META - The Dollar's Easing Has Been A Boon For These Sectors As Predicted

2023-04-14 00:41:37 ET

Summary

- Looking back six months ago, I suggested the USD may be nearing a top. With the expectation the dollar would decline a bit, I laid out some investment options I found viable.

- In hindsight, the dollar did ease, and those options performed extremely well for the most part.

- With the Fed looking to take a less hawkish approach in the second half of 2023, there is a reasonable chance the gains could continue for those same sectors and funds.

Main Thesis & Background

The purpose of this article is to discuss the U.S. dollar ((USD)), its recent performance, and why I think some of the trends that have emerged while its value has declined could be set to see more gains. This is an important macro-implication, as the dollar saw a strong rise for the most of 2022, only to see some of those gains reverse since early November. In this review, I will discuss why some of the biggest winners from this pattern are set up nicely going forward as well.

For perspective, readers may remember I wrote about this topic almost six months ago. Back in October, I saw the USD's continual rise as a sign that a reversal may be in the cards. I laid out the reasoning, and also some sectors and stocks that were likely to perform well if my prediction proved accurate:

Past Article (Seeking Alpha)

Suffice to say, this was a well-timed review. But rather than pat myself on the back and stay complacent, I wanted to do a reassessment here to see if this trend would continue and - just as importantly - if the winners from this backdrop would continue to be winners. Therefore, I will look at each of the sectors (or stocks) I suggested in October and give my updated opinion on them in this article.

USD's Performance Of Late

To begin, let me first take stock of how the dollar has been performing. It may seem counter-intuitive to discuss the dollar's fall because it has been holding steady (and slightly rising) in the immediate term. But the longer term trend has actually been negative. If we look back to October when I wrote the aforementioned article, we see the spot index was in the mid-1300s. Today, it sits near the 1240 level, suggesting a decline around 7%:

{kind=link}

It is fair to see the USD has been struggling over the past six months, as predicted. While looking back has value, the more important consideration is where does it go from here. I personally see an environment where more weakness is possible, which is why I am contemplating whether the winners in this environment will remain good investments. I think so, and will take each in turn below.

Opportunity #1 - Commodities (Oil and Gold)

The first theme I discussed in October as a potential beneficiary to USD weakness was commodities. This included gold, oil, and to a less extent silver. These commodities, as I see them, often perform well when the dollar is weak because they are priced in dollars (i.e. when the dollar declines, it takes more of them to buy an ounce of silver, barrel of oil, etc.). So there is a natural inverse correlation that often holds up well over time.

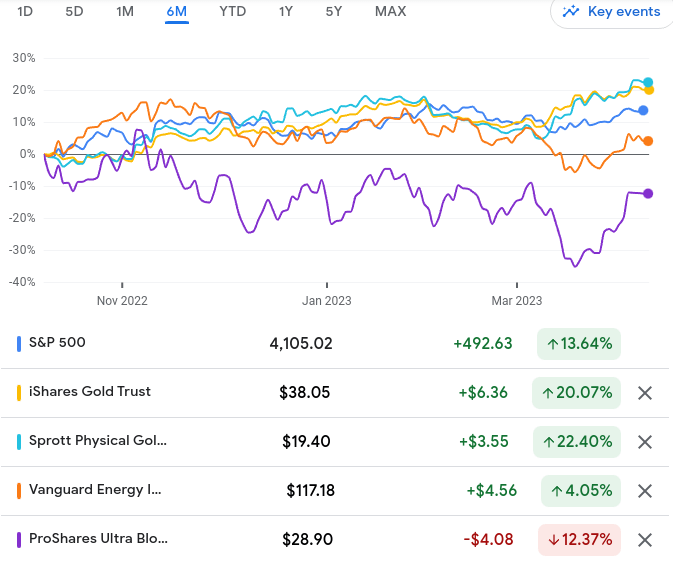

Specifically, I highlighted a number of tickers that I saw value in. For gold and silver, I like the Sprott Physical Gold and Silver Trust ( CEF ), but the iShares Gold Trust ETF ( IAU ) is one of the most popular straight metals plays. Similarly, I mentioned the Vanguard Energy ETF ( VDE ), and the ProShares Ultra Bloomberg Crude Oil ( UCO ) for Energy/oil exposure, albeit there are also a plethora of similar funds to consider for this space.

6-Month Performance (Select Tickers) (Google Finance)

{kind=link}

This was the most interesting performance gap that I saw during my research for this review. It turned out that Energy posted only modest gains, with oil falling a bit over the same time period (UCO is a leveraged play on oil futures, so its losses are twice what the spot price is). By contrast, gold and silver saw strong gains, with both IAU and CEF surging well past what equity investors would have gotten in the S&P 500. That is truly stunning performance.

This really underscores a few key points. One, gold and silver's relationship with the dollar was put to the test and passed in this environment. Two, oil, especially oil futures, remains an extremely volatile asset. While I think this sector idea makes sense during times of dollar weakness, the ensuing volatility means it is not for everyone. Further, leveraged plays like UCO are especially risky and I emphasize that is a type of investment that retail investors should approach with caution and/or enter for shorter than usual time periods. Understanding that dynamic before buying is critical.

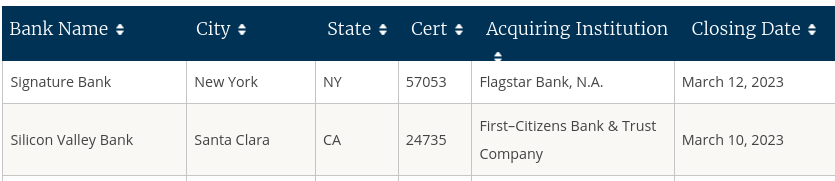

The broader takeaway as a result is that "commodities" are not all equal. Metals like gold and silver have some utility, but are also seen as safe havens during times of economic distress. That explains their strong performance of late as the world continues to grapple with instability and the U.S. and Europe has seen a couple of bank failures in the past few weeks. If investors or households think their "cash" is not safe, then metals see renewed interest as a store of value:

Recent Bank Failures In US (FDIC)

{kind=link}

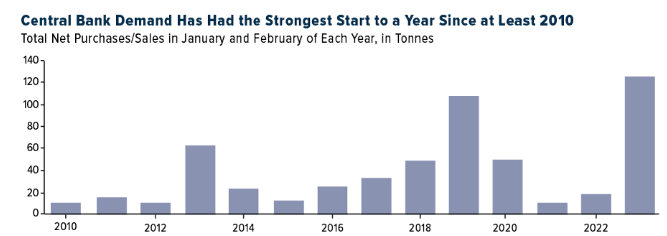

And it isn't just my opinion in this matter that counts. Central banks around the world have taken note and have started buying up gold in particular. After years of suppressed buying, central banks have been rapidly buying up the precious metal so far this year:

Central Bank Gold Demand (Aggregate) (IMF)

{kind=link}

I don't see any compelling reason why this trend will reverse in the immediate term, so it represents an important catalyst for gold going forward.

Oil, and the Energy sector by extension, has a more complicated relationship. While oil and gas are considered commodities and can rise when the USD weakens, there are other factors at play that influence their spot prices. Unlike gold and silver that can benefit from economic weakness, the broader demand for oil can drop when investors are anticipating a recession (or depression). By this token, the recent string of bank failures and continued potential for escalation in the war in eastern Europe means that oil demand may falter. This is why oil futures have not been rallying as hard as gold and silver in the past few quarters.

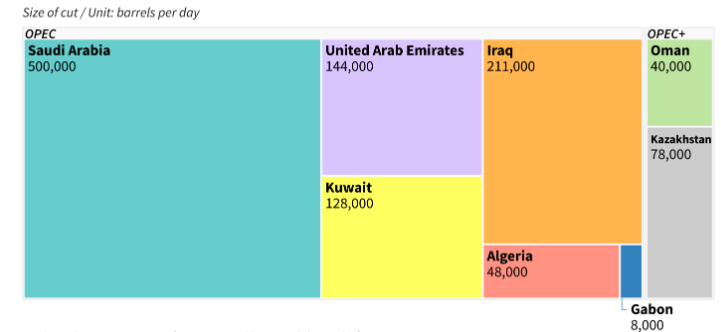

In my personal opinion, I think that weakness is short-sighted. China has proven to be a big buyer of oil in recent months and its push to re-open the economy there provides a nice hedge against an economic slowdown in the U.S. and western Europe. Furthermore, a surprise oil production cut announcement by OPEC+ will limit supply in the months ahead. That is also bullish for prices:

OPEC+ Production Cuts (Announced) (Reuters)

{kind=link}

This is critical to my bull case for oil in the months ahead. OPEC+'s move here is naturally positive for prices in that it should remain supply from the market. It also shows the cartel has a willingness to respond and adapt to changing market conditions and is going to put a floor on prices going forward. To me, this move has longer term implications and supports my decision to own this sector as a permanent allocation in my portfolio.

*I currently own VDE and CEF.

Opportunity #2 - Foreign Exposure

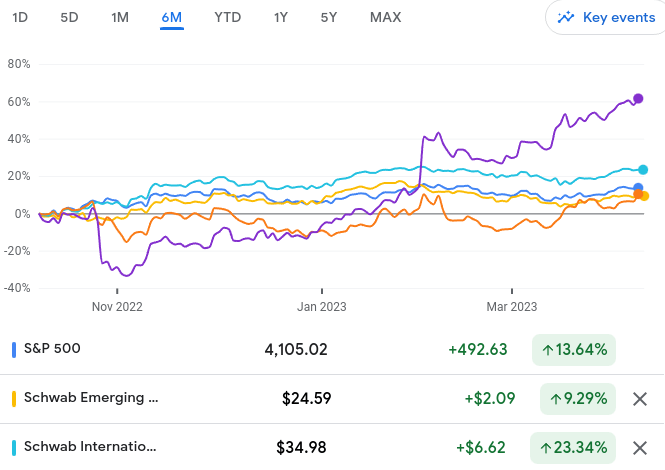

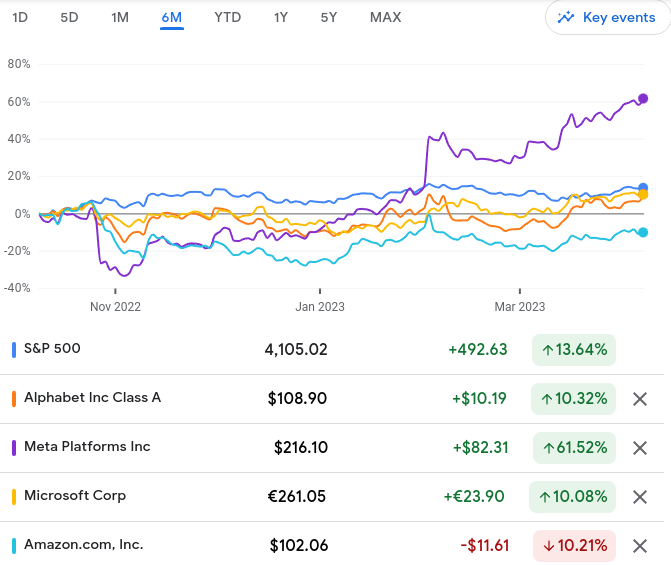

The next topic I had emphasized was for U.S.-based investors to own some foreign exposure. This included both foreign based ETFs and also U.S. companies with significant revenues and profit generation overseas. I highlighted two popular non-U.S. ETFs, and also some of the biggest domestic Tech names that do a lot of business outside our borders. These investments were the Schwab Emerging Markets ETF ( SCHE ) and the Schwab International Equity ETF ( SCHF ), and Meta Platforms ( META ), Alphabet ( GOOG ), Amazon ( AMZN ), and Microsoft Corporation ( MSFT ). Looking at performance, all of these names registered gains, with the exception of AMZN:

6-Month Performance (Google Finance) 6-Month Performance (Google Finance)

{kind=link}

{kind=link}

As you can see, with the exception of AMZN, owning foreign exposure (either directly or indirectly) was a profitable move. Importantly, I think this is going to remain the case for most of 2023.

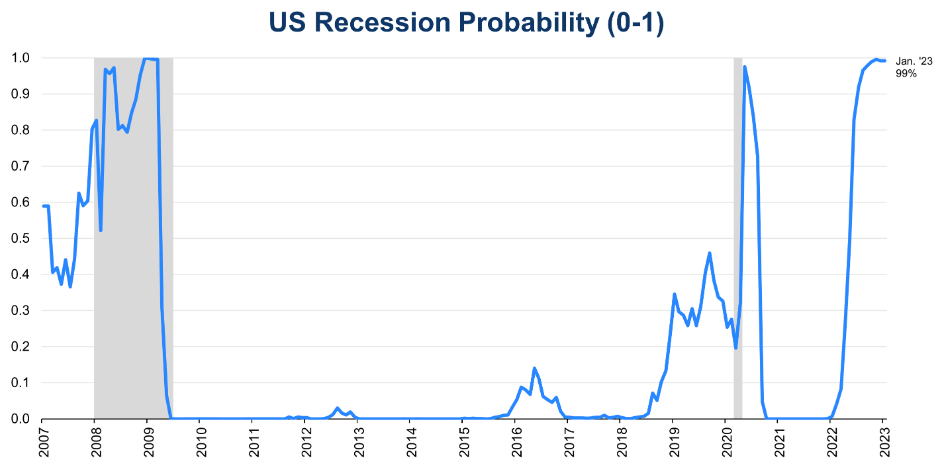

The rationale is multi-fold. Primarily this is due to the increased potential for economic weakness domestically in the second half of the year, and potentially 2024 as well. While the U.S. has so far showed strong resiliency, the cracks are beginning to show. In fact, the Conference Board now puts the potential for a recession within the next twelve months to be 99%:

Recession Probability (The Conference Board)

{kind=link}

This certainly means the broader outlook for U.S. companies will be challenged to say the least. By contrast, global profit margins are also expected to slow down, but will remain elevated on a historical basis:

Global Profit Margins (BlackRock)

What this tells me is that if we see an earnings slowdown here at home, foreign investments might help make up for that. At the very least it supports the idea that having some non-US exposure remains a relevant hedge. That is primarily why I own some non-US stocks and also companies that have substantial earnings power outside their domestic borders. With headwinds on the horizon here at home, that is an investment strategy I will continue following for the foreseeable future.

*I own foreign exposure through the iShares MSCI United Kingdom ETF ( EWU ), the iShares MSCI Canada ETF ( EWC ), and the iShares MSCI Ireland ETF ( EIRL ). I own those big Tech names primarily through Invesco QQQ ( QQQ ) and also the Vanguard S&P 500 ETF ( VOO ), among other ETFs in my portfolio. (For my full holdings list, see my Seeking Alpha profile page).

Opportunity #3 - Bonds Pushed Higher

The other natural spot I saw value in if the USD was going to decline was bonds. This was based on the notion that if the future Fed funds rate was going to drop, so too would the USD and the desirability of bonds and their corresponding income stream. Last year was generally a negative year for bonds as a whole, but Q1 this year turned the page.

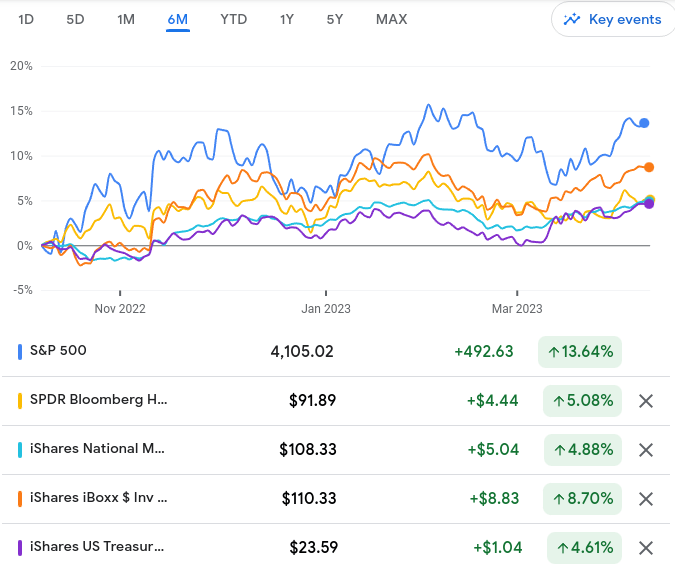

Back in October, I suggested both corporate debt and municipal bonds, and those have performed well. So too have treasuries, which I included in the graphic below, although I did not recommend them nor do I now - simply because I see more value in the other sectors I mentioned on a relative basis:

6-Month Performance (Google Finance)

{kind=link}

While these returns lag the S&P 500, that is natural. But the good news is these fixed-income sectors have seen less volatility and their total returns have been higher than what it illustrated above because those figures exclude distributions. The bottom-line is there have been healthy returns over the past few months in what was a beaten down corner of the market.

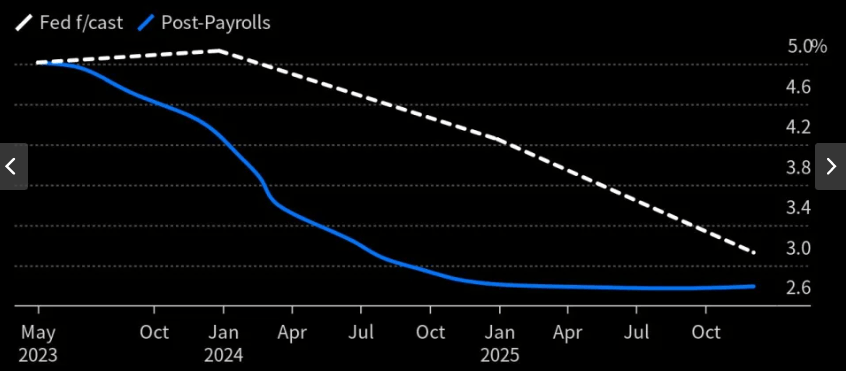

Looking ahead, I believe the current yields offered in the bond markets - both corporate and municipal - remain attractive. Rates have pushed higher in 2023 so far but sectors outside of treasuries still have a potential yield gap. Importantly, investors are beginning to price in the end of the Fed rate hiking cycle. If yields begin to subside in the months ahead, that limits the opportunity for investors going forward. This means taking advantage of this opportunity now is probably the smart play:

Fed's Rate Forecast (Market Anticipates) (Yahoo Finance)

{kind=link}

My point here is that retail investors will want to get in before the Fed is done hiking and yields start to decline. Locking in higher yields now is the prudent way to do this, even if the Fed is not quite done and there is some pressure in the immediate term. Over the longer term, as rates drift lower, this will likely have worked out to be a profitable move.

Bottom-line

Six months ago I laid out a case for why the USD was going to ease and what could benefit if it did. This was an accurate prediction with many of the suggested options beating the broader market. As we have pushed into Q2, I think many of those same arguments remain in place and would continue to be long the sectors, funds, and stocks I highlighted in this updated review.

That said, remember to carefully weigh the risks to this approach. Locking in gains is never a bad idea, so if one disagrees with my central thesis, taking some profit here could be timely. The reason being the market has continuously underestimated the Fed's resolve and that could be the case in the months ahead as well. If the Fed does reiterate a more hawkish stance in the second half the year, the dollar might rally, putting these recent gains in jeopardy.

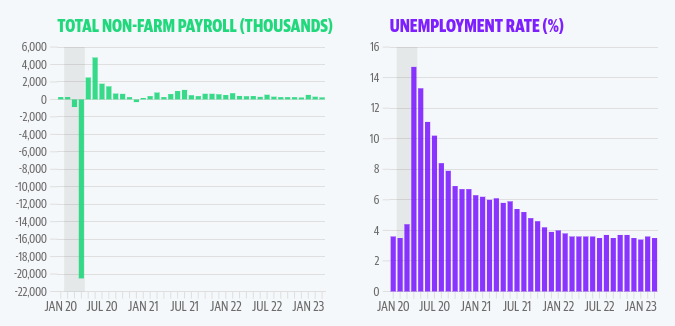

There is some merit to the opposite argument I am laying out here. The broader U.S. economy has been very resilient - with unemployment and inflation remaining low and high, respectively. As long as the jobs market stays hot, that is going to bolster the Fed's case to keep rates higher for longer:

Employment Figures (US) (Bureau of Labor Statistics )

{kind=link}

The conclusion I draw here is that there may be some more room for the Fed to move. If so, the USD could get a bump and that negates some of the points I made here.

But I stand by these calls regardless. If we do see a rally in the USD I expect it to be short-lived. The U.S. is not used to 5% interest rates and I can't see this level as a sustainable one for the long term. That means a weaker USD over time and that bodes well for many of the investments I discussed here.

For further details see:

The Dollar's Easing Has Been A Boon For These Sectors As Predicted