SHYF - The Shyft Group: Great Long-Term Upside Potential But Short-Term Risks Remain

2024-01-19 10:43:41 ET

Summary

- Revenues have declined significantly for three consecutive quarters as demand is stabilizing after a strong 2021 and 2022.

- Profit margins are suffering due to weaker volumes and inflationary pressures.

- The balance sheet is very strong thanks to very high inventories and receivables.

- The company doubled the dividend payout in 2022 and it remains safe despite current headwinds.

- This represents a good opportunity for long-term dividend investors, as well as for those investors interested in obtaining significant capital gains once prospects improve again.

Investment thesis

After an impressive 2021 and 2022 due to high consumer demand in the e-commerce space as a result of self-imposed restrictions to stop the spread of the coronavirus, which pushed delivery companies to increase their fleet of vehicles, The Shyft Group ( SHYF ) is currently suffering a (negative) rebound effect on its operating results due to the complete return to normality as delivery companies are cutting expenses due to excess vehicle units, higher transportation costs, inflationary pressures, and weaker demand. For Shyft, these headwinds have translated into lower revenues, more moderate growth expectations for the medium term, and tighter profit margins. If we add to this the current strict financing environment for customers and consumers, as well as higher interest expenses for the company, it is understandable that expectations regarding Shyft have worsened so much in recent quarters causing an 80% decline from all-time highs reached in 2021.

Furthermore, investors should keep in mind that vehicle repair and the replacement of their parts in times of economic uncertainty tend to be postponed as much as possible by consumers and companies, and this also applies to recreational vehicles given that many consumers are experiencing weakening purchasing power as a result of high inflation rates at a time when they are offered unfavorable financing conditions.

But even so, I believe that the company has a balance sheet robust enough to withstand the current headwinds for a long time and that current efforts to enter the electric vehicle market will mark the growth path in the future, which is why I believe that the current pessimism among investors represents a good opportunity for those long-term dividend investors with enough patience and risk tolerance to wait for the company's landscape to improve, as well as for those investors interested in obtaining significant capital gains.

A brief overview of the company

The Shyft Group is a North American company focused on specialty vehicle manufacturing and assembly for the commercial and recreational automotive industries. The company was founded in 1975 and was formerly known as Spartan Motors before the divestment of its Emergency Response business in 2020 when it changed its name to The Shyft Group in 2020. Its market cap currently stands at $371 million as it employs over 3,500 workers.

The Shyft Group logo (Annual Report (2022))

The company operates under two main business segments: Fleet Vehicles and Services, and Specialty Vehicles. Under the Fleet Vehicles and Services segment, which provided 63% of overall revenues in 2022, the company manufactures commercial vehicles under its Utilimaster brand, as well as vocation-specific equipment upfit services and aftermarket replacement parts and accessories. On the other hand, under the Specialty Services segment, which provided 37% of revenues in 2022, the company manufactures luxury Class A diesel motorhome chassis, service bodies, contract assembly of specialty (and other) vehicles, vocation-specific equipment upfit services, and replacement parts and accessories.

Given the nature of the industry in which it operates, Shyft is a highly cyclical company, which is reflected in its historical share price chart. In this regard, there are, in my opinion, two optimal approaches for investors: one can acquire shares in times of high uncertainty to achieve higher than average dividend yields on cost for the long term, or acquire shares to sell them once optimism reigns again in the market to achieve capital returns (and collect some dividends along the way).

Currently, shares are trading at $10.81, which represents an 80.17% decline from all-time highs of $54.50 reached on November 18, 2020. After significant acquisitions in recent years, expansionary efforts, and efficiency-focused investments, the company announced in 2022 its intentions to penetrate the fully electric commercial vehicle market through the development of Blue Arc, which will be its brand of completely electric vehicles for commercial purposes. Despite this, the company has yet to demonstrate its ability to introduce the brand to the market, and it must do so in a delicate and complex macroeconomic environment marked by multiple headwinds for Shyft and with a new CEO at the helm since October 2023.

Recent acquisitions and divestitures

Although the company has always strived to achieve organic growth, the management has always been willing to expand its reach through acquisitions. Nevertheless, it has always done so fairly conservatively as it has always kept debt at low levels.

In January 2017, the company acquired Smeal Fire Apparatus Company , which manufactures and distributes emergency response vehicle bodies and aerial devices for the fire service industry, for $36.3 million. It had been indeed a long time since the company engaged in M&A activities as the previous acquisition took place in April 2011 when it acquired Classic Fire , a manufacturer of fire truck bodies and firefighting apparatus, for ~$4.7 million.

Almost two years later, in December 2018, the company acquired Strobes-R-Us , a provider of up-fit services, for $5.2 million, and almost a year later, in September 2019, it acquired Fortress Resources (doing business as Royal Truck Body), a leading California-based designer, manufacturer, and installer of service truck bodies and accessories, for $89 million.

Finally, in February 2020, the company divested its Emergency Response and Vehicle business for $55 million to focus on the e-commerce, specialty, and EV markets, as well as on autonomous technologies. Following the divestment, in October 2020, the company acquired F3 MFG , a leading aluminum truck body and accessory manufacturer, for $17.3 million. The acquired company reported annual revenues of $25 million at the time of the purchase as it reported a CAGR growth of 74% in the 2015-2019 period, so it has the potential to provide significant revenue growth for Shyft in the coming years.

As for more recent times, in January 2023, the company acquired XL Fleet intending to use its assets, including talent, to boost innovation efforts for the deployment of its Blue Arc brand.

All of these acquisitions (as well as the emergency response divestment) allowed the company to achieve very acceptable growth rates over the years and maintain a healthy profitability profile, and the management currently keeps looking for new M&A opportunities as the balance sheet remains strong thanks to relatively low debt and very high inventories and receivables.

Revenues have taken a strong hit in 2023 and the recovery will most likely be very gradual

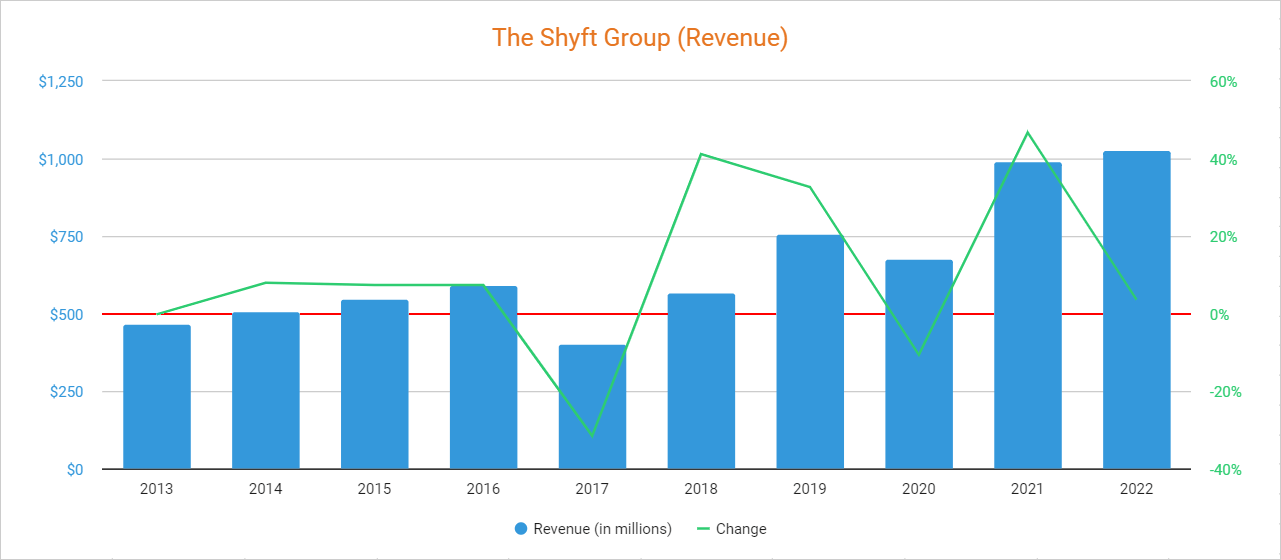

The company achieved very acceptable revenue growth rates in the 2018-2022 period thanks to acquisitions, higher capital expenditures, and strong demand for recreational and parcel delivery vehicles during the reopening of the economy in 2021 after the coronavirus pandemic crisis as consumers chose to buy products in the e-commerce space to avoid visiting public places as much as possible, but the total return to normality has caused demand for the products the company manufactures to drop drastically in 2023 as customers already acquired more units than usual in 2021 to meet their increased demand.

{kind=link}

The Shyft Group revenue (Seeking Alpha)

In this regard, revenues increased by 17.67% year over year in Q1 2023 but decreased by 3.06% year over year in Q2 and by 29.63% in Q3 as a consequence of declining demand for recreational and parcel delivery vehicles. Also, inflationary pressures and recessionary concerns have caused many consumers to postpone the purchase and repair of recreational vehicles, and supply chain issues related to a key battery provider are slowing the plans for the Blue Arc brand, the company's upcoming fully electric last-mile parcel delivery vehicle. We must also not forget that consumers have changed their consumption habits and are currently leaning more toward the consumption of services, which is why the e-commerce industry is suffering. In this regard, 2023 is expected to close with a total revenue decline of 16%, but the decline is expected to stabilize in 2024 as revenues are expected to increase by 3.8% compared to 2023.

As for current measures to drive growth in 2024 and beyond through the introduction of its Blue Arc brand into the market, the company is currently focused on finding new battery suppliers to avoid the same issues from repeating in the future, but battery scarcity is expected to continue representing a headwind in the short term.

The recent revenue decline and expectations of a very progressive recovery from 2024 caused a sharp drop in the P/S ratio to 0.391, which means the company currently generates $2.56 in revenues for each dollar held in shares by investors, annually.

This ratio is 50.94% lower than the average of the past 10 years and represents an 82.41% decline from decade-highs of 2.223 reached during the second half of 2021, which means that investors are placing less value on the company's revenues as the backlog in Q3 2023 was $464.4 million, which represented a 55.5% decline from $1.04 billion in the same quarter of 2022, and an 8.98% decline quarter over quarter. In this regard, revenues are expected to remain weak in the foreseeable future.

Still, revenue struggles are not the only problem that has led investors to have a very pessimistic sentiment toward Shyft as declining volumes and inflationary pressures are currently putting significant pressure on profit margins.

Margin contraction is not a cause for (significant) concern

Before the outbreak of the coronavirus pandemic, the company was focusing on the expansion of its most profitable businesses and the acquisition of new ones, and also made significant investments in its facilities to improve manufacturing capacity and achieve operational efficiencies. Also, it divested its emergency response business in 2020 to correctly align operations in the segments with the greatest potential for long-term growth and profitability. These efforts paid off as the company experienced significant margin expansion in the 2016-2020 period, and 2021 saw a further dramatic improvement in margins as volumes increased due to increased demand for products in the e-commerce space.

As of recent quarters, inflationary pressures, supply chain issues, and more recently decreased volumes are negatively impacting the company's profitability as trailing twelve months' gross profit margins decreased to 18.60%, whereas the EBITDA margin declined to 5.62%.

Furthermore, profit margins have continued deteriorating in the third quarter of 2023 as the company reported a gross profit margin of 18.26% and an EBITDA margin of 4.20% as the volume decline was very significant. To cushion the impact that inflationary pressures and weak volumes are having on the company's operations, the management is currently implementing cost-control actions, but I deduce that we won't see a significant recovery until demand (and therefore volumes) normalizes, inflationary pressures relax even more, and supply chain issues related to batteries are resolved (so that the company can accelerate the introduction of Blue Arc to the market). Still, the company is holding on quite resiliently as it reported positive net income quarter after quarter in 2023.

For this reason, and taking into account that the company has also reported positive cash from operations during all quarters of 2023, I consider that the current margin contraction is not a cause for alarm since most of the current headwinds are, in my opinion, of a temporary nature due to their direct link to the current macroeconomic landscape. Furthermore, the company enjoys a very strong balance sheet, which suggests that it can withstand current (and even worse) headwinds for a very long time.

The balance sheet is very robust

The company currently holds $84.67 million in long-term debt as a result of the acquisitions that have taken place in recent years, as well as higher capital expenditures and recent inventory buildup and share buybacks.

Still, this debt is currently not a problem as inventories have increased significantly since 2020 to $115 million. Furthermore, total receivables of $169 million are well above accounts payable of $99 million, and the company still has $9.88 million in cash and equivalents. Such high inventories and receivables suggest that the company should be able to withstand current headwinds for a long time and continue generating strong cash from operations in the coming quarters, which should allow it to reduce current debt levels or continue financing the development of Blue Arc and new potential acquisitions.

In this regard, the company generated cash from operations of $70.5 million in the past 12 months thanks to the conversion of receivables into cash and expects cash from operations to continue strong as it planned to keep reducing working capital in Q4. This should give the management enough resources to manage current debt levels, which is very important as trailing twelve months' total interest expenses increased to $5.78 million in Q3.

Furthermore, total interest expenses in Q3 were $1.57 million, which means the company is expected to pay over $6 million every year at current debt levels and interest rates, and we must add an increased dividend as the management doubled the payout in 2022.

The increased dividend remains safe

The company used to pay two semi-annual dividends of $0.05 per share, which became four quarterly dividends of $0.025 in 2020 (the annual dividend payout remained static at $0.10). In 2022, the quarterly dividend was raised by 100% to $0.05 per quarter, raising the annual payout to $0.20 per share.

This has caused a significant increase in dividends paid, which went from $3.6 million in 2021 to $7.1 million in 2022. Still, the company has historically reported cash from operations significantly above the current annual dividend payout, so covering this dividend should not be a problem in the long term.

In the table below, I have calculated the cash payout ratio for recent years by determining the percentage of cash from operations used to cover dividends paid and interest expenses. In this way, we can get an idea of the company's ability to cover these two expenses through actual operations.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $6.5 |

| $12.9 |

| $23.3 |

| $22.0 |

| $8.0 |

| $34.2 |

| $64.3 |

| $74.0 |

| -$18.8 |

| Dividends paid (in millions) |

| $3.4 |

| $3.4 |

| $3.4 |

| $3.5 |

| $3.5 |

| $3.6 |

| $3.6 |

| $3.6 |

| $7.1 |

| Interest expense (in millions) |

| $0.3 |

| $0.4 |

| $0.4 |

| $0.1 |

| $1.1 |

| $1.8 |

| $1.3 |

| $0.4 |

| $2.8 |

| Cash payout ratio |

| 57% |

| 29% |

| 16% |

| 16% |

| 58% |

| 16% |

| 8% |

| 5% |

| - |

As one can see, the management has historically been quite conservative when it comes to dividend payouts as the cash payout ratio has rarely exceeded 50%. While it is true that cash from operations was negative in 2022 at -$18.8 million, it is important to highlight that inventories increased by $33 million and accounts receivable by $94 million, while accounts payable increased to a lesser extent by $41.9 million as the company reported a net income of $36.6 million.

During the third quarter of 2023, the company reported $9.2 million in cash from operations, whereas inventories increased by $13.9 million and accounts receivable by $5.3 million, but accounts payable also increased by $13.6 million, and the company reported net income of $4.5 million (compared to $17.3 million in the same quarter of 2022). Taking these numbers into account, the company should be able to keep covering quarterly dividends paid of $1.7 million, interest expenses of $1.6 million, and even capital expenditures of slightly over $5.2 million (also per quarter) through operations themselves.

For these reasons, I believe that the current dividend is safe, and the recent share price decline left a dividend yield on cost of ~1.85%, which is a good opportunity for long-term dividend investors as the cash payout ratio has historically been pretty low, so the company should be able to continue investing in its business in the long term.

Share buybacks are undoing share dilution of recent years

In 2020, the management began repurchasing shares as the total number of shares outstanding has decreased by 3.60% since then. This has been possible as the company spent $7.5 million in share buybacks in 2020, $3.3 million in 2021, $26.8 million in 2022, and $19.1 million in the first 9 months of 2023.

This means that each share now represents a bigger portion of the company compared to 2020, which essentially undid the share dilution that happened in the 2016-2019 period. Furthermore, share buybacks are expected to continue in the foreseeable future as the company repurchased $10.3 million worth of shares in Q3. This leaves $223 million left in the share repurchase authorization, which has the potential to significantly reduce the total number of shares outstanding as the current market capitalization stands at $371 million. Despite this, the management has made it clear that they do not intend for share buybacks to be the only capital allocation, and that they will pause them if opportunities emerge that could provide growth for the company. In this regard, while I expect share buybacks to continue in the future, they will most likely be performed carefully depending on the company's situation at every moment.

Risks worth mentioning

While it is true that the recent share price decline greatly reduced risks for investors as so many headwinds and potential risks are already priced in, there are certain risks that I would like to highlight.

- Recent interest rate hikes could trigger a recession, which could cause an additional decrease in sales, as well as a further margin contraction due to lower volumes.

- Although the commercial EV is an industry with a lot of growth potential for the coming years, this does not mean that Shyft is going to successfully introduce its brand to the market.

- The company operates for a highly competitive industry formed by companies that continually seek to optimize their operations in order to reduce their costs as much as possible. Therefore, demand for Shyft products could be seriously affected if it fails to adapt its products to changes in their needs.

- The company could reduce the dividend if current headwinds last for longer than expected or if they worsen. The same applies to share buybacks.

- We are currently living in very tumultuous times for highly cyclical companies like Shyft, so the share price could continue to fall. In fact, some further share price declines should be expected in the short term for any investor investing in cyclical companies during difficult times.

Conclusion

Times are not easy for Shyft. After two extraordinarily good years thanks to higher-than-usual demand in the e-commerce and parcel delivery industry due to self-imposed restrictions to stop the spread of the coronavirus pandemic, the company is suffering an aftermath in which inflationary pressures are reducing consumer's purchasing power at a time in which delivery companies find themselves with excess units and cost-cutting policies. Furthermore, after the coronavirus pandemic, consumers have changed their consumption habits and currently prefer to consume services instead of goods.

As a consequence, revenues have declined for three consecutive quarters, and profit margins are suffering due to lower volumes and inflationary pressures. Furthermore, supply chain issues are putting an obstacle in the way of introducing Blue Arc to the market while capital expenditures remain high and interest expenses continue to increase due to higher debt exposure and interest rates. For these reasons, the share price has decreased by 80% from all-time highs reached as recently as in 2021.

Still, I believe that the recent share price decline represents a good opportunity for those investors with enough patience to wait for the company's prospects to improve, and also for those long-term dividend investors interested in enjoying a higher-than-usual dividend yield on cost as the historical cash payout ratio has been pretty low, which means the company has the potential to keep investing in growth once current headwinds ease.

The balance sheet is very strong thanks to very high inventories and receivables, and long-term debt should not be an issue as it is at low levels in comparison. Furthermore, the company remains profitable in the current landscape as it reported net income quarter after quarter in 2023, and current headwinds are, in my opinion, of a temporary nature due to their direct link with the current macroeconomic landscape. In the meantime, the company keeps executing its plan to enter the EV commercial vehicle market, which should pave the way for future growth in the long-term.

For further details see:

The Shyft Group: Great Long-Term Upside Potential, But Short-Term Risks Remain