CA - Thanksgiving Income Feast: Can Brookfield Infrastructure Partners Bless Your Portfolio?

2023-11-22 15:19:53 ET

Summary

- A roughly 6% yield draws our attention to Brookfield Infrastructure Partners as we look to stuff our holdings with some income and capital appreciation opportunities.

- Infrastructure is reliable for cash flow, and 70% of sources of flows have no economic or market exposure.

- The distribution payout ratio is targeted between 60% and 70%, though efforts to raise cash lead to questions of where funding is allocated.

- A recent short report raised concerns, though just reported performance and expectations seem to dispel much of the alarm.

- We continue to see growth in all Brookfield Infrastructure segments except for one.

Tomorrow, millions of American families and friends will gather for a Thanksgiving Feast. But ahead of giving thanks, just today we were asked about Brookfield Infrastructure Partners L.P. ( BIP ) and whether there was an opportunity to trade this partnership - and corporation, as it also trades as Brookfield Infrastructure Corporation (BIPC) - in our investing group chat room. The short answer to this question is, maybe, but we would like the price a bit lower for those purposes.

However, from an investing standpoint, despite some of the drama surrounding the name, including a short report (links to pdf of report) that questioned operations, we see this as a name for income investors. We see this name as one that can be scaled into for income, to collect a 6% yield from the partnership version while operations in the infrastructure space are set to enjoy strong gains in the future in our opinion.

Make no mistake, Brookfield is constantly making moves to grow and expand the business. Just last week, one such piece of news was that Cyxtera Technologies ( OTC:CYXTQ ) was informed that the U.S. Bankruptcy Court for the District of New Jersey approved the selling of its assets to Brookfield. So, that is a win. Expect ongoing moves, as Brookfield has a long history of picking up assets to fuel growth.

So, before going more into company specifics, there are a few reasons why we fancy investing in the infrastructure space, generally speaking. First, infrastructure is ALWAYS needed. Roads crumble, bridges need repair, wirelines need replacement, buildings need to be demoed and/or rebuilt, planning for expansion is constant, and all of this and more tends to mean companies operating in the space through either consulting, or construction/execution of planning can enjoy long-term contracts that provide pretty stable revenue and cash flows. And, regardless of what kind of economy we are in, tax dollars will always be funneled to the infrastructure as it is essential to keep the economy running.

As an aside, anecdotally, there seems to be more and more voter desire for true investment in our infrastructure. There is data that supports this notion. That remains to be seen, but is noteworthy. And there are not a lot of new up and comers breaking into the market, because infrastructure projects are massive undertakings that need significant capital, companies need to have demonstrated success, and have the right connections, which keeps the total addressable market, or TAM, contained largely to established names.

Now, one of the reasons we like this name for income, despite valuation metrics that at present seem stretched, is that Brookfield is among one of the few global infrastructure vehicles that invests in premier infrastructure assets with stable cash flows, high margins and strong growth prospects. Now, to be clear, EBITDA and operational cash flow are expected to dip this year, so that has weighed, though funds from operations, or FFO, through perhaps some aggressive accounting has grown.

Further, we like the management team here, as their record is historically sound, and they are committed to returning the company's earnings to partners (aka unitholders). In fact, the 6% yield is highly attractive, but even more so when management has a goal of distribution growth between 5-9% annually. After the recent selloff in many income names, Brookfield looks ripe for the picking, in our estimation.

Looking to the ten-year chart, we see a strong base of support around $20. Now granted, in the past ten years, we had not seen massive rate increases like we saw starting in 2022. In fact, the stock pretty much peaked in 2022 when the rate hiking cycle ramped up. With rates now done being raised, we think income names will start to see some love again as it looks like we have likely seen peak income returns from bonds and money markets.

Make no mistake, you can still get easy safe income from those fixed assets, but little opportunity for capital appreciation. That is what differentiates an income-producing stock from such fixed income. The flip side is that it comes with equity risk of course. But, we have recently started to come back to income names, getting much better prices than most. We see Brookfield as a buy. Should we get another yield spike, we could get some better prices. But here is how we would enter the name.

The play

We like this for investment, though traders could target a $30 exit. We prefer you buy for a longer-term hold for appreciation in units and growing income.

target entry 1: $26.50-$26.75 (25% of position)

target entry 2: $25.00-$25.25 (35% of position)

target entry 3: $23.25-$23.50 (40% of position)

We would then hold shares and monitor quarterly performance.

Discussion

The company has global exposure, but there is still room for expansion. With that said the global nature of the company diversifies the geographic income stream, so if one country or region is struggling, it is likely others are humming along. A global recession, of course, could negate that, but as we said, infrastructure is relatively recession-resistant, as the services are essential.

{kind=link}

Half of the operations are in North America. The remaining half is nearly equally split between South America, Europe, and Asia Pacific.

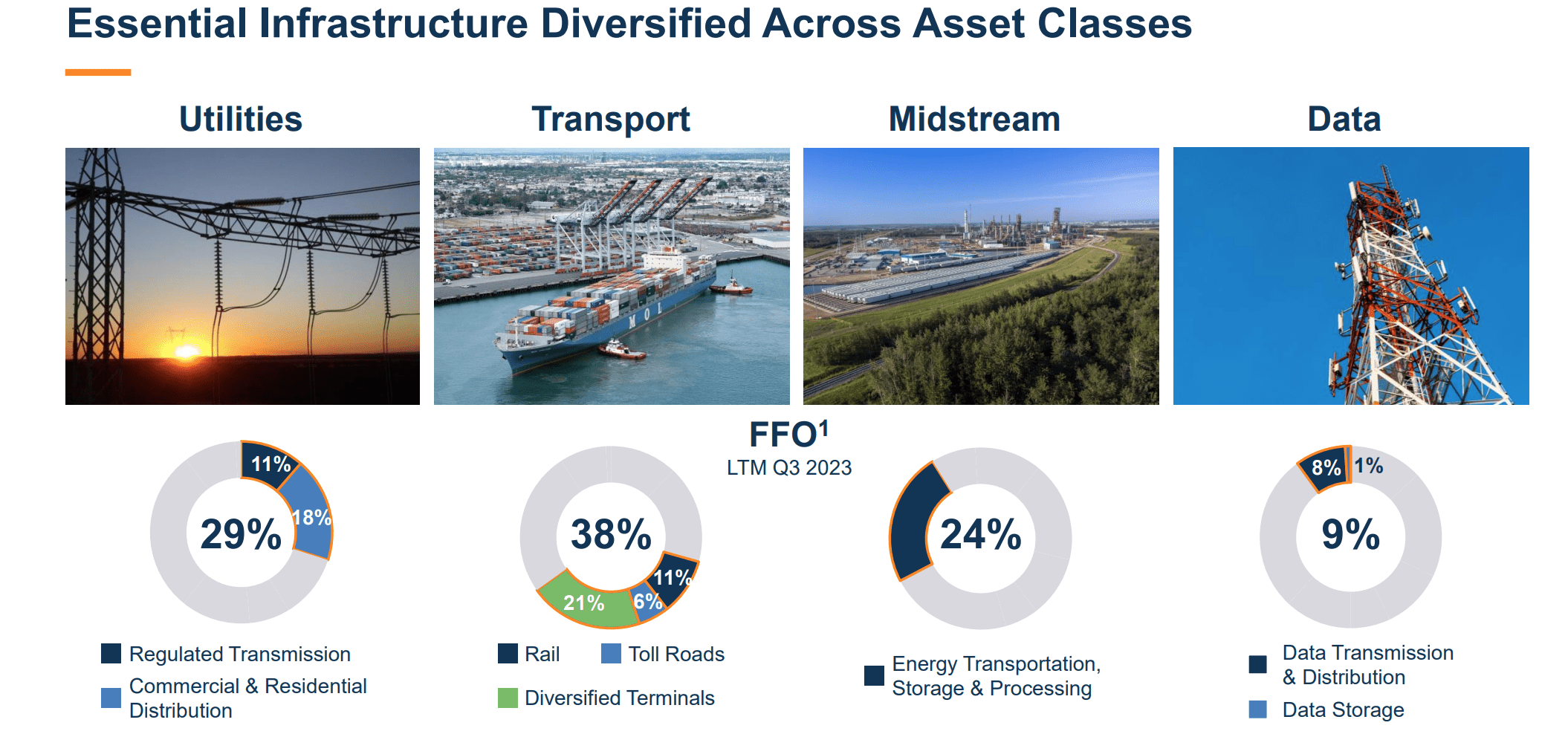

Looking at the breakdown of FFO brought in, we see 38% is derived from Transport operations, 29% from Utilities, 24% from Midstream operations, and 9% from data services.

{kind=link}

The Utilities segment is comprised of businesses that provide regulated transmission and distribution of electricity and natural gas. For Brookfield, this segment is pretty geographically diverse, spanning nine countries across all 4 of the geographic regions aforementioned. The Transport segment is involved in the movement of freight, commodities, and passengers. This segment is also geographically diverse with large rail operations, toll roads, and a portfolio of diversified terminals. The Midstream operations are what you can expect, transporting oil and gas, and are focused in North America. Finally, Data operations provide essential services and critical infrastructure to transmit and store data globally.

If there is one chart that shows why we think you can invest here long-term on this substantial share price decline, it would be the annual growth in FFO:

{kind=link}

This is simply strong, and as you can see as the FFO has grown, so have the distributions. Income here is clear, and the annual raises to your income are also impressive. Moreover, as we mentioned above, infrastructure work often comes with consistent and reliable cash flow.

{kind=link}

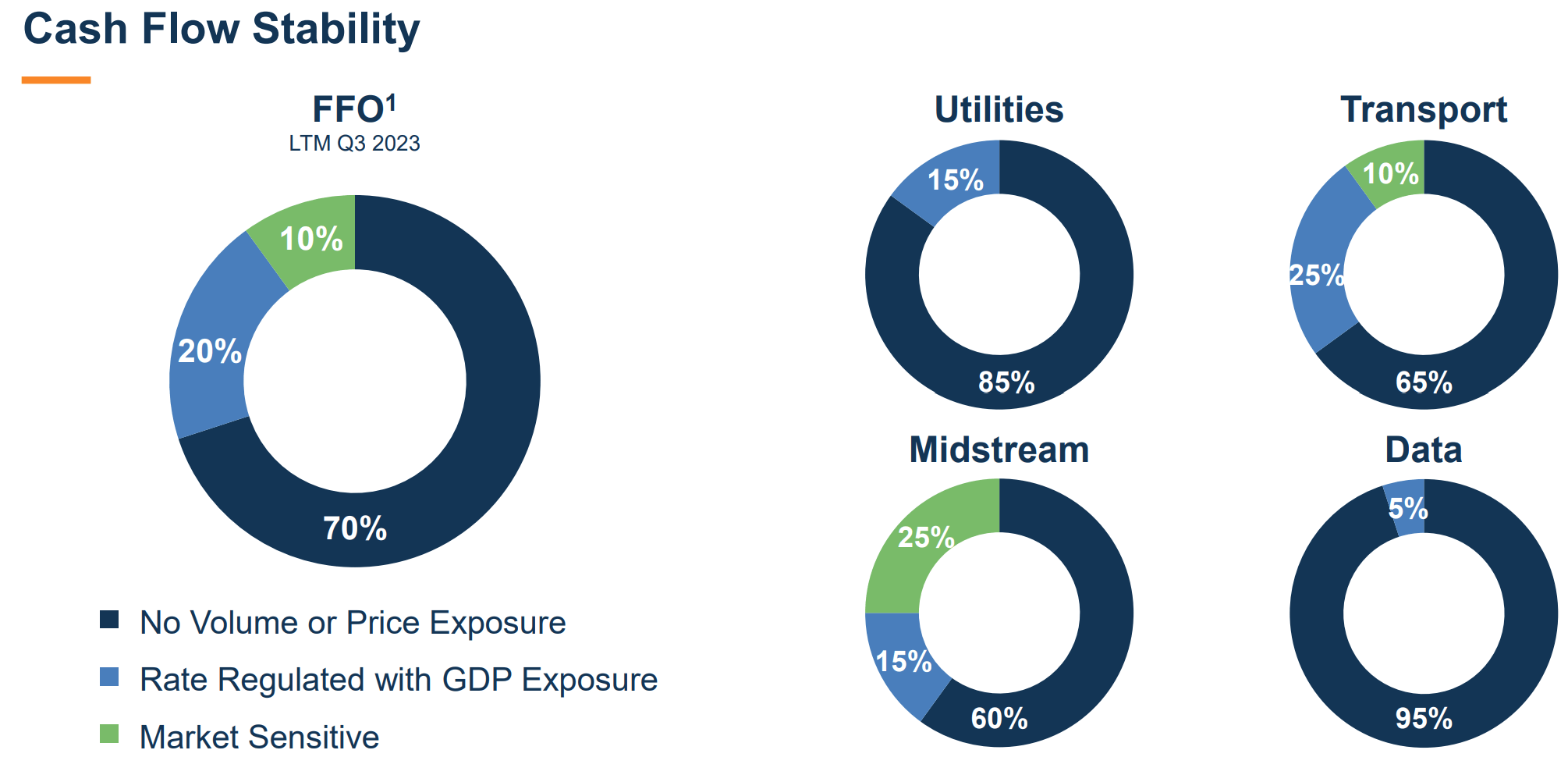

In looking to the operations, 70% of cash flows are not reliant on how a country is doing economically or exposed to the price of a commodity. Obviously in Midstream operations we do see 25% of the cash flow sensitive to the market (e.g., oil and gas), so there is some correlation there with energy pricing. Keep that in mind, but is a small fraction of overall cash flow.

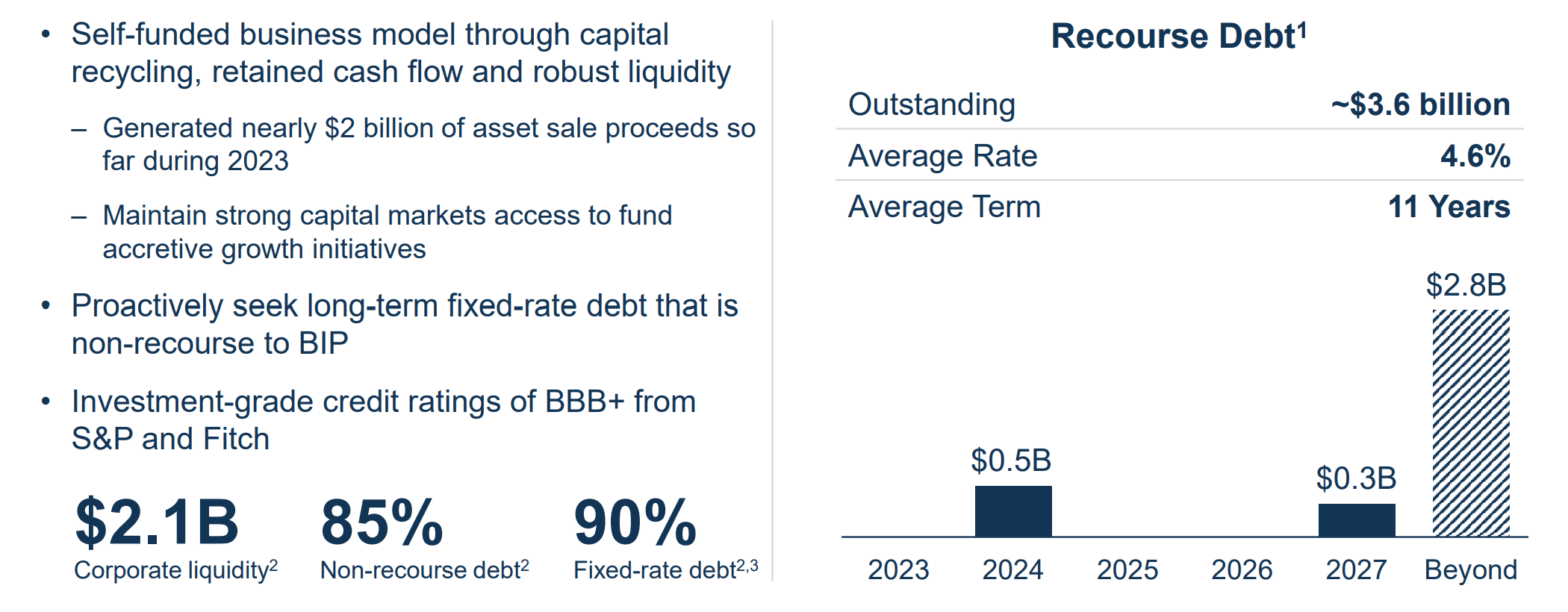

With rates having spiked one of the first things to consider is debt, and how much debt will cost. The balance sheet here is quite manageable in our estimation.

{kind=link}

Now, there is some concern that when cash flow does not cover distributions, more recourse debt is issued, as are shares. At the same time, despite growing through acquisitions over the years, the company has also dumped low-yield assets, selling $2 billion worth of proceeds.

To some degree, the capital recycling that the company engages in as noted on the slide above comes with some opacity. When viewing the financial statements , there seems to be some degree of complex accounting, and following how distributions are fully covered is difficult. In our opinion, we think that in harder times when cash flow may not cover all distributions, that some of this activity of recourse debt additions is likely. However, the most recent performance in our opinion dispels much of the aforementioned short report concerns. We see FFO and cash flow as continuing to grow. In the just reported Q3 , we saw strong performance.

{kind=link}

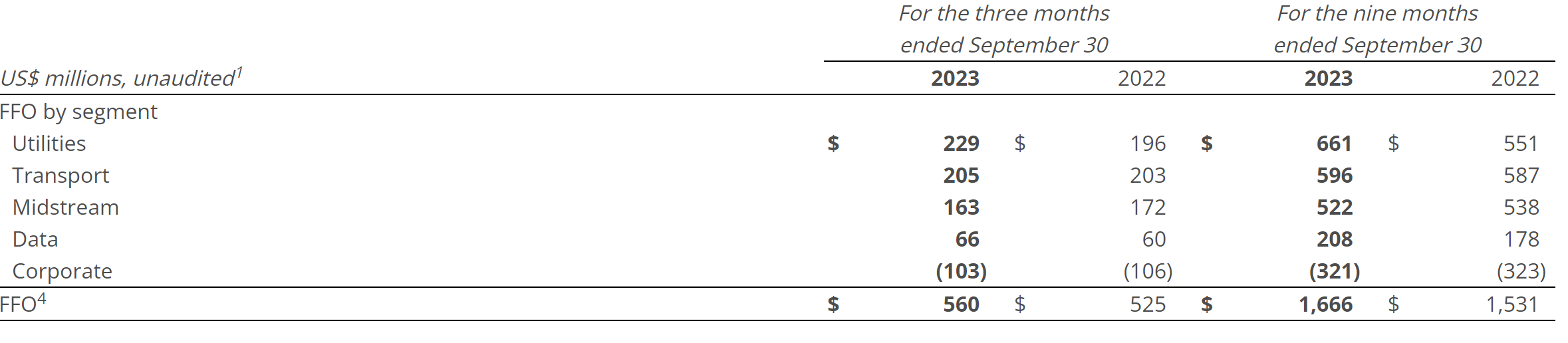

We see strong performance here, though net income dipped in the quarter to $104 million compared to $113 million in the prior year Q3, or $0.03 versus $0.05 per share. However, year-to-date we saw that recently completed acquisitions and organic growth across outpaced the higher borrowing costs associated with the debt. Net income on the year is up to $505 million from $359 million for the first 9 months of the year. More importantly, FFO in the quarter was $560 million, a 7% increase from last year's Q3. It is important to note that those results are yet to see the benefit of new investments this year, but we will see them in Q4. Year to date, FFO is $2.16 versus $1.99 a year ago.

From a segment-specific standpoint, all are displaying growth - with the exception of midstream.

{kind=link}

There is growth in all segments year to date. FFO from the midstream segment was $163 million, a 5% decrease compared to a year ago, but this was largely due to the partial sale a U.S. gas pipeline in June and some declines in commodity pricing. As mentioned above, 25% of Midstream is market sensitive.

So, is the distribution safe? While the company may do some sort of capital raise which may funnel to some degree to the distribution in one capacity or another, cash flow sufficiently does cover the distribution. In fact, the distribution payout ratio is targeted between 60% and 70%, and generally has enjoyed a below 70% payout ratio during this time. In reality the capital recycling of the company, and asset sale proceeds are used to fund internal growth, which we suppose is tangentially related to increasing the distribution.

With that said, the Brookfield Infrastructure distribution appears secure. If you are seeking income, and future capital appreciation, look no further than Brookfield. We view the risk-reward favorable long-term.

For further details see:

Thanksgiving Income Feast: Can Brookfield Infrastructure Partners Bless Your Portfolio?