TTEK - Tetra Tech: Expanding With Sustainability But Stock Price Not Cheap

2023-05-24 22:00:52 ET

Summary

- Tetra Tech, Inc. maintains a solid FY 2023 with its steady revenue growth and margins.

- Its financial positioning remains decent, but Goodwill is still one of my concerns.

- Market tailwinds are evident, despite recession fears across the globe.

- Dividends have consistently increased, but yields are unappetizing.

- The stock price has bounced back but is quite higher than the reasonable value.

The call for sustainable water, infrastructure, and environment has reverberated over the years. Indeed, the pandemic, hurricanes, and earthquakes became an eye-opener for many. With that, the public and private sector has increased their efforts to cushion the blow of climate change. They are also working towards a safer and more eco-friendly economy. These aspects are some primary driving forces behind the robust performance of Tetra Tech, Inc. (TTEK). It remains a staple in the field of science and technology. Unsurprisingly, the company receives numerous project deals and capitalizes on acquisitions. However, M&As come with an increasing amount of Goodwill, which is quite bothersome. Its larger operating capacity remains sustainable with its stable cash levels, but Goodwill erodes its tangible book value.

Meanwhile, TTEK covers its capital returns. It still has a balance under its stock repurchase program. Dividends are also increasing, making it a secure dividend stock. They appear well-covered, given the stable and increasing cash reserves. The only thing that bothers me is the unenticing yield, way lower than the S&P 400 and NASDAQ average. Additionally, the stock price appears higher than the intrinsic value of the company. It may also convey overvaluation, limiting TTEK stock's upside potential.

Company Performance

It’s been over a year since I last covered Tetra Tech, Inc. And in between times, the company has shown an impeccable performance. It capitalized on expansion through continued M&As and contracts. Despite market volatility, it remained unperturbed and exceeded my expectations in my previous coverage. Today, it maintains a larger size as it increases its market presence.

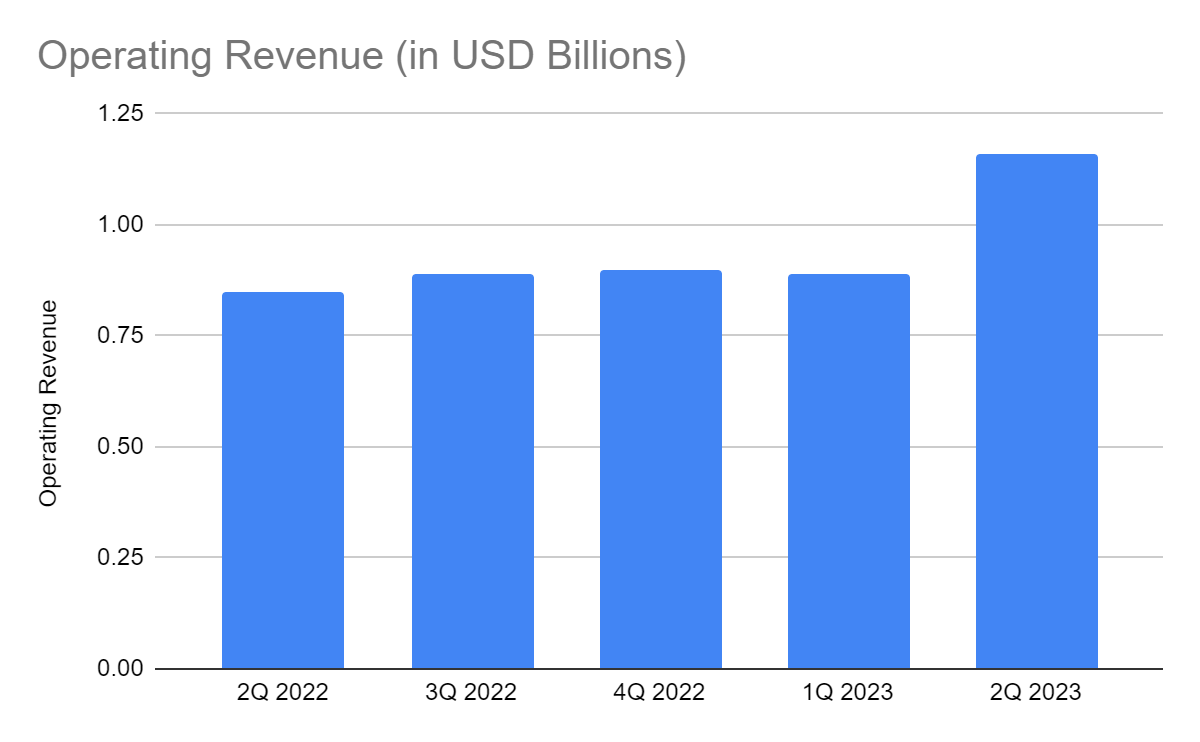

In its most recent quarter, TTEK demonstrated its dominance in the industry. Its operating revenue reached $1.16 billion , a 36% year-over-year increase. The combined value in the first half of FY 2023 was $2.05 billion , 20% higher than the same period in FY 2022. Given this, the company continues to provide innovative solutions through Leading with Science. TTEK remains the leading figure in the consulting and engineering services market. Various aspects contributed to the substantial increase in revenues. To make it more concise, I will focus on the internal aspect.

{kind=link}

Operating Revenue (MarketWatch)

First, the company has capitalized on growth through consistent but prudent M&As. During the first and second quarter of the fiscal year, it acquired TIGA, Amyx, and RPS Group. This move allowed the company to reach more potential clients and expand its services. It also increased its operating capacity, helping it win more contracts. Most importantly, it improved its operational efficiency. TIGA provides SaaS/PaaS applications, cloud data integration, platform visualization, and advanced data analytics. This feature is crucial in streamlining business processes. And given the nature of its business, TTEK must speed up its digital transformation. Second, it is true that reputation precedes you. TTEK is one of the perfect examples. During the quarter, the company won six environmental and climate change awards. Environment Business International (EBI) is a known award-giving body in the industry. Indeed, TTEK proved effective in responding to water and biodiversity management, climate adaptation, and clean energy transition. It is no wonder, many firms continue to trust its services. During the first half, TTEK got eight contracts, as shown in its press releases. With the demand and strategic pricing, the company generated higher revenues.

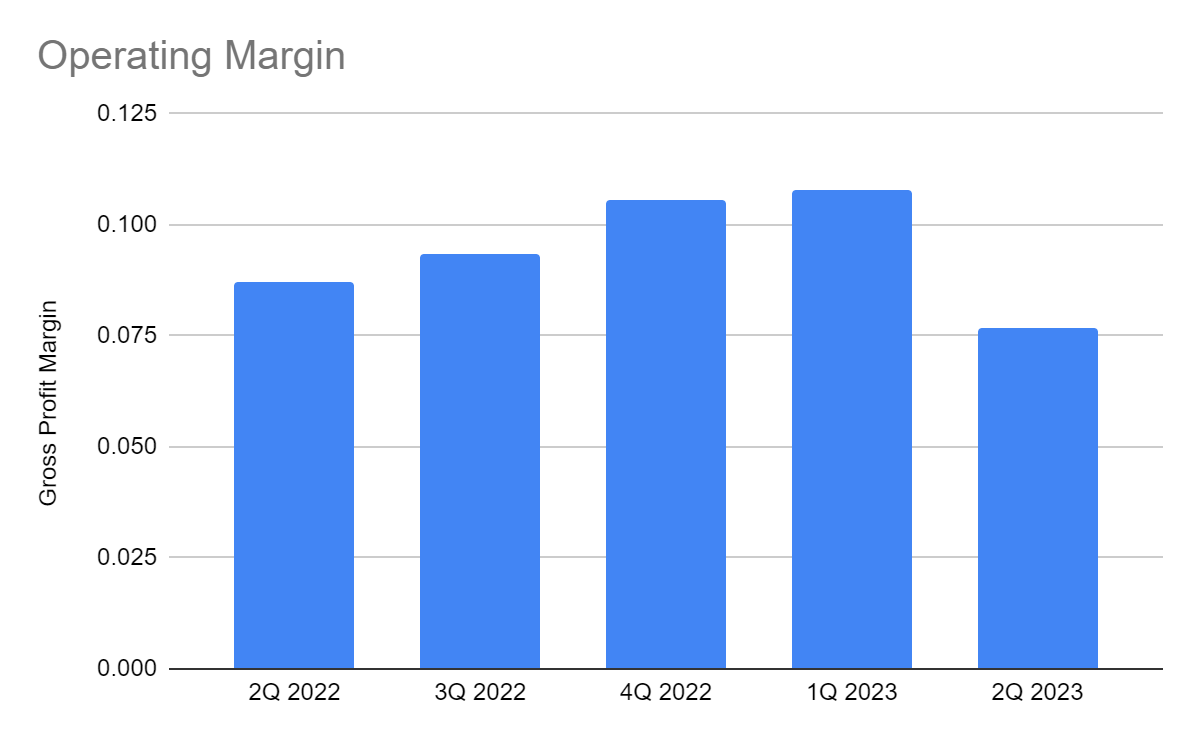

But what makes TTEK a secure business is its maintained efficiency. Amidst the high demand for its services, the company had to deal with inflationary headwinds. Higher prices mean higher subcontractor costs, labor expenses, and marketing expenses. The year-over-year increase was almost the same as in revenues. It was still higher at 37%, leading to margins of 8% versus 8.7%. Despite this, the fact that the company remained viable amidst its expansion and inflation was impressive. If we disregard its acquisition-related expenses, the operating margin will be 9.3%. It shows that the continued M&As of the company were still efficient.

{kind=link}

Operating Margin (MarketWatch)

This year, the company may face similar challenges as prices remain higher than pre-pandemic levels. But it may maintain its market positioning after ranking first in Water by Engineering News for twenty consecutive years. Even better, it won another contract last week, increasing its revenue stream for this quarter. The thing is, TTEK has been and may always be a market staple. We will discuss more of its core strengths, risks, and opportunities in the following section.

How Tetra Tech, Inc. May Remain Solid This Year

Tetra Tech, Inc. maintains solid and robust core operations this fiscal year. But as it begins the second half of FY 2023, it must beware of every risk that may hamper its growth. Interest rates have already increased further than expected. If it continues, it may discourage spending and investments. These are vital for the company as it capitalizes on project deals and M&As. Also, borrowings are equivalent to 37% of the total assets. As such, higher interest rates may decrease liquidity. It can also increase interest expense and lower viability. The consolation is that interest rates appear to be more manageable these days. In the two recent meetings, The Fed kept interest rate hikes flat at 25 bps versus 75 bps in the past four quarters.

On a lighter note, inflation has been more relaxed since 4Q 2022. At 4.9% , it is 46% lower than the highest rate in 2022. The consistent decrease shows that the conservative approach of The Fed remains effective. If the downtrend continues, interest rate hikes may remain flat at 25 bps or the actual rate may no longer increase. Lower inflation can even lead to better pricing flexibility. It can increase the purchasing power of customers and allow the company to set more strategic pricing. Even better, it can help TTEK manage costs and expenses better to stabilize margins.

United States Inflation Rate (Trading Economics )

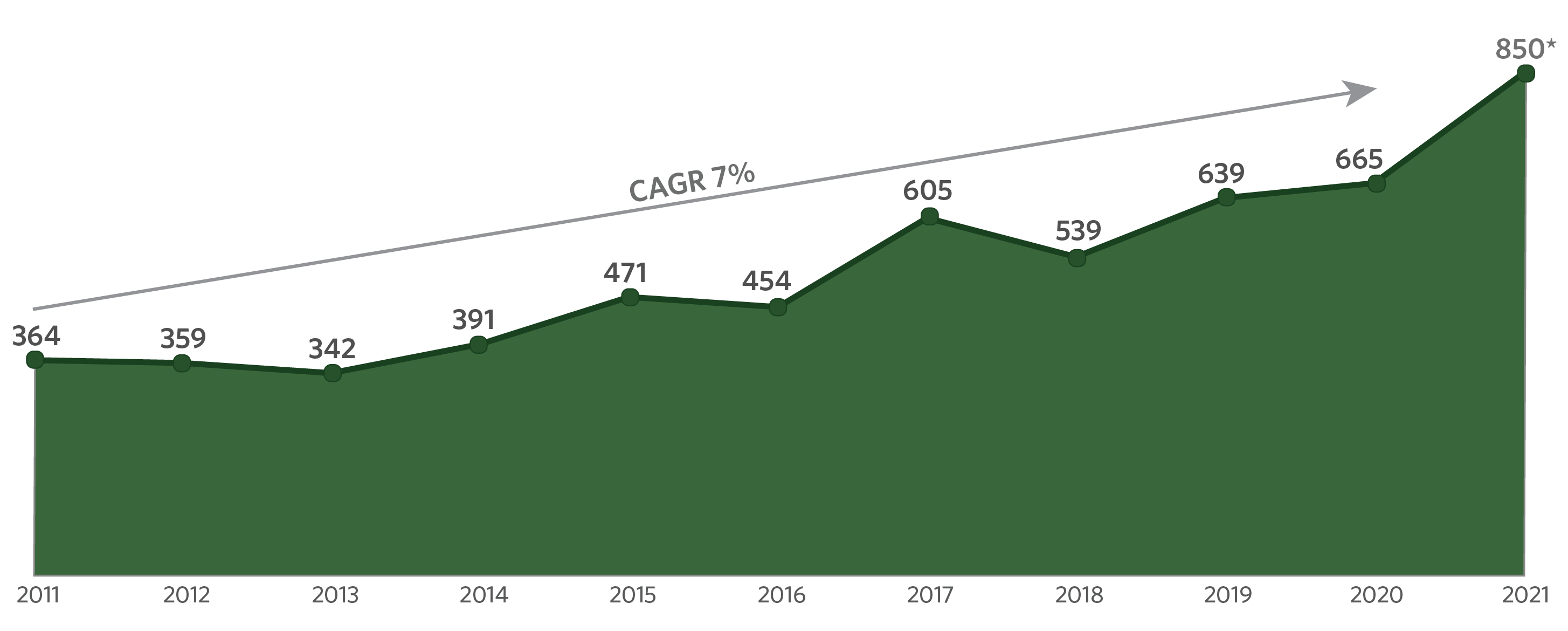

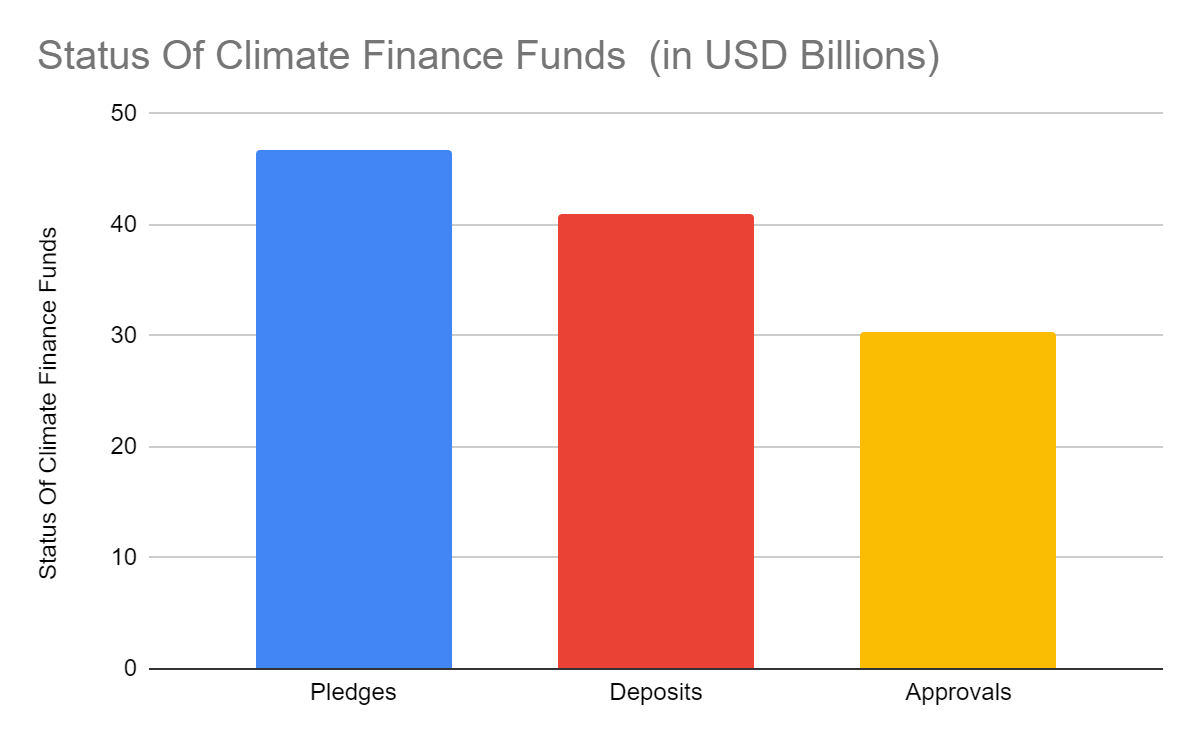

Another potential driving force is the increasing value of climate finance. Amidst the pandemic and natural disasters, the call for environmental sustainability reverberates. One of the primary concerns is climate resilience. As such, the government and private institutions are working together to fund climate finance. Over the past decade, the global climate finance fund more than doubled. It soared in 2021 to $850 billion , allotted for 2022. Today, climate finance remains crucial for society. An organization in the US sees an uptrend in its funds. In a recent report, it generated $118 billion , with 40% of the funds coming from donations and pledges.

{kind=link}

Global Climate Finance (Climate Policy Initiative)

{kind=link}

Status Of Climate Finance Funds USA And Canada (Climate Funds Update)

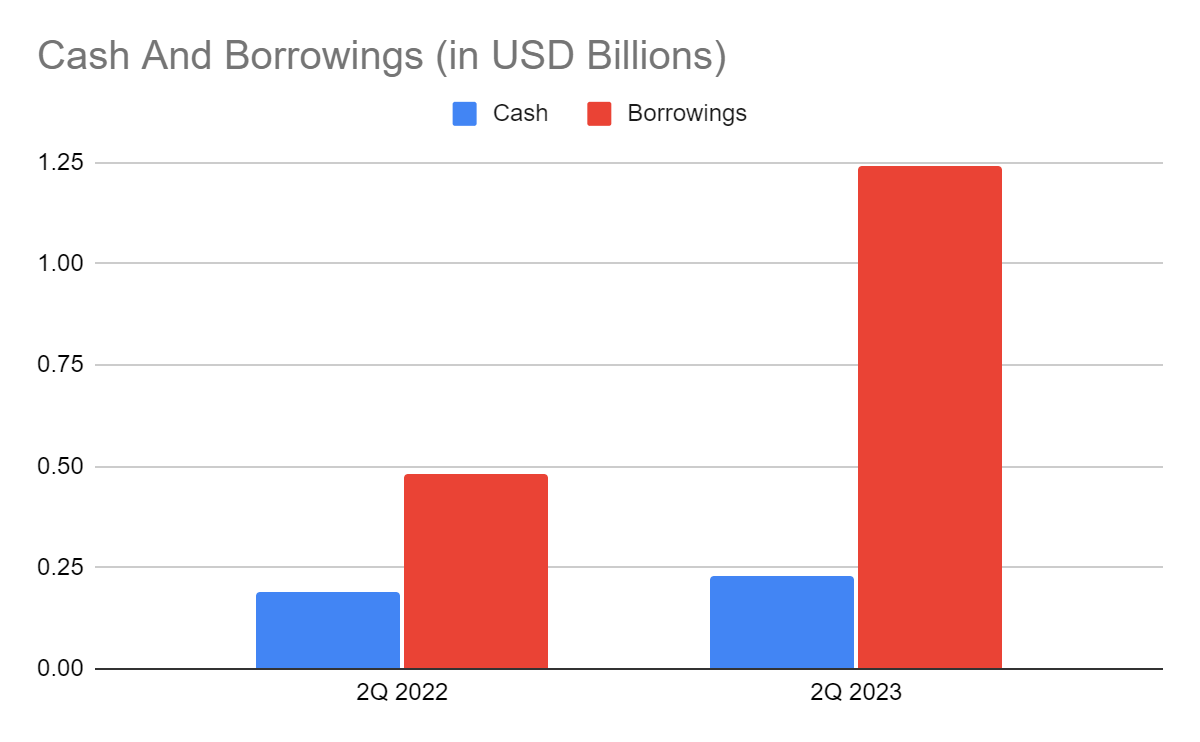

With regard to its financial capacity, TTEK remains a huge company. The only thing that bothers me is the increasing amount of Goodwill. At $1.9 billion , it comprises 47% of the total assets. It may suggest overspending or over-acquisition and erode the tangible book value. It may also affect the quality of its business model. Currently, its Asset Turnover Ratio is 29% versus 31% in 1Q 2022. It may be expanding faster than it generates returns.

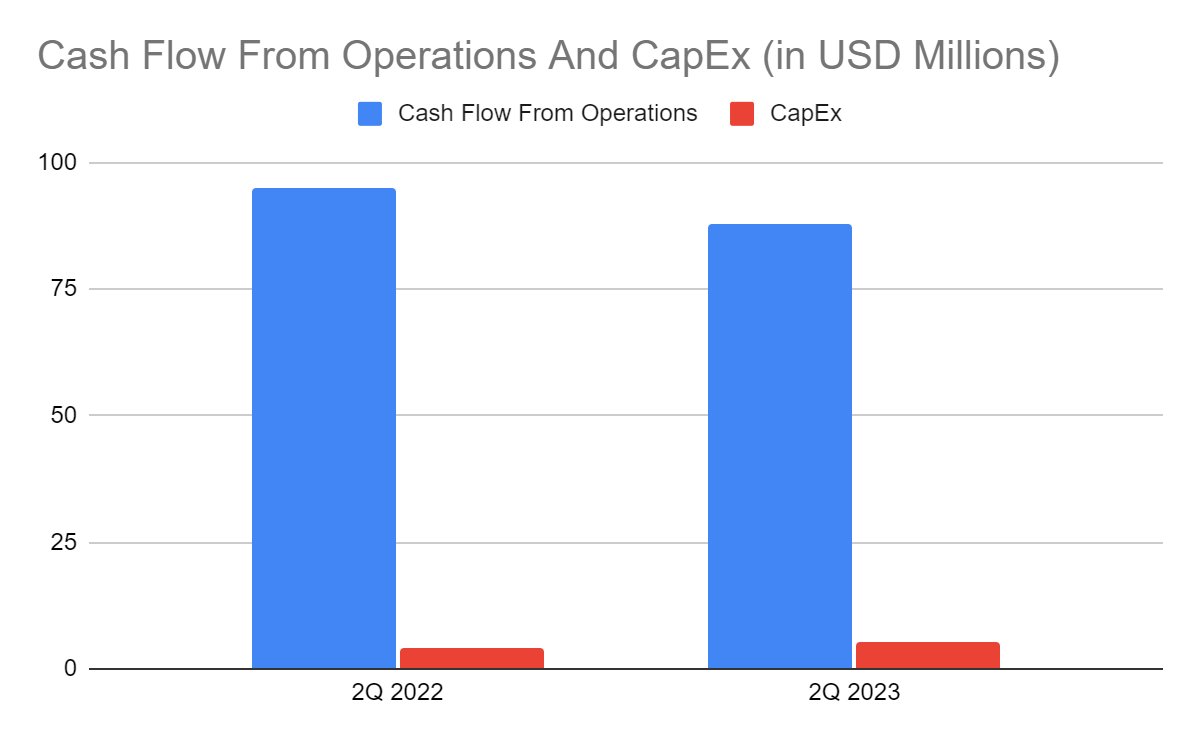

Thankfully, the company maintains adequate cash reserves to suffice its business needs. More importantly, cash increased by 21%, showing zero cash burns. Indeed, returns are enough to cover the expansion of the company. We can confirm it with the Net Debt/EBITDA Ratio of 2.65x, which is still lower than the maximum ratio of 3.5-4x. TTEK does not have to burn cash to sustain its business. Also, only 7% of its borrowings have current maturities. Likewise, the Cash Flow Statement shows the high capacity to cover the operations. The Cash Flow From Operations is enough to cover CapEx. It has an FCF of $83 million, which can cover current borrowings even in a single payment. The FCF/Sales Ratio of 7% also shows that TTEK continues to convert revenues into cash. The company maintains the balance between viability and liquidity.

{kind=link}

Cash And Equivalents And Borrowings (MarketWatch)

{kind=link}

Cash Flow From Operations And CapEx (MarketWatch)

Stock Price Assessment

The stock price of Tetra Tech, Inc. has decreased during the 2021 correction. But it rebounded in the latter part of 2022. At $142.14, the stock price is 14% higher than last year’s value. It is still higher than the intrinsic value of the company, which should be a concern. We can see it using the PB Ratio, given the current BVPS and PB Ratio of 25.47 and 5.65x. If we use the current BVPS and the average PB Ratio of 5.43x, the target price will be $138.33. Its uptrend is reasonable, given the continued expansion of the company. Yet, the actual amount of increase appears quite excessive. Meanwhile, the EV/EBITDA gives a target price of ($7.62 B EV - $1.08 B Net Debt) / 53,228,000 shares = $143.15. But while it shows that the stock is fairly valued, the upside remains limited.

Meanwhile, TTEK is a secure dividend stock with its increasing payouts and high cash levels. However, yields are only 0.73%, way lower than the S&P 400 and NASDAQ average of 1.7% and 1.57%. They remain well-covered, though, given the Dividend Payout Ratio of 32.5%. To assess the stock price better, we will use the DCF Model.

FCFF $326,200,000

Cash $231,300,000

Borrowings $1,308,570,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 53,228,000

Stock Price $142.14

Derived Value $132.67

The derived value adheres to the supposition of a potential overvaluation. There may be a 7% downside in the next twelve months. Given this, I believe that the stock price rebound in the past year was reasonable. The company flourished and increased its operating capacity. But the actual amount of increase may be too high to reflect the intrinsic value of the company.

Bottomline

Tetra Tech, Inc. remains a solid company with steady revenue growth and stable margins. Its capitalization on expansion is sustainable, given its adequate cash levels and core earnings. It also allows the company to cover borrowings with shorter maturities and dividends. However, the stock price appears overvalued relative to the intrinsic value of the company. I am optimistic about its core operations this fiscal year. I also believe it is a secure company despite the high levels of Goodwill. But the stock price may not be an ideal entry point due to limited upside potential. The recommendation is that Tetra Tech, Inc. is a hold.

For further details see:

Tetra Tech: Expanding With Sustainability, But Stock Price Not Cheap