AMZN - The $3 Million Dividend Growth Portfolio That Could Secure Your Retirement

Summary

- We start by diving into a just-released survey showing high retirement expectations. Unfortunately, data shows that the average investor is far from prepared.

- Hence, I present a dividend growth portfolio that comes with decent yields, consistent dividend growth, rock-solid business models, and healthy balance sheets.

- While multiple paths lead to Rome, I show that investors do not need an ultra-high-paying job or a huge inheritance to prepare for retirement.

- The goal was also to dive into what makes dividend growth investing so powerful and why it continues to beat the market so consistently.

Introduction

It's time to talk about investment goals. Recently, an article published by Bloomberg gained significant traction due to survey-based research indicating that investors are aiming to accumulate at least $3 million for a comfortable retirement. This article caught my attention as it provides an excellent jumping-off point for discussing investment strategies. In this article, I aim to provide you with a model portfolio of stocks that can help you achieve your retirement goals without taking excessive risks. We'll also talk about similar strategies that are focused on dividend growth with the incorporation of decent dividend yields and conservative stocks that will allow investors to retire without needing huge financial tailwinds, multi-million dollar inheritances, or other miracles.

So, without further ado, there's a lot to discuss!

We All Need To Become Rich

This is a tricky topic for countless reasons. Here are a few:

- Seeking Alpha has an international reader base, which means various pension systems and requirements.

- Every individual situation is different, as retirement planning includes (somehow) forecasting what the next 10-50 years might look like - depending on your age. This includes the employment situation, personal circumstances (i.e., family planning), and things nobody can predict, like unfortunate circumstances like illnesses, inheritances, injuries, political headwinds, and other things.

- People have different investment strategies. Some prefer stocks, others only buy ETFs, while others invest in art, precious metals, real estate, or their own business.

So, while this is a dividend (growth) focused article, I will try to find some common ground to add value regardless of your situation.

With that said, the other day, I was hit by the headline below:

{kind=link}

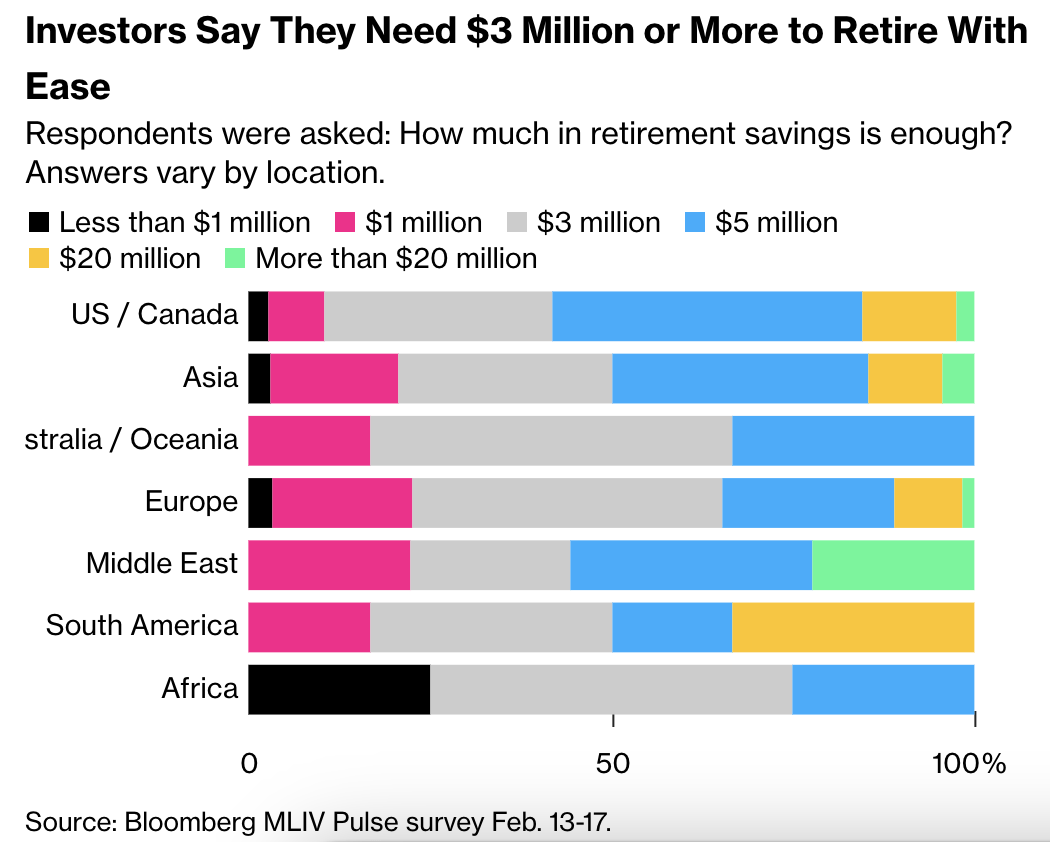

A Bloomberg MLIV Pulse survey asked 553 investors to share their views on retirement issues, including how much money they expect to need to retire.

Roughly a third of investors answered they need at least $3 million. However, an almost equal number of respondents required at least $5 million. That's a huge jump.

In the US and Canada, a big majority of respondents seem to agree that $1 million simply isn't enough.

{kind=link}

Even in Europe (my home base), roughly 75% of respondents believe that at least $3 million is needed to retire.

Before we continue discussing this survey, let's do a quick reality check. Using 2019-2020 Federal Reserve SCF (survey of consumer finances) data , we find that Americans aren't even close to these numbers. People in their mid-50s have saved close to a quarter of a million.

| Age range |

| Average Retirement Savings |

| Ages 18-24 |

| $4,745.25 |

| Ages 25-29 |

| $9,408.51 |

| Ages 30-34 |

| $21,731.92 |

| Ages 35-39 |

| $48,710.27 |

| Ages 40-44 |

| $101,899.22 |

| Ages 45-49 |

| $148,950.14 |

| Ages 50-54 |

| $146,068.38 |

| Ages 55-59 |

| $223,493.56 |

| Ages 60-64 |

| $221,451.67 |

| Ages 65-69 |

| $206,819.35 |

The numbers above are averages. In other words, while it includes people with zero savings (or debt), it also includes very wealthy people.

Hence, below, you're looking at the median, which shows that the median American isn't anywhere close to the targets set by the survey respondents. The numbers in other nations aren't looking much better.

| Age range |

| Median Retirement Savings |

| Americans younger than 35 |

| $13,000 |

| Americans aged 35-44 |

| $60,000 |

| Americans aged 45-54 |

| $100,000 |

| Americans aged 55-64 |

| $134,000 |

| Americans aged 65-74 |

| $164,000 |

| Americans aged 75+ |

| $83,000 |

Hence, it's no surprise that more than half of the aforementioned survey respondents expect to fail their targets.

Respondents were not as sure about whether they'd ultimately have enough saved to maintain their lifestyle in retirement. Less than half of investors placed the odds of that at 100%.

Moreover, the article also mentioned the concerns I addressed by showing average and median retirement savings.

Of course, building a seven-figure nest egg is an impossibility for many would-be retirees. Only about two-thirds of US private-sector workers had access to a workplace retirement savings plan in 2021, according to the Bureau of Labor Statistics. The average participant account balance across the 5 million or so plans where Vanguard is a recordkeeper was $112,572 at the end of 2022, and the median balance was just $27,376.

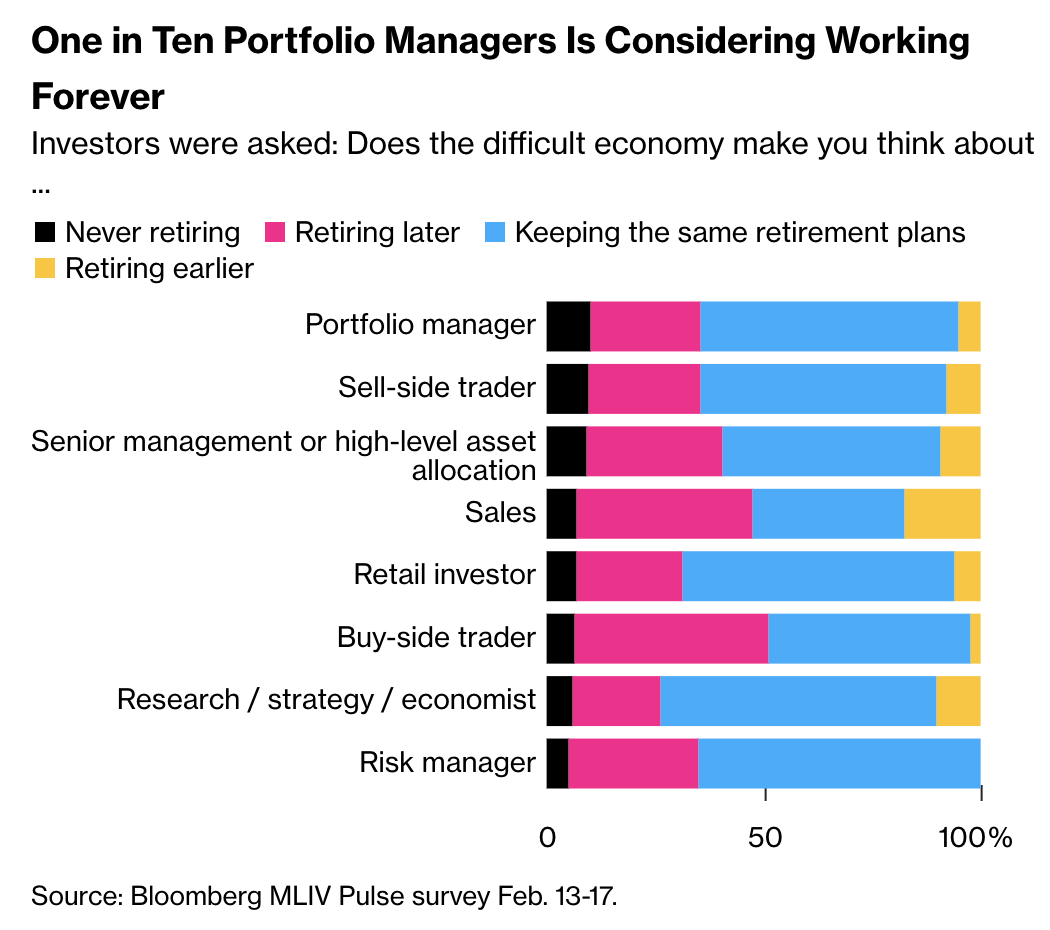

Hence, when we dig a bit deeper, we find that a lot of investors who participated in the survey are considering retiring later than expected - or to avoid retiring entirely.

{kind=link}

I have to say that I am in the group that isn't planning on ever retiring. However, that's very personal. In this survey, only investors were asked. All of the jobs above can be done by the elderly.

People in construction or other jobs that require manual labor are in no position to willy-nilly postpone their retirement if their funds aren't sufficient.

Measures To Prepare

Investing is a fascinating arena as it involves countless variables. As mentioned briefly in this article, each circumstance is distinct. Life is unequal and unfair, and individuals experience various scenarios. While some inherit substantial amounts of money, ensuring their retirement, others live from paycheck to paycheck with no additional support. Unfortunately, some individuals pass away before they reach retirement age. These are just a few examples of the numerous circumstances individuals face in life.

My view on these things is to have fun in whatever you do. However, measures need to be taken in order to be prepared for what may lie ahead. I benefit from the fact that I'm very easily satisfied in life. I have very low discretionary spending and enjoy putting almost all of my money into long-term investments. My friends and I sometimes joke that if we were to be run over by a bus tomorrow, we would at least have enjoyed accumulating whatever is in our accounts.

If you're working a job you really don't like, finding it hard to save money, and putting any extra cash you do have into investments you don't really care about, it's no surprise that you might end up feeling pretty down. In fact, it's one of the easiest ways to start feeling depressed.

With that said, it's important to start early when it comes to investing for additional cash in addition to social security and other benefits you may receive in the future. Even if you start small, time in the market is your biggest friend.

JPMorgan ( JPM ), for example, calculated that investors who saved $200 per month at age 25 ended up with $158,300 at age 65 based on cash earning 2.3% per year. That's awful.

However, investors who invested in stocks returning 7.0% ended up with more than $500,000.

Even investors who started at age 35 with the same yield added $270K to their retirement fund. Needless to say, the higher your monthly investments, the more money you will end up with.

JPMorgan

You might be surprised to find that even if you're not able to invest a lot of money each month, you can still build up a nice little nest egg over time. While $270,000 might not seem like a lot if you live in an expensive place like the San Francisco Bay Area, it can still be a good amount to have saved up for your later years. For people living in less wealthy areas, that amount of money can be truly life-changing. With $270,000, you could even retire comfortably in a place like Indonesia without additional support.

With that said, we'll discuss the retirement topic in more articles in the months ahead, as it's a complex topic that requires more attention.

For now, and based on everything said so far, I want to highlight two things.

- Time in the market is key. Start early and invest as much as possible. Even if you start small, it will end up making a difference. Bear in mind, the human brain has tremendous difficulties understanding the concept of compounding interest.

- When investing, investors need to be conservative. There's no room for error. Dumb (or less educated) mistakes can cost you valuable time in the market.

Hence, the portfolio I'm about to show you is entirely constructed around the second point I highlighted above.

If you decide to invest in single stocks instead of ETFs, you need to make sure you know what you're doing and invest in stocks that will provide you with outperforming returns (to make up for single-stock risk) and safety (again, no room for error).

So, I came up with a portfolio that might get the retirement job done.

The $3 Million Retirement Portfolio

If there's one thing I take away from my article's comment sections I read daily, it's that my readers seem to know what they are doing. While strategies differ, I get the feeling that people have clear goals, a good understanding of the assets they own, and a plan for unexpected situations like major sell-offs.

However, when I talk to retail investors outside of Seeking Alpha, I usually get people to invest in ETFs, as they provide diversification and safety.

Hence, in the stock selection of this article, I emphasized safety without sacrificing the ability to outperform the market.

So, for starters, I used the Yahoo Finance stock screener . I usually use other screeners. However, this one is free, which means you can copy my research. For the sake of this article, I think that's some added value. Also, it's fun to play with these screeners.

These are the filters I used:

- Region : only US-based companies.

- Size : only small, mid, large, and mega-cap companies.

- Sector : all sectors

- Consecutive years of dividend growth : >15

- Forward dividend yield : >2%

- Net debt/EBITDA : <3x

- Net income : >$0 (positive)

- 1Yr % change in EBITDA : >0% (positive)

In other words, we get a number of United States-based companies that have consistent dividend growth (even during the Great Financial Crisis), a decent yield at minimum, and a healthy balance sheet (all but one are A-rated!), positive net income, and positive 1-year growth EBITDA growth, meaning we even filtered out the ones that struggled in 2022 (some stocks I like a lot left the stock selection at that stage).

The result was 29 stocks. I erased 14 of them to get the 15 that are listed below. I did that because of two reasons. The first reason is that I didn't like a lot of them. In other words, while I stuck to the rules of the screener, I applied some bias in the final selection. Reason number two is that 29 stocks are too many stocks to discuss in a single article. In general, it is hard to give each stock the attention it deserves in articles like these. Hence, I will be using links to good articles when discussing these companies.

So, this is the list I ended up with:

| Name |

| Industry |

| Yield |

| 5Y Div. CAGR |

| Payout Ratio |

| Credit Rating |

| Chevron ( CVX ) |

| Oil & Gas |

| 3.7% |

| 5.8% |

| 30% |

| AA |

| Exxon Mobil ( XOM ) |

| Oil & Gas |

| 3.3% |

| 3.1% |

| 25% |

| AA- |

| Coca-Cola ( KO ) |

| Beverages |

| 3.1% |

| 3.5% |

| 71% |

| A+ |

| Johnson & Johnson ( JNJ ) |

| Pharmaceuticals |

| 2.9% |

| 6.1%% |

| 44% |

| AAA |

| Texas Instruments ( TXN ) |

| Semiconductors |

| 2.9% |

| 16.4% |

| 48% |

| A+ |

| Union Pacific ( UNP ) |

| Freight & Logistics |

| 2.7% |

| 15.4% |

| 45% |

| A- |

| Cummins ( CMI ) |

| Automobiles & Auto Parts |

| 2.6% |

| 7.6% |

| 36% |

| A+ |

| PepsiCo ( PEP ) |

| Beverages |

| 2.6% |

| 7.4% |

| 67% |

| A+ |

| Emerson Electric ( EMR ) |

| Machinery & Components |

| 2.5% |

| 1.4%% |

| 42% |

| A |

| Air Products and Chemicals ( APD ) |

| Chemicals |

| 2.5% |

| 11.3% |

| 62% |

| A |

| Kroger ( KR ) |

| Food & Drug Retailing |

| 2.4% |

| 14.9% |

| 23% |

| BBB |

| Hormel Foods ( HRL ) |

| Food & Tobacco |

| 2.4% |

| 8.6%% |

| 57% |

| A |

| Automatic Data Processing ( ADP ) |

| Software & IT Services |

| 2.3% |

| 13.3% |

| 58% |

| AA |

| Archer-Daniels-Midland ( ADM ) |

| Food & Tobacco |

| 2.2% |

| 5.0%% |

| 20% |

| A |

| Raytheon Technologies ( RTX ) |

| Aerospace & Defense |

| 2.2% |

| 4.8% |

| 45% |

| A- |

Average Yield : 2.7%

Before we dive into the numbers, let's talk about this selection. What we're dealing with is a list of companies that have massive footprints in the industries they operate in. We have the two big energy giants Exxon and Chevron, which are basically energy ETFs, given their size and diversified energy operations (upstream and downstream). They are also the highest-yielding stocks.

We have the two beverage/snack giants PepsiCo and Coca-Cola. Both come with decent yields as well. We have industrial stocks like Emerson Electric and Cummins, a chemical giant with hydrogen exposure (Air Products), and many more.

Moreover, except for Kroger , all these companies have A-rated balance sheets, which is important as we want a low-risk portfolio.

That is also the reason why I included companies like Archer-Daniels-Midland , a company that is key in the global food supply chain. Raytheon Technologies is a key supplier of aerospace engines, parts and defense equipment, and missiles. Texas Instruments is a chip heavyweight, while Union Pacific has one of the biggest moats imaginable, thanks to its duopoly with Buffett-owned BNSF.

While competition risks are always an issue, I believe the companies on this list are in a good spot to withstand high competition risks.

Moreover, not only do these companies come with an average yield of 2.7%, but they also consistently grow their dividends.

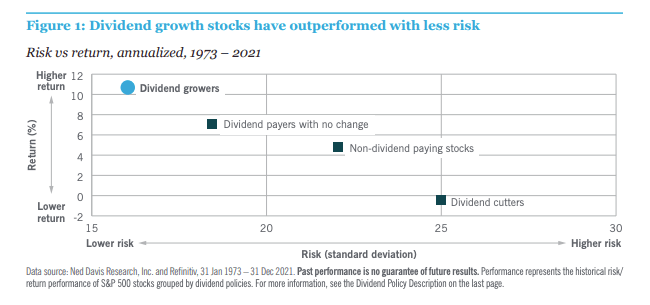

As I often explain, consistent dividend growth is the key to outperformance. Dividend-paying stocks tend to have a decent return with subdued risks. Dividend growers, however, have superior returns and risks that are well-below average.

{kind=link}

The theory behind this is rather simple. While a dividend transaction does not generate value (it's just a cash transaction from corporation to investor), it does send a signal: we're a company strong enough to share our profits with investors.

Doing this consistently while growing the dividend is not something a lot of companies can compete with. It's a stamp of approval. This a sign that a company can grow throughout business cycles, withstand secular economic changes, and whatever the market throws at it.

It's the reason why these stocks do rather well during bear markets, as investors sell low-quality stocks first. This bear-market outperformance is a huge driver of long-term outperformance.

After all, protecting one's downside is what makes or breaks an investment strategy. It's even more important than finding "multibagger" stocks.

Portfolio Performance

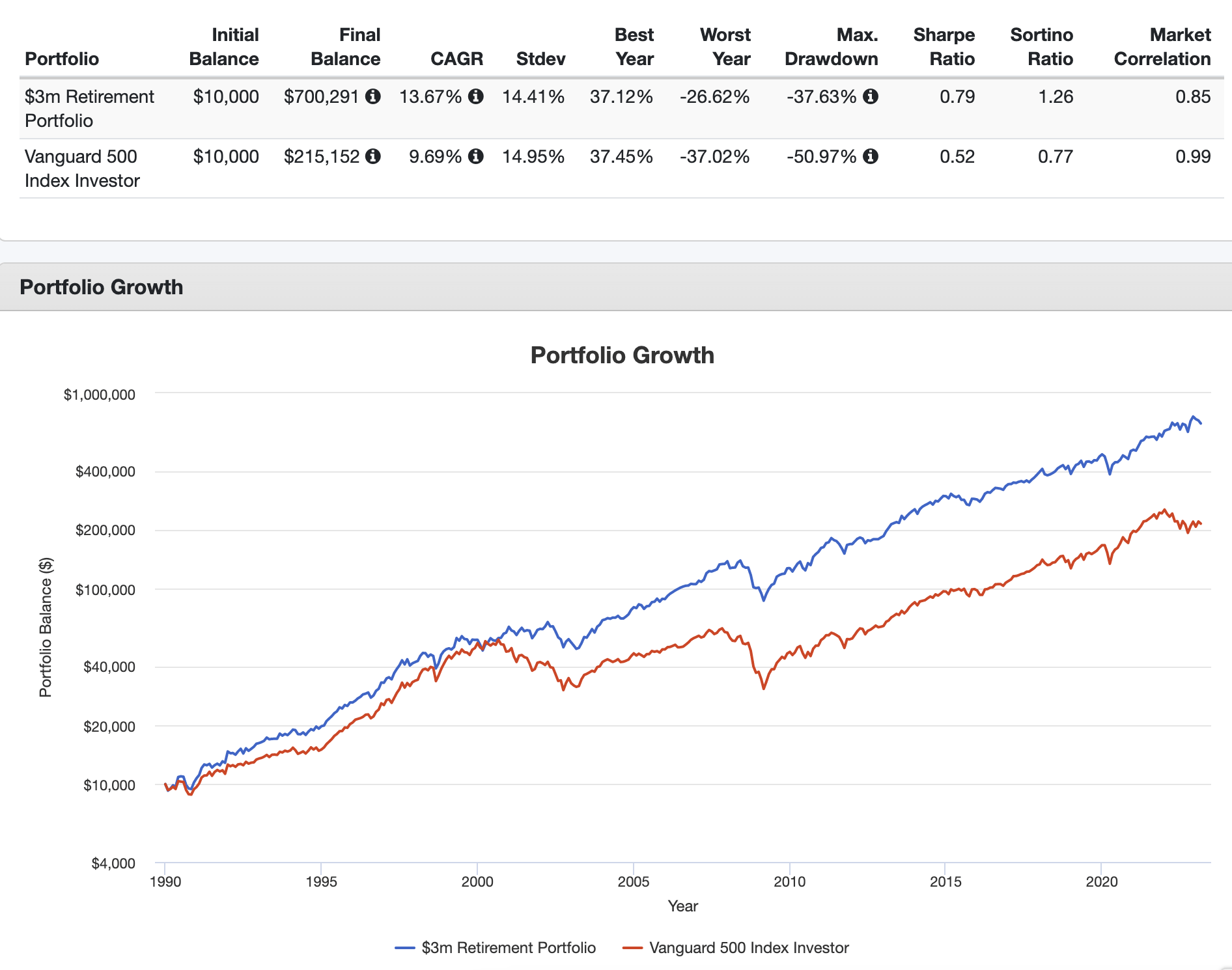

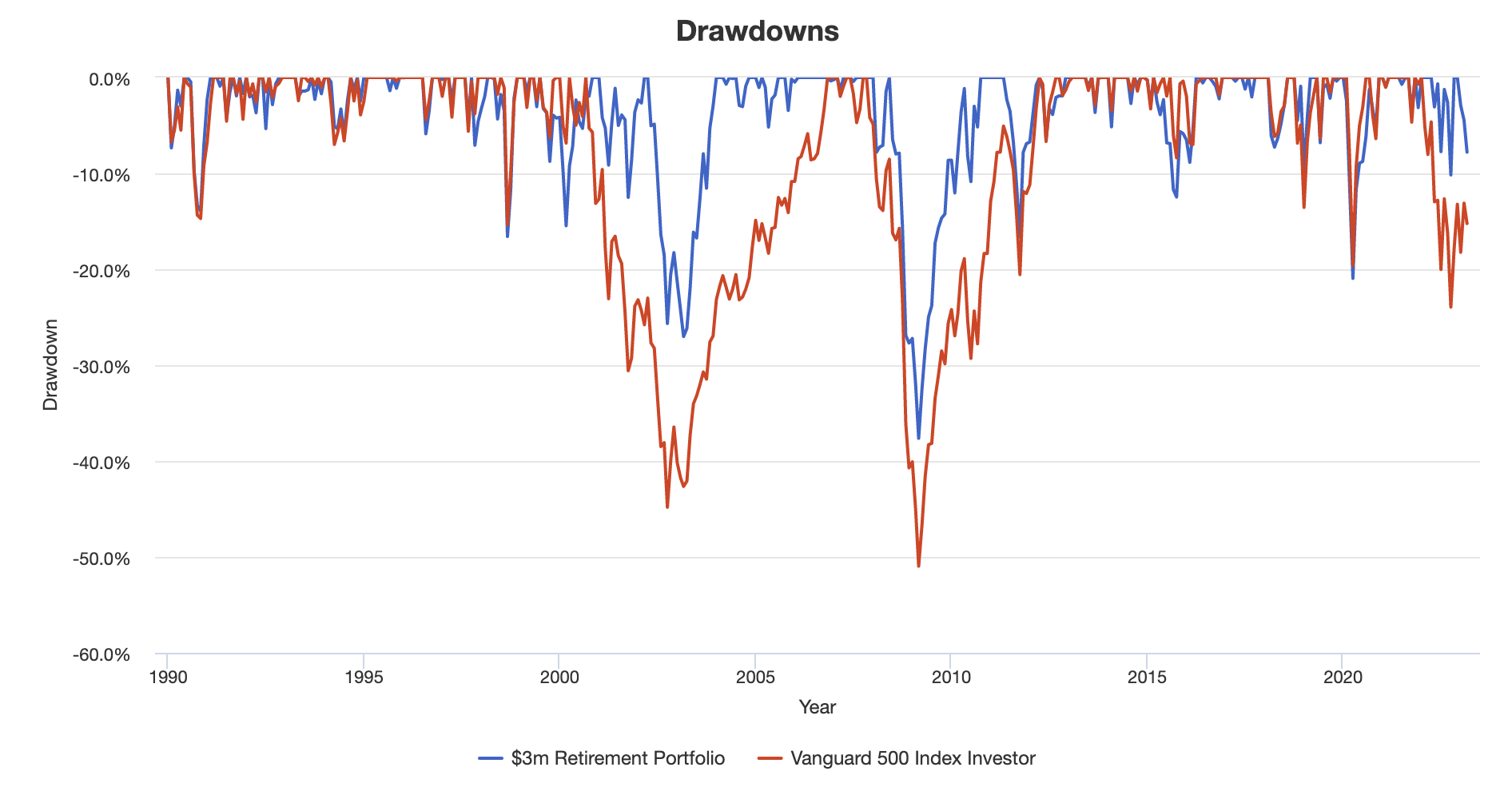

With that said, this portfolio did exactly what I expected before I looked at the numbers. Since 1989, this portfolio has returned 13.7% per year, which beats the S&P 500 by roughly 400 basis points per year. This would have turned an initial investment of $10,000 into $700,000 without any additional contributions. Moreover, the standard deviation is below average, despite the fact that the portfolio holds just 15 stocks! The worst year was just -27%. The portfolio never sold off more than 38% from its peak. That's still a lot, but bear in mind, it does not hold any bonds, it doesn't go short, and it beats the market by a mile (-50% max drawdown).

{kind=link}

In fact, the only time the portfolio did worse than the market was during the commodity/manufacturing recession of 2015, which did a number on energy and industrial companies.

{kind=link}

Now, you're probably wondering how the portfolio did in recent years. After all, we're dealing with mature companies that had much higher growth rates in the 1990s. Meanwhile, the S&P 500 benefited from massive growth in stocks like Apple ( AAPL ), Microsoft ( MSFT ), Amazon ( AMZN ), and others. This portfolio still holds the same stocks it had in 1990.

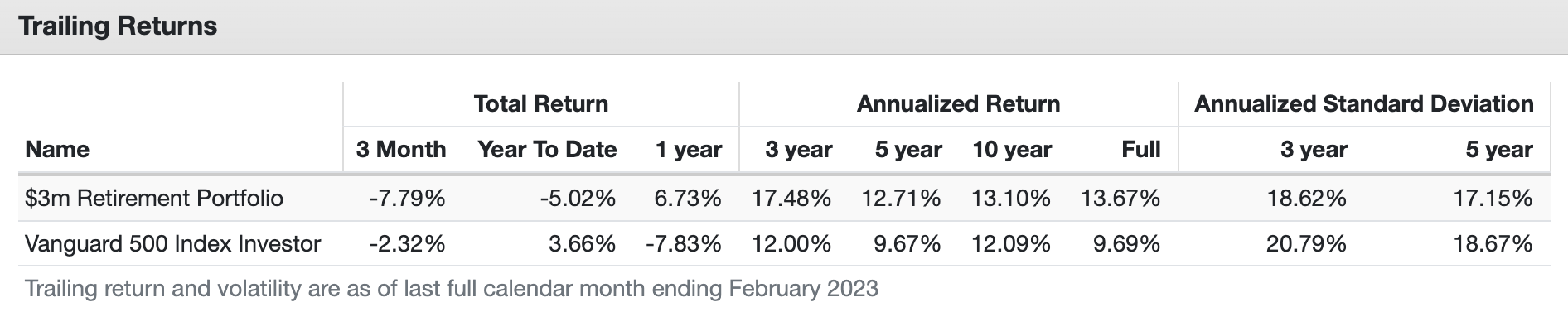

Looking at the table below, we see a number of time intervals. The model portfolio outperforms the market in every single time interval. Even over the past five and ten years, it generates higher returns than the market - despite having close to no technology/growth exposure! Think about that for a second. It perfectly confirms the theories that support dividend growth investing.

{kind=link}

Even better, the portfolio remained conservative, showing a below-average standard deviation on a three and five-year basis.

With that said, let me give you a few more numbers.

If investors had bought this portfolio in 1990 with an initial investment of $10,000 and a monthly contribution of $500, they would have ended up with $4.3 million pre-tax in February 2023.

Bear in mind, that's just $500 per month. Moreover, that number is adjusted for inflation, meaning less than $500 in prior decades.

Don't get me wrong, I know that people struggling with costs still aren't able to invest $500 per month. My aim is to show that one doesn't need to make a ton of money to build a massive nest egg.

But wait, there's more! As I made sure to pick stocks with a decent dividend, investors do not need to sell their initial investment once they retire!

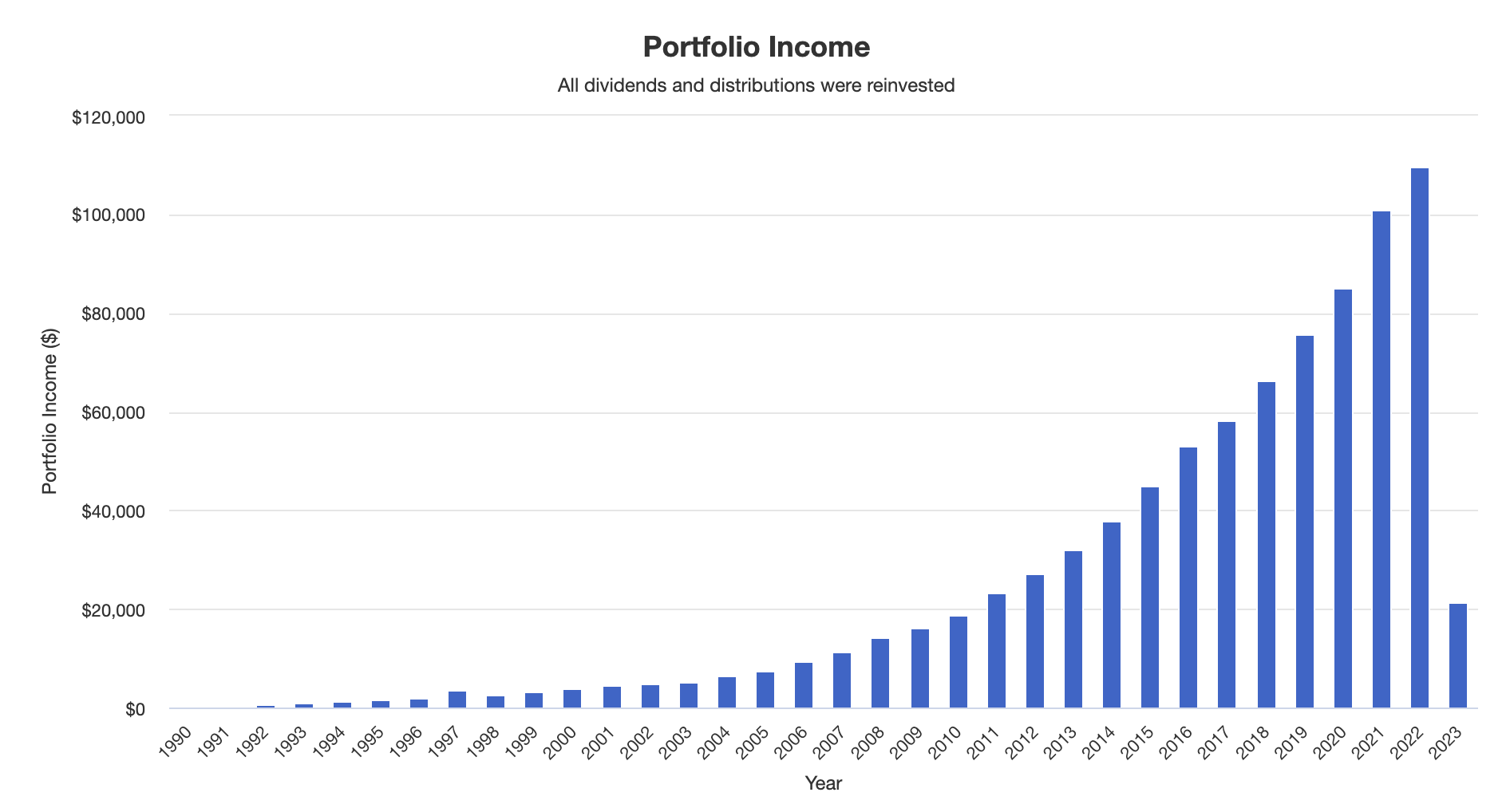

Last year, this portfolio generated $109K in pre-tax dividends. Where I come from, that guarantees a fantastic retirement.

Also, thanks to the magic of compounding, investors received more than $20K in dividends in the first two months of this year. That's as much as they got in all of 2010.

{kind=link}

And yes, nothing guarantees that these stocks will continue to outperform the market. However, everything that supported outperformance in the past is still valid.

So, I do expect these 15 stocks to continue to outperform the market.

Takeaway

In this article, we discussed a just-released survey, which showed that the average investor expects to need at least $3 million to retire. Unfortunately, most people are very far away from that goal and more than half of survey respondents aren't sure they will achieve their targets.

Hence, I presented a dividend growth portfolio based on decent yields, consistent and high dividend growth, rock-solid business models, and safe business models that will allow investors to invest for retirement.

While past results don't guarantee anything, I think we built a good framework that allows investors to outperform the market with subdued risks, while building a portfolio that allows them to retire comfortably or at least with a strong tailwind in case investors are already close to retirement.

On top of everything else, I was fascinated by the fact of how consistent the performance of this portfolio was, despite having very little exposure to high-flying stocks that boosted the S&P 500 in the past decade.

Going forward, we'll talk more about retirement and discuss investment opportunities that should help us reach our financial goals.

So, let me know in the comments how you are preparing! Maybe we can incorporate some of it in future articles.

For further details see:

The $3 Million Dividend Growth Portfolio That Could Secure Your Retirement