ARCC - The Battle Of Two Goliaths: Ares Capital Vs FS KKR Which One Will Win In 2024?

2023-12-29 09:32:54 ET

Summary

- The BDC market has been boosted by constrained access to conventional loans, high interest rates, and minimal corporate defaults.

- Ares Capital and FS KKR Capital are the largest and most liquid BDCs, making them attractive options for defensive allocation.

- In this article, I explain which one of these BDCs will likely deliver relative alpha performance in 2024.

Recently, I have been actively covering the BDC universe in an attempt to identify specific players which could be positioned to capitalize on the secular tailwinds in the private credit markets, while still preserving capital in case of a recession.

The current environment of constrained access to conventional loans, high interest rates, and minimal corporate defaults has boosted the overall BDC market. Even despite the recent runup in BDC capitalization levels, the average BDC yield, as implied from the VanEck BDC Income ETF (BIZD), still stands at a very attractive level of 10.9%.

Now the question is whether BDCs will continue to perform well going into 2024. Nobody knows as the underlying drivers in this current juncture are mostly of a systematic nature (e.g., level of interest rates, the pace of falling SOFR, corporate defaults in the system, etc.).

So my thinking here is to make sure of the following:

- Have the current yield show a sufficient margin of safety and protected from any shocks in the economy

- Have the portfolio more biased towards the conservative end even if that means foregoing a couple of percentages in yield, which would anyway be quite attractive

With this in mind, it certainly does not hurt if such allocations are assumed through the largest and most liquid BDCs out there:

- Ares Capital (ARCC) - the largest BDC with a market cap of ~$11.4 billion

- FS KKR Capital (FSK) - the second largest BDC with a market cap of ~$5.6 billion

Let's now explore and compare the two BDCs to determine which one of these is in a better position to register alpha (relative to each other and the BDC index) going forward.

I will not focus on aspects that are very obvious and have more or less the same patterns within ARCC and FSK structures, such as portfolio diversification, liquidity, and access to a diversified base of external leverage.

Instead, I will focus on - (1) valuations, (2) portfolio quality and (3) profile of external leverage as, in my view, these will be the key drivers of favourable risk-adjusted returns over the foreseeable future.

FSK is more attractively valued

In terms of the prevailing valuations between ARCC and FSK, the story is very straightforward. FSK is much cheaper.

RaymondJames, BDC report 2023-12

In the context of the overall BDC sector, ARCC trades at a slight premium, while FSK has massively diverged from the average with a 20% discount to its NAV.

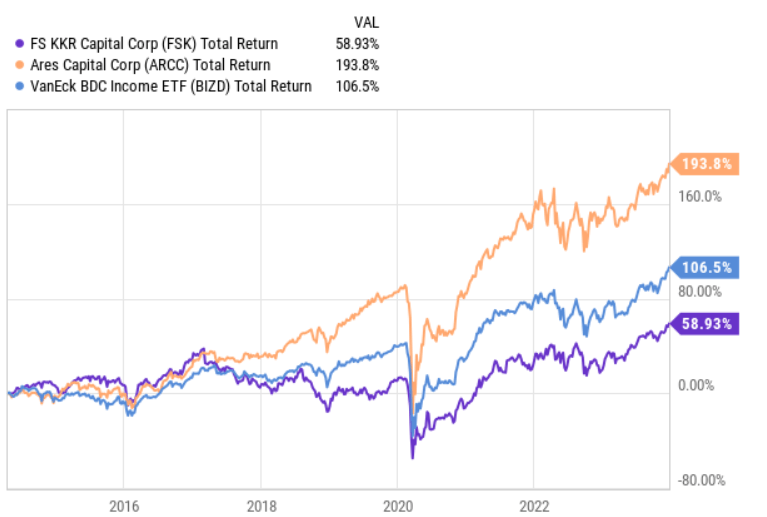

{kind=link}

Looking at the chart above, we can instantly notice how in the past 10-year period ARCC has managed to register outsized returns not only compared to the BDC index, but also relative to FSK. It is important to underscore that the presence of ARCC's alpha has been very consistent starting from 2017. In other words, for seven years in a row, ARCC has rewarded its shareholders with way more attractive returns than FSK.

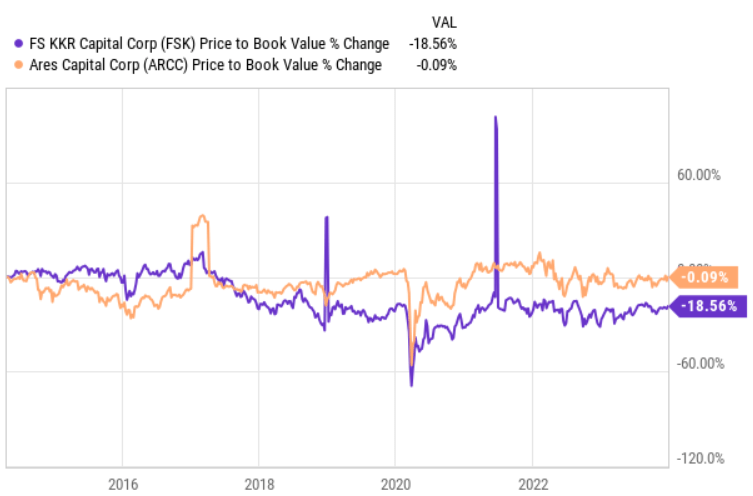

{kind=link}

This chart, in turn, indicates that the valuation (price to NAV) discount of FSK has closely correlated with the underlying underperformance, while ARCC has managed to keep this multiple stable over the past decade.

So, from a valuation perspective, there is no doubt that FSK, theoretically, provides a way more appealing entry point than ARCC, which trades at a premium of ~20.4% relative to FSK .

ARCC has a stronger portfolio, but not to an extent that justifies the entire discount

All in all, the general characteristics of ARCC and FSK portfolios are relatively similar.

Ares Management

For instance, ARCC has close to half of its AUM allocated into first lien senior loans, which are commonly deemed as one of the safest locations, where BDCs can channel financing. Yet, the total debt-like investment of ARCC accounts for ~90% of the portfolio (including preferred shares) indicating an additional layer of safety in terms of yield predictability.

{kind=link}

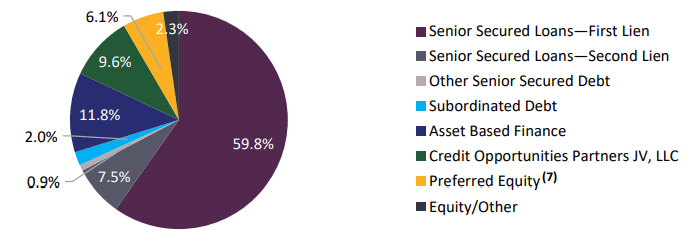

For FSK the portfolio breakdown is similar if not better. In this case, we can see a bit more focus on first lien investments (~60% of the portfolio) and an even smaller chunk of equity instruments. In fact, here we have ~12% of the total exposure stemming from an inherently sound segment - i.e., asset-based finance, which is not present in the ARCC's structure at all.

Having said that, there are a couple of ARCC-specific elements that offset the relative negatives described above and, in my opinion, render ARCC's portfolio slightly better than that of FSK.

First, is the average company size for which the financing has been provided.

In ARCC's case, the average EBITDA (as of Q3, 2023) of the underlying companies stood at $315 million, while for FSK the comparable figure was considerably lower at $118 million. Here we just have to remember that even $118 million in EBITDA is significantly above the norm in the BDC sector. Nevertheless, given the high EBITDA figure, ARCC is obviously more protected than FSK from potential struggles in the economy.

Second, the leverage profile of ARCC's portfolio constituents seems to be optically in a more favorable position.

ARCC and FSK disclose different and theoretically incomparable leverage KPIs of their companies, but based on the EBITDA factor as described above and the following data points, I think it would be fair to say that ARCC holds companies, that are less exposed to financial risk and have safer capital structures:

- ARCC's companies carry on average a LTV of 42%, which is surely in the safe zone (i.e., below 50%).

- FSK's interest rate coverage ratio has been on a constant decline since the pandemic years and currently has decreased to 1.5x. Typically, ICR below 2x is a level at which the market starts to factor in higher probabilities of potential distress.

Third, while earlier in the article I stated that on the diversification end both BDCs are well positioned due to their size and that I will not touch on this item, it is still worth distinguishing an important specificity of ARCC.

Ares Management

Namely, while ARCC embodies a clear focus on private credit, a notable chunk of the total AUM is actually spread across other types of credit opportunities, which introduces an additional layer of diversification benefit on top of the underlying diversity in the private credit structure.

In a nutshell, ARCC's portfolio is superior to FSK, mostly due to the quality of businesses for which the financing has been provided (albeit at slightly less favorable structures). Yet, this alone, in my opinion, is not enough to justify the valuation discount.

Leverage-wise, both are solid and in a position to enjoy favourable spreads

In the BDC business, one of the most critical things is to make sure that the spread between cost of capital and portfolio yields is high and stable over time. For this to happen, BDCs tend to source external debt proceeds in as cheap a manner as possible and then in most cases lock them in to capture some stability and predictability in the spread. Granted, this is also to some extent a balancing act between how much variable debt is assumed and how much is locked in via fixed-rate financing since the bulk of BDC (including ARCC and FSK) investments are based on SOFR, which per theory would require floating borrowing to isolate asset and liability mismatch risk.

{kind=link}

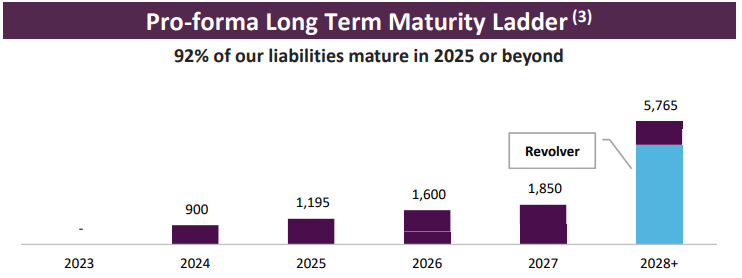

As of June 30, 2023, FSK had a 5.31% of weighted average interest rate stemming from its external borrowings. This is very low compared to the double-digit portfolio yields that FSK is able to capture from its investments.

More importantly, only 8% of the total debt proceeds mature before 2025, which means that in 2024 FSK will manage to maintain these spreads by avoiding significant refinancing events that could send the relevant interest rate closer to the market levels (which is somewhere between 7.5-9% depending on the debt structure).

Ares Management

The table above depicts a rather similar situation for ARCC as for FSK. Namely, as of June 30, 2023, ARCC had 5.44% weighted average interest and a debt maturity profile, where most of the borrowing fall due beyond the 2024 period; thereby allowing it to enjoy lucrative spreads between double-digit portfolio yield and the cost of capital.

The bottom line

Both BDCs are attractive investments and could be considered defensive long positions going into 2024 with decent yield stability.

Yet, in my view, FSK's 20% discount to its NAV and compared to ARCC lacks sufficient basis, which, in turn, indicates that FSK could be a greater BDC investment with a higher probability of outperforming ARCC from multiple convergence.

Granted, ARCC carries a higher quality portfolio, but the difference is not great enough to justify the valuation gap. Plus, we have to remember that FSK offers a ~300 basis points higher yield (~12.7%) than ARCC, which is more than enough to compensate for a slightly worse portfolio quality.

For further details see:

The Battle Of Two Goliaths: Ares Capital Vs, FS KKR, Which One Will Win In 2024?