SHOP - The Hunt For Potential 10x Returns: Shopify's Push Into AI With Lower Overhead Will Drive Growth

2023-08-24 09:44:10 ET

Summary

- I examine whether Shopify has the potential to appreciate ten times over with its current valuation as part of 'The Hunt For Potential 10x Returns' series.

- As previously done, I use a rating system based on factors such as returns on invested capital, insider ownership, share repurchases, gross profit margin, and intangibles to evaluate Block.

- SHOP stock has scored the highest rating yet due to its great returns on invested capital and intangible value through AI product initiatives and employee cuts that decrease overhead.

- Pursuing market share gains through product development in AI while focusing on the bottom line may ultimately pave the way for Shopify to quickly expand its valuation multiple going forward.

Introduction

Shopify (SHOP) is a notable contender for the 10-bagger series. The company's valuation has grown a whopping 18x since its U.S. "IPO" in 2015. The company's stock price appreciation is a reflection of the quick pace with which Shopify has taken e-commerce share, especially in the U.S. As of June 2022, 28.51% of the registered websites in the U.S. were powered by Shopify ( Kinsta ). Today, the company powers around 4.3 million active websites globally ( Yaguara ). Shopify is now at the forefront of making commerce even more seamless through its generative AI offerings. In this article, I'll run Shopify through the 10-bagger rating scale and discuss whether the company's AI push, coupled with layoffs will continue fueling strong results.

Check out how Shopify fairs against these companies that I've run through the 10-bagger rating list:

The 10-Bagger Rating List

Check out the start of this series in " The Hunt For Potential 10x Returns: 2 Software Giants " where I have calculated the required annualized return to gain 10x returns over different time horizons. The power and influence 10x returns can have on your portfolio is immense, and I believe there are certain factors that correlate with this outcome. In short, this is what the series is all about:

In this series, I will be rating one/two companies based on pre-determined criteria which have been found to increase the chance of a stock becoming a 10-bagger. My goal in this series is hence to give investors a quick checklist of 10-bagger factors for a multitude of different companies to compare with over time. Furthermore, I will be cumulatively adding to a scatterplot each company's 10-bagger rating and Seeking Alpha Quant rating which we can track over time.

With inspiration from Christopher Mayer and Peter Lynch, as well as my own experience with investing, I have created the following rating list, which ranges from 1-10, with what I believe are the most important factors that contribute to a potential 10-bagger status.

Rating List

- Profitability ("ROIC"), ("ROE") or ("ROCE")

- Insider Ownership

- Share Repurchases

- Gross Profit Margin

- Intangibles.

Profitability: Ex. Returns on Invested Capital ("ROIC"), Return on Equity ("ROE"), Return on Capital Employed ("ROCE").

| Rating |

| Level |

| 1-2 |

| 0-5% |

| 3-4 |

| 5-10% |

| 5-6 |

| 10-25% |

| 7-8 |

| 25-50% |

| 9-10 |

| 50%+ |

Share Repurchase (yearly % purchase of outstanding shares)

| Rating |

| Level |

| 1-2 |

| Compressing |

| 3-6 |

| Steady |

| 7-10 |

| Expanding |

Intangibles

| Rating |

| Intangible Asset |

| Returns on Invested Capital ("ROIC") |

| 22.44% |

| 10 |

| Insider Ownership |

| 6.33% |

| 7 |

| Share Repurchases |

| 2.72% |

| 7 |

| Gross Profit Margin |

| Stable |

| 6 |

| Intangibles |

| Exceptional |

| 9.33 |

Total Points: 39.33/50

Returns on Invested Capital ("ROIC")

Shopify has a relatively clean and understandable balance sheet. Firstly, the company has $1.6 billion in deployable cash and $3.1 billion in liquid marketable securities both of which sum to a total of $4.78 billion of liquid assets. Along with these marketable securities, Shopify has investments in private and publicly traded companies to the amount of ~$2.3 billion, of which the largest holdings are in Affirm (AFRM) and Global-e (GLBE) ( 2022 Annual Report ). I have included this sum in invested capital because although the investment is not directly related to the company's operations, they have been used to build stronger relationships with the companies Shopify has invested in. This, in turn, may give Shopify better cost terms for the investee's products and should be considered capital used for business operations. Apart from these items, Shopify has $719 million in loan receivables from merchants using the platform as well as $914 million in convertible debt. These are the largest items on Shopify's balance sheet and, in total, I find that the company has an invested capital amount of $3.6 billion ( Q2, 10Q ).

The Author

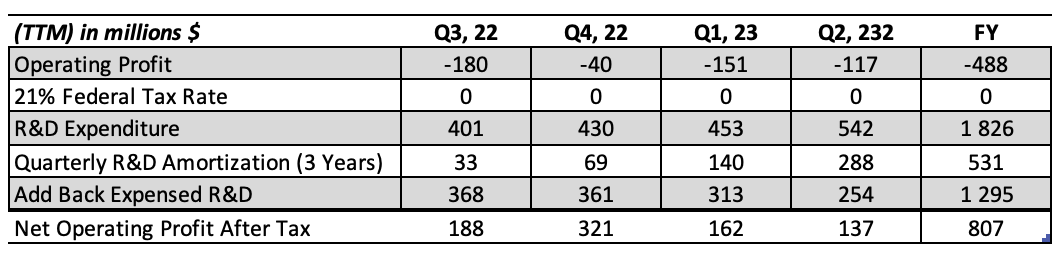

For the sake of this calculation, and in line with my previous articles, I will use twelve trailing months figures and I will adjust "NOPAT" by capitalizing R&D costs for an assumed 3 years. As you will see below, Shopify spends heavily on R&D initiatives. In fact, in the most recent quarter, the company spent around 32% of sales on R&D ( Seeking Alpha Financials ). So, while Shopify remains unprofitable on an operating profit basis, the story is quite different when capitalizing on R&D expenditures. During the "TTM", I found that Shopify generated an adjusted "NOPAT" of $807 million.

While R&D expenditure is constantly on the rise, "SG&A" has stayed relatively flat. If we break it down more specifically, Sales & Marketing expenditures decreased by 3.5% "YoY" while General & Administrative expenses increased slightly - by 6.28%. Overall, Shopify's 20% headcount purge seems to be reflected in the financial figures and it will continue doing so even more going forward as compensation is completely paid out ( Tech Crunch ).

{kind=link}

When dividing adjusted "NOPAT" by invested capital, I find that Shopify has an impressive return on invested capital of 22,44%. This level of underlying profitability warrants a 10/10 rating on the 10-bagger scale for profitability. Shopify is able to reinvest its cash at high levels as it builds better solutions and attracts more merchants onto its platform. One recent development that will likely drive even more user adoption is Shopify Magic - a free AI tool that integrates with website building and merchandising among other integrations - as it makes it even easier to adopt the platform.

The Author

Insider Ownership

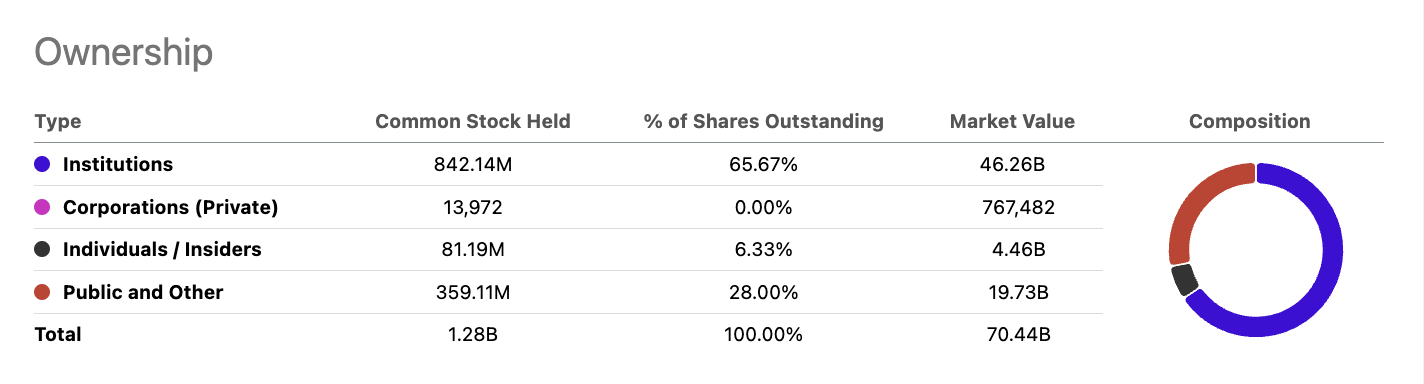

Tobi Lütke, the founder and CEO, has significant ownership in Shopify and holds a large amount of voting rights through Class B shares. In total, as of the year-end 2022, all outstanding Class B shares retained a 39% voting power. Therefore, although Tobi only has a 6,33% share in the company, he has significant influence over the company through voting rights.

Apart from the CEO and Harley Finkelstein, the COO, Shopify has a myriad of experienced leaders who have recently (2019, 2020, 2022, etc.) joined the company ( Shopify Leadership Team ). The compensation that these executives receive is a mix between a fixed wage and option awards. Interestingly, Tobi Lütke only earns 1 in fixed salary, while the other executives earn around 900,000. With regard to equity compensation programs in 2022, however, Lütke earned awards of $20 million. The other executives earned between $6-$16 million, depending on the position they were in. Equity compensation is well above fixed salary, which is in line with most U.S. corporation's wage standards.

The high amount of insider ownership, coupled with good compensation packages for management are strong attributes for Shopify. Another important attribute that Shopify has is Harley Finkelstein, who has been with the company since 2010. Finkelstein is an outward figure for Shopify and despite not being a founder, he has a founder-led excitement when talking about new product launches. This makes sense as he has most likely shaped the company significantly within the past 13 years. Due to these reasons, I believe Shopify is warranted a 7/10 on the insider ownership scale.

{kind=link}

Share Repurchases

As we saw earlier, Shopify does not have a large debt position ($900 million) and the debt that it has is convertible into shares. When coupling convertible debt financing with stock-based compensation policies, I find that Shopify slightly dilutes shareholders over time. Since 2021, shareholders have been diluted in total by around 3,9% or 1,95% on an annual basis. This level of dilution is far less than I had expected.

For comparison, Block Inc ( SQ ) has diluted shareholders by 31,3% over the same period. Shopify has been very disciplined with its acquisition strategy, in which the company has made relatively smaller purchases while focusing more on developing capabilities from within ( Tracxn ). Shopify's largest (disclosed) acquisition was Deliverr in 2022, a part of the company that it has recently sold in a reprioritization effort. The quick pivot is a reflection of Shopify's disciplined approach to its core mission and core products. In return for selling Deliverr to Flexport, Shopify received a 13% stake in Flexport ( Shopify Press Release ). This gives Shopify some influence over fulfillment, without managing it day-to-day. Finkelstein explained some of the reasoning behind selling to Flexport well:

"We also realized that in order to adapt and stay at the forefront of commerce, Shopify must operate with even greater speed and efficiency. So we are making changes and refocusing the priorities that we believe will get Shopify to the size and the shape necessary to unlock the next era of growth and innovation, but that does not make this earnings call any easier."

( Earnings call Q1 )

Block, on the other hand, recently acquired Afterpay for a final sum of around $13 billion - which it purchased with its own stock ( Block 2022 10K ). This acquisition extremely increased the amount of share dilution incurred by the company, which it has not yet reduced with share repurchases. Due to Shopify's low level of share dilution and extreme discipline, I rate the company with a 4/10 on the share repurchase scale.

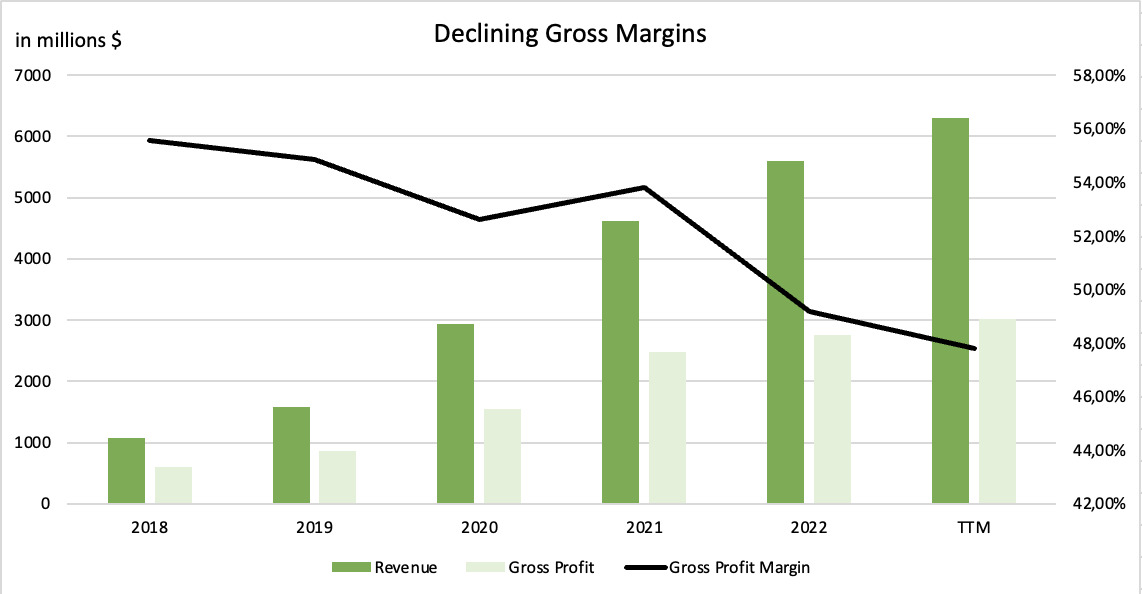

Gross Profit Margins

On a consolidated basis, Shopify has been experiencing declining gross margins over the past five years - moving from 56% to ~47% during the "TTM". Shopify has two main revenue drivers: a Subscription Services business with very high gross margins and a Merchant Solutions business with lower gross margins due to its Shopify Payments business integrated with the latter revenue stream.

Shopify's CFO stated in the Q1 earnings call that:

"[O]ur gross margin this quarter was primarily affected by the dilutive impact of Deliverr. Additionally, Q1 gross margin was also impacted by Merchant Solutions being a larger percentage of our business, driven by growth in Shopify Payments. And within our Shopify Payments business, we continued to see gross margin pressure due to the greater mix of Plus and higher mix of credit cards versus debit cards compared to Q1 last year."

{kind=link}

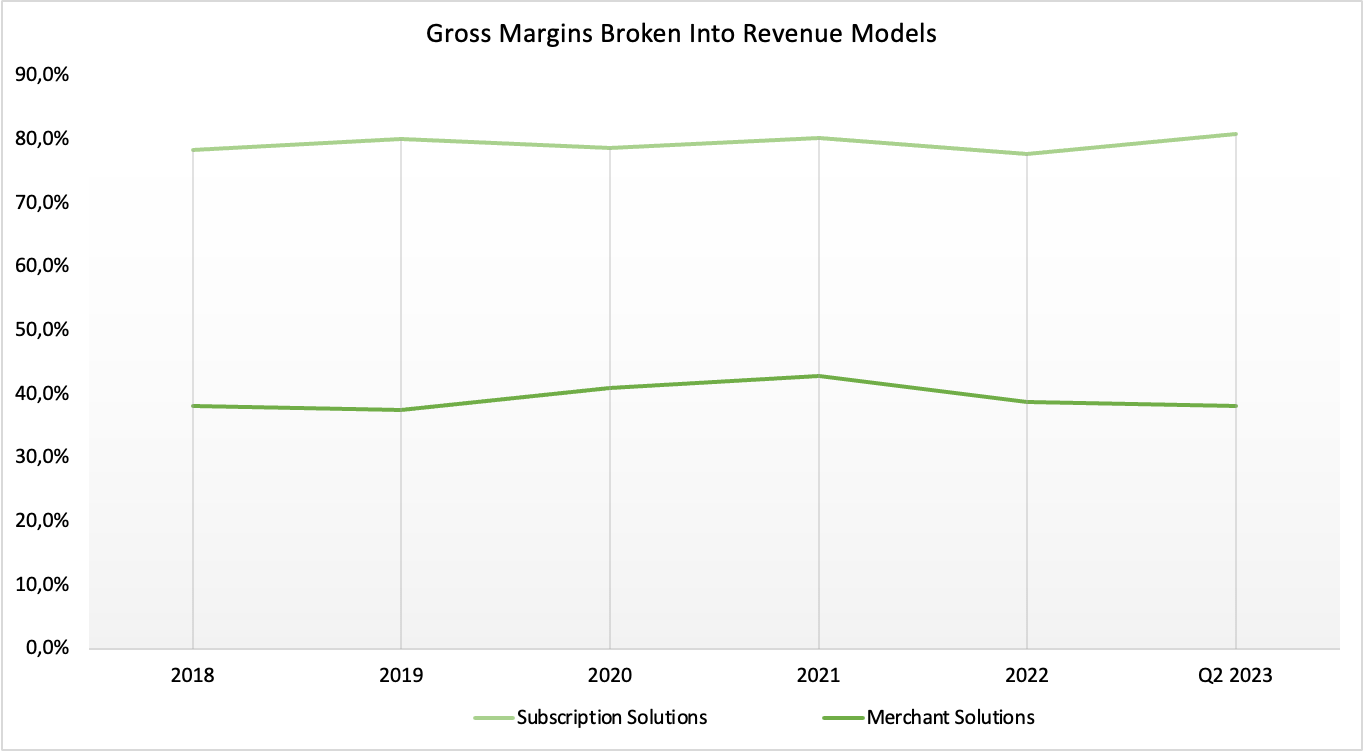

Essentially, the fast growth in merchant solutions is causing downward pressure on Shopify's overall gross profit margin. But, when looking at the margin broken into the two revenue streams the results are quite different. Over the past five years, Merchant Solutions' gross margins have been stable while Subscription Solutions' margins have grown by over 2%. Shopify could experience slight growth in merchant solution margins as Shopify Pay matures, which is an interesting growth driver to look for in the long term.

{kind=link}

In all, Shopify's gross margins are high and stable. In the latest quarter, subscription margins amounted to 80,9% - its highest in five years - and merchant solution margins amounted to 38,1%. Given the fact that Shopify is still growing newer parts of its business such as Shop Pay and the Shop app, it is impressive that the company has been able to retain its merchant solution margins. Also impressive is the company's growth in software margins to over 80%. For these reasons, I rate the company a 6/10 with regard to gross margins.

Intangibles

| Intangible Asset |

| Rating |

| Company Culture |

| 9 |

| Industry Growth Rate |

| 10 |

| Operating Leverage |

| 9 |

Average Points: 9.33

1. Company Culture

Shopify's company culture is far from normal. Recently, the company has been in the news for conducting quiet layoffs - even after its publicly announced 20% headcount reduction ( LinkedIn ). The layoffs have been complemented with radical changes in internal operations within the company as well. Shopify has recently implemented a tool that calculates the opportunity cost lost for taking meetings ( CBS News ). Meeting opportunity costs depend upon the amount of time for the meeting, the number of attendees, and the professional level of the employees in the meeting. To me, it seems like Shopify is onto something with regard to the new meeting policies. Harvard Business Review was cited in another CBS article for estimating that companies spend a total of $37 billion on meetings. Most of this cost comprises wages paid to employees in unnecessary meetings. This implementation may drive more efficiency within the firm by creating a more rigid and competitive work environment. The downside, however, is that employees may feel concerned about job security. Massive layoffs followed by quiet layoffs as well as stricter standards may put incredible pressure on Shopify's employees.

Ironically, Shopify is simultaneously developing a whole suite of new AI products. Shopify Sidekick may become a new blockbuster product for merchants around the world. Sidekick is an "AI-enabled commerce assistant that allows merchants to use AI to increase productivity, improve workflows, make smarter decisions, and spend less time on operational tasks" ( Q2 Press Release ). Hence management is not only implementing cost efficiencies for itself, internally, but also for customers through "AI" offerings. It seems as if Shopify has pivoted its attitude completely - shaking all parts of its organization and product suite up. Shopify is now slimmer without its fulfillment business, it is more overhead-light as a result of layoffs, and it is fully and very quickly embracing a new era of AI-powered products. In all, I believe this adaptation may be "cold" but it is completely necessary to remain a market leader. Although it may be difficult for Shopify's ex-employees, these recent moves should be embraced by shareholders as an attempt to withhold more gross profit with less overhead in order to continue gaining market share. Based on these observations, I rate Shopify's company culture with a 9/10 .

2. Industry Growth Rate

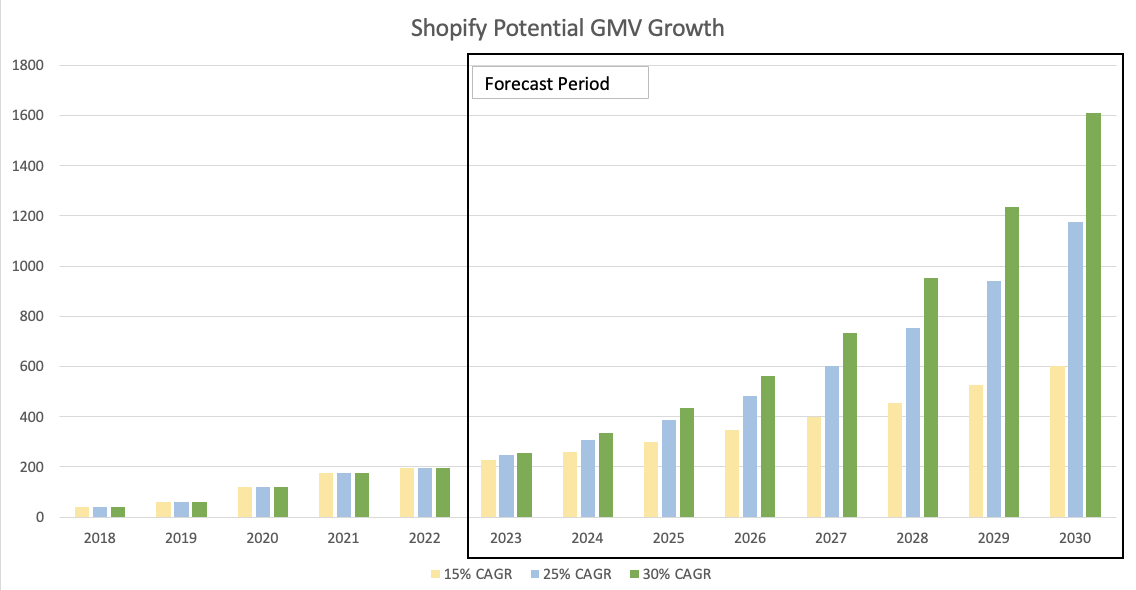

Similarly to Block Inc. - which I analyzed earlier in the 10-bagger series - Shopify technically operates in several varying industries. The company has a Shop app for merchants to sell items on, offers a platform for website creation and management, sells POS systems, and has its own payment service. All of these factors make it difficult to appreciate the industry growth rate for Shopify. However, one metric that the company is very oriented toward is Gross Merchandise Volume "GMV" which is the amount of sales made through its platform. GMV growth and the company's ability to earn revenue for every dollar of GMV - known as the "attach rate" - are largely correlated to the financial success of the company. During the past five years, Shopify's GMV has grown by a whopping 175% "CAGR". The growth in GMV was especially boosted by the e-commerce boom that occurred during and after the pandemic.

During the "FY" 2022, however, the company's "GMV" growth slowed to 12,4%. This is natural given the explosive growth in 2020 and 2021. The growth figures have seen a recovery in the latest quarter in which GMV grew by 17% "YoY". Since it is unlikely for Shopify to continue growing at its historical pace, I have laid out three realistic "CAGR" scenarios which range from 15-30%. This means that Shopify could achieve a GMV of between $603 and $1608 billion in 2030.

{kind=link}

On top of Shopify's quick GMV growth, attach rates have increased to the highest levels ever of 3,08% in the most recent quarter ( Shopify Investor Relations ). Given that Shopify retains this attach rate, then the company will earn revenue from merchant solutions in the range of $18,57 and $49,3 billion in 2030. The latter outcome would be considered incredible, while even the low-end of the outcome would represent merchant revenue growth of 4,5x from 2022 levels.

Currently, Shopify has a "P/S" ratio of around 10. Furthermore, Subscription Services account for 35,5% of merchant solution revenues. Given that this ratio remains constant, Shopify could be earning revenue of $18,57 + $6,59 = $25,16 billion at the low end in 2030. If the "P/S" ratio still holds, then the company could be valued at $250,16 billion in 2030 - a 462% upside from today's valuation. Similar to Block's case, this case is very achievable given that consumer spending has increased by a "CAGR" of 7% over the past 53 years in the U.S. ( Macrotrends.net ). In all Shopify's impeccable growth is undeniable and it is likely to continue at least a 15% growth rate going forward due to continued market share gains. For these reasons, Shopify earns a 10/10 with regard to industry growth rate.

3. Operating Leverage

Shopify claims a 10% market share of all e-commerce in the U.S., according to its investor relations site. I believe that the company's incredibly strong market position will give it an opportunity to drive outsized operating leverage in the future. Recently, however, Shopify has only made cuts in "SG&A" which will provide slight leverage for the coming quarters and perhaps even years.

The larger leverage driver, however, for Shopify has historically been scale. When "GMV" growth took off in 2020, so did the gap between the company's revenue and operating expenses. Shopify is likely to enjoy even more economies of scale as more merchants adopt its products and as Shopify upsells its high-margin software products. It is encouraging to see below that Shopify has been able to maintain its operating leverage since the pandemic.

With a unique position as a market leader, Shopify is able to create incredible products in order to make its platform expand and stick. One example of Shopify leveraging its strong capital position is the fact that the company is providing its initial AI services for free to all merchants. This significantly improves the feel of the platform and allows merchants to become more efficient at no cost. If Shopify is able to capture even more market share, say 20% or more, then it will be able to cut down on R&D and marketing spend in order to reap incredibly large profits. While Shopify is still in this growth phase, however, the focus will be on driving higher "GMV" and a higher attach rate through new products. In all, Shopify has a clear history of driving operating leverage through scale and as the company continues to massively scale against a backdrop of more consumer spending, I believe the company has an even larger opportunity to drive operating leverage. For these reasons, I give Shopify a rating of 9/10 with regard to operating leverage.

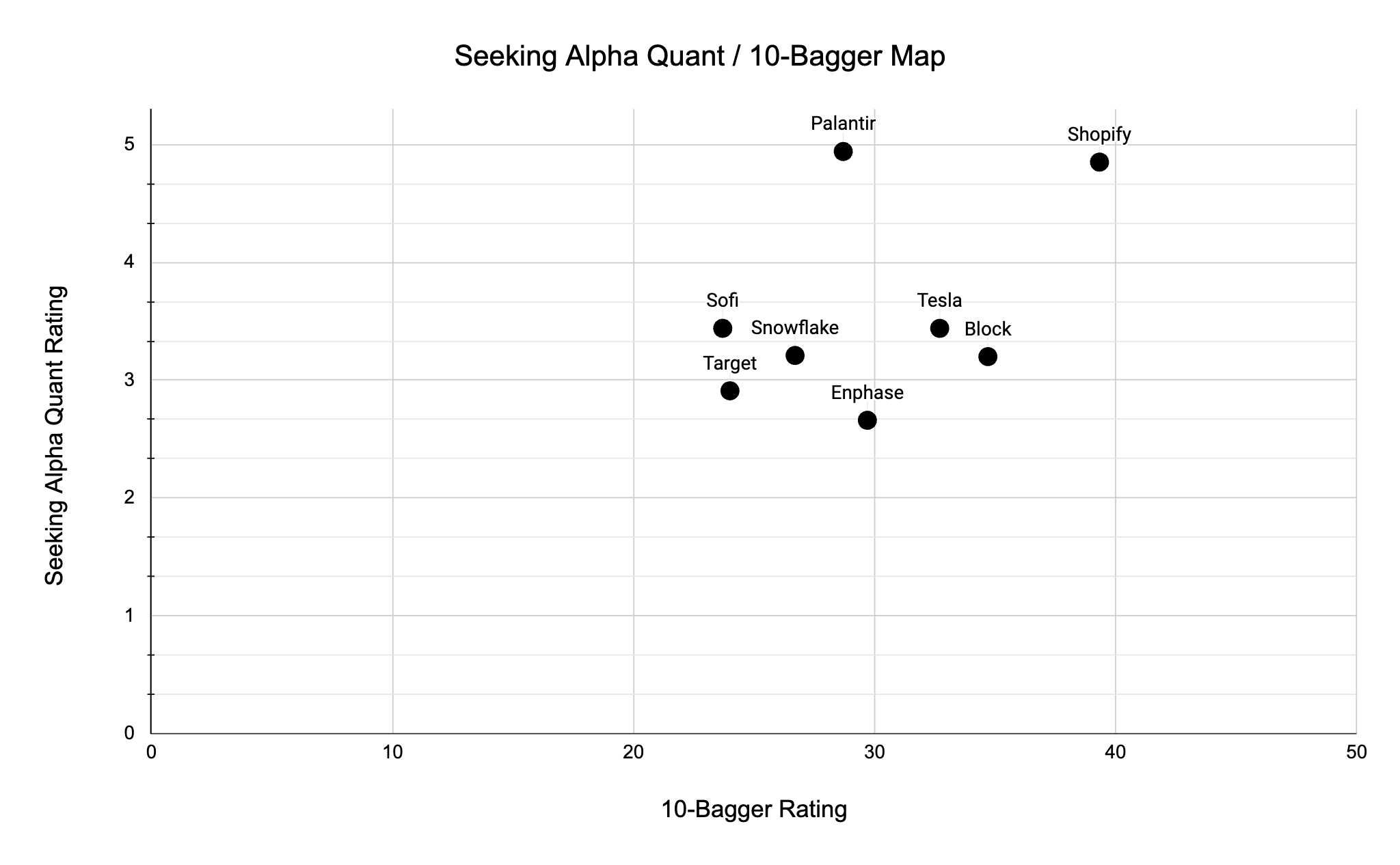

10-Bagger Rating & Seeking Alpha Quant Map

What follows now is a map continuously plotting the companies I analyze based on my 10-bagger rating and Seeking Alpha's quant rating. This allows us to gauge different companies' performance over time.

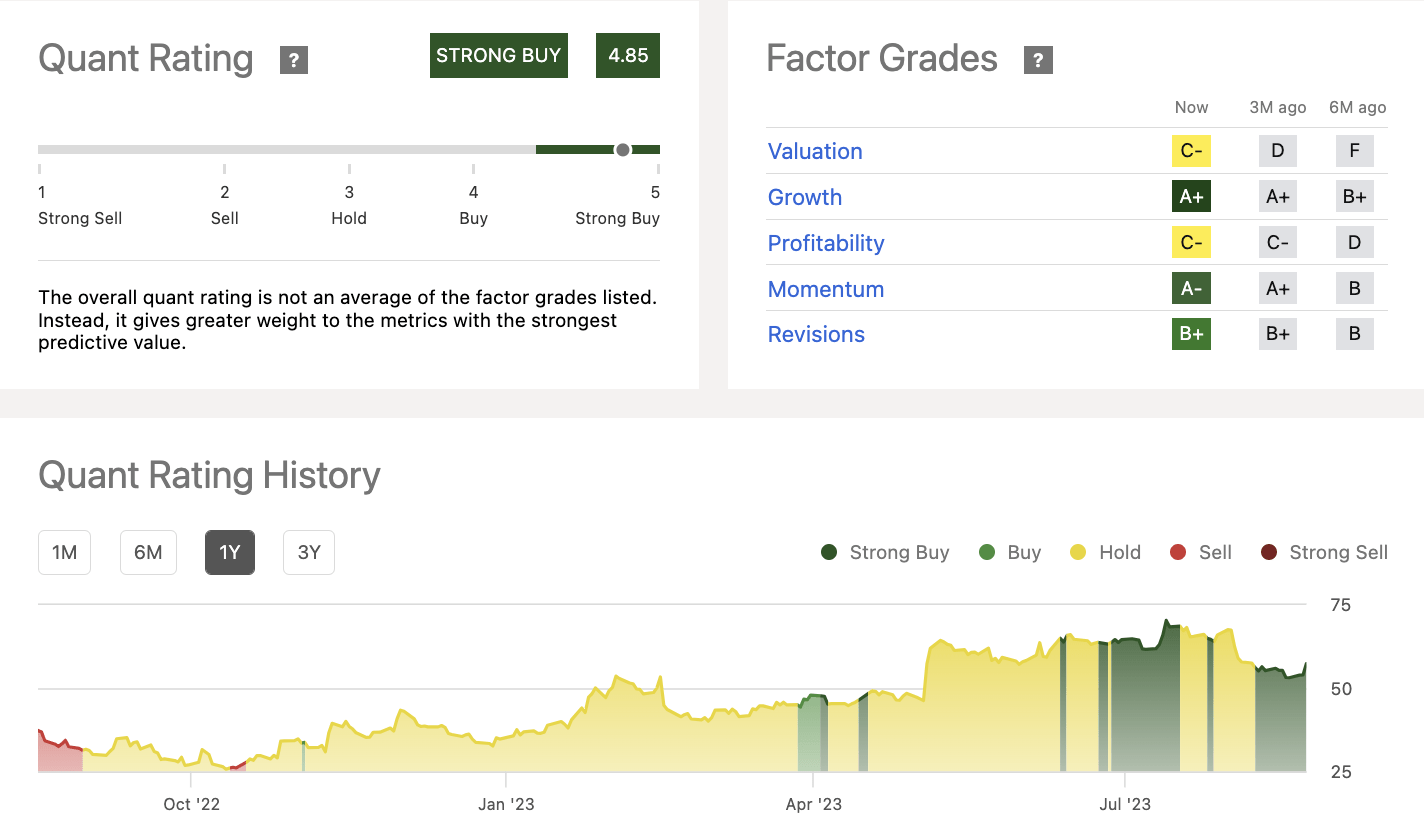

Shopify Quant Rating: 4.85/5.00

{kind=link}

Rating Map

In this analysis, I find that Shopify scores a record 39.33/50 on the 10-bagger scale and a 4.85/5.00 with Seeking Alpha's quant rating. This is the highest total rating yet, which implies that Shopify has the highest 10-bagger potential based on this scale. Similar to my analysis, the quant analysis finds that growth at Shopify is the best possible (A+). However, the quant rates Shopify's profitability much lower than I do - most likely due to differing measuring methods. Lastly, the quant rates Shopify with a C- in regard to valuation, which we will explore more below.

{kind=link}

Valuation

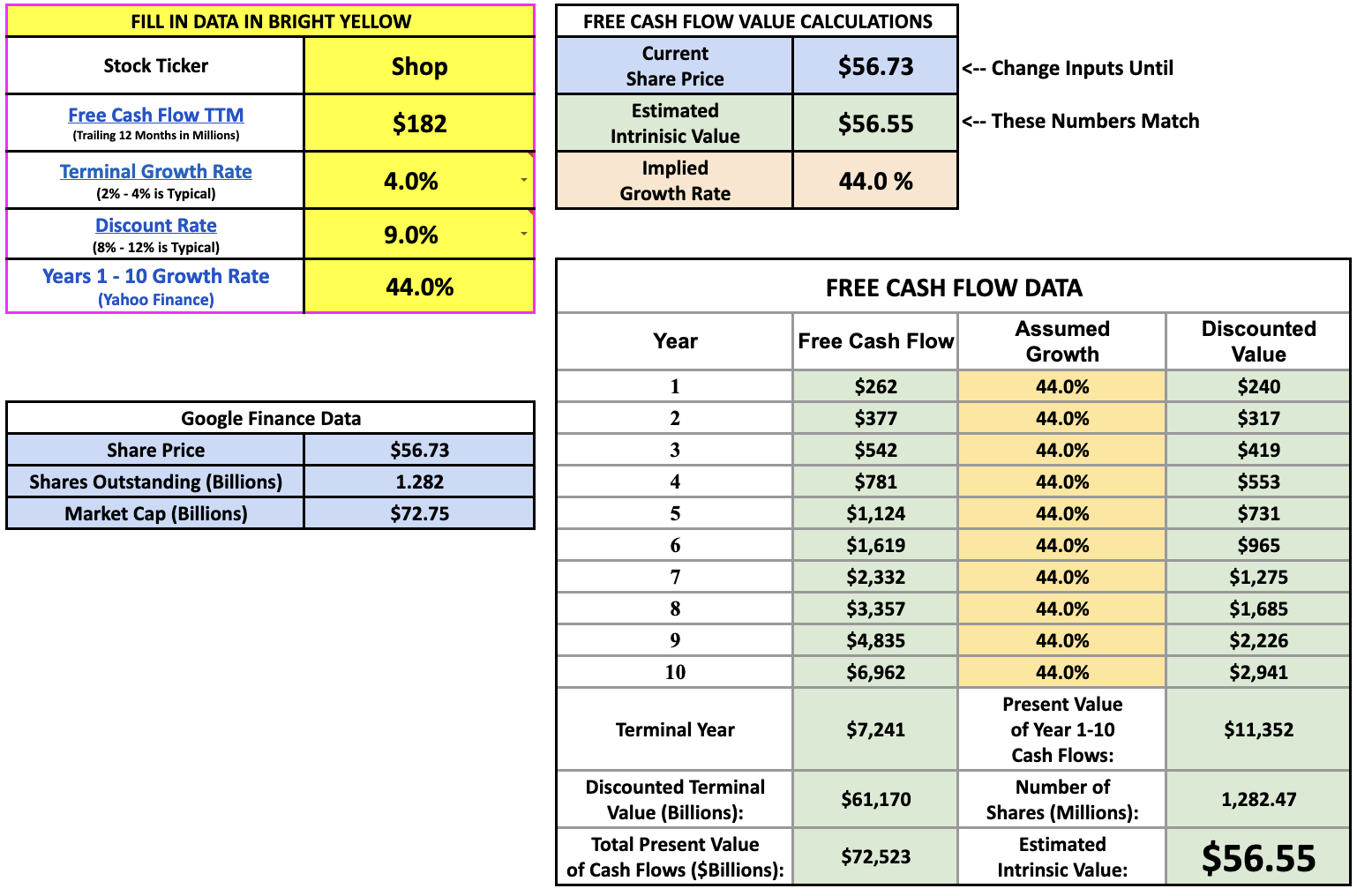

Similar to Block Inc., Shopify is not a business optimized for cash flow generation as of now. During the "TTM" the company generated $182 million in free cash flow, in contrast to earning $535 million in 2021. Shopify is essentially investing in growth which makes its own required cash flow growth rates extremely high. Given the assumptions below, Shopify needs to expand its cash flows by 44% per year for the next ten years. Since Shopify has a huge runway for growth, I can imagine them, instead, growing free cash flow by 22% per year over the next 20 years. So, although the recent run-up has created a slightly high valuation for Shopify - it is completely fair given that the company continues to grow quickly.

In all, I need to change my hold rating to a strong buy rating based on the dynamics shown on the 10-bagger scale. Shopify is a company that is able to deliver incredible growth while becoming leaner as an organization. Furthermore, the company's product development in "AI" will likely pave the way for market share gains and customer adoption for years to come.

{kind=link}

For further details see:

The Hunt For Potential 10x Returns: Shopify's Push Into AI With Lower Overhead Will Drive Growth