LI - The Diverging Growth Story Of NIO And Li Auto

2023-06-07 11:42:28 ET

Summary

- Despite starting off on a stronger foot, NIO's growth has been decelerating while rival Li Auto's deliveries continue to defy a slow-growing Chinese economy with profitability cushioning investor confidence.

- This has led to a widening divergence in both companies' fundamental and valuation outlook.

- The following analysis will gauge the similarities and differences in both companies' forward growth roadmaps and discuss their respective implications on the stocks' prospects ahead.

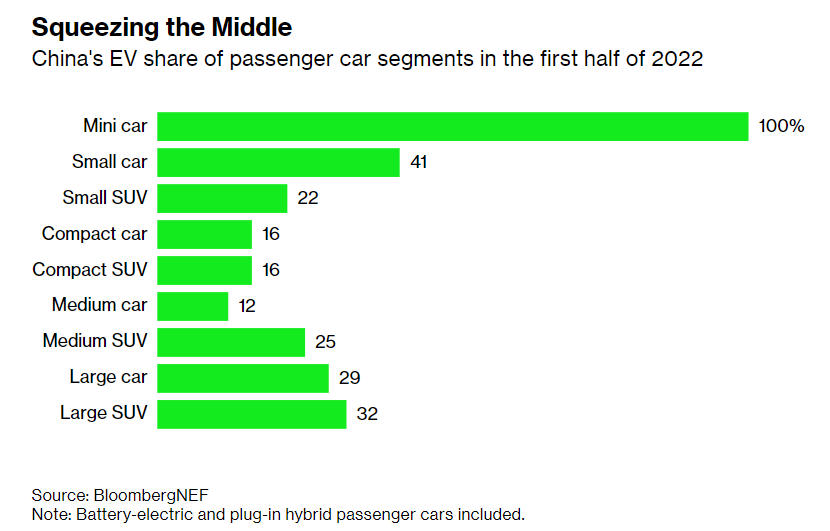

China continues to account for the lion’s share of the global EV market, with 1.5 million units sold in the first quarter alone. The Chinese market now accounts for almost 60% of global EV sales, with one in three new cars sold in the region now either a battery or plug-in electric vehicle. Despite the recent retraction of a decade-long EV subsidy program initiated by the Chinese central government – which had been critical in pushing the technology into mainstream adoption – and a shaky economic recovery, the region remains on track to increase EV sales by 30% this year to more than 6.4 million units.

NIO ( NIO ) and Li Auto ( LI ) were our first coverages on the Seeking Alpha platform, and it has been impressive to see how fast the two Chinese automakers have grown their market share over the past several years, despite unprecedented industry challenges spanning the pandemic and acute supply chain constraints during the period. Our visit to China earlier this year also provided validation on Li Auto and NIO’s growing brand reputation in the region, especially across higher-tier economic zones where the EV adoption rate has been highest.

In addition to juggernauts like BYD ( OTCPK:BYDDF / OTCPK:BYDDY ) and Tesla ( TSLA ), Li Auto has been an uprising winner – especially in the premium electric SUV segment – despite our earlier skepticism over the durability of its preference for hybrid powertrains amid stringent emissions standards that will eventually favour fully battery electric vehicles. Meanwhile, despite targeting a similar premium end-market, NIO’s market share gains have been decelerating in recent quarters, as rival Li Auto’s continues to rise at a relatively rapid pace , with ensuing scalability likely helping its margin preservation efforts under a slowing domestic economy and increasingly competitive EV landscape. The following analysis will gauge the diverging growth story between two of China’s most prominent homegrown EV brands, despite similarities ranging from their direct sales and vertically integrated business models to premium end-market appeal.

Li Auto – The Uprising Star

During our recent visit to China, we were surprised at the number of Li ONE hybrid plug-in SUV sightings – not only in the city but also on cross-country highways – which corroborates the brand’s rapid share gains in recent quarters, especially after the expansion of its line-up with new models. Similar to rival NIO and XPeng’s ( XPEV ) vehicles, sightings of the Li ONE were no less than Teslas, while BYD vehicles – across both new electric and old ICE powertrains – continue to dominate the roads.

Recall that Li Auto came out of the gates with a differentiated strategy from its domestic EV pureplay peers. While it targeted the premium segment like NIO, Li Auto started off with a single SUV model – the Li ONE. Unlike many of its EV pureplay peers at the time, the flagship ONE SUV runs on a hybrid plug-in powertrain. It also boasts more than 40 premium features in one standard package, which was comparable to other luxury SUVs in the RMB 600,000+ ($85,700) range, but at an attractive fixed MSRP of RMB 328,000 at launch in 2019 (the car sells for RMB 349,800 today).

Initially, we had outlined our skepticism over Li Auto’s brand differentiation strategy. While hybrid powertrains represent a good option in addressing prospective buyers’ range anxiety – which is still a key barrier to EV adoption today, despite significant improvements made in battery technologies and the availability of public charging infrastructure – relying solely on it did not seem like a durable strategy compared to EV pureplays in the industry that were boasting development of proprietary battery technologies with best-in-class range per charge amid the increasingly stringent emissions policy environment at the time. This was especially true given hybrid models were typically viewed as a “layover” strategy implemented by legacy automakers in their respective transitions to electric as a mean to soften the impact of phasing out ICE vehicle sales and preserve cash flows.

But looking in hindsight, the strategy appears to have paid off by paving the way for the brand’s ultimate debut of fully electric models by mid-decade:

…Li Auto's president and chief engineer Ma Donghui said the line-up by 2025 will include one flagship model, five range-extended electric models and five high-voltage pure electric models.

Source: Reuters

The simplified, yet focused, business strategy of offering one, single-variant plug-in hybrid model at launch has likely played a significant role in helping Li Auto establish its brand reputation and build sustained market share gains, which inadvertently supported scale towards profitability. And its roll-out of additional models (namely, the L9, L8, and L7 SUVs) over the past 12 months underscores further market share expansion in the years to come, as the company seeks to further its penetration into new pricing and vehicle segments.

In addition to building out its brand and the underlying business’ fundamental strength, the focus on selling a single-model premium plug-in hybrid SUV at an affordable price range in the meantime has allowed Li Auto to expand and sustain operations, while waiting for maturity in supporting technologies and infrastructure needed to enable mass market EV adoption. Specifically, EV battery technology and availability of public charging infrastructure in China have improved significantly in the three years since the Li ONE’s debut. Even without Li Auto’s proprietary “extended-range” EV powertrain – which combines plug-in charging and a fuel tank to enable as much as 1,315km / 817 miles of range at full power capacity – its roadmap for “High Power Charging Battery Electric Vehicles”, or “HPC BEVs”, is expected to alleviate range anxiety by enabling best-in-class fast charging.

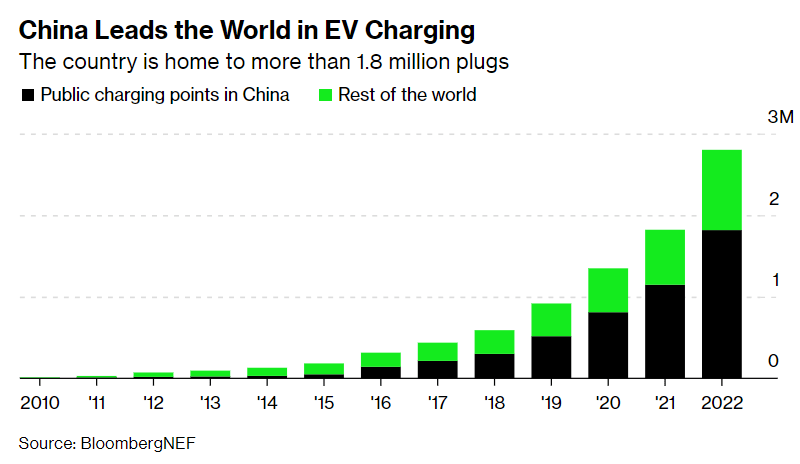

The HPC BEVs are part of Li Auto’s longer-term growth strategy . The company aims to roll out five HPC BEV models by mid-decade to accompany a slate of five EREV models that include the existing Li ONE, L9, L8 and L7 SUVs. The fully electric segment is expected to “include an 800-volt electric drive system based on the third-generation silicon carbide power module”, which paired with Li Auto’s ongoing build-out of its fast-charging network is expected to enable 400 km / 250 miles of range “with just a 10-minute charge”, replicating ICE vehicle refuelling time efficiency. The next growth phase at Li Auto also complements the significantly improved public charging scene in China today, which has ballooned to “more than 1.8 million plugs” from merely 800,000 in 2018, and accounting for two-thirds of the global fleet. This is equivalent to about one plug per seven EVs in the region, which compares to a ratio of one-to-18 in the U.S.

{kind=link}

Bloomberg News

About half of them are equipped with fast-charging capability, accompanying improvements in battery technologies available in the market today that have been critical in narrowing the time efficiency gap between EVs and ICE vehicles. The batteries that will be powering Li Auto’s planned HPC BEVs, for example, stem from CATL’s latest “ 4C-rate Qilin ” technology, enabling a charge speed of just 10 minutes from 10% to 80%. The Qilin cell-to-pack (“CTP”) technology boasts a “volume utilization efficiency of 72% and energy density of up to 255Wh/kg” when fitted with the traditional nickel-cobalt-manganese (“NCM”) cell composition, up from the average 160Wh/kg to 190Wh/kg observed in the current low-cost LFP cells that power standard Tesla Model 3/Ys. The Qilin CTP technology, when combined with NCM packs, are capable of “delivering a range of over 1,000 km [620 miles] in a breeze, validating Li Auto’s plans to offer a similar extended range capacity in its upcoming HPC BEVs as its existing portfolio of EREVs.

The technology is also expected to differentiate Li Auto’s HPC BEVs from rising competition as battery prices come down with continued innovation. In addition to the common LFP packs currently integrated in many standard models, battery makers are already in the process of developing next-generation technologies like lithium-iron-manganese-phosphate (“LMFP”) batteries. The LMFP composition can achieve as much as 240Wh/kg, up from the energy density ceiling of 190Wh/kg in current LFP cells, with an additional 5% discount on costs. Taken together, LMFP batteries, which are expected to start productions in mid-2024, can drive up to 25% in savings compared to traditional NCM cells. This spells further range and price competition for China’s burgeoning EV market ahead. And Li Auto’s focus on first locking-in its market share and profitability through plug-in hybrids, then pursuing purely electric opportunities with an anticipated range advantage when costs and battery technologies approach operational efficiency parity with ICE vehicles, comes at an opportune time.

Li Auto - Fundamental and Valuation Analysis

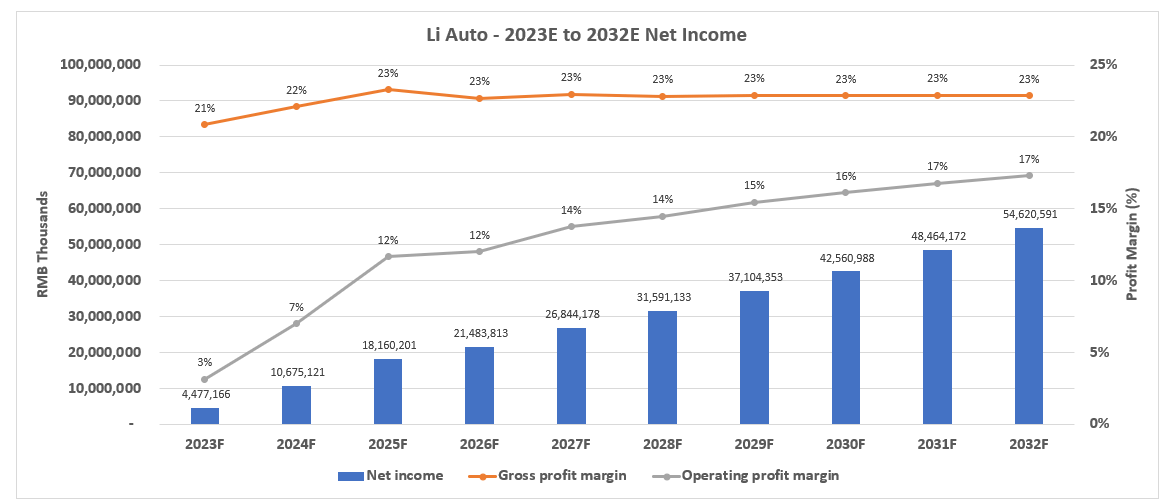

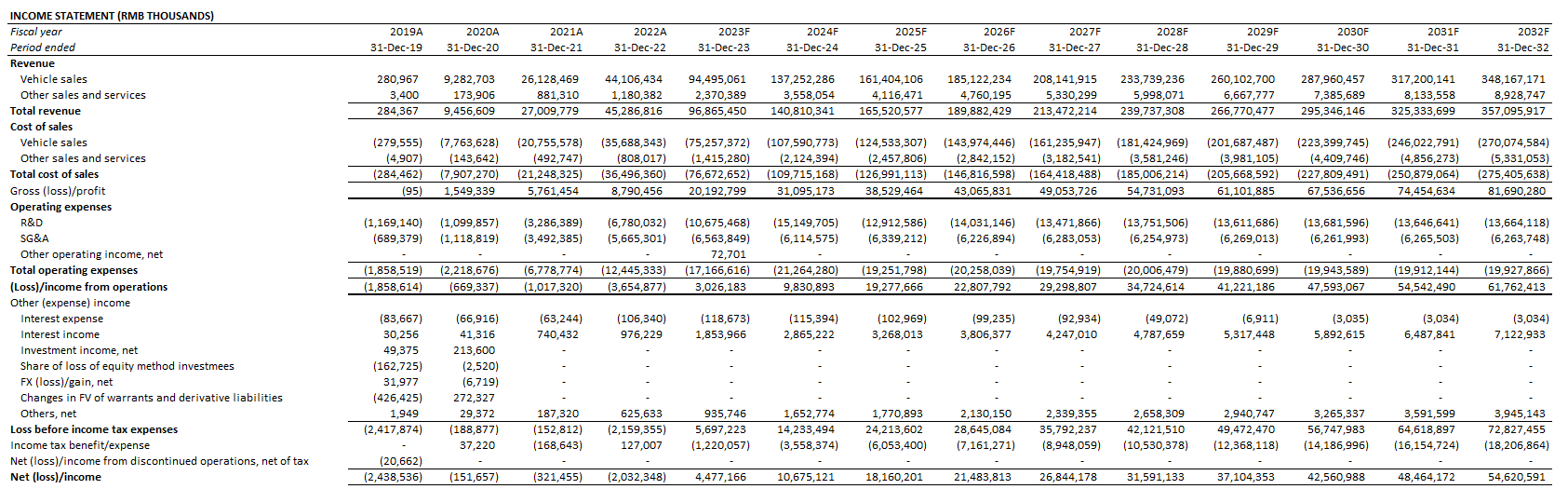

From a fundamental and valuation perspective, Li Auto also demonstrates favourable prospects ahead. It is all written in its results in recent quarters, with deliveries soaring by triple-digits in a slowing economy. Meanwhile, GAAP profitability observed over the past two quarters has also become more durable with positive operating income in the first quarter.

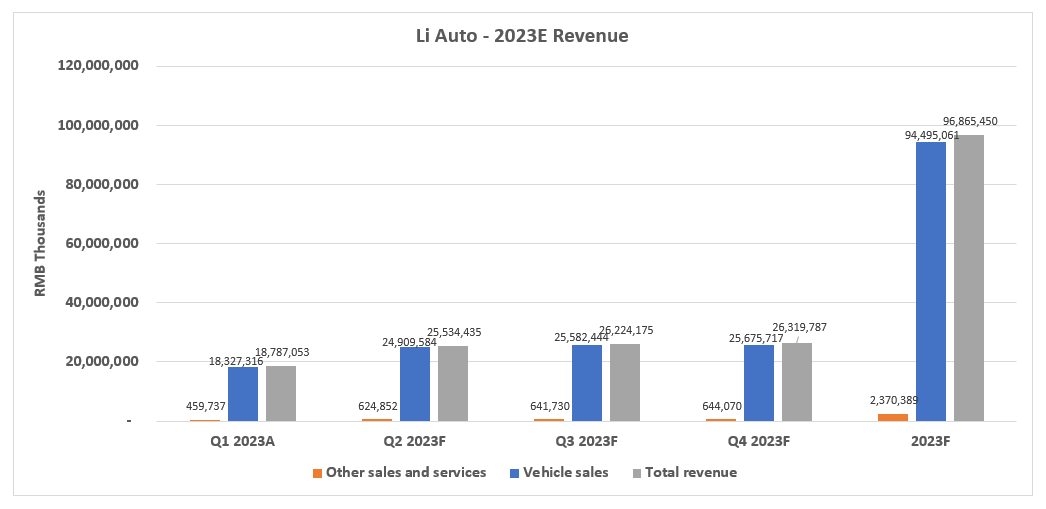

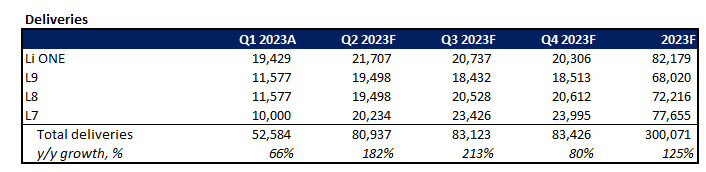

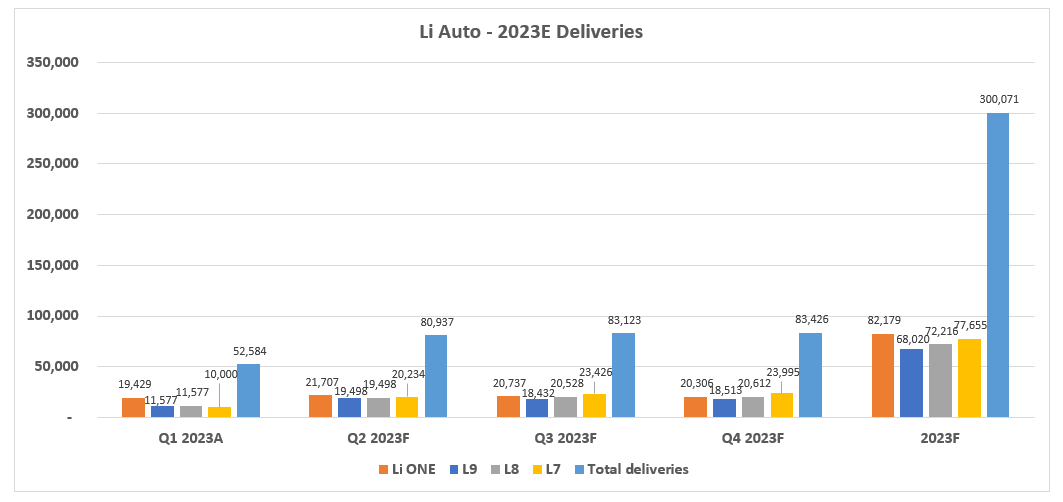

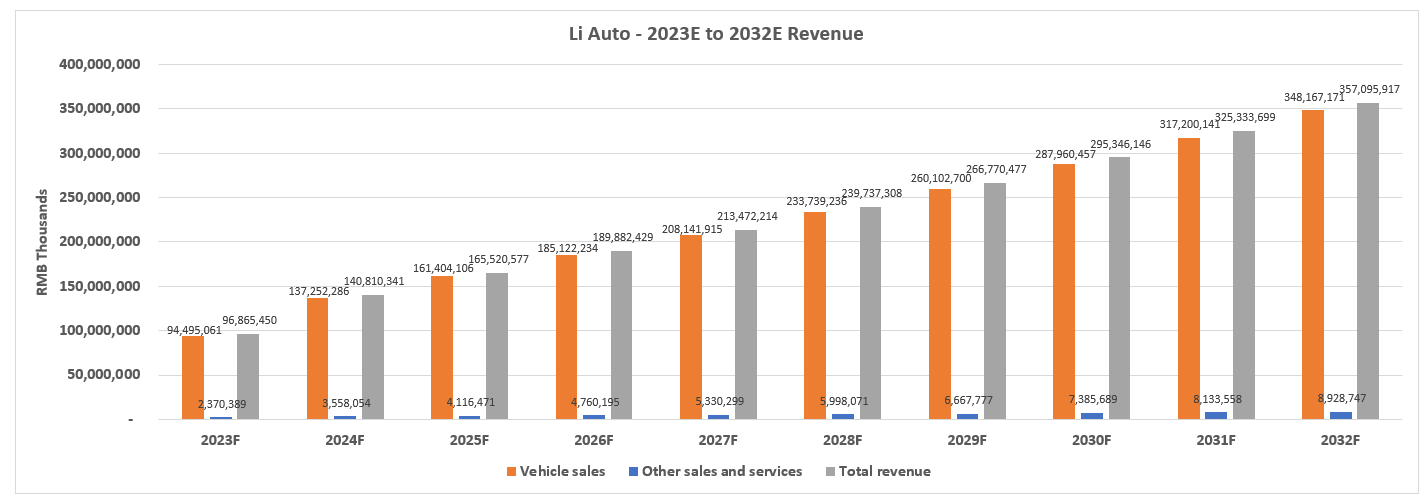

Looking ahead, with expectations for continued ramp up in deliveries of the new models, helped by Li Auto’s affordable pricing strategy in offsetting near-term macroeconomic challenges, the company is expected to reach RMB 97 billion in consolidated revenue this year, with more than RMB 94 billion generated from vehicle sales. This would imply deliveries of approximately 300,000 vehicles this year, representing growth of 125% y/y.

{kind=link}

Author

{kind=link}

Author

{kind=link}

Author

{kind=link}

Author

And over the longer-term, with the addition of incremental EREV and HPC BEV models to its line-up to bolster market penetration, Li Auto’s total revenues are expected to expand at a 14% CAGR over the next ten years. The expansion is expected to be primarily driven by the addition of more affordable models in the longer-term, including the planned L6 and L5 which management has said would “stick to the RMB 200,000 to RMB 300,000 price range”, which would improve mass market penetration.

{kind=link}

Author

{kind=link}

Author

With Li Auto having achieved two consecutive quarters of GAAP net income, alongside positive operating margins during the first quarter despite having to simultaneously ramp productions of three new models in addition to the existing Li ONE SUV, the company has proven durability to its profit profile. The company’s gross profit margins are expected to expand from the current low-20% range to the mid-20% range as sales growth continues to drive scalability over the longer-term, in line with levels observed at current market leaders like Tesla. Taken together with continued operating margin improvements through scale in R&D and sales, general and administrative spend over the longer-term, Li Auto is expected to further expand its bottom-line, bolstering durability in its cash flow generation and, inadvertently, its valuation prospects.

{kind=link}

Author

{kind=link}

Author

{kind=link}

Author

{kind=link}

Author

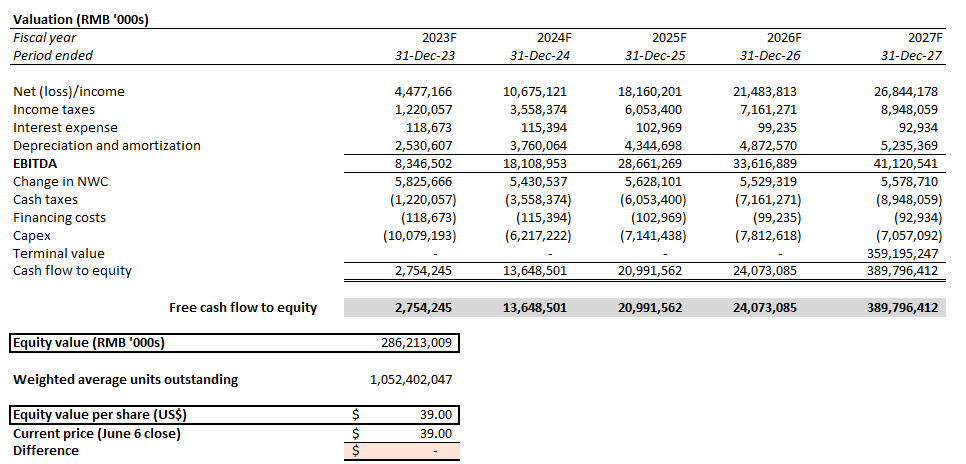

Li_Auto_-_Forecasted_Financial_Information.pdf

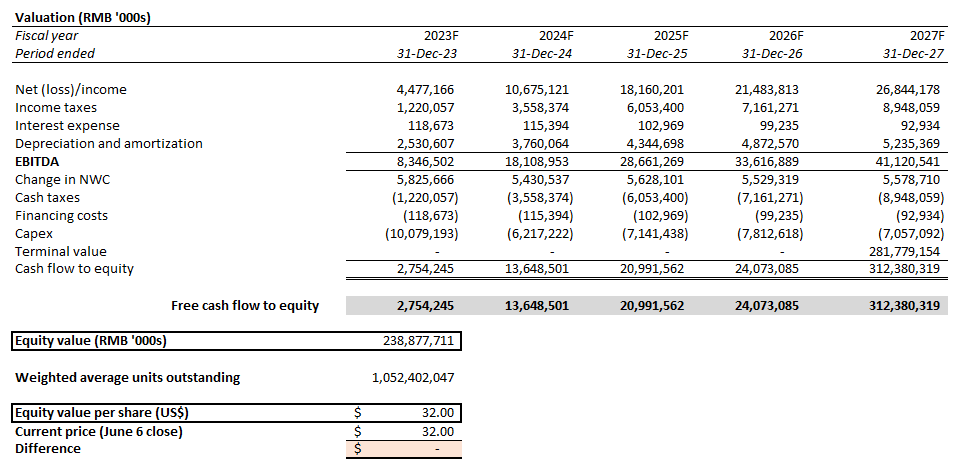

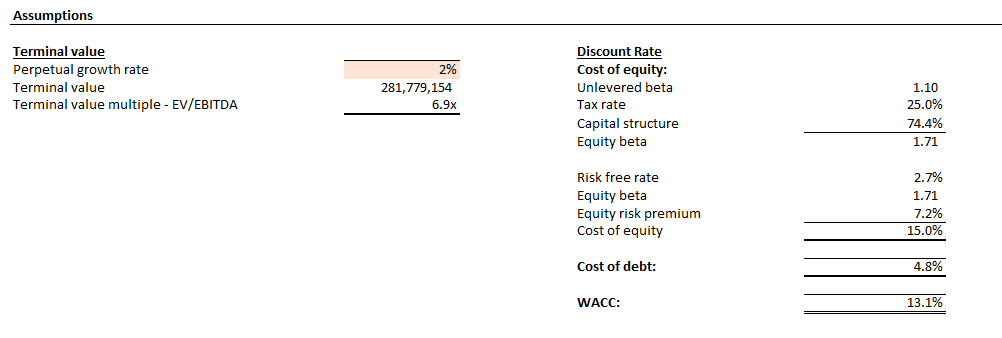

Based on the discounted cash flow analysis on projected cash flows taken in conjunction with our fundamental forecast for Li Auto, with the application of a 13.1% WACC in line with the company’s capital structure and risk profile, the stock’s current price at about $32 apiece implies a perpetual growth rate of about 2%.

{kind=link}

Author

{kind=link}

Author

While this is not reflective of the company’s longer-term growth prospects considering its roadmap for further market share gains across the Chinese EV market, and discounted from the anticipated pace of economic expansion in the region, the 2% implied perpetual growth rate reasonably reflects ongoing market conservatism over industry-specific and macroeconomic risks. In addition to the lacking appeal of capital-intensive endeavours under the current market backdrop, Li Auto’s operations in China also subjects investors to elevated geopolitical and regulatory uncertainties, which have been driving the ongoing valuation discounts observed across U.S.-listed Chinese equities compared to their American counterparts.

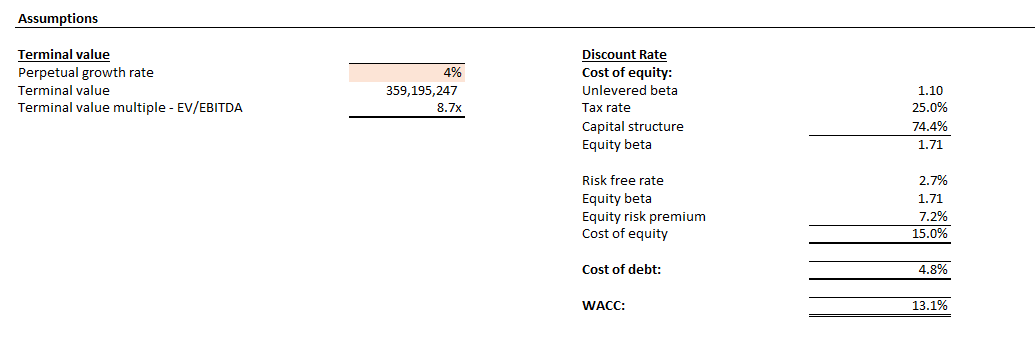

However, considering Li Auto’s profitability – a rare sighting across NEV pureplays both within and outside of China – we believe the stock has a fundamental advantage to drive incremental upside potential over the near-term despite the lingering industry-specific, macro, geopolitical and regulatory risks. Based on the current average consensus price target of about $39 on the stock, Li Auto’s free cash flows to equity are expected to expand at an implied perpetual growth rate of about 4%, which is in line with the anticipated pace of longer-term economic expansion in China, its core operating region, and reflective of Li Auto’s growth role in the Chinese economy.

{kind=link}

Author

{kind=link}

Author

Continued outperformance in delivery volumes in the near-term, alongside consistent margin expansion, would be critical in maintaining investor confidence in the stock despite the risk-off market climate, as such accomplishments would provide validation to Li Auto’s business strategy in defying ongoing macroeconomic weakness. Meanwhile, checking off items on its longer-term growth roadmap (e.g. the introduction of HPC BEVs) would reinforce durability to its trajectory in capturing market share, and reduce its valuation’s exposure to execution risks.

NIO – It’s Getting There

As discussed in a previous coverage , NIO vehicles – especially their SUVs – are also frequently seen in China’s more affluent cities and on cross-country highways like the Li ONEs. But unlike Li Auto, ongoing headwinds spanning a slow economic recovery, stiffening competition, and lingering supply chain bottlenecks have collectively stifled NIO’s growth story in recent quarters.

While NIO targets a similar premium SUV segment as Li Auto, with incremental expansion into the premium sedan segment in recent years, its pace of market share gains have trailed Li Auto’s by a widening margin in recent quarters. Not only have monthly delivery volumes been declining in April and May, but the company’s margins have also been compressed by incremental production ramp-up costs of its newer models and a higher material cost environment. This has collectively dulled the appeal of NIO's stock in the risk-off market climate, as investors continue to chase profitable growth amid mounting macroeconomic uncertainties.

As mentioned in the earlier discussion on Li Auto, affordability has continued to be the predominant driver of purchase decisions, especially given lingering economic weakness in China. And this has likely been an increasing challenge to NIO’s efforts in reinforcing sales growth, given its cheapest offering available right now – the standard ET5 five-seater compact sedan – starts at RMB 328,000.

Prospective buyers’ preference for affordability is further corroborated by the accelerated take-rate of NIO’s new sedan offerings in recent months. Although NIO no longer discloses the breakdown of its more expensive ET7 and cheaper ET5 sedan sales, combined deliveries of both models have surpassed SUV deliveries in the first quarter , and continues to exhibit similar trends in April and May . And the cheaper ET5 sedan has likely dominated NIO’s total sedan deliveries, given the last time it had separately disclosed sales of its two sedan models indicated an ET5 take-rate that had exceeded the ET7’s by a wide margin:

NIO delivered 15,815 vehicles in December 2022, a new record-high monthly delivery, representing an increase of 50.8% year-over-year. The deliveries consisted of 6,842 premium smart electric SUVs including 4,154 ES7s, and 8,973 premium smart electric sedans including 1,379 ET7s and 7,594 ET5s.

Source: ir.nio.com

While NIO has turned to brand-specific gimmicks like its battery subscription service, or BaaS , and proprietary battery swap technology, to reduce vehicle pricing for customers and bolster differentiation of its brand from competition, its fundamental performance in recent quarters indicate an “affordable or bust” mentality across the bulk of its prospective buyers as China reels from an economy that is struggling to recover from yearslong pandemic restrictions. This also leads us to think of the impact that the central government’s retraction of its EV purchase subsidy program this year, which NIO had benefited from thanks to its proprietary battery swap technology, might have had, in addition to the mixed economic recovery, on the company’s demand environment.

According to the 2020 policy, only passenger EVs costing less than RMB 300,000 (US$42,376) per unit are eligible for the fiscal incentives, along with the above-mentioned conditions for mileage and power efficiency.…vehicles with battery-swapping functions are exempted from the limit on vehicle price, to promote technology and battery swapping as a business model.

Source: China Briefing

This leads to speculation that recent expectations for a revival of the subsidy program later this year, as part of Beijing’s broader efforts in shoring up China’s sluggish economy, would be a potential catalyst to jumpstarting NIO’s sales by making their cars more affordable relative to rival offerings. Specifically, the central government is considering extension of the fiscal financial incentives for EV purchases, including a purchase tax break, for new energy vehicles – including battery electric and plug-in hybrid vehicles – priced below the RMB 300,000 threshold. While none of NIO nor Li Auto’s existing EV models would qualify based on the pricing threshold, NIO just might have a chance of being exempt like in the previous incentive program given its rigorous build-out of battery swapping stations and related in-vehicle technologies to facilitate China’s electrification goals.

Improved affordability through extended fiscal policy support, as well as burgeoning opportunities in the mid-sized EV market in China are expected to be complementary to NIO’s longer-term growth story as well – especially as it ramps its mid- and compact-sized offerings spanning the newest ET5 sedan , EC6 Coupe SUV , and ES6 SUV .

{kind=link}

Bloomberg News

And onto something more concrete, NIO’s plans to further its presence in lower-tier economic zones across China with the upcoming launch of two mass market sub-brands will be of further importance in addressing consumer demand for affordability. And the company’s battery swap technology is expected to be a complementary advantage in its expansion to the less penetrated tier 3 and below economic zones, where public chargers (let alone fast chargers) are hard to come by, hence the lack of EV adoption in those regions despite availability of bargain options like the GM-SAIC-Wuling Hongguang Mini . With NIO’s battery swap stations capable of switching a dead battery for a fully charged one within minutes (each Power Swap Station is capable of finishing 312 swaps on average per day), the fleet’s expanding presence can address range anxiety better and faster than building out plug chargers, and quickly accommodate go-to-market plans for the upcoming mass market sub-brands.

When it comes to the expansion into the sub-tier cities, we're not talking about the deployment of the NIO houses or NIO spaces. We believe that the more efficient way is to deploy the power swap stations in the sub-tier cities.

NIO - Fundamental and Valuation Analysis

Admittedly, the endeavour will weigh further on NIO’s margins as the company seeks to simultaneously ramp up its new premium offerings to stay competitive within the increasingly crowded EV landscape in China. The ongoing build-out of its NIO Power and NIO Power Swap stations will be crucial to facilitating the adoption of its core and sub-brands, but the capital-intensive investments ahead will likely delay its profit realization timeline and deter investors from the stock.

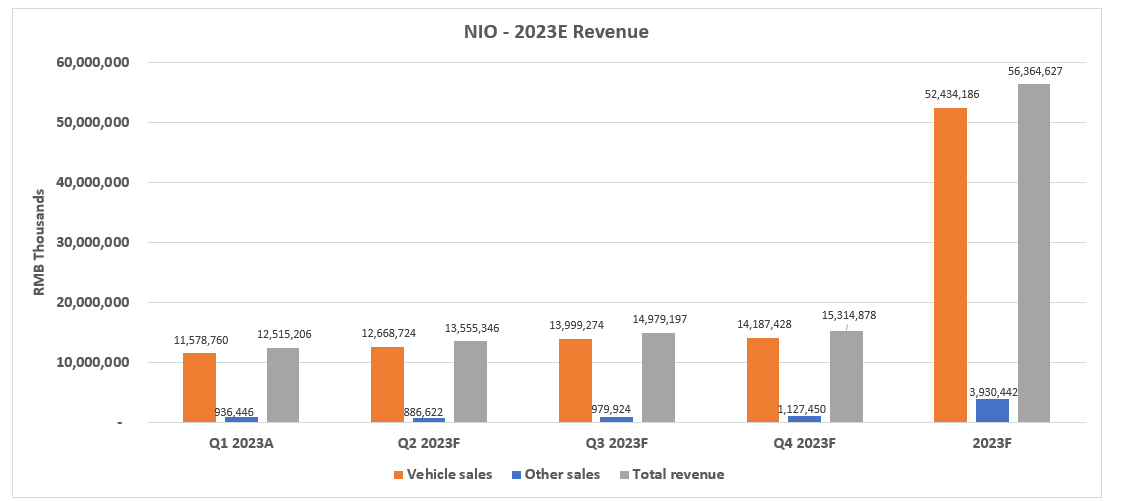

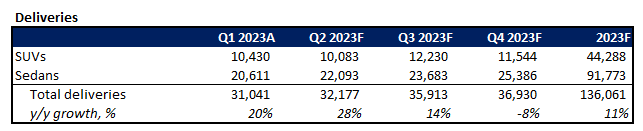

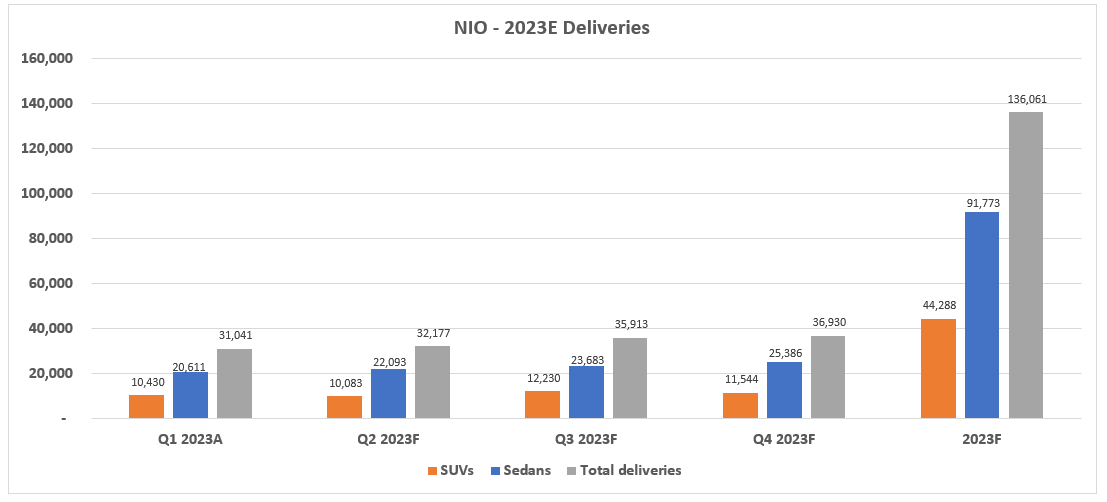

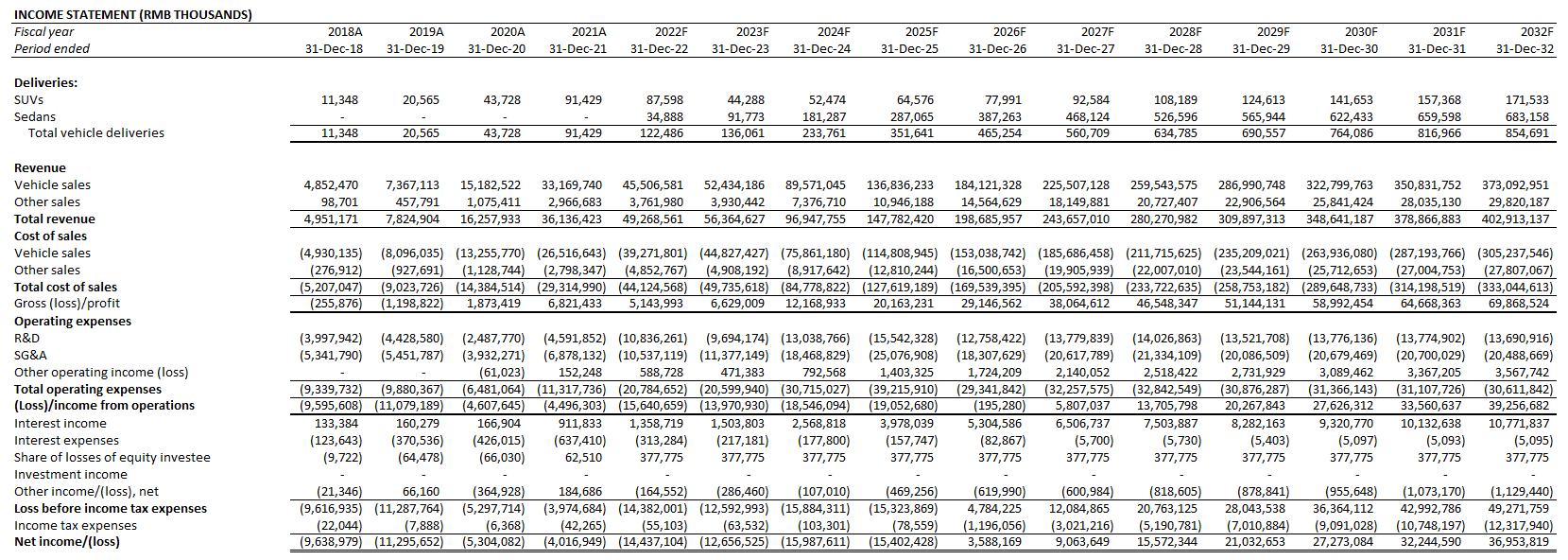

Considering NIO’s near-term demand environment, the company is expected to finish the year with about 136,000 deliveries, driven primarily by its lower-priced sedans. Related revenues are likely to finish around the RMB 56 billion mark this year, with the average vehicle selling price to hover in the high RMB 300,000 range, in line with observations in 2H22 after NIO introduced a mix of both higher- and lower-priced sedan and coupe models to its existing portfolio of offerings.

{kind=link}

Author

{kind=link}

Author

{kind=link}

Author

{kind=link}

Author

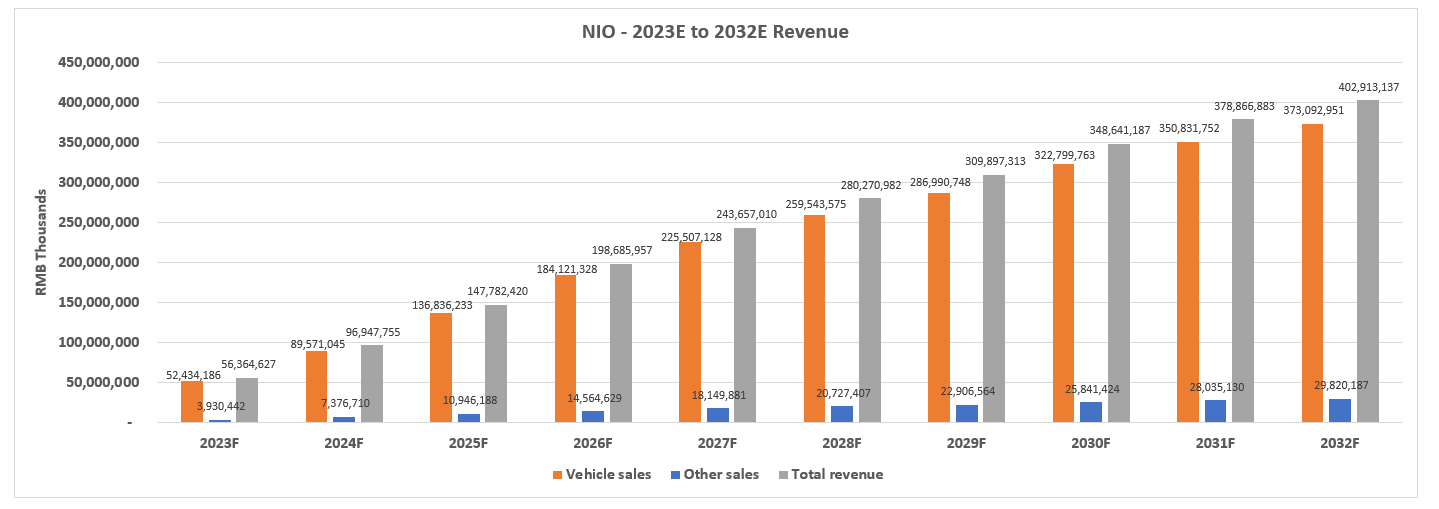

And over the longer-term, considering the durable brand reputation NIO has built in recent years, alongside budding opportunities in the mid-sized EV segment in which the company’s core brand has been looking to gain share with the introduction of new sedan and coupe models, the company is expected to expand deliveries beyond the 854,000 mark by 2032. This would represent a 10-year CAGR of about 20% at NIO to potentially make up for lost ground to competition like Li Auto in recent quarters, as it penetrates opportunities in new markets through diversified offerings. Considering NIO’s higher ASP, its revenues are also expected to expand at a faster pace of about 21% on average over a 10-year forecast period relative to rival Li Auto’s estimated 14%.

{kind=link}

Author

{kind=link}

Author

While NIO management is targeting to breakeven by next year, realizing such ambitions are highly unlikely considering near-term demand challenges due to transient macroeconomic headwinds, as well as its compressed vehicle margin profile observed in recent quarters. While NIO’s newest NT 2.0 platform – on which its newest vehicles are built – is expected to drive greater production efficiency and enable higher margins, those benefits are unlikely to be realizable within the foreseeable future given ongoing early-stage ramp up costs. This is consistent with the drastic reduction in vehicle gross margins from the 20% range observed in early 2021, to the sub-10% range observed in recent quarters following the introduction of the ET7 and ET5 sedans, as well as the revamp of its existing SUVs. Ongoing R&D spend is likely to remain elevated to support the continued improvement and expansion of its proprietary battery technologies – including the 150 kWh “semi solid-state battery” slated for start of production soon to enable range of up to 1,000 km / 620 miles per charge in newer models like the ET7, as well as the ongoing build-out of Power Swap stations.

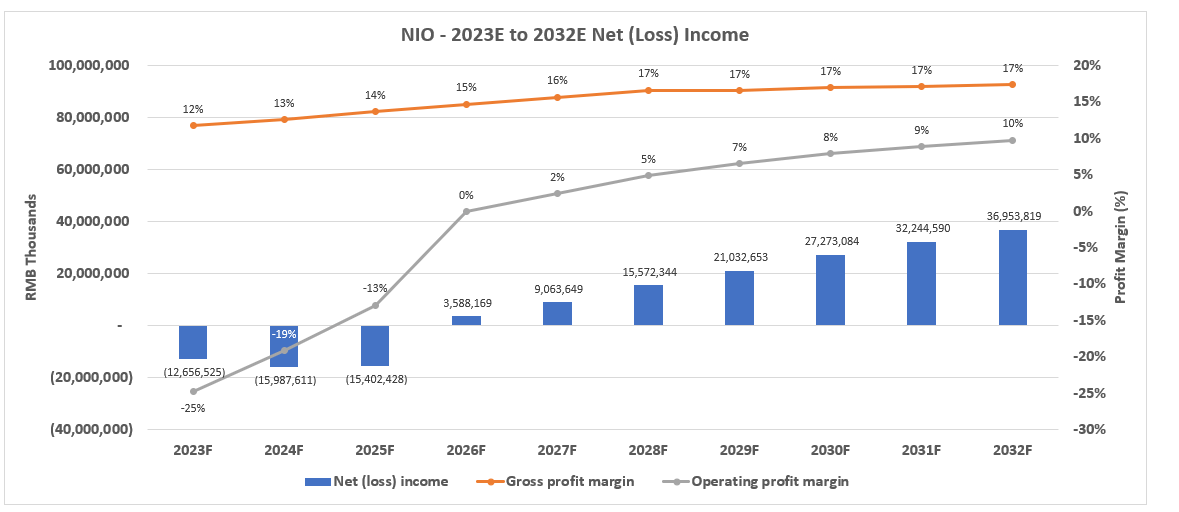

Taken together, we do not expect NIO to achieve GAAP profitability until 2026, with further durability in 2027 when operation margins are expected to turn positive.

{kind=link}

Author

{kind=link}

Author

{kind=link}

Author

NIO_-_Forecasted_Financial_Information.pdf

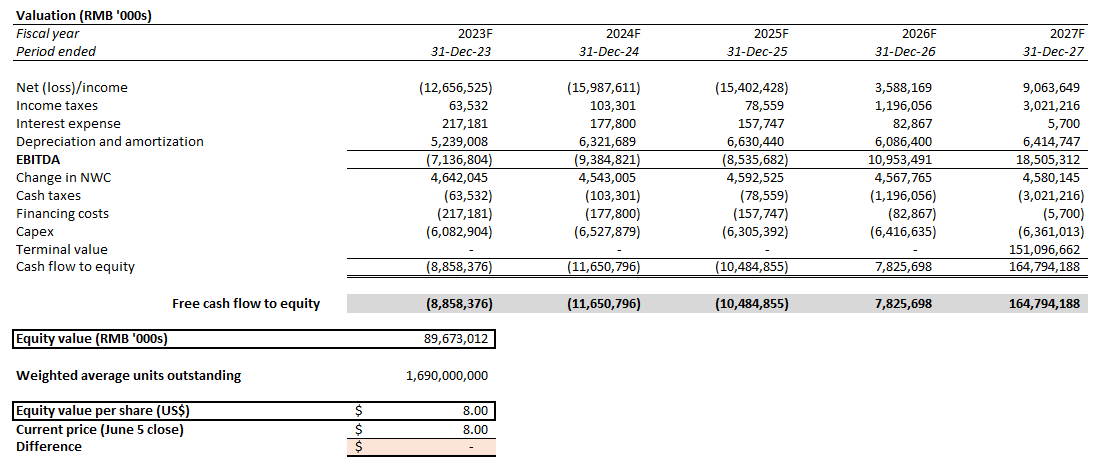

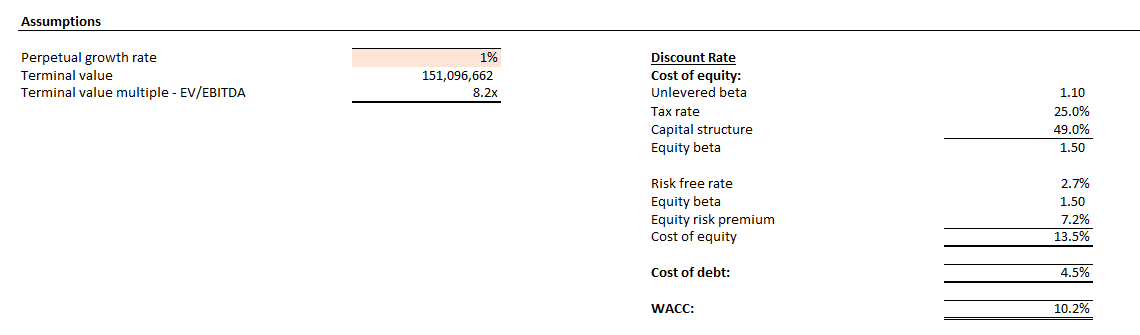

Based on the discounted cash flow analysis on projected cash flows taken in conjunction with our fundamental forecast for NIO, with the application of a 10.2% WACC in line with the company’s capital structure and risk profile, the stock’s current price at about $8 implies a perpetual growth rate of about 1%.

{kind=link}

Author

{kind=link}

Author

Although the key valuation assumptions and implications are similar to those applied in Li Auto’s analysis, alongside a lower WACC for NIO’s projected cash flows given its comparatively debt-heavy capital structure, the latter’s lower valuation is consistent with its pushed-out profit realization timeline, leading to lower cumulative free cash flows to equity. While the implied perpetual growth rate of 1% at NIO’s current market value is not reflective of its growth prospects either, even without incremental considerations of the upcoming launch of mass market sub-brands, the discount likely prices in investors’ cautious optimism considering near-term industry demand risks and other geopolitical considerations, especially given the core brand is not yet profitable. This is also consistent with elevated execution risks ahead as NIO juggles a more ambitious growth roadmap by diversifying into new vehicle and pricing segments across both its core and planned sub-brands.

The Bottom Line

While the near-term growth story of both Li Auto and NIO are showing signs of divergence, both brands’ increasing prominence in China – the world’s largest and fastest growing EV market – continue to exhibit captivating market share gain prospects over the longer-term.

On one hand, Li Auto has demonstrated seamless execution of its conservative go-to-market strategy, which is corroborated by eyepopping delivery growth rates observed in recent months with its introduction of additional models, as well as an increasingly durable trajectory of profit margin expansion. This continues to support the stock’s recent market-defying rally, as investor confidence is reinforced by the underlying business’ fundamental improvements. But downside risks remain at current levels, as much of Li Auto’s delivery growth in recent months is supported by new demand for the recent release of three additional models to the existing Li ONE. And considering China’s mixed economic recovery outlook, those numbers might normalize significantly from the current pace of triple-digit y/y growth by next year once the lapping benefits pass, and potentially slow the stock’s momentum to create a better risk-reward entry set-up.

Meanwhile, on the other hand, NIO’s sluggish quarterly delivery volumes, and comparatively lack of appeal given its unprofitable state has compressed its valuation this year. The stock’s performance at current levels likely reflects the elevated company-specific fundamental and execution risks ahead of its ambitious growth roadmap, in addition to ongoing industry-wide and market headwinds (e.g. geopolitical and regulatory uncertainties, macro-driven demand risks, supply-driven inflationary pressures, etc.). Considering persistent macroeconomic challenges, alongside an uncertain timeline to the realization of its mass market penetration plans, the stock risks trading in a range for the foreseeable future, with incremental susceptibility to volatility in tandem with risk-off sentiment across the broader cohort of U.S.-listed Chinese equities.

Looking ahead, we remain focused on consistent developments pertaining to NIO’s mass market sub-brand offerings, as well as progress in ramping up productions on the NT 2.0 platform at its upcoming earnings release – both would be key indicators to whether the company’s longer-term growth and profitability prospects are sustainable. Meanwhile, despite Li Auto’s impressive feat in achieving GAAP profitability in the capital-intensive and competitive automaking business, we are staying incrementally cautious over the durability of its eyepopping growth over the past several months, which has been a key driver to the stock’s recent rally that is poised to normalize and create a better entry set-up for partaking in the company’s longer-term growth prospects.

For further details see:

The Diverging Growth Story Of NIO And Li Auto