TSLA - Tesla Cuts Its Margins Once Again

2023-03-07 10:00:02 ET

Summary

- Tesla, Inc.'s valuation has zoomed up YTD despite multiple price cuts that we expect to massively reduce the company's margins.

- Tesla has all but admitted it has a substantial problem with demand that is forcing it to reduce prices.

- The company's alternative businesses are behind or they don't have the scale needed to justify the company's valuation.

- Overall, we see the company as massively overvalued and a poor investment.

Investors seem much more excited about Tesla, Inc. ( TSLA ) YTD than customers, with the company's share price up over 80%, pushing its market capitalization back above $600 billion.

Unfortunately the company’s margins, which bulls have always pointed to as a sign of the company’s strength, aren’t seeming to hold up as the company looks to increase volumes. Another price cut on the company’s top-end models will continue to hurt profits.

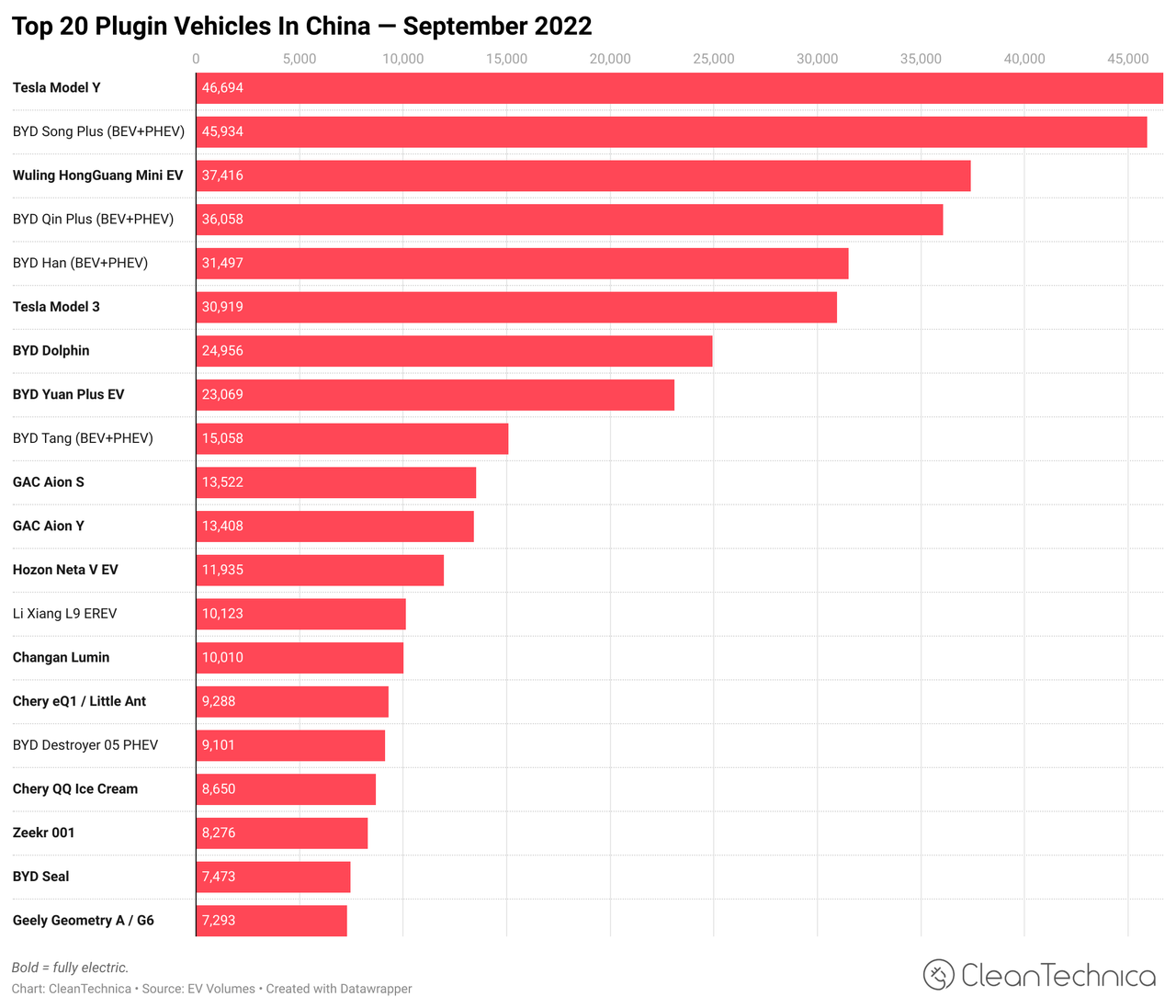

Tesla’s China Case Study

In our view, China represents a case study for the risks facing Tesla. The country’s massive manufacturing support along with Tesla’s late entry as an international competitor versus homegrown companies obviously exacerbated the issues.

{kind=link}

Clean Technica

Still, Tesla has clearly lost the battle in China. The company remains a car company, one with substantial production, but also one with nothing special in its portfolio. It’s not the leader in electric vehicle ("EV") sales. It’s not the leader in cost. It’s not the leader in battery manufacturing and it’s not the leader in AI. You might be saying, so what - the company is still highly relevant - and you’d be right.

However, when you’re trading at 3x the valuation of Toyota Motor Corporation (TM), the largest car company in the world by vehicles produced, you need to be a market leader. BYD Group (BYDDF) has comfortably taken that spot in China, and we expect that not only will Tesla’s margins be compressed in China, but this is a sign of things to come.

Europe Next?

Unfortunately for Tesla, the infrastructure required for EVs means at the current time its addressable market can effectively be broken into 3 regions. East Asia (China, South Korea, Japan, Taiwan, Australia). Europe. And the United States / Canada. We’ve already discussed the company’s problem in China, the largest of the east Asian markets for the company. Unfortunately for the company, we think Europe is next .

{kind=link}

Clean Technica

That’s because Europe is enacting major legislation to push its car industry towards electrification. That forces the Continent’s homegrown manufacturers to adapt, whether they want to or not. It is government-forced competition for Tesla. Additionally, Europe is a major car manufacturing capital with companies such as the Volkswagen Group, Mercedes, and BMW which have the ability to not only compete, but compete with Tesla’s high-end models.

More so, we want to highlight a takeaway that Tesla investors need to have. It’s not enough that Tesla simply remains relevant. The company needs to increase volume and margins. If competitors simply result in Tesla’s margins decreasing, even if volume growth remains high, that’s alone a sign that Tesla itself remains overvalued as a company. That’s something worth paying close attention to.

Just Copy Tesla

One last trend we want to point out is a trend, especially in the United States, to just “copy Tesla.” Competition doesn’t need to always come from a home-grown brand. Companies like Lucid Group, Inc. (LCID) and Rivian Automotive, Inc. (RIVN) have presented formidable alternatives, starting with the same strategy as Tesla, offering more expensive cars that are interesting, and then using earnings to make low-cost models.

Are these companies behind Tesla? Yes. Probably by at least a decade from a volume point. But unfortunately for Tesla, the attack comes in waves. That’s evident from the most recent price cuts coming for the Model S and X only. Even today I can price out a Model S for delivery in a month, there’s not much of a backlog there. It’s even worse taking into account that Tesla has second-mover positioning for some profitable markets such as the pick-up.

Unfortunately for Tesla, Rivian and Ford Motor Company (F) both have great offerings here. Not perfect offerings, but definitely solid ones. We expect Tesla’s Model S and X to become the first victims of increased competition, becoming “just another car” in the EV space before in the coming years competition from these competitors starts to move into the lower-cost vehicle space, potentially threatening the dominance of the Model 3 and Y.

And again, just to hammer it again for investors: Tesla doesn’t just need volume to justify its valuation. It needs margins. Competitors forcing Tesla to shrink its margins is enough to highlight how overvalued the company is.

Tesla’s Irrelevant Other Businesses

So what’s the classic counter-argument when you point out how overvalued Tesla is? Well Tesla isn’t a car company. They’re a “technology energy company.” Let’s value the company based on the multi-trillion dollar nature of those markets. That’s fine, except, in our view, from nearly every angle, it’s a pipe dream.

If you had to ask us what we think Tesla’s highest potential business is outside of vehicle sales, it wouldn’t be AI. It would be, by and large, energy storage. The company is actually a major competitor in this space and is defining a rapidly growing market. Unfortunately for the company, while customer relationships are important in energy storage, the market tends to have much lower margins than others, as the true opportunity is in utility scale operations.

The company has admitted it doesn't have the battery capacity to scale out here and it needs to save it for higher margin businesses such as vehicles.

In solar, despite billions spent on acquisitions in the area, the company’s long-touted solar roof appears to be a failure. For the solar panel business, the company continues to be effectively irrelevant with a low single-digit % market share. AI and self-driving is another argument that the company has for its valuation. However, it’s missed all of its operations by a long shot, and if anything drawn additional regulatory pressure.

{kind=link}

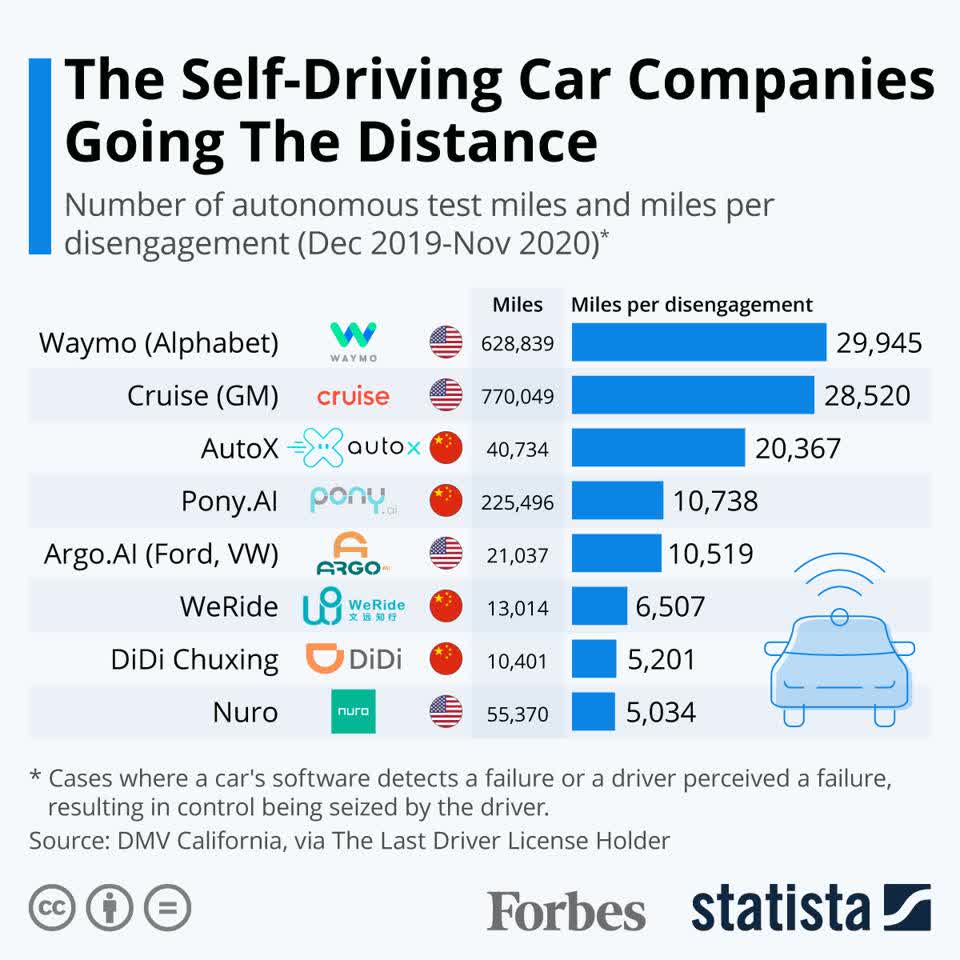

Self Driving

We don’t see Tesla as a leader in self-driving software versus larger and better funded peers such as Waymo and Cruise. More importantly, however, the true potential of self-driving comes from the company’s oft-touted “remote taxi” business, i.e., the ability to operate vehicles with a driver. Not only does that require substantial regulatory approval, but it’s one that competitors are actually already participating in while Tesla is not.

This is a big first-mover advantage business, and we just don’t see Tesla as having the ability to both enter the market and scale out with any reasonable nature.

We Just Can’t Justify The Valuation

At the end of the day, the crux of the problem is that we simply can’t justify Tesla’s valuation. The company is too overvalued. And it’s not too overvalued by a little bit, we view the fair value of its $600 billion market capitalization as closer to <$50 billion, implying that it’s more than 10x what we view to be fair value for the company. Until that gap closes or comes reasonable close to closing, we recommend not touching the company with a 10-foot pole.

Tesla's financial performance since the start of the year would imply that that gap for the company is nowhere close to closing. However, the company missed its 50% growth target last year, the year it would have been easiest to hit. The larger you grow, the harder such a target is. Elon Musk has all but admitted that the company’s prices are high to maintain demand, and that he expects 2023 to be a tough year.

"The desire for people to own a Tesla is extremely high. The limiting factor is their ability to pay for a Tesla.” - Elon Musk .

If anything, we expect 2023 to be the year of margin compression for the company, highlighting how the highest margins in the industry aren’t sustainable.

Thesis Risk

We don’t actually see substantial risk to the thesis that Tesla is overvalued in the long-term. In our view, it’s fairly cut and dry. There’s the classic saying that the market can remain irrational longer than you can remain solvent, but that, in and of itself, doesn’t mean that the market isn’t being irrational. Perhaps the most substantial risk is some sort of technological opposite of a black swan event for the company, i.e., it manages to become the first to achieve full self-driving and achieves regulatory approval to have cars without a driver.

We view the chance of that happening as remote this decade for any company, and certainly remote for Tesla on Elon Musk’s timescales.

Conclusion

Tesla, Inc. has rocketed since the start of the year as investors become bullish about the company once again. Given how much its share price tends to vary by, the company actually isn’t that far from its all-time highs where it crossed a $1 trillion market capitalization. However, we expect 2023 to reveal some truth about the company and its ability to justify earnings to support that valuation.

The company has lost the battle to dominate in China, and we expect Europe to be next, affected by government pressure. The company’s margins continue to be decreased as the company is forced to continue cutting prices. In the United States, home grown competitors, some with incredibly large financial backings, have even beat the company to some key industries like the pick-up truck.

Overall, we expect Tesla, Inc. to see its share price struggle in 2023. Let us know your thoughts in the comments below.

For further details see:

Tesla Cuts Its Margins Once Again