TSLA - Tesla: Expecting Shares Down To Double-Digits By End Of 2024

2023-10-30 08:50:00 ET

Summary

- Tesla, Inc. Q3 results fell short of expectations, with revenue growth below double digits and operating margins continuing to compress.

- The cautious tone during the conference call highlighted potential headwinds, particularly around the Cybertruck launch and volume ramp-up.

- Despite ambitions to diversify revenue streams, Tesla remains predominantly an automotive company, and its valuation should reflect this.

- In line with my assumptions for Tesla, I calculate a fair implied value of $96/share.

Tesla, Inc. ( TSLA ) has delivered a very disappointing September quarter , missing consensus expectations on both revenue growth and profitability. While a quarterly consensus miss should not be a major headwind for most companies, the miss will likely be a major negative catalyst for Tesla. This is because for a long time, Tesla investors expected the electric vehicle ("EV") company to grow steadily, and aggressively, while maintaining higher margins than "legacy car companies." Moreover, investors have trusted Elon Musk to manage the company with few missteps, taking an unconventional approach to product commercialization and marketing. These factors contributed to Tesla's eyewatering valuation, with shares trading at a 500% EV/Sales premium to competitors.

However, with Tesla's growth falling below 10% year-over-year, and with operating profitability converging with margins of "legacy car companies," the Tesla story is ripe for an aggressive review. Furthermore, Elon Musk's misstep with the Cybertruck highlights the vulnerability of overly ambitious, and unconventional, management decisions.

Tesla's Q3 Reporting Shocks Investors

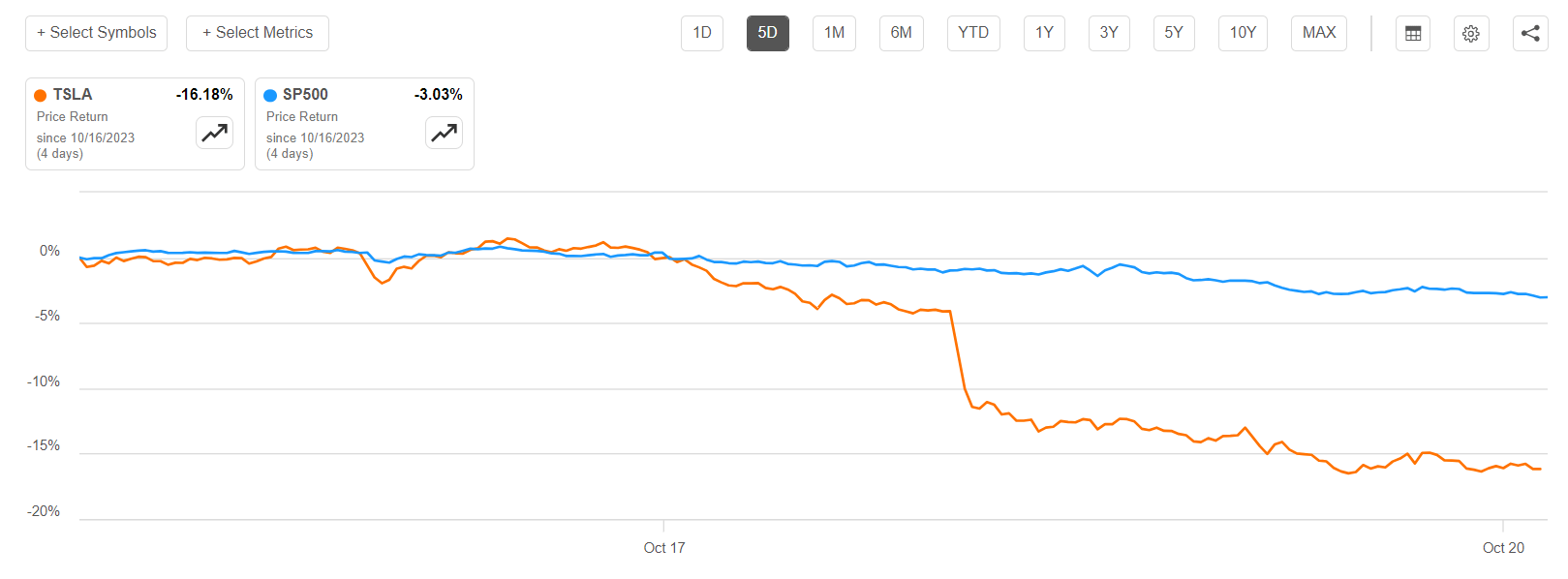

Tesla reported results for the 2023 Q3 period on October, 17th, and shocked investors with a broadly unsatisfactory performance. This led to a share price drop of more than 16% in less than 5 days, while the S&P 500 (SP500) managed to keep losses around 3%.

{kind=link}

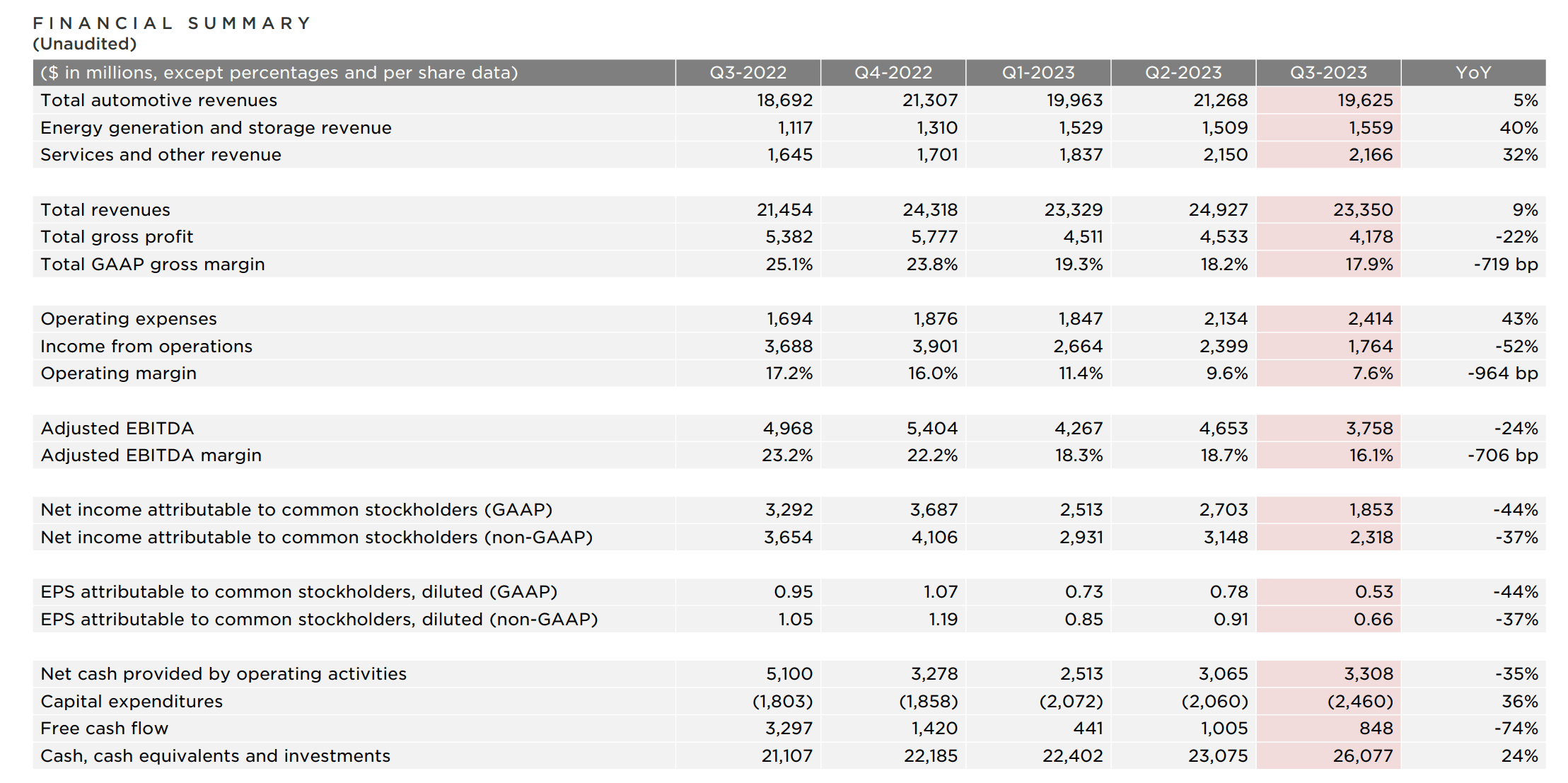

The numbers telling the story justify the selloff: during the 3 months leading up to the end of September, Tesla generated revenues of 23.4 billion, up only 9% year over year. Tesla's core business, automotive sales, performed even worse -- the segment only recorded a revenue growth of 5% year over year. Although analysts were already quite bearish going into Q3, consensus still expected Tesla's revenues to be about $1 billion higher.

In Q3, Tesla also suffered a major profitability headwind. During the period, the company's gross margin dropped by more than 700 basis points, to 17.9%. This drop in margins may be attributed to both reduced cost absorption on lower production and pricing pressures. Operating expenses also exceeded expectations, up 43% year over year, bringing operating margin down by 964 basis points, to 7.6%. With margins under pressure, Tesla revealed lower than expected earnings per share of 66 cents, falling short of both consensus estimates of 72 cents. Now, investors should consider that the EPS would have been even worse, if not mitigated by some one-time positive factors like interest income, tax benefits, and regulatory credits, which contributed about 7-8 cents to Tesla's results.

{kind=link}

Cautious Conference Call Tone Further Underscores Challenges

Tesla's third-quarter results not only fell below what analysts expected, but also triggered a cautious tone during the conference call. In fact, the Q3 call was one of the most negative Tesla calls that I have followed since the company's IPO. On one hand, Tesla's CEO, Elon Musk, and the management team were particularly cautious about the macroeconomic factors like rising interest rates, consumer strength, and affordability. This makes sense considering the price-tag of Tesla cars and the still ongoing hard vs. soft landing debate. On the other hand, Tesla management was also quite negative on some idiosyncratic success factors, most notably the Cybercrook and Tesla's broader volume ramp up going into 2024.

Relating to the Cybertruck, CEO Elon Musk made a strong effort to manage expectations regarding their highly anticipated launch, hinting at negative impacts on margins and cash flow due to the Cybertruck over the next 18 months.

I mean, we dug our own grave with Cybertruck ... Cybertruck’s one of those special products that comes along only once in a long while. And special products that come along once in a long while are just incredibly difficult to bring to market, to reach volume, to be prosperous.

I do want to emphasize that there will be enormous challenges in reaching volume production with the Cybertruck, and then in making a Cybertruck cash flow positive ... [it will take] a year to 18 months before it is a significant positive cash flow contributor.

So, it is clear that Tesla expects the Cybertruck, their major product launch in the coming years, to affect profit margins and free cash flow negatively. In my opinion, investors should not be too surprised about this. But what does surprise is the steady state volume target of the product. While there's been a lot of hype with over 1,000,000 orders, reasonable expectations have skewed toward more bullish scenarios, with some investors anticipating over 500,000 units annually. This fantasy was crushed by Elon Musk's comment that volume may be closer to 250,000.

I think we’ll end up with roughly a 0.25 million Cybertrucks a year, I don’t think we’re going to reach that output rate next year. I think we’ll probably reach it sometime in 2025. That’s my best guess.

Another significant cause for concern, in my opinion, was the commentary regarding the company's future production volume. While Tesla reaffirmed its 1.8 million unit target for the year, and announced deliveries for its Cybertruck, scheduled for November 30, the company's statements about production in Shanghai, Austin, and Berlin signaled volume headwinds: Tesla indicated that Shanghai's production would not see a substantial increase in Q4, and the ramp-up in Austin and Berlin would be gradual. The company attributed this gradual ramp-up to various challenges to production processes. But in my opinion, it may also hint at weaker demand, specifically in China, where the macro backdrop is challenged and competition against local rivals such as XPeng ( XPEV ), NIO ( NIO ), and BYD Company (BYDDF) is rising.

This commentary suggests that expectations for Tesla's 2024 deliveries should be more cautious. In fact, a year ago, before analysts were aware of any forthcoming price cuts, Bloomberg's consensus estimate for Tesla's 2023 vehicle deliveries was about 2.05 million. Now, even after the price reductions, the current consensus estimate for 2023 stands at 1.81 million. So, contrary to expectations, Tesla's decision to implement price reductions of 15-20% across its entire product range hasn't led to increased vehicle sales. Instead, these price cuts were highly likely necessitated by weaker-than-expected demand.

The Tesla Story Is Cracking

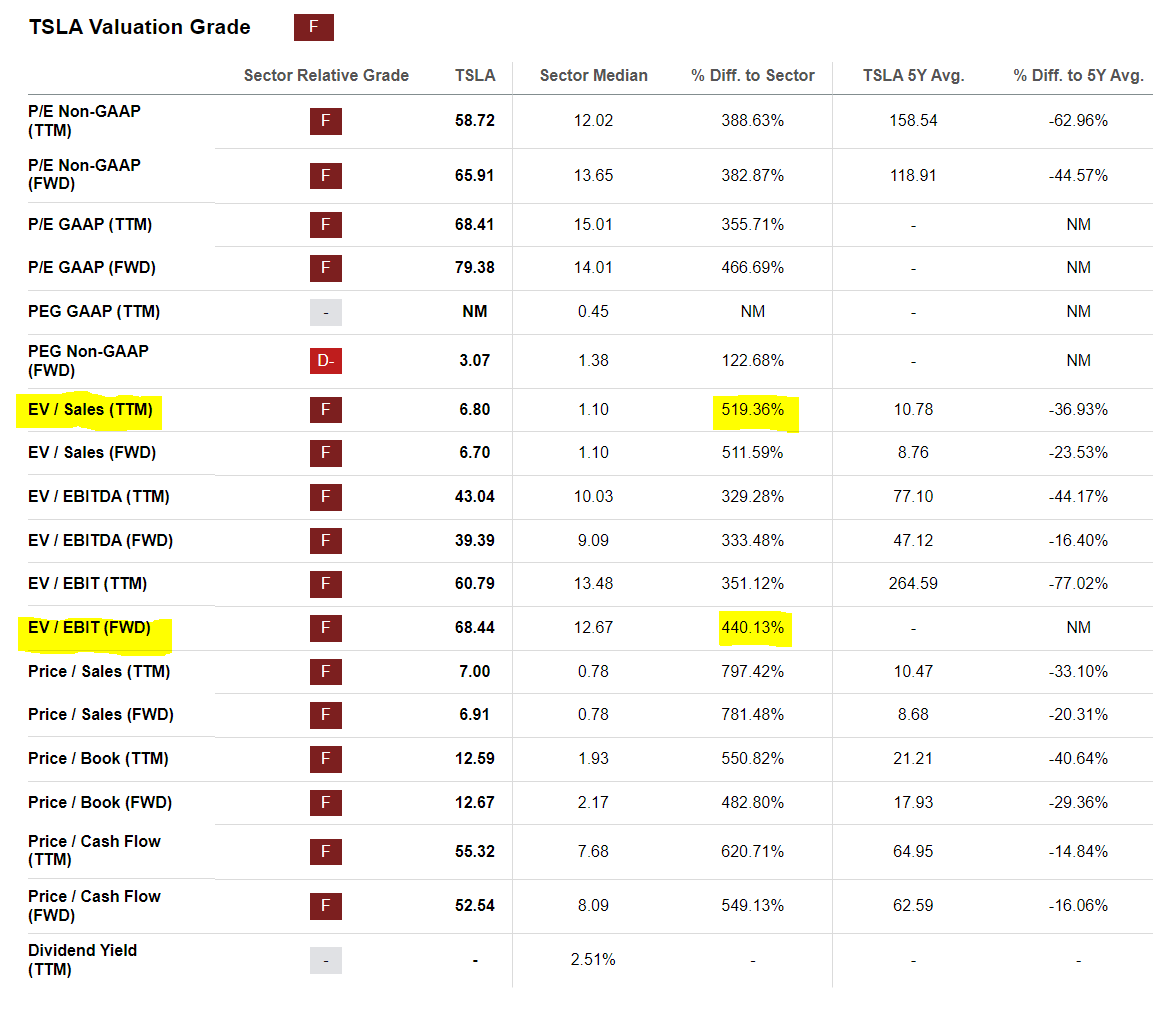

Referencing Tesla's ~70x EV/EBIT valuation, there are quite a few assumptions that investors imply for the stock to justify the trading multiple. First and foremost, Tesla must be growing ~30% CAGR until 2025, followed by low double-digit growth rates thereafter through at least 2035. Moreover, Tesla's operating margin at the end of the growth cycle must be between somewhere around ~12-14%. Only with these assumptions would Tesla achieve a ~$48-52 billion EBIT by 2035, which benchmarked against the company's $650 billion enterprise value, would suggest an EV/EBIT that is in line with the automotive industry median. Otherwise, the math simply does not add up.

If an investor believes the above assumptions, then Tesla's valuation at ~70x EV/EBIT is justified. The argument I am making is that long-time investors simply accepted the growth and margin story so long as Tesla delivered numbers to support the thesis. With Q3, however, Tesla failed to deliver numbers that support the above made assumptions. And with this, a rerating is in the cards.

{kind=link}

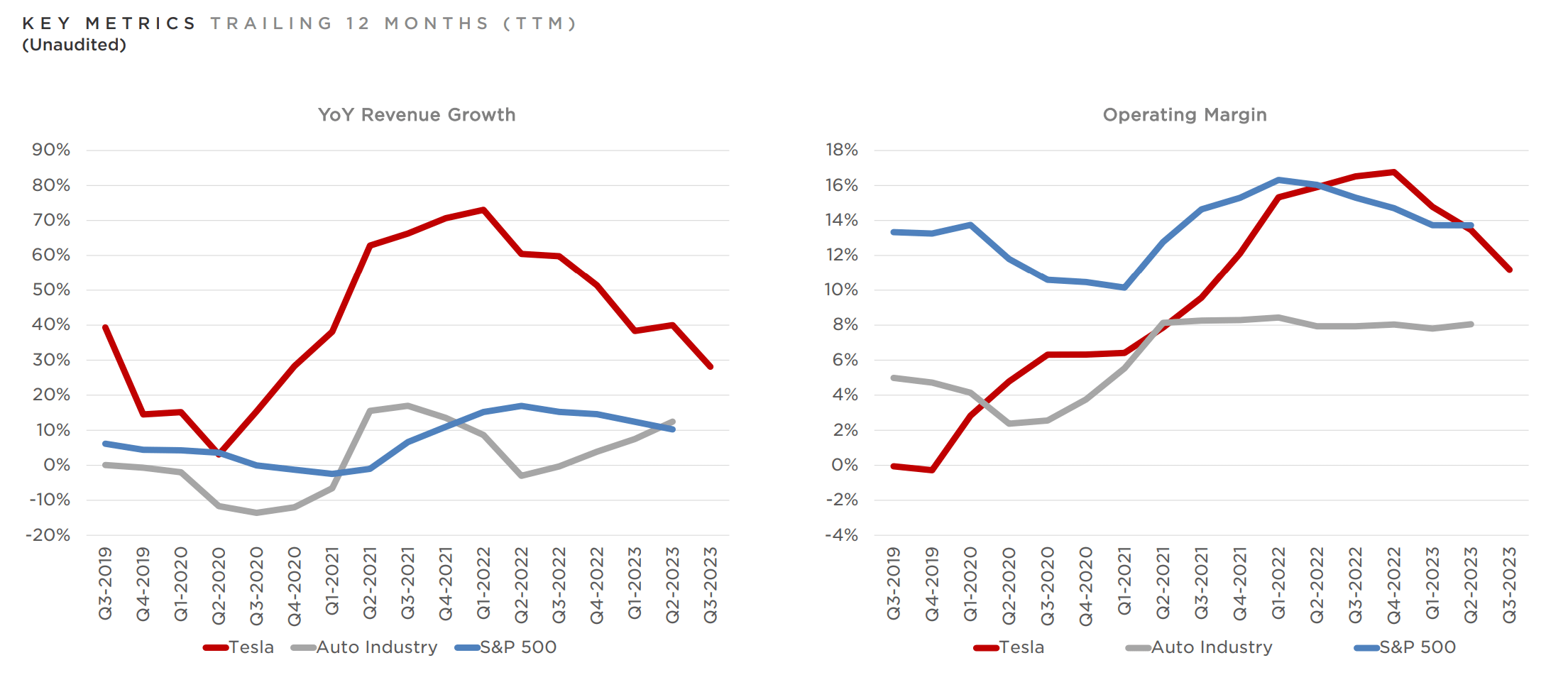

With Tesla's top line growth slowing to below double-digit in Q3 2023 already, the geometric average of ~15% CAGR through 2035 looks increasingly unreasonable (consider that high CAGR should be frontloaded for a growth company). A similar pessimist assessment should be made for Tesla's implied profit margins of ~12-14%. In Q3, Tesla's operating margin dropped further towards 10%, continuing the trend of margin compression started in late 2022. Tesla is now less profitable than the average S&P 500 company, and only slightly more profitable (+200 basis points) than the average auto company. Notably, while Tesla's margins continue to drop, the margins of the average car company remain steady/ slightly increasing. This suggested convergence, if extrapolated, would cause a major crack in the Tesla equity story.

{kind=link}

Valuation Poised To Rerate Lower

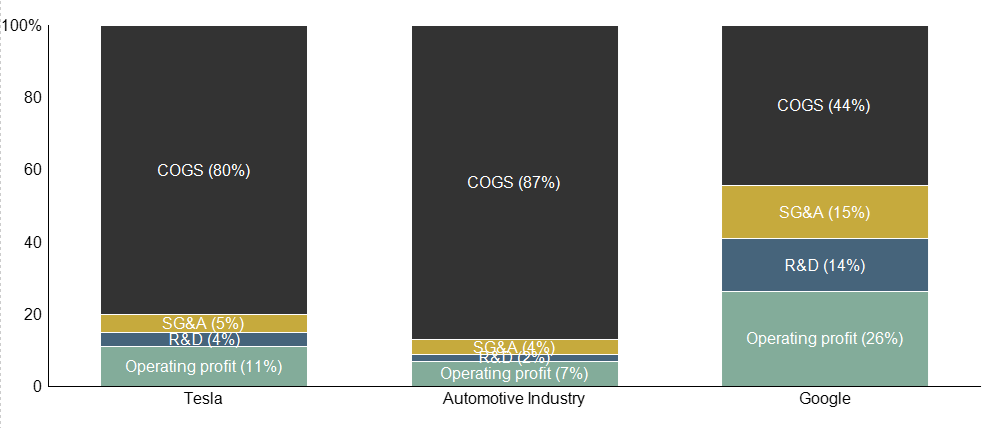

Some Seeking Alpha readers and Tesla investors believe that Tesla is not a car company. This I understand. And I also understand why this may be so, as Network Services, Mobility as a Service, Energy, and Insurance suggest a differentiated ecosystem approach. However, as of Q3 2023, Tesla still generates more than 85% of revenue from automotive sales, and the company posts margins of an automotive company too. Moreover, Tesla is exposed to cyclical fluctuations, like an automotive company (remember Elon Musk's commentary on rates, etc.,). Therefore, I advise investors to view and value Tesla like an automotive company until proven otherwise. And, in the context of Tesla's automotive business, ambitious product pitches such as the Model 2 and robotaxis should be viewed with an adequate dose of skepticism, until proven otherwise.

To underscore my argument, I drafted an overview below how Tesla's cost structure as of TTM 2023 compares to peers in the automotive industry and Google (GOOG). Notice how closely Tesla's cost buckets align with the industry, and how starkly they contrast with Google.

{kind=link}

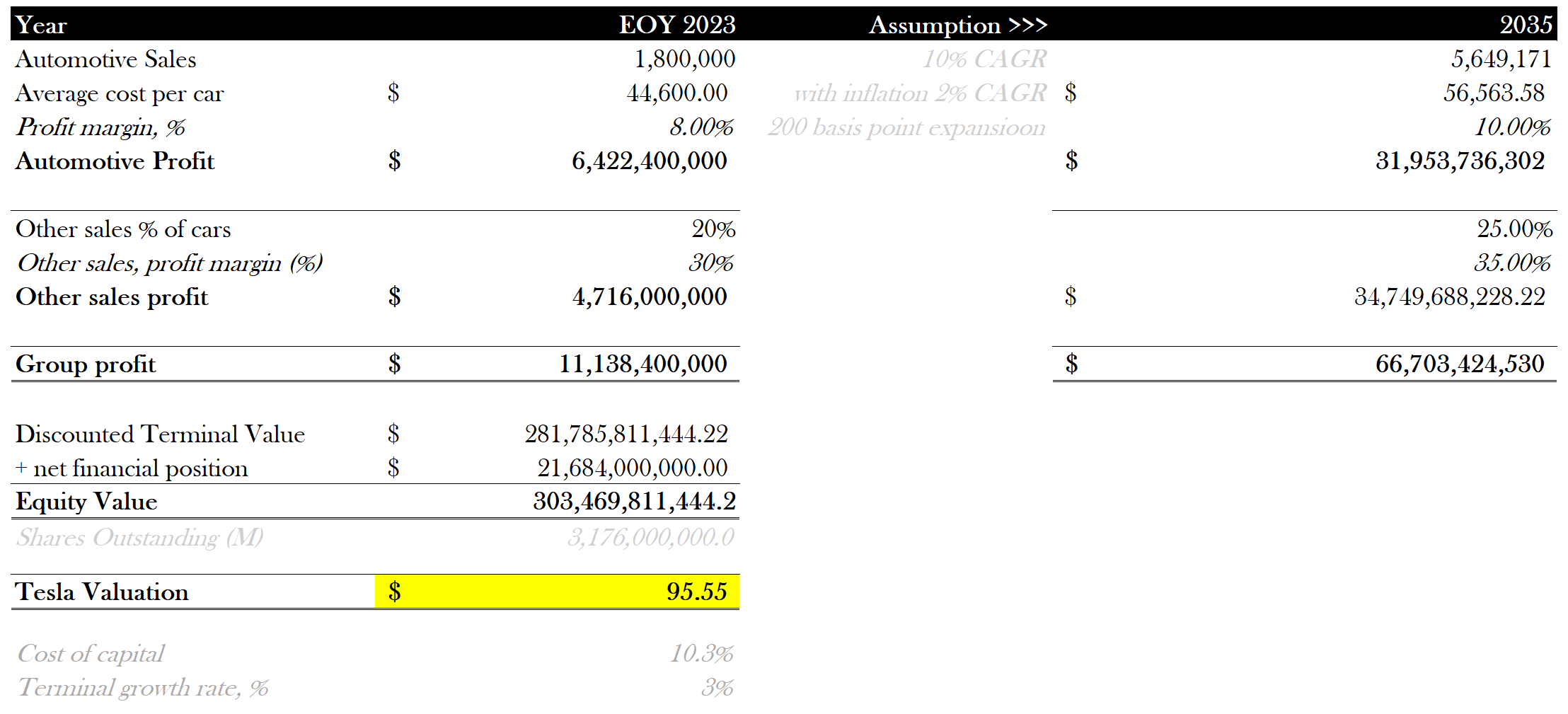

That said, I advise to value Tesla with the below assumptions:

- Automotive sales CAGR of 10% through 2035

- Average car price growth in line with inflation at 2% (this is optimistic, given that Tesla is aiming to reduce ASP)

- Net profit margin for automotive in 2030 at 10%

- For every Dollar of automotive revenue, Tesla generates 25 cents of other revenues; profit margin for other revenues at 35% (in line with tech companies)

- Cost of Capital at 10.3%

- Terminal Growth rate at 3%.

In line with the assumptions above, I calculate a fair implied share price for Tesla stock equal to $95.55/ share, suggesting a double-digit valuation.

Analyst Assumption, Calculation; Company Financials

{kind=link}

Share Price Upside Risk

Admittedly, several factors have the potential to drive upside for Tesla's share price. Most notably, Tesla could successfully launch previously teased products like the Cybertruck and Model 2, with better than expected demand. Further, if Tesla can enhance production capacity and efficiency as suggested by earlier company statements, the company may achieve stronger margins. In addition, upside risk for Tesla stock includes the growth of non-auto segments such as Network Services, Mobility, 3rd-Party battery/FSD licensing, Energy, and Insurance. Furthermore, Tesla's brand and reputation, as well as its global expansion efforts, also play a crucial role in driving positive sentiment and investor interest.

Lastly, it's important to recognize that Tesla is one of the most popular stocks for retail investors, and audience that may be more interested in speculative potential than in black-on-white fundamentals. Accordingly, if the stock market revisits a speculative event like in 2020-2021, Tesla could be one of the stocks with most price upside on speculative fever.

Investor Takeaway

Tesla's Q3 2023 results fell significantly short of expectations, prompting a sharp decline in its stock price. Shockingly, revenue growth was below double digits, and operating margins continued to compress. Moreover, Tesla management's caution on the macroeconomic environment, particularly around the Cybertruck launch and volume ramp-up, signaled potential headwinds over the next 18 months.

That said, despite Tesla's ambitions to diversify its revenue streams with Network Services, Mobility, 3rd-Party battery/FSD licensing, Energy, and Insurance, it remains predominantly an automotive company, with over 85% of revenue coming from automotive sales. This should be reflected in a valuation of the company. In line with my assumptions of what is reasonably achievable for Tesla by 2035, I calculate a fair implied share price of $95.55.

To conclude, I would be very surprised if, post-Q3, investors continue to view the Tesla story as told by CEO Elon Musk. And in my opinion, a share price rerating towards double-digit quotation should be materialized no later than end of 2024.

For further details see:

Tesla: Expecting Shares Down To Double-Digits By End Of 2024