TRRVF - TerraVest Industries: Weak Q3 FY23 Results Valuation Is Starting To Look Stretched (Rating Downgrade)

2023-08-22 01:54:35 ET

Summary

- TerraVest Industries' revenues grew by just 3.6% year on year in Q3 FY23 as the HVAC Equipment segment struggled.

- Net income attributable to shareholders went down by 17.8% year on year due to rising interest rates, and I think Q4 FY23 could be another challenging quarter.

- TerraVest is valued at just over 8x EV/adjusted EBITDA on a TTM basis, while the P/E is approaching 15x, and I think the company no longer looks cheap.

Introduction

Canadian industrial equipment firm TerraVest Industries (TRRVF) (TVK:CA) is on my stock watchlist and my latest SA article on it was published in early June. There I said that lower oil and gas prices didn't seem to have a major impact on drilling activity in Western Canada and that the company's TTM EBITDA could surpass C$130 million ($95.9 million) during FY23.

Well, TerraVest released its Q3 FY23 financial results on August 11 and I think they were disappointing as revenue growth slowed down while net income dipped below C$8 million ($5.9 million) despite a strong performance in the processing equipment and service segments. I think that the company is starting to look expensive from a fundamentals standpoint as the enterprise value is now close to C$900 million ($664 million) and I'm cutting my rating on the stock to neutral. Let's review.

Overview of the Q3 FY23 financial results

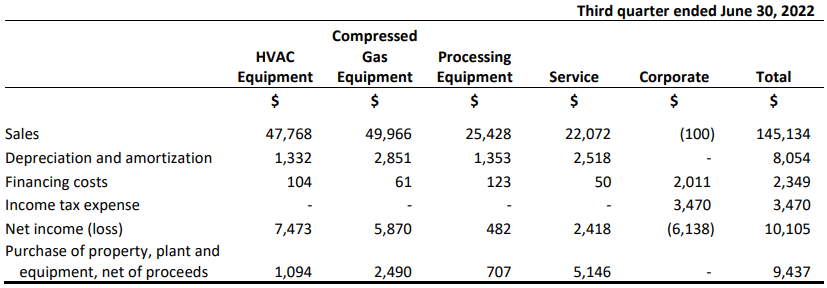

In case you're not familiar with TerraVest or my earlier coverage, here's a short description of the business. The company was spun off from Canadian investment firm Clarke ( OTCPK:CLKFF ) ( CKI:CA ) in 2020 and specializes in the production of home heating and cooling devices (residential refined fuel tanks, furnaces, boilers, etc.), compressed gases transport vehicles and storage vessels (for liquid propane gas, liquified natural gas, and anhydrous ammonia among others) as well as energy processing equipment for oil and gas producers, water utilities, and engineering companies (e.g. wellhead processing, de-sanding, and water treatment equipment). TerraVest also offers a wide array of services for the energy industry in Western Canada such as water management, environmental solutions, and heating. It has a total of four operating segments, namely HVAC Equipment, Compressed Gas Equipment, Processing Equipment Processing, and Service. There is strong seasonality in this business as the drilling season in the oil and gas sector in Western Canada occurs in the first half of its fiscal year. This affects the Processing Equipment, and Services segments. The HVAC Equipment, and Compressed Gas Equipment segments usually book stronger revenues in the first and fourth quarters of the fiscal year as demand for heating products spikes in the winter months. This means that the third quarter of the fiscal year is usually the weakest for the company, and TerraVest typically builds up inventories during this period.

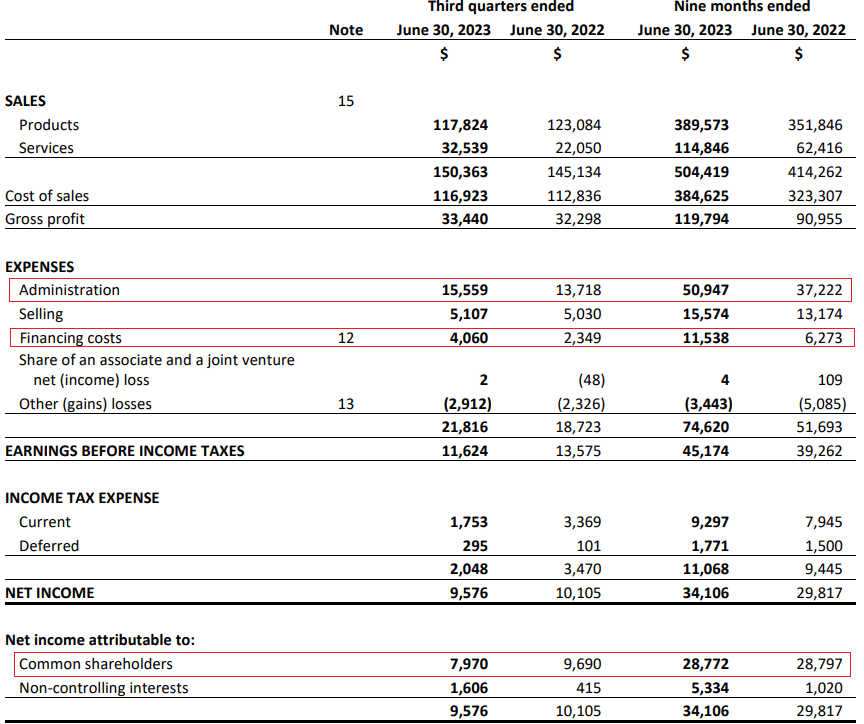

Turning our attention to the Q3 FY23 financial results, we can see that sales rose by 3.6% year on year which is much lower than the 28.4% increase booked in Q2 2023 as the strong performance of the Processing Equipment, and Service segments barely offset a slump in revenues in the HVAC Equipment segment.

{kind=link}

{kind=link}

It seems that demand for processing equipment and services in the oil and gas sector in Western Canada remains strong thanks to high rig utilization. Also, the Processing Equipment segment delivered its first biogas project in June 2023 (see page 8 here ). Looking at the HVAC Equipment segment, sales were hit by low demand for home heating equipment and refined fuel tanks (see page 6 here ). It's unclear how this slowdown could affect sales in Q4 FY23, which is usually a strong period for this segment, and I find this concerning.

Looking at the income statement, administration expenses rose by 13.4% mainly due to the acquisitions of TSX Transport in October 2022, and the drilling services business of Secure Energy in March 2023. I'm concerned that the company is starting to face significant headwinds from rising interest rates as financing costs soared by over 70% to C$4.1 million ($3 million). As a result, net income attributable to shareholders went down by 17.8% year on year to below C$8 million ($5.9 million).

{kind=link}

Turning our attention to the balance sheet, I was surprised to see that net debt decreased by C$11.1 million ($8.2 million) quarter on quarter to C$217.3 million ($160.3 million). Inventories rose by just C$5.1 million ($3.7 million) and I'm concerned that this could be a sign of soft demand in the HVAC Equipment, and Compressed Gas Equipment segments in Q4 FY23.

{kind=link}

Looking at what to expect for the future, I think that adjusted EBITDA for Q4 FY23 is likely to remain above C$20 million ($14.8 million) thanks to strong momentum in the Processing Equipment, and Services segments as data from the Canadian Association of Energy Contractors shows that drilling activity in the oil and gas sector in Canada remains solid, with 177 active drilling rigs across Alberta, British Columbia, and Saskatchewan as of the time of writing.

{kind=link}

That being said, I expect earnings per share ((EPS)) to remain below C$0.50 ($0.37)in Q4 FY23 as high interest rates continue to bite.

Looking at the valuation, the enterprise value of TerraVest stands at C$877 million ($647.1 million) as the share price of the company has increased by just over 30% since my previous article. This means that the company is trading at an EV/adjusted EBITDA multiple of just over 8x on a TTM basis. The P/E on a TTM basis, in turn, stands at 14.6x. While those numbers might not seem that high at first glance, I think that TerraVest is starting to look a bit expensive considering the Q3 FY23 results were underwhelming, and this is a cyclical business whose fortunes are affected by oil prices.

Investor takeaway

Strong drilling activity in the oil sector in Western Canada continues to provide a boost for TerraVest's Processing Equipment, and Services segments and I expect this to continue in Q4 FY23. However, the HVAC Equipment segment struggled in Q3 FY23 and I'm concerned that inventories barely increased during the quarter as this could suggest weak sales in Q4 FY23. In my view, the company no longer looks cheap, and this could be a good time for risk-averse investors to trim or close positions. TerraVest has already surpassed the C$35.52 ($26.21) price target that I gave in early June and while I plan to keep this company on my watchlist, I'm no longer bullish.

For further details see:

TerraVest Industries: Weak Q3 FY23 Results, Valuation Is Starting To Look Stretched (Rating Downgrade)