XLU - The Magnificent 7 Dividend Stocks For 2024

2024-01-20 08:35:00 ET

Summary

- The Magnificent 7 mega-cap corporations have outperformed the S&P 500, and some now have market caps as large as entire developed economies.

- The dominance of these companies in the stock market is reminiscent of the dot-com bubble in 2000.

- There are signs of a potential reversal in relative performance, with increased fund manager allocations to real estate, staples, and utilities.

- I present 7 magnificent dividend stocks that I'm betting will outperform the market, and maybe even the Magnificent 7, in 2024.

I am not one for jumping onto bandwagons, in investing or in most other areas of life.

In my investing just as in my personal life, I'm not drawn to the fancy or flashy. Sticking with timeless, tried-and-true wisdom is fine by me. In my investment portfolio, that means buying high-quality, dividend-growing, low-risk compounders in order to build my passive income as fast as I can.

No trading, no tricks, just dividends.

But even a brassbound dividend investor like myself can recognize true greatness outside my sphere of competence when I see it.

The Magnificent 7 mega-cap corporations that dominate the stock market indexes have put up truly astounding performance in recent years.

Just since the Roundhill Magnificent Seven ETF ( MAGS ) was launched in the Spring of 2023, the 7 have trounced the S&P 500 ( SPY ), more than doubling its total returns in less than a year.

The picture is even more impressive when you zoom out.

Since the US economy rebounded out of the Great Financial Crisis in 2010, all seven of these demigods -- Nvidia ( NVDA ), Tesla ( TSLA ), Microsoft ( MSFT ), Apple ( AAPL ), Amazon ( AMZN ), Meta Platforms ( META ), and Alphabet/Google ( GOOG ) -- have outperformed the market by at least double.

Nvidia in particular has crushed the market with its legendary growth, built on the back of its top-tier gaming, data center, and artificial intelligence microchips.

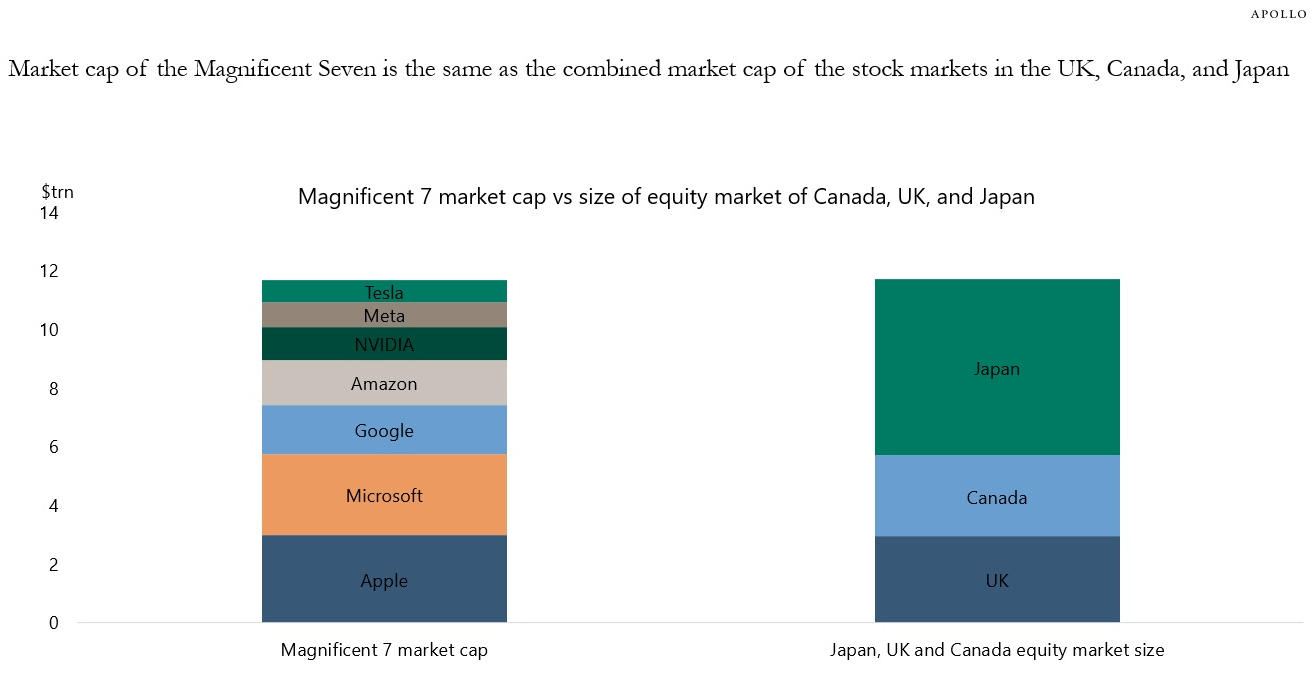

On top of incredible growth in revenue and earnings, this massive expansion in market cap has rendered these 7 titans as large as entire developed economies on their own.

Apple and Microsoft, for example, both sport market caps about the same size as the entire GDP of France as well as the entire market cap of the United Kingdom stock market ( EWU ).

Together, the Mag 7 boast about the same total market cap as the entire stock markets of the next three largest national exchanges in the world besides the US.

{kind=link}

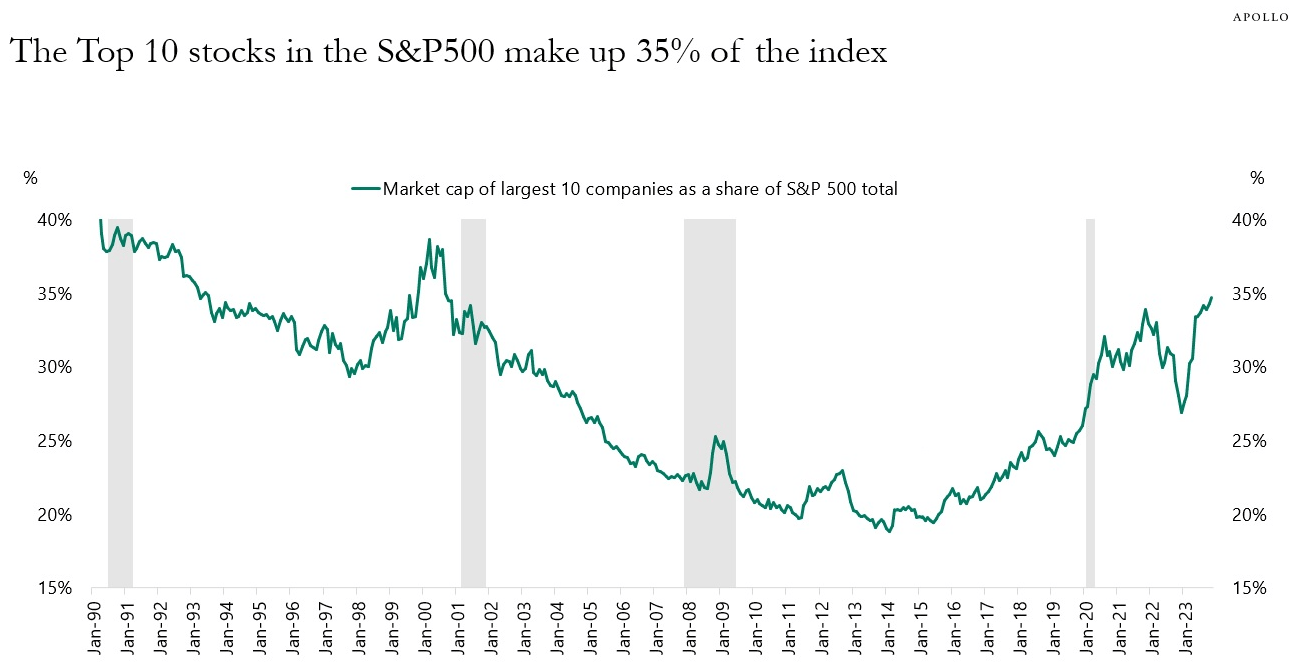

If you expand the list out to the 10 largest companies in the S&P 500, which would include Berkshire Hathaway ( BRK.A , BRK.B ), Broadcom ( AVGO ), and Eli Lilly ( LLY ), maker of the blockbuster diabetes/weight loss drug Mounjaro, then you get a top 10 combined market cap making up 35% of the total S&P 500 index.

{kind=link}

It was higher during the 2000 dot-com bubble, and higher still in 1990, but today's 35% is still above-average. The two largest stocks, Microsoft and Apple, together account for 15% of the total index!

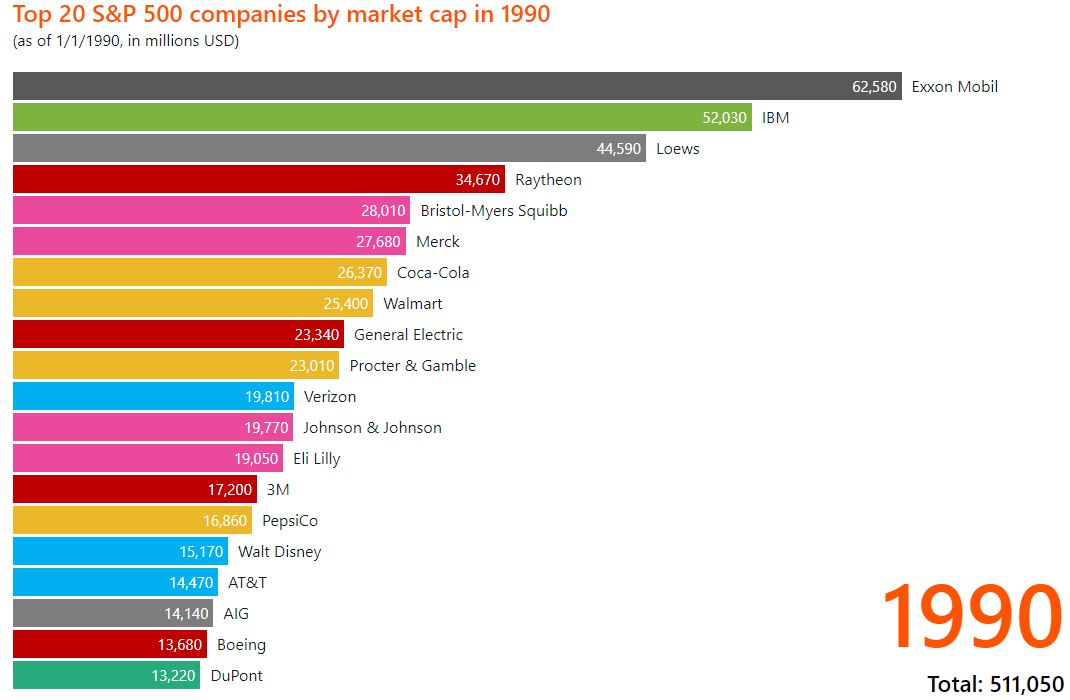

For what it's worth, today's top stocks by size are more reminiscent of the year 2000 than of 1990. In 1990, only one of the top 10 stocks in the S&P 500 was a tech stock, International Business Machines ( IBM ).

{kind=link}

In 2000, 5 of the top 10 largest companies were tech names: Microsoft, Cisco Systems ( CSCO ), Intel ( INTC ), IBM, and Oracle ( ORCL ). Microsoft alone accounted for 3.8% of the total index.

{kind=link}

The "total" seen in the bottom right corner is only the total for the top 20 stocks, not the entire index.

It is not unusual to see that the biggest companies in the stock market are really, really big.

But even by historical standards, today's biggest corporate giants are abnormally larger. Microsoft's ~7.5% share of total S&P 500 market cap is bigger today than it was at the beginning of the year 2000.

I don't mean to suggest that these titans haven't earned their place in the stock market hall of fame, nor that they are dramatically overvalued relative to their growth rates.

But how long can their magnificent run go on?

I am by no means calling a top, but consider the following.

The Nasdaq 100 Index ( QQQ ), dominated by the Mag 7, exhibits a level of total return outperformance against the Vanguard Real Estate Index ( VGSIX , VNQ ) not seen since the 2000 dot-com bubble.

Again, I am not suggesting the Mag 7 is a bubble. I'm saying the level of outperformance over real estate hasn't been seen since techy growth stocks were in a bubble.

The same holds for the relative outperformance of QQQ over utility stocks ( XLU ):

And the same also holds true for the relative outperformance of QQQ over consumer staples stocks ( XLP ):

These three stock sectors -- real estate, utilities, and staples -- cover a lot of the defensive, steady dividend compounders that typically populate the portfolios of dividend growth investors like myself.

Being a DGIer has often felt like standing outside in the snow, alone, peering into a warmly lit house where partygoers laugh and jovially clink their champagne glasses.

Could 2024 be our year? Our long-awaited comeback?

I'm not holding my breath, but it's possible.

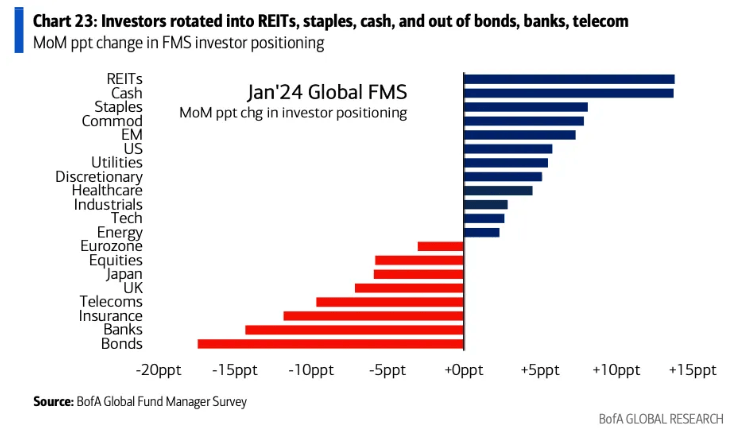

In January 2024, global fund managers greatly increased their allocation to REITs, staples, and to a slightly lesser degree utilities -- notably, more so than tech.

{kind=link}

These fund flows haven't been enough for utilities or staples to beat the Mag 7, but real estate has barely edged out the 7 in total returns since November 2023.

Even so, a reversal of relative performance is possible.

The Last Stand of the "Higher For Longer" Narrative

Right now, I believe we are in the midst of a "stubborn inflation" head-fake.

The dominant narrative today is that the "last mile" of disinflation will be the hardest. Structural inflation is higher today than before the pandemic, so goes the narrative, and thus returning to 2% inflation will take a long time, and the Fed will not be able to cut interest rates anytime soon. The cash-rich and debt-light Mag 7 perform just fine in this environment, therefore they'll continue to outperform.

Pardon my sailor's tongue here, but the macro portion of this narrative is pure dog water .

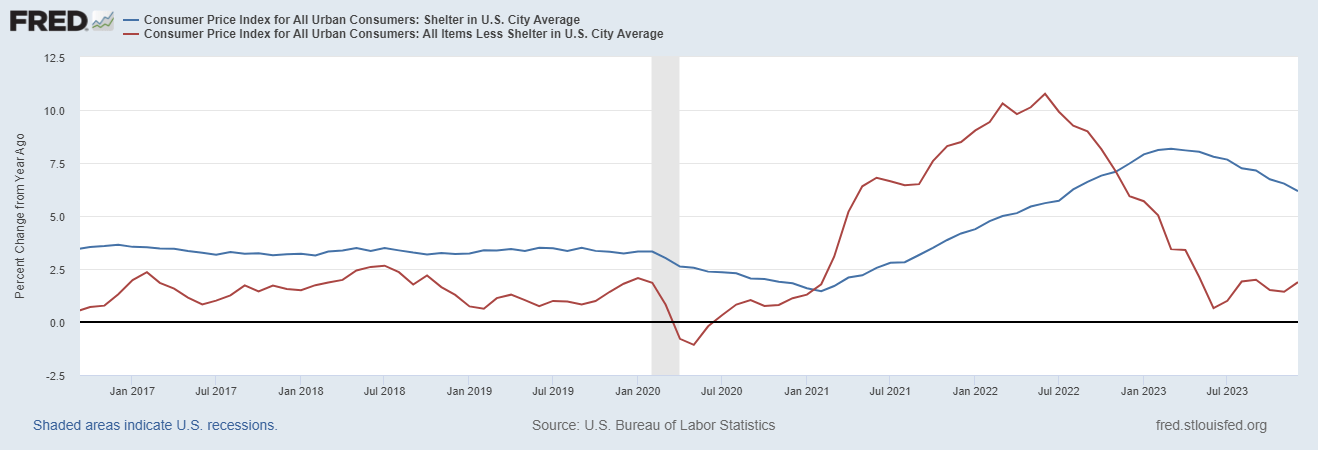

The only reason the CPI still shows a number over 2% is the severely lagged shelter component, which still showed a 6.2% increase in shelter costs in December 2023 despite all major real-time national rent indexes showing rents flat or negative year-over-year. Shelter CPI will continue to its slow, downward slide this year.

If you exclude the lagged shelter component of the CPI, the headline number would have been 1.9% in December, the seventh straight month below 2%.

US Shelter CPI (Blue Line) Vs. CPI Ex Shelter (Red Line):

{kind=link}

The same would hold true if you plugged in any national rent index (Apartment List, Zillow, Redfin) instead of the Bureau of Labor Statistics' lagging shelter metrics.

The biggest reason why CPI ex shelter has slightly crept up in recent months is soaring car insurance prices . This, admittedly, is a real-time price increase consumers are really facing. But car insurance premiums are simply reacting with a lag to the spike in car and auto parts prices over the last few years. Since car and auto parts prices are no longer going up, car insurance premiums will likely halt as well once they've built in the last few years of auto cost increases.

Real-time inflation is already below 2% ( including car insurance) and has been so for the better part of a year. There are no indicators of a big resurgence in inflation coming anytime soon.

So, I believe this current market selloff is the last stand of the "higher for longer" narrative that says the Fed won't be able to cut interest rates for a long time due to "stubbornly high" inflation.

For a more thorough broadside on the "higher for longer" narrative, check out my recent article " The Five Horsemen of Deflation Are Returning ."

The Magnificent 7 Dividend Stocks

If my macro thesis above bears out -- if inflation continues to drop and the Fed begins lowering the Fed Funds Rate sooner rather than later -- then I think many dividend stocks will end up outperforming the market and perhaps even the Mag 7 this year.

But if I had to pick just 7 dividend growth stocks to try to beat the Mag 7 in 2024 on a total return basis, it would be the following:

Agree Realty ( ADC )

ADC is a net lease REIT that invests exclusively in single-tenant retail properties leased to the nation's largest and strongest retailers. These tenants operate primarily in defensive, essential retail industries like grocery, home improvement, discount, auto parts, warehouse club, and convenience stores.

{kind=link}

Nearly 70% of ADC's tenant base are investment grade-rated corporations.

ADC also enjoys a pristine balance sheet, low debt, very little debt maturities until 2028, and a best-in-class cost of capital that enables it to profitably acquire the best of the best omnichannel retail real estate.

Even after a slight rebound in price, ADC still trades near its lowest valuation in the last decade -- 15.5x adjusted funds from operations, or AFFO.

If inflation and interest rates come down further in 2024, as I suspect, ADC's long-term and bond-like leases should fuel strong performance for this high-quality REIT.

American Electric Power ( AEP )

AEP is a regulated utility company that provides power to vast swathes of territory in the Midwest and South, especially Texas. It boasts an ambitious capital deployment plan in the coming years, focused almost entirely (99%) on expanding its regulated rate base via investments in transmission & distribution (power lines) and renewable energy.

The stock has been dealt some setbacks lately with unfavorable rate decisions in some of its lower ROE territories, but management still projects 6-7% long-term earnings growth and a reduction in leverage. Getting there may take a little longer than hoped, but lower interest rates over the course of 2024 would lend AEP a massive boost in achieving its capital deployment and earnings growth plans.

In the meantime, AEP sits near its lowest valuation in a decade while sporting its highest dividend yield in a decade.

Brookfield Renewable ( BEP , BEPC )

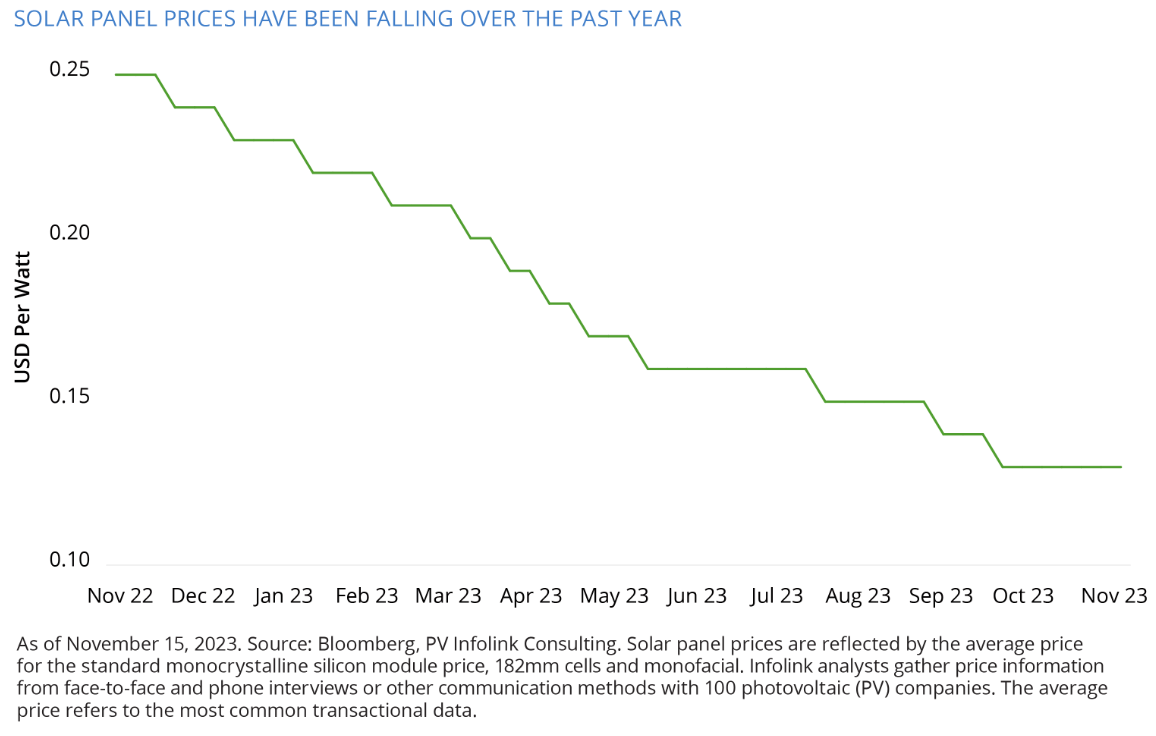

Renewable power producers like BEP have sold off heavily in sympathy with regulated utilities. BEP is the largest independent renewable power producer with about 50% of its assets in stable, semi-dispatchable hydropower dams and the rest split between wind, solar, battery storage, and few small bets.

The problem for renewables comes down almost entirely to capital costs. The cost of materials, especially for solar panels, have continued to fall recently.

{kind=link}

The only area of significant operational difficulty for renewables lately has been offshore wind, but BEP has no exposure to offshore wind. Onshore, utility-scale wind and solar continue to be a phenomenal growth story, both in the US and globally.

BEP has a strong market share in the renewables space and is poised to capture a sizable portion of that future growth.

Even after rebounding off its lows, BEP still looks cheap, and its 5.3%-yielding dividend should continue to grow at a 5-7% annual pace.

Medtronic ( MDT )

MDT is one of the world's largest medical device makers, famous for (among other things) pacemakers, blood sugar monitoring systems, and blood pressure monitoring devices. But MDT has also invested heavily in surgical robotics and various other products that will give it a boost from the resurgence in elective surgeries.

MDT has been plagued in recent years by pandemic-related delays in elective surgeries, inflation, supply chain breakdowns, and most recently, blockbuster drugs that threaten to reduce demand for some of its devices.

Management insists that the GLP-1 drug hype is overblown and that it will have less effect on demand for their products than the market thinks. I'm inclined to believe them, if for no other reason than that these drugs are not widely available and affordable to most people yet.

Blood sugar monitoring and automatic insulin pumps will probably continue to be needed for a long time to come.

Innovative healthcare companies like MDT have a lot of tailwinds, and with the elective procedure environment back to its pre-pandemic norm, most of the headwinds are behind.

NextEra Energy Inc. ( NEE )

NEE was a major loser in 2023, dropping almost 30% over the course of the year. As one of the highest valued utility companies, NEE had some of the most room to drop in order to compress its valuation multiple. The issue of high capital costs plagued both NEE and its publicly traded subsidiary company, NextEra Energy Partners ( NEP ), which acts as a financing vehicle for NEE's renewable energy development platform.

But let's look at the basics: NEE enjoys the enviable status of supplying power to one of the fastest growing parts of the country in Florida with its Florida Power & Light regulated utility. Plus, it enjoys all the same tailwinds as BEP through its renewable energy development arm, NextEra Energy Resources.

The problem is relatively high capital costs.

But whether it ends up being fast or slow, the direction of interest rates this year will almost certainly be down . Maybe the Fed doesn't cut until the second half of 2024 or even the first half of 2025. I doubt that, but even if so, NEE can still find ways to finance its growth investments until debt financing becomes feasible again.

Now at around a 18x P/E ratio, NEE may not seem cheap on an absolute basis, but it is definitely cheap compared to its historically average multiple in the high 20s. And it is also cheap relative to its robust growth prospects in the golden age of renewables.

PepsiCo ( PEP )

This consumer staples blue-chip is experiencing a rare correction right now, having sold off a little over 10% in the last 6 months. That's a lot for a low-beta company like PEP!

The company manages such best-in-class staples brands as Pepsi, Quaker Oats, Frito Lay, Gatorade, Sabra, and dozens more. Like MDT, PEP has been dinged by the fear that popular weight loss drugs will take a big bite (pardon the pun) out of PEP's sales, especially for snack foods.

Count me skeptical.

I think GLP-1 drugs may have a big effect on a small number of people and little to no effect on the vast majority of the population.

Given PEP's 50-year dividend growth streak and recent history of 10% dividend hikes, a 3% dividend yield strikes me as being adequate for this snacking and beverage giant.

Verizon ( VZ )

This member of the three-part wireless communications oligopoly in the United States got shellacked in recent years, shedding 50% of its value from its early 2020 peak to its October 2023 trough.

As the premium plan provider in the wireless space, VZ suffered a loss of subscribers from the aggressive marketing and discounting of its peers. Plus, it invested tens of billions of dollars into its 5G rollout. Lots of investments + flattish revenue + tons of debt + rising interest rates = bad combination.

Today, however, subscriber growth is gradually coming back as peer discounting cools down, 5G investment spending is dropping, and VZ is seeing its free cash flows rebound.

And, of course, when you've got as much debt as VZ has, falling interest rates really help too. I think the falling interest rate environment this year should add to VZ's tailwinds.

While waiting for the rebound, VZ's 6.8% dividend yield pays you for your patience.

Bottom Line

I am not arguing that the Magnificent 7 are overhyped or overvalued. They are phenomenal companies.

But trees don't grow to the sky. Stock prices, even for magnificent companies, are not unconstrained by the gravity of valuation.

After such a strong run in 2023 up to today, I would argue that many dividend stocks are well-positioned to begin outperforming from here.

Maybe my "Magnificent 7 Dividend Stocks" above will outperform the Mag 7 this year. Maybe they won't.

In any case, for dividend investors like me, I think it would be hard to go wrong with these 7 high-quality, reliable dividend growers.

For further details see:

The Magnificent 7 Dividend Stocks For 2024