ACTV - The February Payrolls Preview: Luck Be A Lady

2023-03-08 12:57:03 ET

Summary

- The payrolls report for February is likely to be strong, possibly exceeding expectations.

- The Fed might be forced to accelerate the pace of interest rate hikes to 50bpt in March.

- Thus, the probability of a sharp selloff in S&P 500 is very high.

Luck be a Lady is one of the greatest Frank Sinatra songs, famously performed at the Sands Hotel & Casino in Las Vegas in 1963. It's still sort of an unofficial Vegas anthem.

The title is of this article is appropriate as a preview for the February payrolls report, to be released on Friday, for two reasons.

The January surprise

First, the January payrolls report surprised everybody. Almost all analysts were expecting the continuation of the labor weakness from the end of 2022 into the 2023. Big surprise, the new non-farm jobs created jumped to 517K, more than double the estimates, and the unemployment rate dipped to 3.4%.

Was this a one-off event, due to some seasonal adjustment, or was this really a reflection of the strengthening labor market? Nobody was really able to explain the sudden January bump in new jobs created. Thus, the prediction for the February payrolls is very uncertain, like the craps shoot - luck be a lady.

The full post-COVID reopening thesis

Second, I actually found myself in Las Vegas on the New Year's Eve, on my way to Los Angeles. The local news reported that 400,000 people were expected to attend the "America's Party 2023" on Dec. 31, which was the first unrestricted New Year's Eve party since COVID. I think at the end it was probably more than 400,000.

I didn't think about this until the January Payrolls report - this was the first post-COVID Vegas New Year's Eve party! Maybe this finally reflects the full post-COVID US reopening. And thus, if the same holds nationally, it's showing up in the economic data, and explains the sudden bump in the payrolls. I know I was not always comfortable in indoor crowded spaces last year, but I didn't even think about it this year.

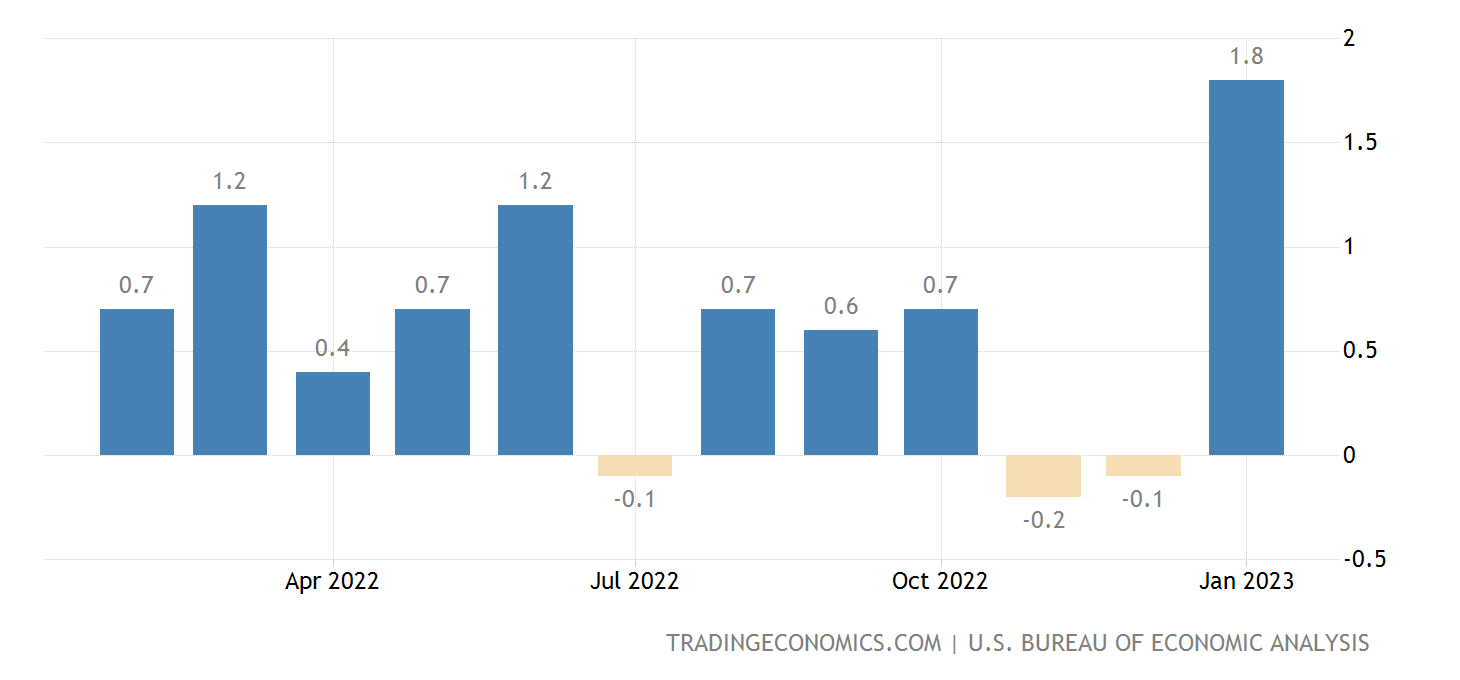

This is the personal spending data, and it's showing the big bump in January, after what looked like a pre-recessionary decrease in November and December of 2022. Thus, it's difficult to dismiss the January payroll data as a "seasonal adjustment." There's definitely something else going on, and it could be the full all-inclusive post-COVID reopening.

{kind=link}

Expectations for the February

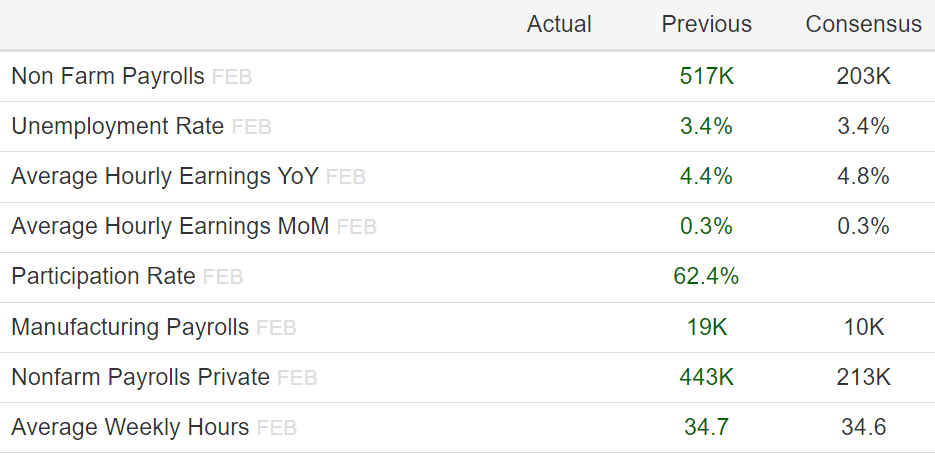

Here are the expectations for the February jobs data:

{kind=link}

These are important points:

- The total of non-farm payrolls is expected to fall to 203K, with the implication that the January's surprise bump to 517K was some kind of one-off event.

- However, the unemployment rate is expected to stay steady at 3.4%, reflecting still a very tight labor market.

- Most importantly, the average hourly earnings are expected to accelerate to 4.8% from 4.4% YoY, with a steady 0.3% MoM change. This is likely the most important number for the monetary policy expectations, since the Fed specifically views the wage growth as the key input into the sticky service inflation.

- Similarly, the average weekly hours are expected to decrease to 34.6 from 34.7. This also is very important, since the average weekly hours work is a leading indicator of the labor market strength.

Overall, the market expects a very strong February labor market report, with the accelerating wage growth, and the leading indicators pointing to the continuous strength into the March payrolls.

What's likely to be the "actual" number?

So, let's speculate now. I was following the leading indicators from the end of 2002 and expected that the January report would be weak and signal an imminent recession. Specifically, the leading indicators were pointing to a weak labor report: The number of hours worked has been decreasing, and the number of temporary workers has been decreasing. This also was consistent with the personal spending data (see above). Well, that was wrong, both of these leading indicators reversed in January.

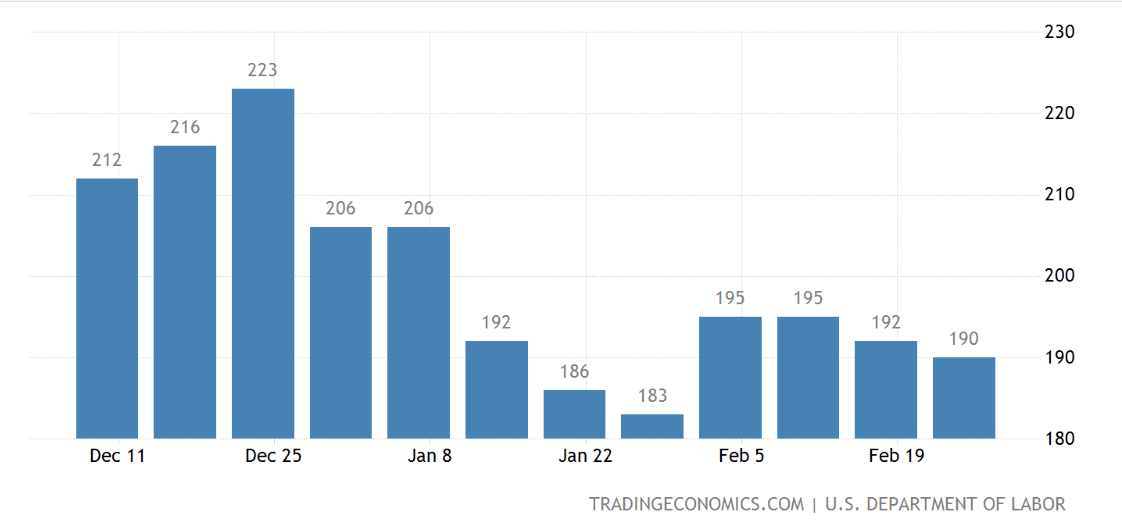

The high-frequency weekly labor market data suggest that the February labor market report will be strong. The weekly clams for the unemployment insurance has been near historic lows in January and February - below the 200K level.

{kind=link}

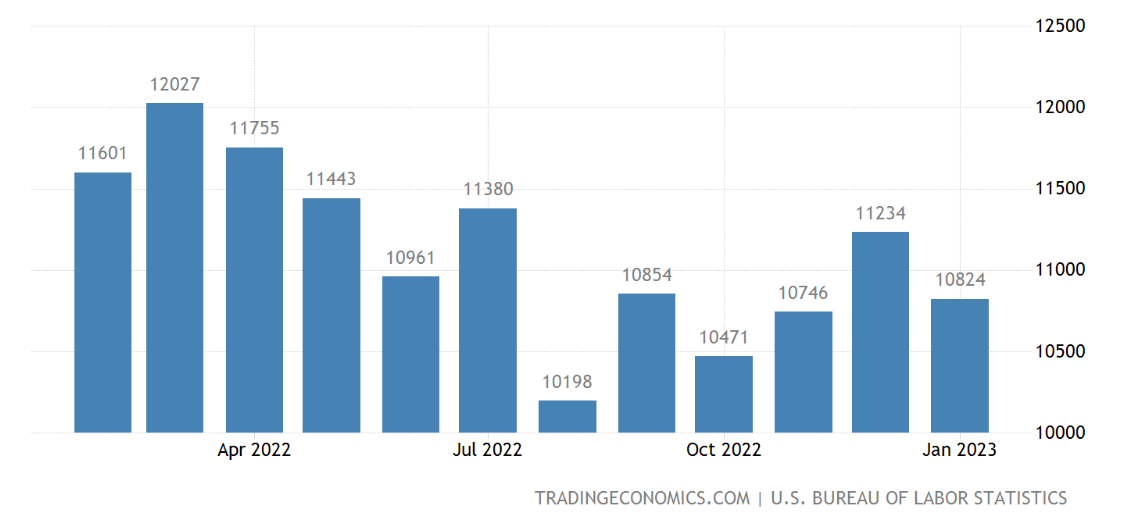

Meanwhile, the JOLTS report is showing that US job openings are still holding near the very high level, suggesting that US companies are still struggling to fill open positions. This confirms still an extremely tight labor market.

{kind=link}

Based on these indicators, the February payrolls report will be as strong as expected, with the risk that the headline non-farm number exceeds the expectations of 203K.

The big picture

The Fed has been clear that the labor market has to weaken "somewhat" to ease the inflationary pressures on the sticky services inflation. In December's Summary of Economic Projections , the Fed projected the increase in the unemployment rate form 3.7% to 4.6% in 2023. Well, the data is going the wrong way, the unemployment rate went down to 3.4%.

The aggressive monetary policy tightening in 2022 (as illustrated in the chart below) works with lags, but it has not affected the labor market yet. The Fed decreased the pace of the interest rate hikes to 0.25% to evaluate the lagged effects of prior aggressive tightening on current data. But the labor market strength accelerated in 2023 and inflation seems to be turning around as well. Thus, the Fed might be forced to be more aggressive in 2023, which is what the Fed Chair Powell indicated in his testimony on May 7.

Trading Economics

If in fact the US is finally going through the full post-COVID reopening, the New Year's holiday strength is likely to extend to the summer travel season. People have jobs, with rising wages, still some savings, and ready to leverage the consumption with the credit. As long as these hold, people don't really mind paying more for the hotel rooms, airline tickets, restaurants, etc, which really complicates the Fed's inflation fight.

Implications for the stock market

The labor market is likely to remain strong in February, even going forward to March. The Fed might have to become more aggressive, and induce the "shock" to the system by increasing the pace of interest rate hikes in March to 50bpt, which is what the Federal Funds futures market is already pricing.

Thus, the probability of a very sharp selloff in S&P 500 ( SPX ) in March is very high to a level possibly exceeding the October lows toward the 3000 level.

However, the lagged effect of the previous hikes could start showing up in the data at any time, which would reignite the "Fed's pivot" hopes and squeeze the shorts. That's the short-term risk of the directional short position. As the recession becomes obvious, and companies start significantly reducing the profit guidance, the upside volatility is likely to subside.

For further details see:

The February Payrolls Preview: Luck Be A Lady