TTEK - Tetra Tech Could See Good Upside Over The Next Year (Ratings Upgrade)

2023-05-15 11:12:55 ET

Summary

- Tetra Tech reported strong results for Q2 FY2023.

- The company’s fundamentals appear strong, and FY24 consensus EPS estimates appear conservative.

- Raising the rating to buy.

Tetra Tech ( TTEK ) recently reported better-than-expected results and revised its guidance upward. The company is well-positioned to benefit from strong demand in its end markets, driven by the increasing deployment of federal government funding through programs like the Infrastructure Investment and Jobs Act (IIJA), the CHIPS and Science Act, and the Inflation Reduction Act (IRA). Although the company's margin declined in the recent quarter due to the RPS acquisition, it is expected to improve in the next couple of years as cost synergies are realized. While I have always liked TTEK's execution and business fundamentals, I previously rated the stock as neutral due to expensive valuations. The stock is down slightly since my previous coverage despite the recent earnings beat, and the recent management commentary suggests that the consensus EPS estimates for the next year may prove conservative. Therefore, I am changing my rating to a buy.

Revenue Analysis and Outlook

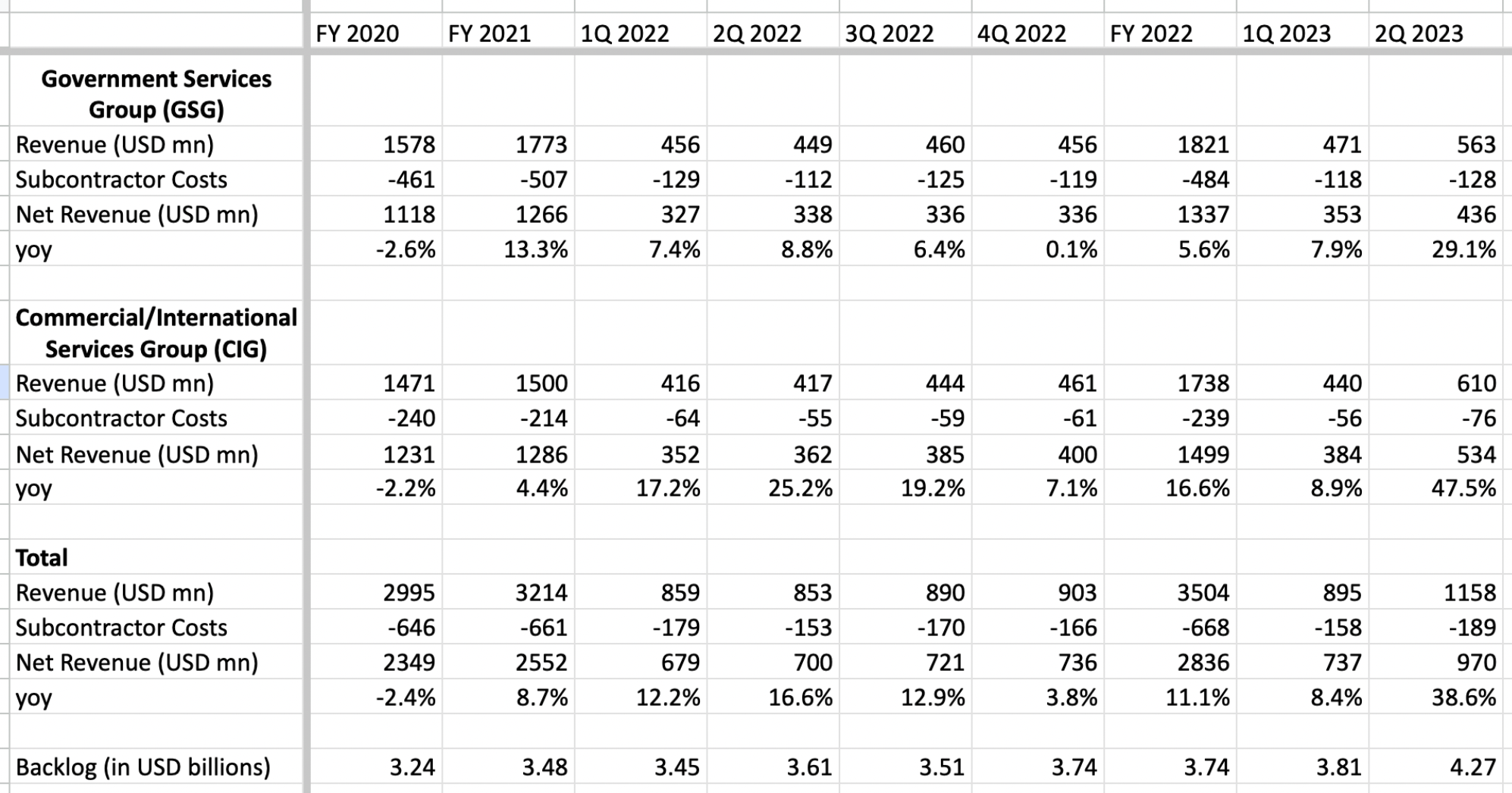

In Q2 FY23, the company's net revenue increased by 34% Y/Y to $970 million, driven by the recent RPS acquisition and continued strength in its end market. Even excluding the contribution from RPS, the underlying growth was solid, with net revenue (excluding acquisition) growing by 18% year-over-year (YoY).

The Government Service Group ((GSG)) segment experienced 29% YoY growth, benefiting from substantial contributions from USAID humanitarian projects related to Ukraine energy. These projects involved grid reliability maintenance, temporary power supplies, and power restoration during the Russia-Ukraine war, contributing $70 million to the revenue. However, disaster response projects for local and state governments declined in the quarter compared to last year, when there was unusually high demand. Excluding the unusual impact of Ukraine energy projects and disaster response projects, the GSG segment's revenue increased by 16% YoY.

The Commercial International Group ((CIG)) segment achieved 47% YoY growth, with a significant contribution from the RPS acquisition. Even excluding RPS, the segment's revenue grew by a healthy 13% YoY, driven by growth in renewable energy programs, environmental works in the U.S., and high-performance building projects worldwide.

TTEK segmentwise and total revenue (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, the company's growth prospects appear favorable due to healthy backlog levels, continued strength in the end market supported by a positive government funding outlook, and synergies from the RPS acquisition. The company ended the last quarter with a backlog of $4.27 billion, showing an increase both sequentially from $3.81 billion in Q1 2023 and YoY from $3.61 billion in 2Q 2022. This backlog provides good visibility into the company's future revenue growth.

Furthermore, the deployment of funding from various U.S. federal government infrastructure programs, such as the $1.2 trillion IIJA, the $280 billion CHIPS and Science Act, and the $369 billion IRA, has begun and is expected to gain momentum in the coming years, further accelerating the company's order growth. Additionally, the RPS acquisition should yield revenue synergies, doubling the company's staff in the U.K. and Australia and providing access to new markets like Norway, the Netherlands, and the Republic of Ireland, where the company can cross-sell its other service offerings.

Margin Analysis and Outlook

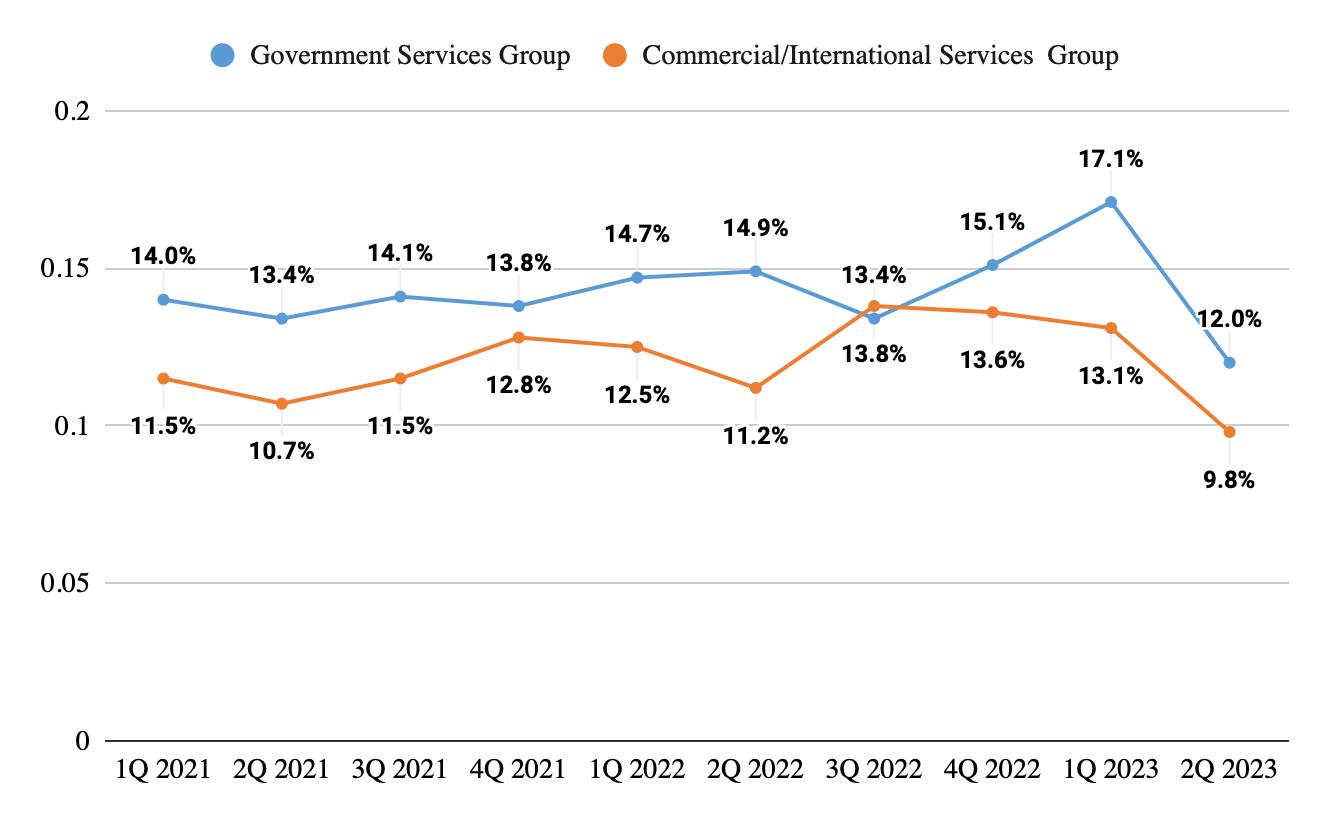

Last quarter, the company experienced a decline in adjusted operating margins for both segments compared to the same period last year, as well as sequentially. The GSG segment's adjusted operating margin declined by 290 basis points YoY to 12%, while the CIG segment saw a 140 basis-point decline.

{kind=link}

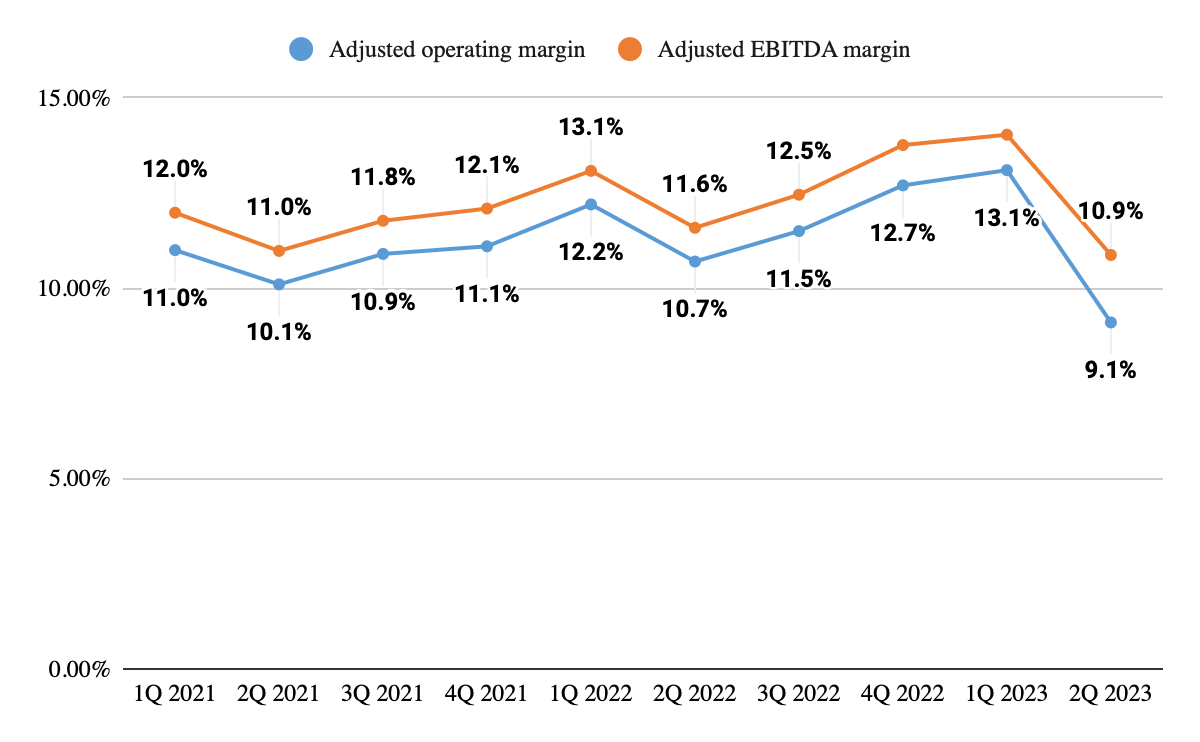

Overall, the company's adjusted operating margin declined by 160 basis points, and the adjusted EBITDA margin declined by 70 basis points. The decline in the margin can be attributed to the RPS group acquisition, which has a significantly lower EBITDA margin (~5% in FY22) compared to the rest of TTEK. Additionally, USAID humanitarian work typically carries a lower margin, and last quarter there was $70 million of such work related to Ukraine energy projects.

TTEK Adjusted operating and EBITDA margins (Company Data, GS Analytics Research)

{kind=link}

Both of these factors are temporary in nature. The company has a strong track record of acquiring companies and improving their margins to align them with TTEK's business. This has been demonstrated in the past with the company's previous two public company acquisitions, Coffey (in 2016) and WYG (in 2019). Management has provided guidance indicating a similar improvement for RPS, with a target of improving RPS' EBITDA margin to 13% or higher by 2025. Furthermore, the Ukraine Energy projects are mostly short-term in nature and are not expected to continue being a big part of the company's portfolio mix in the medium term. Therefore, I anticipate a meaningful expansion of margins in the coming years.

Valuation and Conclusion

One concern I have always had with TTEK is its high valuations. Over the past five years, it has traded at an average forward P/E ratio of 29.51x. Looking at consensus estimates, it is currently trading at 28.46x FY23 (ending Sep.) consensus EPS estimates of $5.14 and 25.44x FY24 (ending Sep.) consensus EPS estimates of $5.75. While the company's P/E multiple on FY23 estimates is only slightly lower than historical levels, its P/E for FY24 estimates appears attractive for investors with a medium-term horizon.

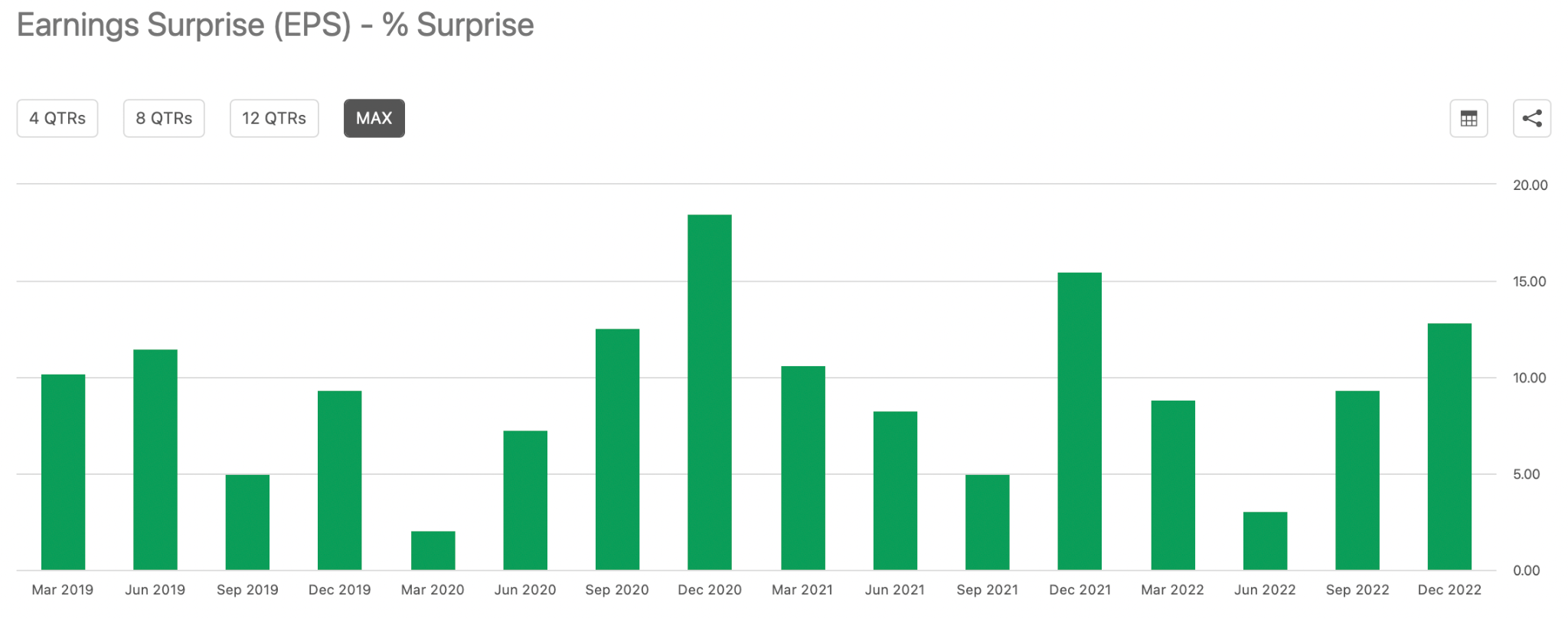

Moreover, the consensus estimates for FY24 seem conservative. Management has indicated a neutral impact from the RPS acquisition in FY23 and a 50-cent EPS tailwind from it for FY24. This implies that FY24 EPS should be 50 cents higher than FY23 based on synergies from the RPS acquisition alone. Therefore, it appears that sell-side consensus estimates ($5.14 for FY23 and $5.75 for FY24) assume that excluding RPS, the remaining business will only grow EPS by approximately 11 cents or around 2%. This seems unreasonably low considering the positive momentum in the company's end markets as government funding under IIJA, IRA, and CHIPS Act is being deployed. Thus, I believe there is potential for an upward revision in FY24 EPS estimates. The company has a history of positively surprising investors and has surpassed earnings expectations every quarter in the past four years, indicating that Wall Street analysts have often underestimated the company's potential.

{kind=link}

Considering the reasonable discount of the company's FY24 P/E multiple compared to historical levels and the potential for an upward revision in FY24 EPS estimates, I believe the stock is a buy at its current levels.

For further details see:

Tetra Tech Could See Good Upside Over The Next Year (Ratings Upgrade)