WBA - The Retiree's Dividend Portfolio: Complete 2022 Review - Cash Flow Is King

Summary

- John and Jane's Portfolio generated an average of $6,376.71/month of dividends in 2022 compared with $5,321.93/month in 2021.

- Their Portfolio has an average balance of $1.72 million in 2022 compared with $1.63 million in 2021.

- Cash balances have increased heading into the end of the year and is comparable to what we saw in 2021.

- One of the most valuable tables is the unrealized gain/loss table because it underscores the power of generating cash flow in retirement.

Generating cash flow has become the number one topic I talk about with anyone who is interested in my take on personal finance. Even in the industry I work in there are many people who have never considered the concept or who may not find it relevant because they have 30 years of work before they can reach retirement age. Not only that but too many Americans (other countries may be similar but I can't speak for them) live paycheck-to-paycheck so the concept of cash flow is meaningless because they either don't care or see a way to manage it.

Now, I could find a website and provide the Webster's dictionary definition of what cash flow means but I often use the following example because I find it more relatable, especially when it comes to those who are currently working and have various types of loans (cars, home, etc.).

Let's assume that you have an interest rate that is better than anything that is currently being offered but your payments exceed the amount of monthly income that you generate. On one hand, someone might tell you that you shouldn't consider refinancing (which seems pretty obvious considering going from a better rate to a worse rate doesn't make a lot of sense) but if you don't refinance you're going to likely rack up more debt, and over time, reach the point where you can no longer sustain the payments needed which will result in delinquency and potentially cause you to default on the loan altogether.

Cash Flow - Working Age Borrowers

One of the pitfalls of younger borrowers is that refinancing or consolidating debt is often seen as an opportunity to justify buying something else instead of enabling better savings habits or focusing on the elimination of other debt. One of my favorite things to do is walk through the math of what a consolidation loan will do for someone and then ask: "what do you plan to do with the additional cash flow?" Most responses look something like this:

- I have been wanting to renovate the kitchen.

- We have been talking about buying an RV.

- A trip to Mexico sounds enjoyable.

- Or the most common scenario was that the husband will have something in mind for himself (like a motorcycle) while the wife has something in mind for herself (like a new car).

All of these items often include spending more money than the cash flow being saved which then puts those borrowers back into the same position that we are trying to get them out of (which is why I have to remind them that consolidating debt isn't eliminating anything it's just rearranging how that debt impacts you). When I am training new staff I always tell them that when I was in their position, I considered 50% of my job to be talking people out of doing dumb things with their money.

Now, the responses I would like to see (in my perfect world):

- Paying some of the extra cash flow towards the consolidation loan to get out of debt faster.

- Establishing emergency savings with X% of the cash flow to cover unavoidable future expenses. This allows borrowers to avoid unnecessary debt in the future.

- Affording meaningful lifestyle changes (one of my absolute favorites) like allowing one parent to quit their job or work part-time so they can be a full-time parent, home-school, or pursue a side-hustle full-time. The difference between lifestyle changes and buying stuff is that lifestyle changes create meaningful improvement in someone's quality of life whereas buying a motorcycle really only makes you happy when you can drive it (and even that is debatable when we factor in the monthly payment).

This is why one of the most concerning signs is to see working-age borrowers with newer lines of credit (credit cards, home equity LOC, etc.) with escalating balances.

- Newer credit lines (less than two years of history) with escalating balances can be assumed that the borrower is using the credit line to live a lifestyle that is unsustainable from a cash flow perspective.

- Established credit lines (more than two years of history) with higher balances are still concerning but it demonstrates that the borrower has experience covering the payment of the debt from their cash flow.

There are exceptions in both of these scenarios, but the first bullet point is more likely to represent a borrower from age 18 to 40 while the second scenario is more likely to represent a borrower from age 40 to age 65.

Cash Flow - Retirees

Borrowers who are retired or closing in on retirement age are frequently relying on mortgage debt to consolidate and make their payments affordable on the reduced income they have available to them in retirement.

Now, you might be wondering how common is this? One of the most common reasons for a mortgage refinance (30-year mortgage) that I have seen is that the borrower reaches retirement age but is unable to retire when they have 10 years' worth of payments remaining on their 30-year note because the payment is based on the original mortgage amount. In order for a retiree to afford their mortgage payment, car payment, and credit card debt they will likely choose to consolidate their debts to a 30-year mortgage because this will reduce the monthly payment to less than what they are currently paying on all of the debts.

Consider the following example:

- $350K loan at 3.5% interest = $1,572/month Principal & Interest

- $30K car payment of $500/month

- $20K of credit card debt = $500/month

Total monthly obligations of $2,572/month (and remember, this doesn't factor in insurance, property tax, etc).

The balance with 10 years left is $160K on the mortgage so with the addition of $50K of debt we have $210K of total debt.

- $210K loan at 6.5% interest = Total monthly obligation of $1,327.34/month

What this tells us is that retirees are more likely to refinance their home to a higher interest rate if cash flow is a concern because it is still likely to improve their cash flow and then allow them to actually enjoy their retirement.

I am confident in saying this because my primary job is to underwrite and review loans. It has become abundantly clear that our retirees have been relying on cheap mortgage debt to make their retirement sustainable (and even though rates have increased) a retiree is still able to make their situation more affordable than what it would be even though their existing loans are offering better interest rates.

Cash Flow - Final Points

Cash flow is a topic that even well-educated individuals don't understand because we have completely failed to teach any of these concepts in our K-12 education system. I am not disparaging working-age borrowers for buying frivolous toys or going on vacation (believe me, as the proud owner of an excavator and a dump trailer I don't have a leg to stand on) or that retirees shouldn't have debt when they go into retirement.

My primary goal of this discussion is to encourage the average person to think about whether or not their debts are covered by their cash flow and if they maximize cash flow what can they do to improve their situation. Maximizing cash flow is a good thing, but where you choose to allocate that cash flow is even more important because consumers who maximize cash flow but allocate it poorly aren't improving their situation (in some cases they might even worsen their situation). For example, I previously mentioned that I own a mini excavator and dump trailer but I made the decision to purchase these because I generate enough cash flow from my side hustle to cover the payments associated with those debts. I also have plans to use those items in the future to generate additional cash flow (which is why it's important to consider the true purpose of buying something).

Getting back to the focus of this article, John and Jane have done everything right when it comes to creating a sustainable retirement. They retired with no debt and had enough money to make all the purchases they wanted prior to retirement (they were able to buy an RV and a new car and it had absolutely no impact on their ability to create an affordable stream of income in retirement). This means that they will have significant cash flow available above their normal monthly bills, traveling, putting fuel in their vehicles, etc.

Cash Flow - John and Jane's Portfolio

I recently did an annual update with John and Jane where I discussed the cash flow being generated by each of their accounts and I gave them the following numbers to give them perspective on how much money they are currently taking and how much is available to them without impacting their current investments (i.e. the need to buy/sell shares to cover the withdrawal).

- The Taxable Account generates $1792.62/month of dividend income on average and John and Jane were only withdrawing $1000/month. Because they are being taxed on this income (regardless of whether or not it's withdrawn or left in the account) decided to increase the amount taken out to $1700/month.

- In Jane's Traditional IRA, she generates an average of $1619.80/month of dividend income on average and is not making any withdrawals. She has no plans to begin withdrawing funds until she speaks with her accountant (since this would have tax consequences).

- In Jane's Roth IRA, she generates an average of $768.10/month of dividend income on average and is not making any withdrawals. She does not have plans to begin withdrawing funds but understands that she could withdraw these funds and it would have zero implications on her Taxable income.

- In John's Traditional IRA, he generates an average of $1485.63/month of dividend income and is currently withdrawing $1000/month. John plans to continue withdrawing $1000/month but will discuss what it would look like to withdraw more with his accountant since this income is taxed.

- In John's Roth IRA, he generates an average of $710.57/month of dividend income on average and is not making any withdrawals. He does not have plans to begin withdrawing funds but understands that he could withdraw these funds and it would have zero implications on his Taxable income.

In total, John and Jane's Portfolio generated an average of $6376.71/month of dividend income in 2022 and they have elected to draw $2700/month from these accounts moving forward in 2023. Using these figures, John and Jane are only withdrawing 42.3% of their available cash flow. With no debt and no significant purchases on the horizon, they should feel very comfortable with the current lifestyle especially because I am not factoring in what they earn from Social Security or other interest income generated from investments that I do not manage (primarily CDs at brick and mortar financial institutions). Even though I see a rough 2023 for the market as a whole, their portfolio continues to grow the dividends paid (please reference the "Five-Year Total Portfolio Income" table) every year for the last five years that I have been helping them with their portfolio.

John and Jane's Realized Gain/Loss - 2022

I don't like to spend too much time on the realized gain/loss aspect of the portfolio because there is a lot of noise that comes from this. The first reason I like to include this information is to demonstrate that we aren't buying/selling shares with major gains (in most cases) and that most trades that occur are wash trades which aligns with my primary strategy of selling off high-cost shares and accumulating more when the price is low.

The second reason I like to show this is that it is possible for someone who writes articles like this to make their results look better than they are specifically by selling shares at a major loss so that it doesn't show up in their daily portfolio numbers. Therefore including this information will make it clear that there was no manipulation that took place to make the portfolio look like it performed better.

I know this might sound easy but if it was easy everyone would do it. This requires a lot of patience and a contrarian mindset. To make my point, look at the table of Total Portfolio - Cash Balance in the 2020 column. Prior to the initial commotion of COVID cash balances were $125.3K in February 2020 and dropped to $31.3K in May 2020. During this time account balances dropped but the only reason cash dropped is that it was being deployed or withdrawn. During this time John and Jane were taking no withdrawals so that tells you the money was being deployed.

As the market recovered we were able to sell off some of our high-cost positions and were left with the same number of shares because we purchased the stock when the price was rock bottom.

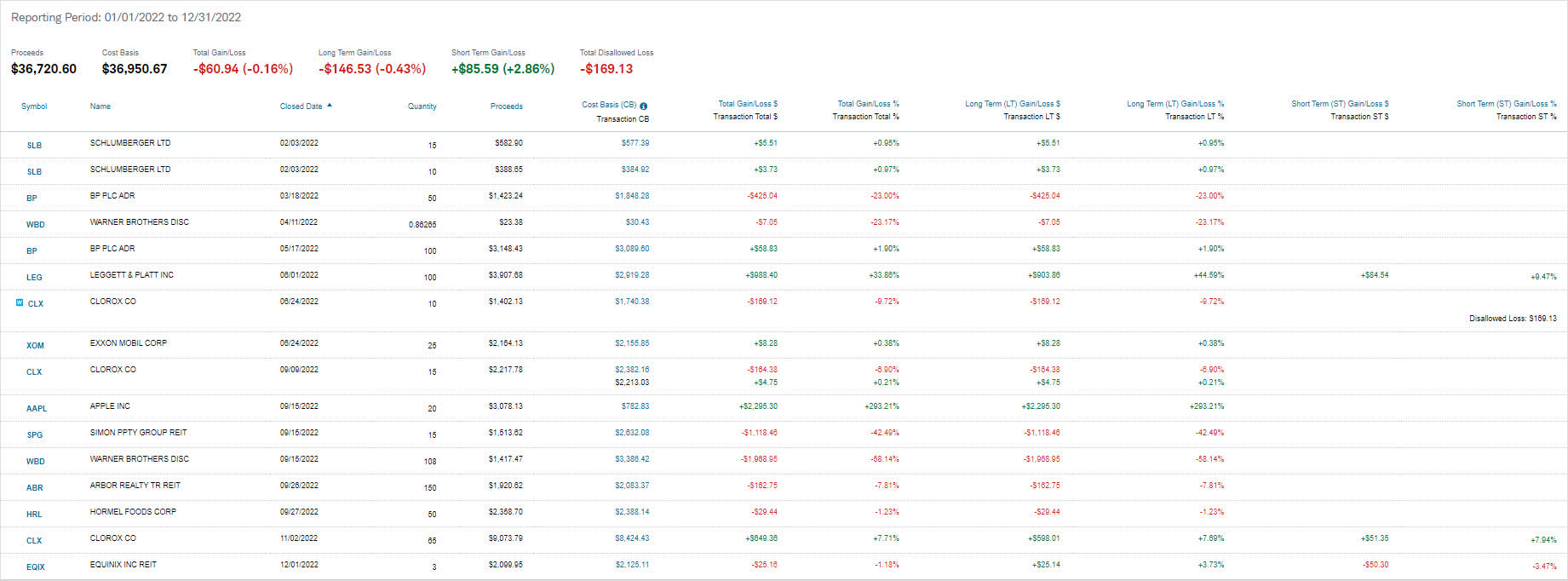

Taxable Account

{kind=link}

In the Taxable Account, we always consider the negative tax implications that can come from selling shares when a large gain might be involved or the potential benefit of selling underperforming shares at a loss to reduce taxable income. This year we are able to take advantage of selling a few shares of Apple ( AAPL ) stock to help balance out some of the losses that were taken on the sale of other positions. The main point I want readers to take away from this section is that most gains or losses are low dollar amounts and typically involve the sale of a portion of the position (compared to the sale of the entire position). This is intentional as my primary strategy is to buy shares when they are low and then sell off the higher-cost shares as the stock recovers.

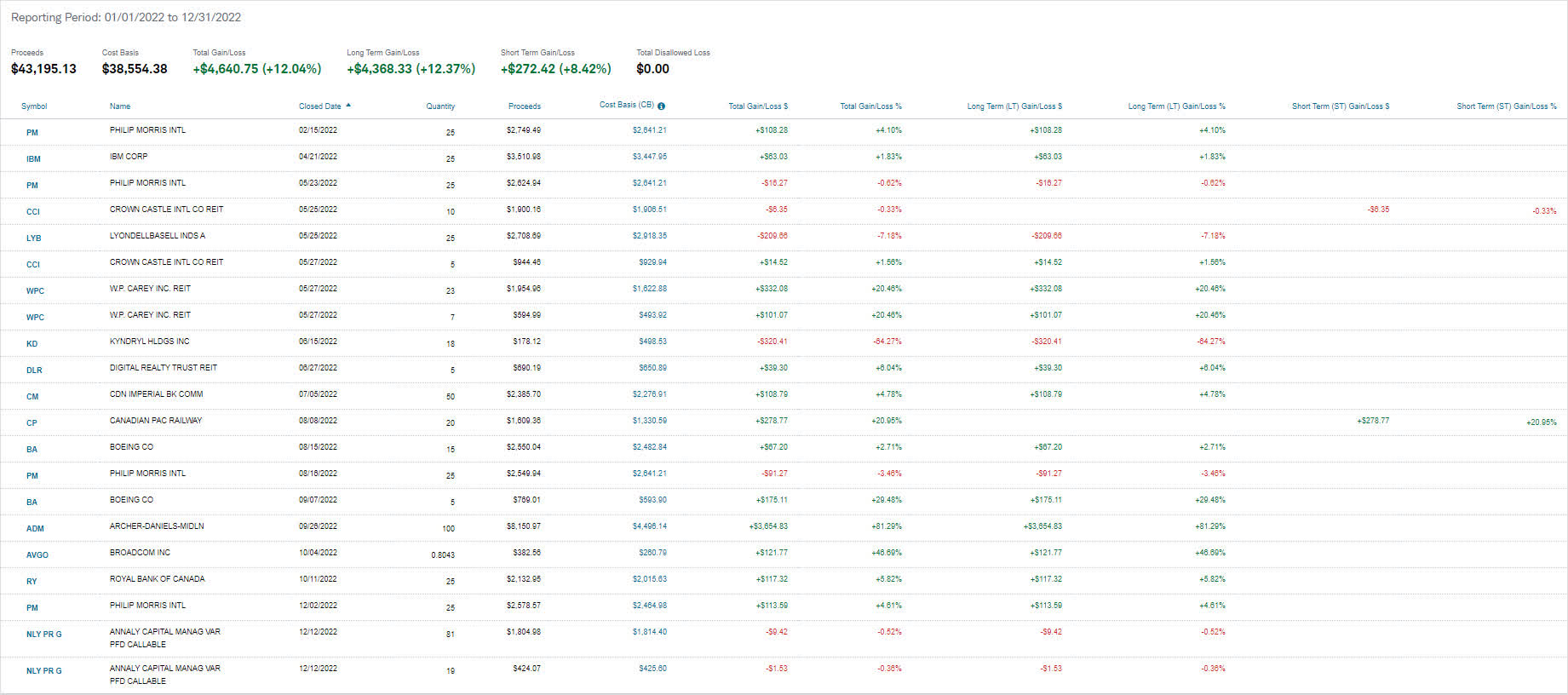

Jane's Retirement Accounts (Traditional IRA & Roth IRA)

The image below represents Jane's Traditional IRA.

2022 - Jane Traditional IRA - Realized Gain-Loss (Charles Schwab)

{kind=link}

There was quite a bit more activity in Jane's Traditional IRA in 2022. As mentioned in the Taxable Account summary, most of the sales that you see resulted in low dollar gains or losses with the exception of Archer Daniels Midland ( ADM ) because this position was specifically reduced because the stock reached a point where I believed it to be significantly overpriced (it is down approximately 15% from its 52-week high). One of the most successful sets of trades we made in this portfolio was the paring down of the Philip Morris ( PM ) position by buying in the low $90/share range and then selling off some of the higher-cost shares with a cost-basis over $100/share.

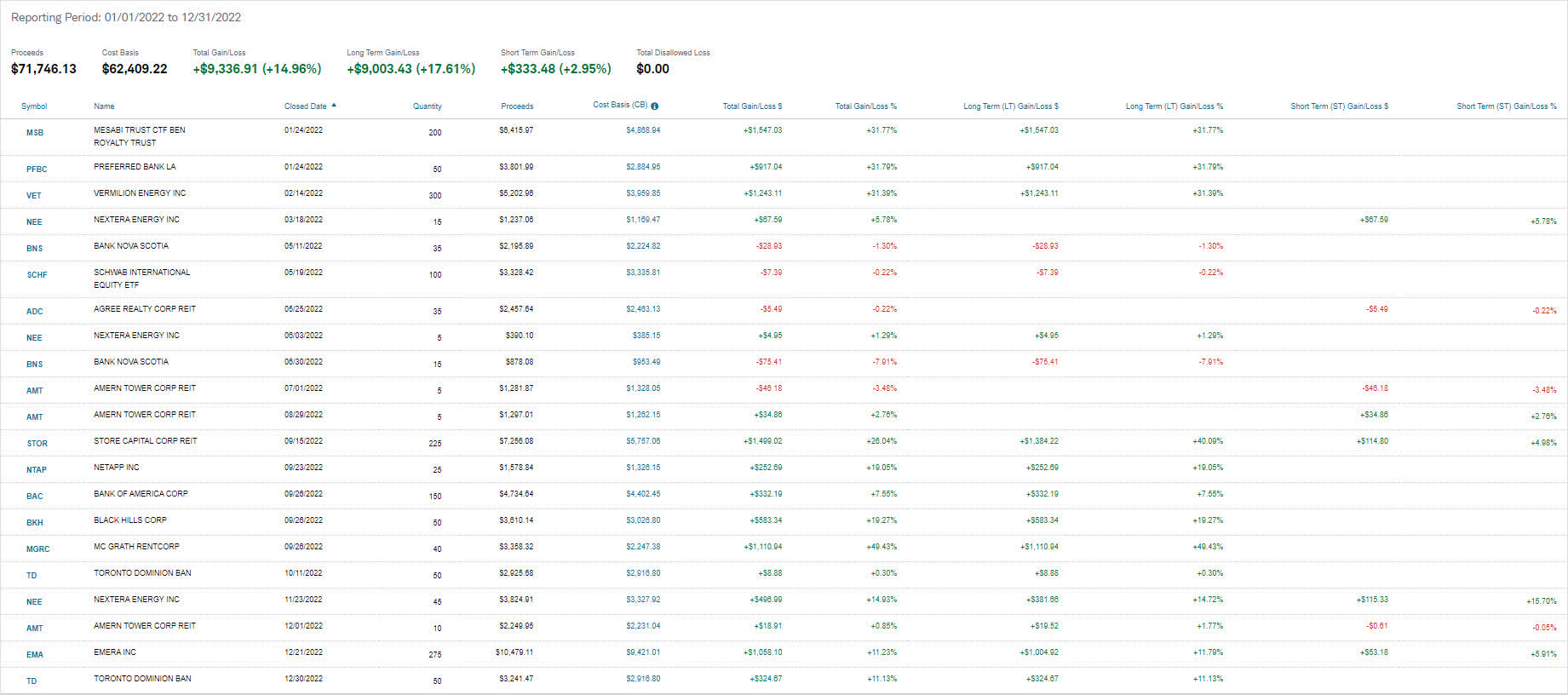

The image below represents Jane's Roth IRA.

{kind=link}

We made quite a few trades in the Roth IRA with a few more position eliminations. Some of these were because it made sense and others like Store Capital ( STOR ) were because the company was being taken private and there was nothing we could do about it. Other stocks like Emera ( EMRAF ) and Vermilion ( VET ) were eliminated from the portfolio as we really focus on quality moving forward.

For those who are interested in why we have concerns about EMRAF I strongly recommend reading the article Emera: Don't Chase That Yield by Trapping Value. The author also has an excellent write-up about Clorox ( CLX ) which we sold the majority of our position in the Taxable Account available as well.

John's Retirement Accounts (Traditional IRA & Roth IRA)

The image below represents John's Traditional IRA.

2022 - Jane Traditional IRA - Realized Gain-Loss (Charles Schwab)

There were a number of notable trades in John's Traditional IRA:

- CyrusOne - This data center REIT was purchased and taken private so there is nothing that we can do regarding the sale of these shares.

- Valero ( VLO ) - We amassed a very large position in VLO during the period of time when there was major volatility in gas prices. We decided to reduce the size of this holding by eliminating the high-cost shares but this resulted in some large gains due to the explosive growth of the stock price when gas prices reached record highs.

- RPT Realty Preferred Series D ( RPT.PD ) - We sold off this preferred as interest rates started climbing and the capital gains were too good to pass up and reinvest in a more stable preferred or a certificate of deposit.

- Aflac ( AFL ) - The stock price has reached 52-week highs and we reduced the position because it seems too richly valued with concern about the economic environment in 2023.

- Pepsi ( PEP ) - The stock has seen a tremendous improvement in share price but has reached a point where it looks fully valued. We sold off 25 shares at $180/share with the hope that we can add more shares on a pullback.

Still, the majority of shares focused on eliminating high-cost positions after purchasing additional shares at a much lower price. This strategy is more efficient for capital allocation but offers more downside protection to where shares can be potentially held longer but still sold closer to break-even.

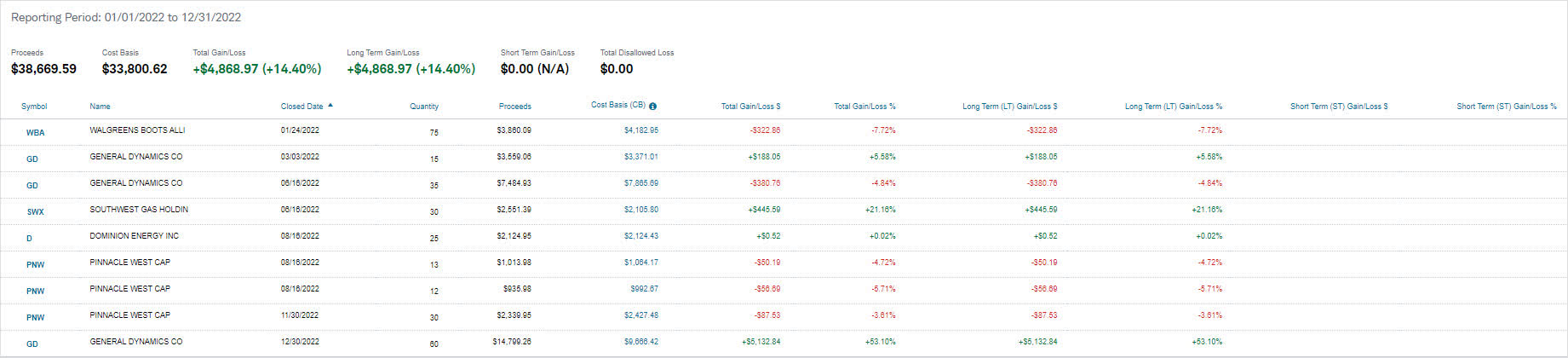

The image below represents John's Roth IRA.

{kind=link}

We eliminated Walgreens ( WBA ) as the stock continues to underperform and finally sold General Dynamics ( GD ) because of its rich valuation.

Pinnacle West ( PNW ) went from being one of the worst utility company trades we had made to one of the best using the strategy of buying low and selling high. As you can see we took small losses on the sale of shares but the current position of 100 shares is now sitting on $1200 in unrealized gains with a cost basis close to $66/share compared to a cost basis that was in the mid-70's a few months after the position was first established.

2022 Results And Historical Comparisons

Here are the highlights of how John and Jane's Taxable and Retirement portfolios performed in 2022 along with historical comparisons over the last five years.

- Total dividends collected in 2022 were $76,520.55 for a total increase of 19.8% over the $63,863.13 of dividends collected in 2021.

- Although the total account balance was down approximately $62,000 year-over-year the average balance (using month-end balances for all 12 months) was actually up by approximately $92,000 year-over-year.

- The total balances of these accounts were down -3.49% in FY-2022. If we add back the $24,000 of withdrawals made from the account the total balances were only down -2.13%. By comparison, the Dow Jones was down -10.63%, the S&P 500 was down -19.44%, and the NASDAQ was down -33.1%.

The tables below are similar to the table of my normal articles but I have compiled all of the information from each account to show the total impact of their cumulative holdings.

The first table shows the total amount of dividends received into the portfolio on a monthly basis for 2022 and 2021.

2022 - Total Portfolio Income (CDI)

The next table shows the same information but goes back five years when I first began helping John and Jane with their portfolio.

2022 - Total Portfolio Income - Five-Year History (CDI)

The table below shows the month-end balances on the Charles Schwab statements. I use these month-end balances to be consistent so that I am not inputting random balances on different days.

2022 - Total Portfolio Balances - Five-Year History (CDI)

We use the same month-end balances from the Charles Schwab statements to collect the numbers for the unrealized gain-loss totals

2022 - Total Portfolio Unrealized Gain-Loss - Five-Year History (CDI)

{kind=link}

The last table shows the withdrawals made from their portfolio in 2022. This was the first year that John and Jane opted to withdraw funds from the portfolio.

2022 - Total Portfolio Withdrawals (CDI)

Conclusion

2022 was a terrible year for the market but John and Jane's portfolio fared quite well by focusing on companies that pay dividends and consistently raise their payouts and some even pay special dividends when they can. With that said, I believe that 2023 will be one of the worst years for dividend growth and that is because so much of the dividend growth in 2022 was the result of large special dividend payouts.

If we exclude special dividend payouts then I believe we will see dividend growth between 4-5% because companies will likely focus on maintaining cash reserves with concerns about the economic environment. Additionally, with interest rates rising it has quickly become less advantageous to support a generous dividend payout by financing it with cheap debt. I expect that companies will begin focusing on a more balanced debt structure and shareholders will be negatively impacted (the impact won't be that negative but the dividend increases are likely to be less generous).

John and Jane are long on all of the holdings in the tables above. I would normally list all of them but there are too many to list.

December Articles

I have included the links for John and Jane's Portfolio for the month of December.

The Retirees' Dividend Portfolio: John And Jane's December Taxable Account Update

The Retiree's Dividend Portfolio, Jane's December Update: Index-Beating Year-End Results

The Retiree's Dividend Portfolio, John's December Update: Outperformed The Major Indexes In 2022

For further details see:

The Retiree's Dividend Portfolio: Complete 2022 Review - Cash Flow Is King