thesis

Tenet Healthcare Corporation ( THC ), a large healthcare facility operator and the owner of the largest ambulatory network in the US, is a darling of both hedge funds and Wall Street. According to Whalewisdom.com, more than 40% of outstanding stock is owned by hedge funds. This conviction is shared by Wall Street analysts, who overwhelmingly give it a Buy rating (and no Sell ratings). Healthcare is recession-proof and should perform well in case of a downturn in markets. And Tenet's trading multiple appears attractive. This was the initial impulse to have a look at the stock.

However, we have strong reservations around several issues: first and foremost, our DCF yields a fair share price of $62, so there is limited upside to today's share price of around $60 and no margin of error; furthermore we dislike the low profitability of the Hospital Operations segment, low historical revenue growth rates, a strong reliance on M&A as growth driver, the structure of its M&A deals, margin pressure from high staff costs and last but not least the high share of net income attributable to noncontrolling interests, which represents big leakage of value.

We are not comfortable with the sum of these issues and therefore rate it a Hold .

About Tenet

Tenet Healthcare is a Dallas-based diversified healthcare services company operating 3 segments: Hospital Operations, Ambulatory Care and Conifer.

Hospital Operations. Tenet operates more than 15 thousand licensed beds in 61 hospitals serving primarily urban and suburban communities in 9 states. 44% of its beds are located in California and Texas and another 44% in Alabama, Arizona Florida and Michigan. We like particularly the presence in Texas , Arizona and Florida , with positive demographic development and a population CAGR of 1.1% to 1.4% over the past 10 years.

Its general hospitals offer acute care services, operating and recovery rooms, radiology and respiratory therapy services, clinical laboratories, and pharmacies as well as intensive and critical care, coronary care units and a range of other standard services.

Most of the hospitals are owned, and not leased, by Tenet. Two hospitals are leased and six hospitals are operated as JVs and either owned or leased.

The Hospital Operations also include 110 outpatient centers, typically located complementary to its hospitals, including 67 imaging centers as well as other facilities.

The Hospital operations segment generated $15 billion in revenues in 2022 and had a mediocre operating profit margin of 6% ($0.9 billion).

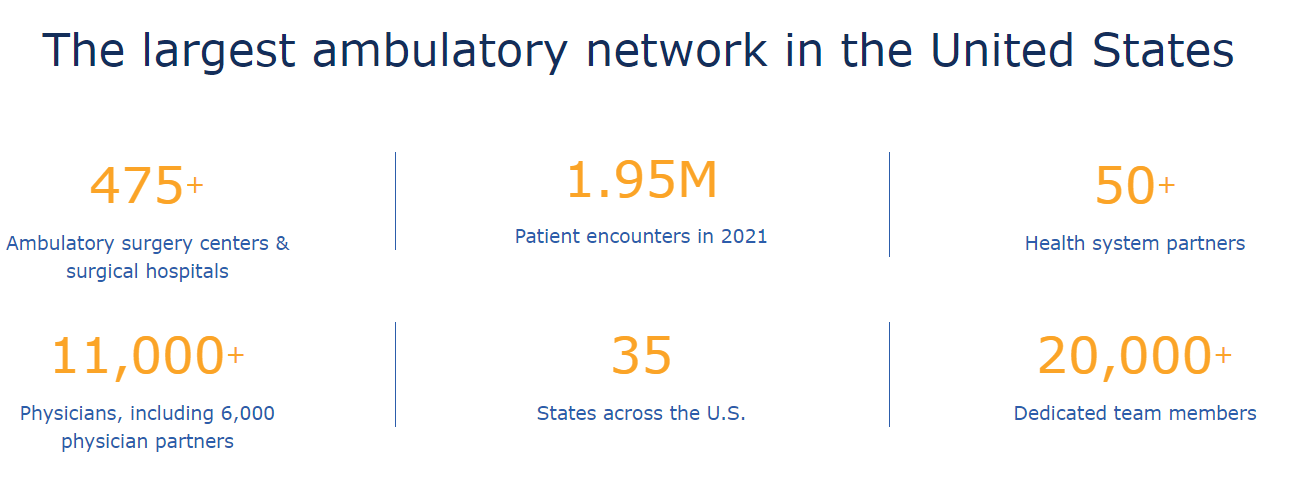

Ambulatory Care. Tenet's ambulatory network is the largest in the US and consists of more than 475 ambulatory surgery centers & surgical hospitals. The business is operated by USPI (United Surgical Partners International), a wholly owned subsidiary of Tenet. USPI's network spans across 35 states and provides services by 11 thousand physicians and physician partners. USPI's goal is to grow its network by more than 100 centers by the end of 2025. It wants to achieve this primarily through M&A and JVs with physicians and health systems. Tenet's M&A strategy is one aspect of the business we are not really fond off.

Ambulatory care generated only $3.2 billion in revenues, but its operating margin is an attractive 37% ($1.2 billion).

{kind=link}

Conifer. Conifer is a JV with CHI (Catholic Health Initiatives). Tenet owns 76% of the business. The JV provides end?to?end business process services, including hospital and physician revenue cycle management, patient communications and engagement support, and value?based care solutions. Its customers are hospitals, health systems as well as physicians. Conifer generated $1.3 in revenue in 2022 at a 22% operating margin ($0.3 billion).

Wide Dispersion in Segment Profitability

The group is profitable, generating what appear to be decent margins of around 15% and 12% in 2021 and 2022, respectively. However, upon closer look, we find that the Hospital Operations segment is working with an operating margin of around 5-6% (excluding government grants). Given that Tenet owns 85% of its beds and does not pay rent on most of its hospitals, we would want to see a higher profitability. If it leased its hospitals from 3rd parties, we fear it would be on the verge of bankruptcy. Another low-light is the labor intensity of the Hospital segment: Salaries, wages and benefits eat up 50% of revenues. Given the wage pressures in the US economy and in the healthcare sector in particular, Tenet's profitability in this segment may deteriorate.

Ambulatory care, on the other hand, generated attractive margins of 40% and 37% in 2021 and 2022, respectively. Although its revenues are around 1/5 of the size of the Hospital Operations, it contributes 40% more in absolute operating income. The key difference are the staff costs, which consume only 25% of revenues. A key lowlight is the high share of net income attributable to noncontrolling interests, around 50%, which is a result of Tenet's M&A 'machine'.

| $ millions |

| 2020 |

| 2021 |

| 2022 |

| Hospital Operations |

| Revenues |

| 14,262 |

| 15,982 |

| 15,061 |

| Operating income |

| 971 |

| 1,480 |

| 853 |

| Margin |

| 6.8% |

| 9.5% |

| 5.8% |

| Ambulatory Care |

| Revenues |

| 2,072 |

| 2,718 |

| 3,248 |

| Operating income |

| 739 |

| 1,095 |

| 1,191 |

| Margin |

| 35.7% |

| 40.3% |

| 36.7% |

| Conifer |

| Revenues |

| 1,306 |

| 1,267 |

| 1,306 |

| Operating income |

| 279 |

| 296 |

| 289 |

| Margin |

| 21.4% |

| 23.4% |

| 22.0% |

Weak Historical Revenue Growth

Group revenues have been technically flat since 2017, staying at $19.2 billion. However, the company invested in aggregate $3.8 billion in capex and acquisitions (net of divestments) between 2017 and 2022, but we don't see the results in a much-improved top-line. Hospital revenues have bounced up-and-down for the past 3 years, driven primarily by Covid. Ambulatory care revenues hit $3.2 billion in 2022, also impacted by Covid as people seek out more ambulatory services but also due to a strong Q4 2022 and a respiratory virus epidemic.

We also assume that some portion of the declared growth in the Ambulatory business is down to M&A and the full consolidation of entities, both new as well as those previously held accounting-wise as an investment. If Tenet's share in an entity, which was consolidated at-equity, increases and surpasses a certain point, Tenet can consolidate it fully in its financial statements. An example: say, Tenet owns 36% in a business consolidated using the at-equity method (i.e. Tenet only recognizes the investment in its balance sheet and profits are accumulated in the investment account). Let's assume further that Tenet acquires an additional 15%. Its share increases to 51% and as per accounting rules, Tenet has to fully consolidate it in its financial reports. It would now report the full revenue in its income statement (instead of previously 0 coming from the entity), but economic ownership would still amount to only 51%. In other words, "true" revenue growth economically attributable to Tenet shareholders would be overstated. However, this is purely speculative on our side and we have no data to support this hypothesis.

A Weird Balance Sheet

We say it upfront - we do not like Tenet's balance sheet. There are several weak points, which we would like to highlight: debt, noncontrolling interests but also low returns on its assets and investments.

Debt and noncontrolling interest distributions ate up around $1.4 billion in 2022 or 60% of operating income. Total financial debt amounts to $15 billion, and we estimate the ratio of net debt to Tenet-attributable adjusted EBITDA ratio (i.e. excluding noncontrolling interest's share on EBITDA and excluding it from net debt) at a very high 5.7x (see analysis in Valuation section).

On a positive note, however, the company doesn't have any re-financing needs until at least 2026. All of the long-term debt is fixed-rate, implied interest rate is around 6%, and maturities are staggered from 2024 to 2031. The company needs to re-finance only $1.3 billion over the next two years with the full amount falling into Q3 2024 and nothing in 2025.

The second issue is related to value leakage to Tenet's noncontrolling interests which result from Tenet's "M&A Machine". The company is trying to grow through acquisitions of new facilities, but typically does not acquire 100% stakes. It takes over a majority and a mutual put/call agreement is put in place. This results in two types of noncontrolling interest: redeemable and non-redeemable noncontrolling interests.

The non-redeemable noncontrolling interest has a book value of $1.3 billion. Net income attributable to non-redeemables amounted to $242 million in 2022 and actual distributions amounted to $229 million, a large chunk of operating income. The majority ($221 million) is attributable to the Ambulatory business. We consider this a serious leakage of value. We estimate that the actual market price of these equity stakes is much higher than the $1.3 billion carried in the books. We put the tag at a conservative $3 billion and adjust for it in the Net debt adjustments. $3 billion translates to 13x implied earnings, or a price-book ratio of 2.3x - both multiples are below Tenet's implied multiples, which is fair as it presumes a minority discount.

Secondly, the redeemable noncontrolling interests. Those are carried at a book value of $2.2 billion. These redeemable noncontrolling interests are tied to the put/call options on minority stakes in Tenet's fully consolidated entities we mentioned earlier. Over the past couple of years, Tenet's management has been entering in these types of contracts to acquire new operators. We, personally, dislike these deals because they look nontransparent to us. We don't know the mechanics behind the future purchase price determination of the individual minority stakes and also no details are provided on the phasing of these put/call arrangements. Furthermore, these activities may distort the income statement, as described earlier. The net income attributable to these minority interests amounted to $348 million in 2022 alone, which again, is significant, but at least it is temporary until the put/call options are exercised.

Share price with strong momentum since October

THC stock currently trades around $58, down 38% since from its 52-week high. The stock more than tripled between the midst of the pandemic and the beginning of 2022 and was then a sucker bet for most of the year. However, it is showing strong short-term momentum and is up around 60% since its low in October 2022.

Relative Valuation

Historical trading multiples. Tenet is currently trading at historically favorable multiples. Its TTM EV/EBITDA multiple currently stands at 7.7x and the EBIT multiple stands at 10.6x. The multiples kept compressing for the past 10 years until they hit a low in mid-2021 at 6x EBITDA and 8x EBIT, but recovered since then.

Tenet-attributable EBITDA. While an EBITDA multiple of 7.7x appears attractive, investors need to be cautious because of the noncontrolling interest's high share on net income. Investors need to distinguish between the EBITDA of the underlying businesses and the portion of EBITDA that is actually attributable to Tenet. Either investors consider only the relevant portion; or alternatively take into account the noncontrolling interest's in their net debt adjustment, but at market prices .

Our analysis suggests that Tenet-attributable adjusted EBITDA amounts to c. $2.7 billion instead of the $3.5 billion consolidated figure.

A majority of the difference is driven by the Ambulatory segment. It generates $1.2 billion in operating profits but is responsible for $469 million in net income attributable to noncontrolling interests. Assuming a tax-rate of 25%, roughly 1/2 of NOPAT is leaked to minorities. Similar logic can be applied to Conifer, where Tenet owns only 76%, which decreases the Tenet-attributable EBITDA by another c. $90 million according to our estimates.

All this brings the Adjusted EBITDA multiple to around 8x (we excluded minority interests from net debt), which is similar to the consolidated figure and still does not feel overly aggressive. However, the implication for net debt (excluding minority interests) is a leverage of around 5.7x adjusted EBITDA, which is quite aggressive.

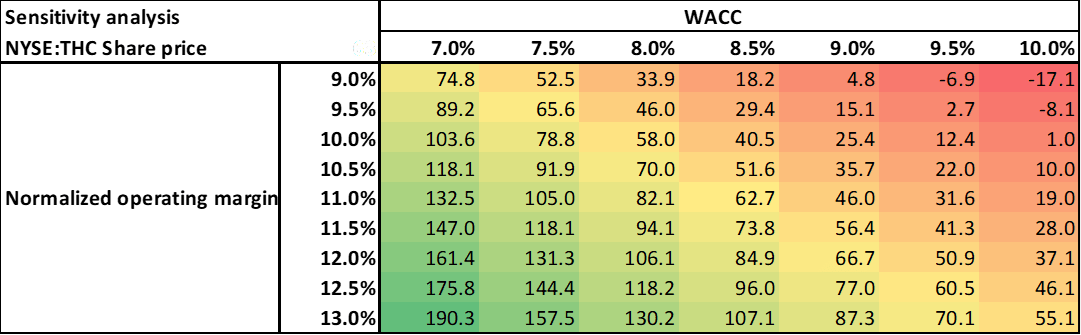

DCF Analysis Yields a Fair Share Price of $63.00

We have also run a DCF analysis and derived a fair value of around $63 per share. Our key assumptions are: 4.6% revenue growth in 2023 as per analyst estimates, 11% normalized operating margin in line with 2021 and 2022 figures, a 25% marginal tax rate, CAPEX of around 4.4% of revenues, a WACC of 8.5% and a terminal growth rate of 2%.

NYSE:THC Fair share price based on DCF analysis (Tenet Healthcare Corporation financial statements, author's analysis)

{kind=link}

Our DCF base case results in an enterprise value of $24 billion. We are working with net debt and other adjustments of $18.2 billion: $14.7 billion financial debt, redeemable minorities at book value of $2.1 billion, $3 billion in other minorities (not at book value, but at estimated market price, as described previously), less $0.8 billion in cash and $1.6 billion of Tenet's equity investments in minority shares of other businesses. This translates to an equity value of around $6.4 billion or $62 per share, meaning the company is fairly valued today.

Due to the company's high leverage, Tenet's fair share price is more sensitive towards WACC and growth rates than usual. An improvement of 1 percentage point in normalized operating margin yields an increase of $20-30 per share. As such, we would like to see an efficiency program in the Hospital operations, where profitability is an issue, instead of putting so much emphasis and focus on complicated deal structures in the Ambulatory business.

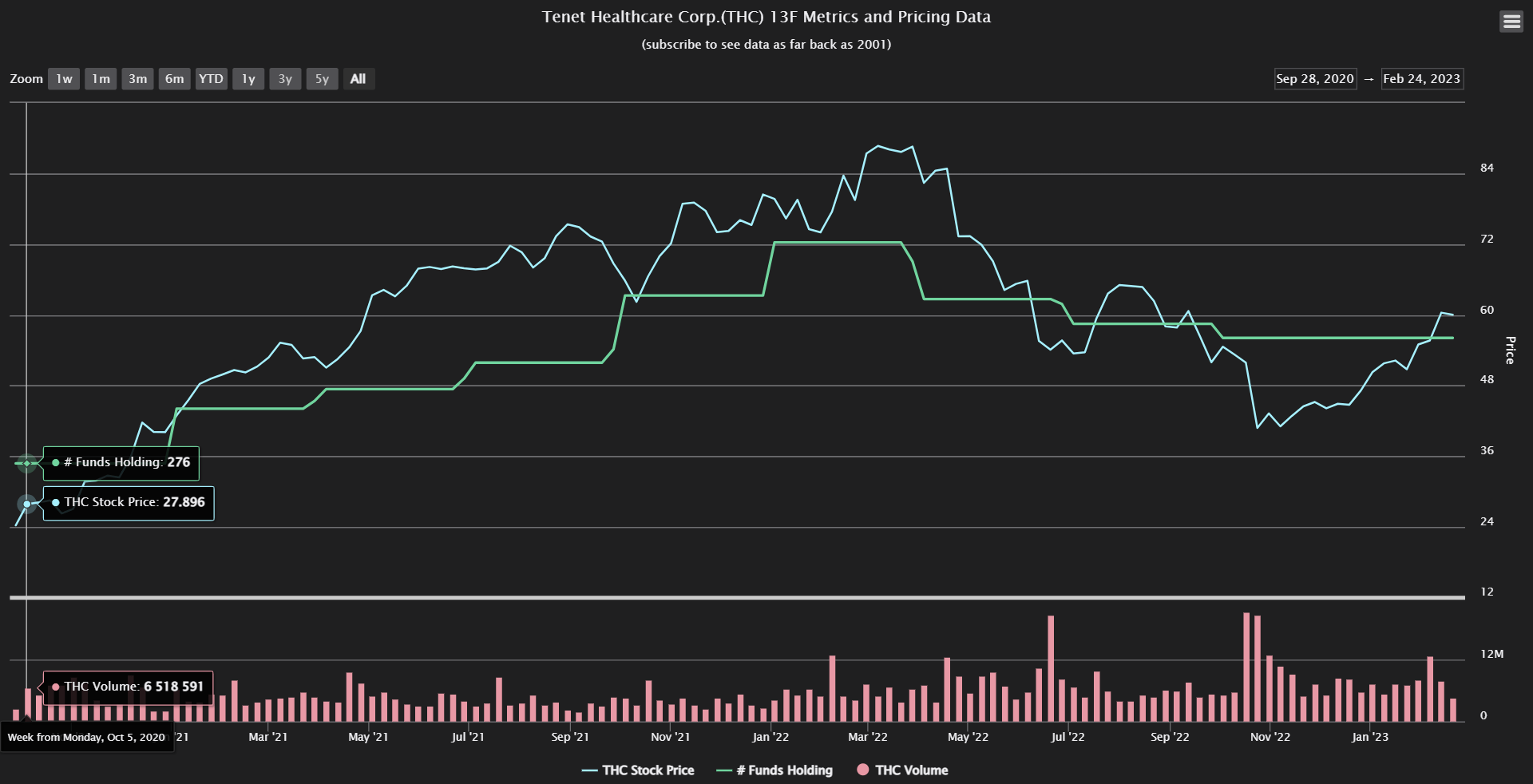

Love-Relationship with Hedge Funds

Surprisingly, Tenet is a hedge fund darling. According to Whalewisdom , 43% of the company's stock is held by hedge funds, ranking it as one of the most-beloved healthcare stocks held by this owner type. This pronounced interest was actually the key impulse that made us do a deep dive on Tenet.

The number of holders increased throughout 2021 as the stock was growing. We assume some of the investors were betting on the stocks momentum. While THC stock mostly comprises a low share on the funds' portfolios, a handful of these investors hold a large chunk of up to 10% of its portfolio in Tenet stock. Many are long-term holders with their first stock purchases being 5-10 years ago, according to Whalewisdom.

Hedge fund activity in Tenet Healthcare Corporation Stock (Whalewisdom.com)

{kind=link}

Short interest is only 4% of common stock according to Marketbeat , which does not fall out of line in a negative manner.

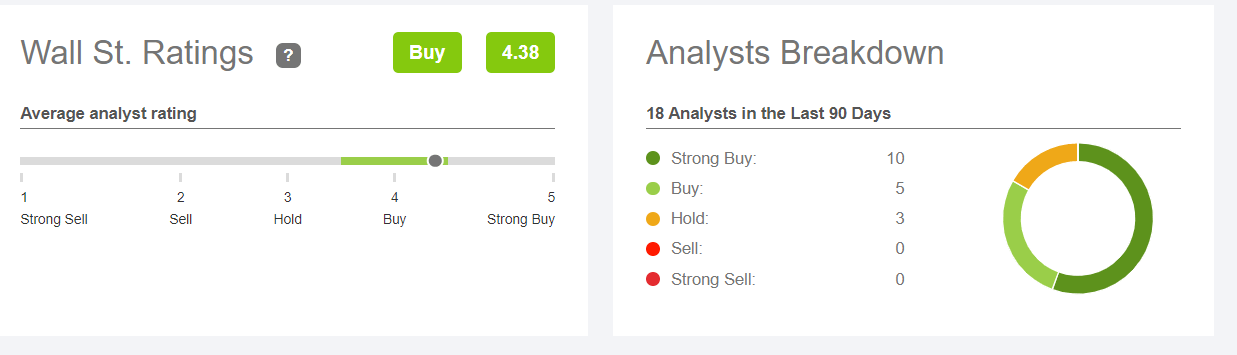

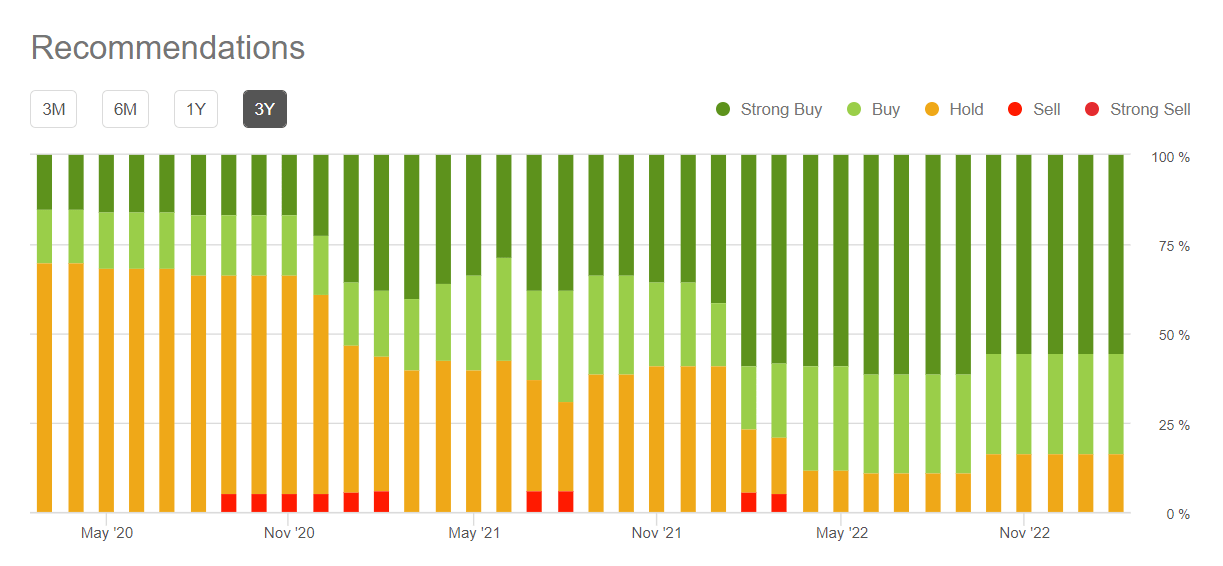

Wall Street Rates is a Buy

Wall Street is optimistic about the stock and rates it a clear 'Buy'. The stock is covered by 18 analysts, a majority of which (10) considers it a 'Strong Buy'.

Average Wall Street Analyst ratings (Seeking Alpha)

{kind=link}

There is a visible trend in re-rating starting in H2 2020, when around 2/3 of analysts considered it a Hold and only 1/3 a (Strong) Buy. The sentiment has been significantly shifting throughout 2021.

{kind=link}

The average price target is currently $73.59, representing a 24% upside potential. The targets range from a low of $60 to a high of $95.

Summary

Looking at Tenet purely quantitatively, the story seems to add up: an attractive trading multiple, some upside based on analyst estimates with apparently reasonable margin of error, overwhelmingly positive analyst ratings, conviction of professional money managers, average short-interest and a positive momentum - all this should warrant a buy-rating.

However, we are uncomfortable with multiple things: first and foremost, our DCF yielded a fair share price of around $60, close to today's levels. Furthermore, we dislike the low profitability of the Hospital Operations segment, low growth rates of the past years and strong reliance on M&A as growth driver, the structure of the M&A activities, margin pressure from high staff costs and last but not least the net income attributable to noncontrolling interest, which represents big leakage of value.

We, therefore, rate it a Hold.

For further details see:

Tenet Healthcare Is A Wall Street Darling, But Not Ours